Ethereum [ETH] concluded June with a 27% bearish push in the last five days of the month after enjoying a brief relief rally. The bearish end of June resulted in the token dropping below $1,000, followed by a pullback. Could this be a sign of a strong buy wall within the $1,000 price level?

June was one of the most bearish months for ETH in recent history. It dropped from a monthly high of $1,972 at the start of the month, to a monthly low of $881 on 18 June. ETH fell below $1,000 twice in the same month. Both instances yielded a quick recovery back above the same price level.

Source: TradingView

ETH’s end-of-June performance reveals that the price had a higher low, while the RSI hovered just above the oversold zone. Furthermore, the MFI’s uptick, despite the sell-off, confirms that investors have been buying up ETH at lower prices.

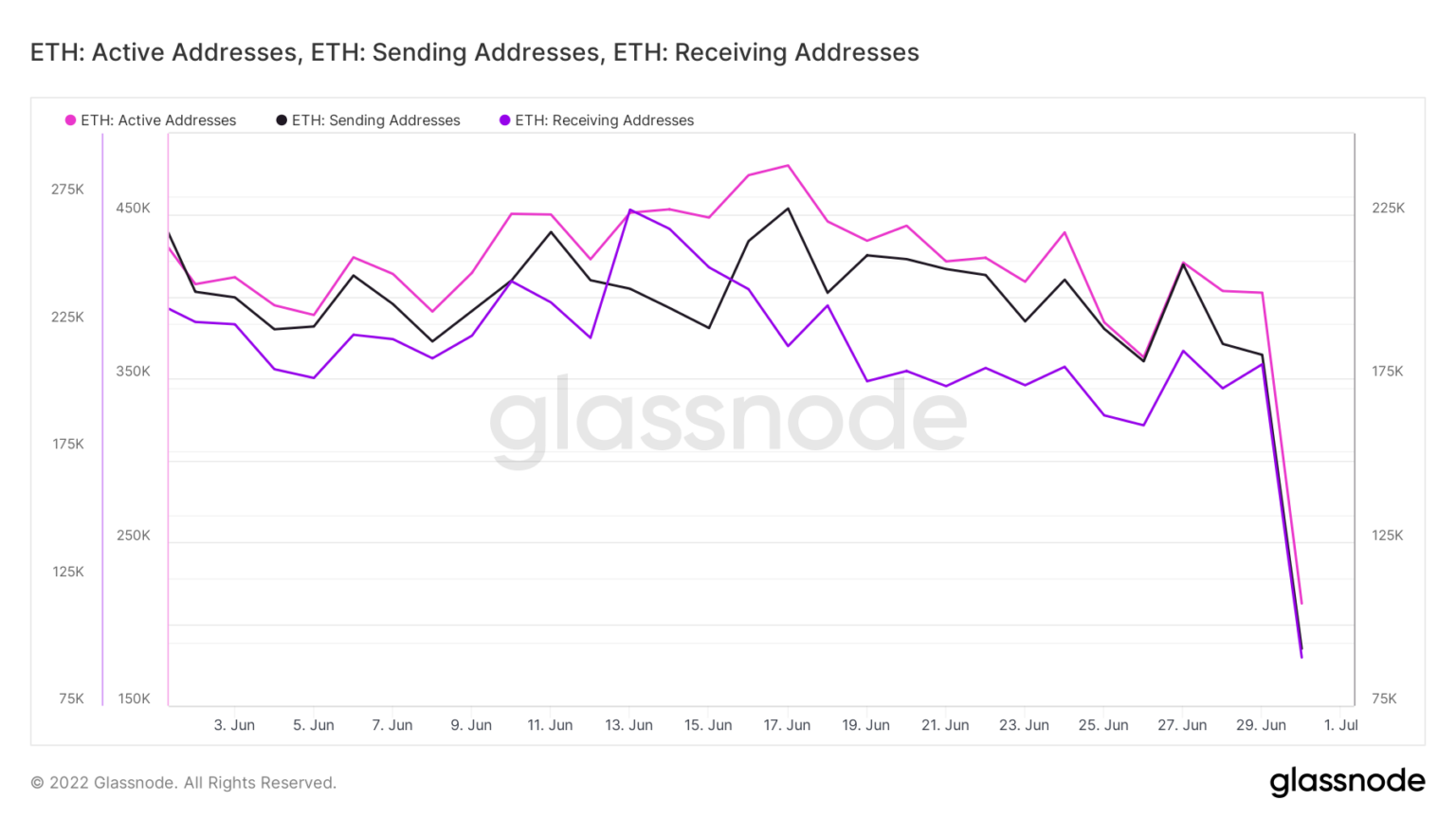

A look at ETH addresses confirms that accumulation outweighed the sell-off in the last 24 hours, resulting in strong support near $1,000. However, it also reveals that active addresses have reduced, reflecting the volatile market conditions.

Active addresses dropped sharply from 402,586 on 29 June to 212,569 on 30 June. Sending addresses (addresses offloading ETH) reduced from 182,304 to 92,459 during the same period.

