Федеральная резервная система вливала около $37 млрд в банковскую систему США с прошлого пятницы.

Несмотря на такое значительное вливание капитала, настроения инвесторов в криптовалютных рынках упали до уровня крайнего страха. Крупнейшие активы демонстрируют резкие снижения, а общая капитализация сектора снизилась на 6,11% в этом месяце.

Ликвидность поступает, а цены падают: объяснение разрыва между ФРС и криптовалютой

Согласно последним данным, 3 ноября Федеральная резервная система провела дополнительные операции репо на сумму $7,75 млрд. Этот шаг был предпринят вскоре после того, как в пятницу ФРС добавила $29,4 млрд в банковскую систему.

Это было крупнейшее однодневное вливание ликвидности с эпохи доткомов. В совокупности сумма ликвидных вливаний составила около $37 млрд.

«Это самое крупное печатание денег за последние 5 лет. Рынок криптовалют готовится к параболическому росту», — написал Алекс Мейсон в своем сообщении.

Помимо казначейских облигаций, ФРС также влила $14,25 млрд в ликвидность через операции репо, обеспеченные ипотечными ценными бумагами в тот же день.

Когда Федеральная резервная система увеличивает ликвидность, это означает, что в финансовой системе обращается больше наличных средств. Банки и учреждения получают дополнительный капитал, который может быть направлен в более рисковые активы, такие как акции и криптовалюты. Теоретически, эта дополнительная ликвидность поддерживает рост цен.

«Все говорят о медвежьем рынке в самый неподходящий момент. Глобальная ликвидность готова выстрелить: поступления от репо ФРС, открытие шлюзов TGA, волна стимулирующих мер в Азии, смягчение кредитных условий. Весь этот цикл проходил без ликвидности. Поэтому только биткоин достиг новых высот. Когда ликвидность вернется, альткоины оживут. Макроэкономическая ситуация заряжена», — отметил Merlijn The Trader в своем комментарии.

Тем не менее, несмотря на недавнее увеличение ликвидности, криптовалютные рынки пока не ощутили положительного эффекта. Более того, настроения резко ухудшились.

Причины падения крипторынка во время вливания ликвидности ФРС

Читайте также: У биткоина всего два года, чтобы защититься от квантового взлома – статья от BeInCrypto

Индекс страха и жадности крипторынка упал до отметки 21, что указывает на «Экстремальный страх». Это самый низкий показатель с апреля 2025 года, снизившись с нейтрального уровня 50 всего за неделю.

Кроме того, наблюдается снижение цен на активы. Биткоин (BTC) потерял почти 5% в ноябре, в то время как Ethereum (ETH) упал почти на 9% за тот же период.

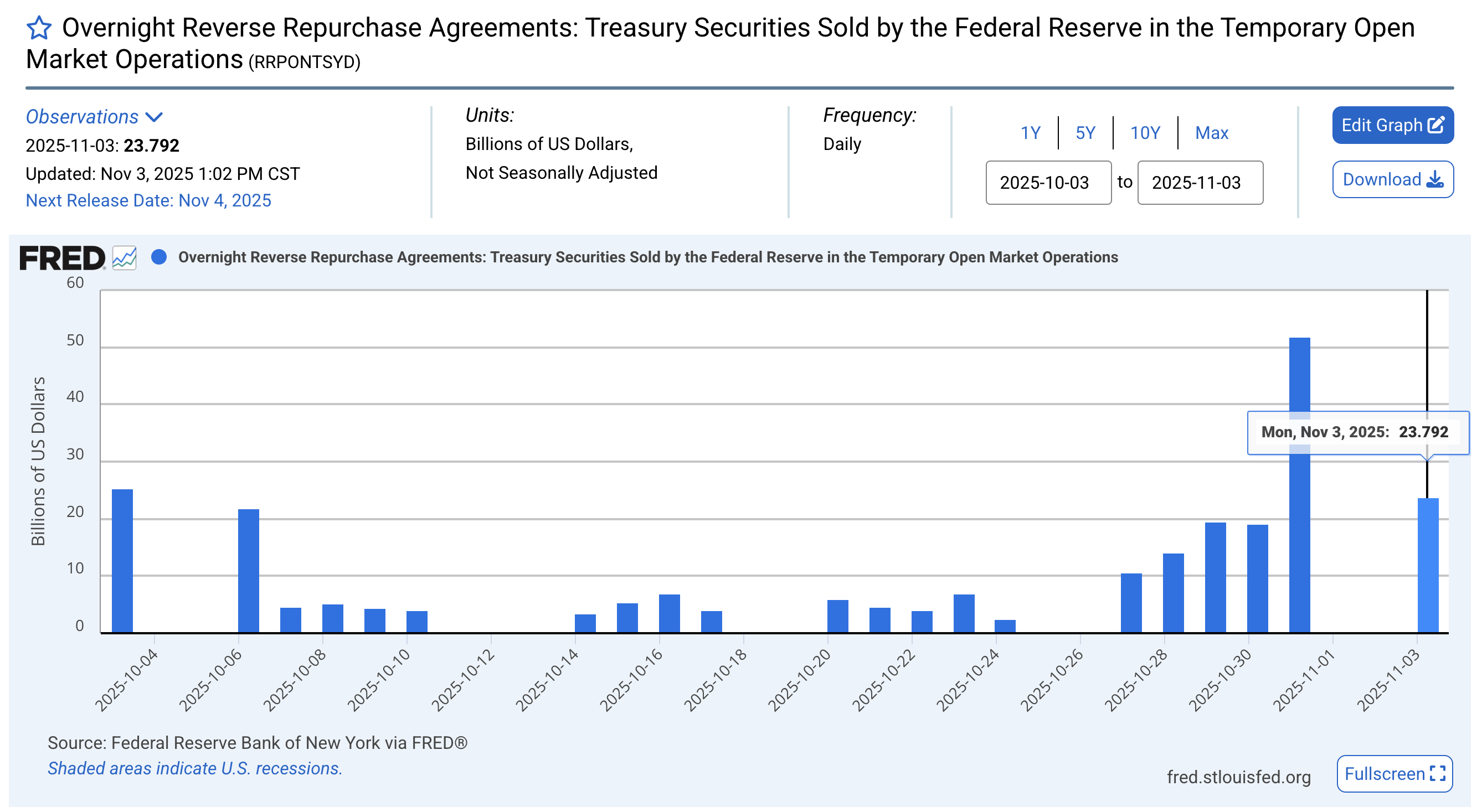

Эта ситуация может быть связана с операциями обратного РЕПО Федеральной резервной системы. Согласно последним данным, с прошлой пятницы центральный банк провел обратные РЕПО более чем на $75 млрд, включая почти $24 млрд только 3 ноября.

В отличие от операций РЕПО, которые вводят ликвидность в финансовую систему, обратные РЕПО выводят наличность. В этих транзакциях Федеральный резерв берет деньги в долг у банков и фондов денежного рынка в обмен на казначейские облигации в качестве залога. Это фактически изымает ликвидность из обращения, ужесточая условия краткосрочного финансирования.

Резкий рост использования обратных РЕПО говорит о том, что финансовые учреждения ищут безопасности и паркуют излишки наличности в ФРС вместо того, чтобы вкладывать их на рынок. Эти смешанные сигналы — вклады через РЕПО, но одновременное изъятие ликвидности через обратные РЕПО — подчеркивают неопределенность в финансовой системе.

Для рискованных активов, таких как криптовалюта, это динамическое взаимодействие объясняет, почему рынки остаются волатильными: несмотря на новые вливания ликвидности, общее состояние все еще ощущается как жесткое, что держит инвесторов в напряжении.