Source: Glassnode

ETH’s receiving addresses dropped from 209,268 on 29 June to 94,002 on 30 June. However, the key point to note here is that receiving addresses slightly outweighed sending addresses in the last 24 hours. Even the whales have been buying the dip as indicated by the supply of the top 1% addresses metric. The latter registered a significant upside from 27 to 30 June.

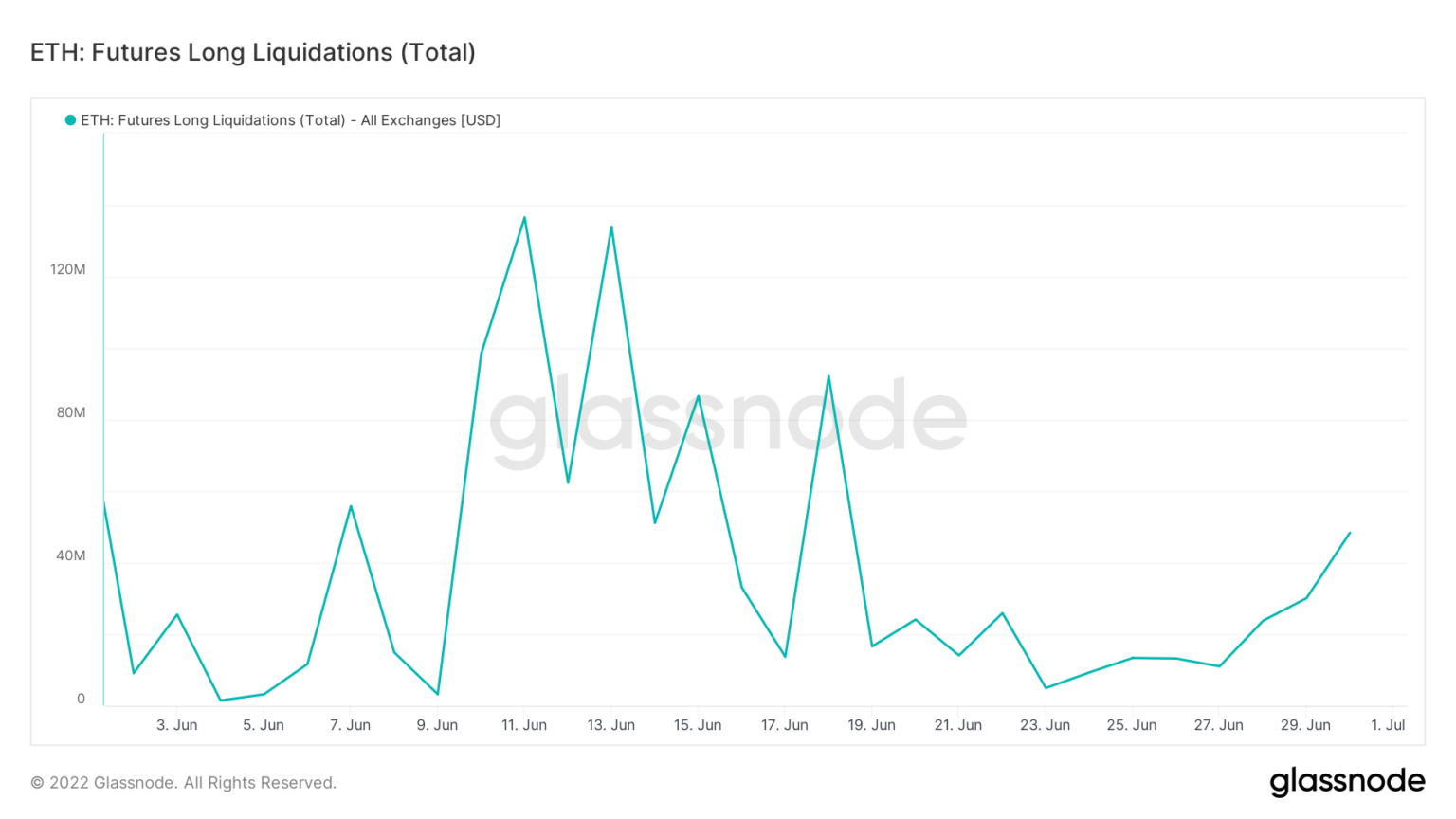

ETH’s last sell-off was characterized by heavy sell pressure coming from the liquidation of long positions. The previous three days of June resulted in an uptick in the number of liquidations from just over $11 million on 27 June to $48.37 million by 30 June.

Source: Glassnode

In contrast, the number of liquidations during ETH’s mid-June price crash peaked at $136.5 million. This means we can expect less selling pressure from the liquidation of leveraged long positions in the latest downside.

The futures long liquidations metric reveals why ETH’s latest sell-off was not as severe as the mid-June sell-off. Moreover, healthy accumulation has contributed to the higher lows. Now, it will be interesting to see how ETH will shape up in the first month of Q3.