Web3 用户增长平台 Layer3 宣布,截至 2024 财年度,Layer3 营收已正式突破 2,000 万美元大关,并稳健实现正向现金流与盈利能力。这一里程碑式表现,为当前高度竞争且尚处于成长期的加密产业树立了少见的商业化典范。

在大多数项目仍依赖代币激励与外部融资的背景下,Layer3 已率先建立可持续商业模式,并以企业级合作客户为基础,实现高速增长。其营收来源涵盖:协议端的导流任务合作、平台订阅服务,以及链上互动数据洞察。

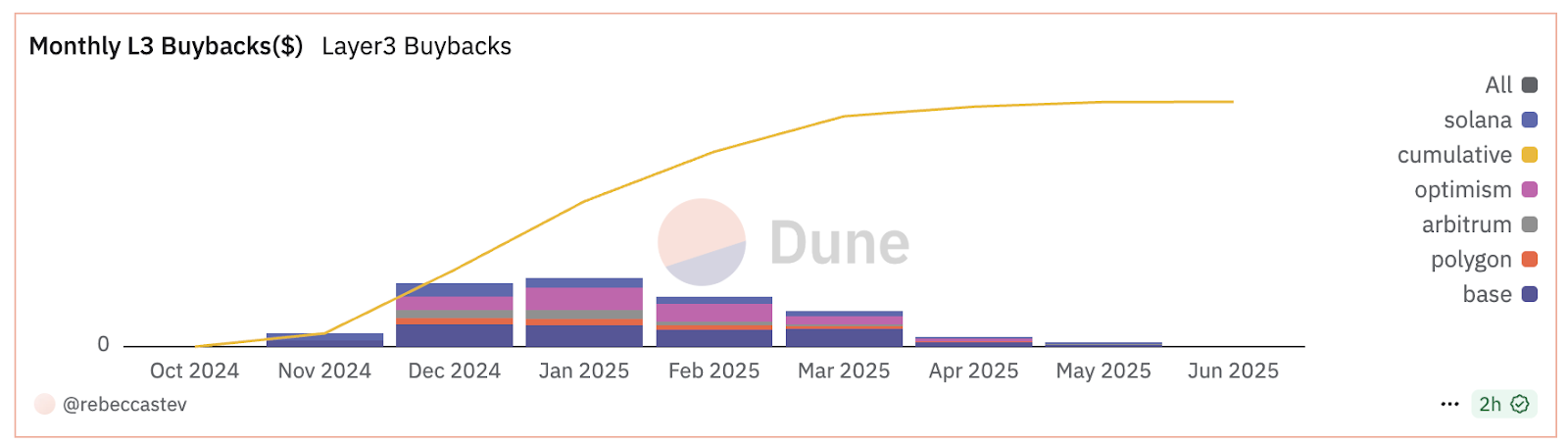

Dune图表展示了 L3 平台随时间推移收到的 L3 回购金额。该金额近 1,000,000 美元。

大规模代币回购,展现财务实力与长期承诺

Layer3 同时宣布,团队已完成一笔金额高达数百万美元的代币回购计划。此举不仅有助于优化代币流通供给,也再次强化市场对于 Layer3 团队承诺与执行力的信心。

该回购行动为市场提供坚实支持,有效提振社区情绪与中长期持币者的信任预期。

专注解决Web3用户增长问题

Layer3 的平台定位明确,旨在解决 Web3 项目面临的最大挑战之一:高质量用户获取与留存困难。Layer3 作为 Web3 的核心探索层,正在成为聚合用户、应用与多链生态的中枢引擎。平台是以太坊区块链上使用量第二高的 dApp,仅次于 Uniswap。平台已汇聚超 200 万用户,其中月活跃付费用户突破 3 万;更支持 760+ 个热门协议,无缝集成 40+ 条主流区块链。像 Google 一样,Layer3 正在重塑全球用户探索与接纳加密技术的方式。

Layer3 是强劲的增长引擎 Linea、Jito Labs、Uniswap 等头部项目通过 Layer3 驱动用户增长与忠诚度,案例; Linea 实现 6 周突破 100 万用户,Jito Labs 用户留存率超 70%。

平台通过结构化任务系统(Mission)、链上行为追踪与激励模块,协助协议达成真实转化行为,例如:钱包链接、质押、跨链、治理投票等。企业客户可根据实际结果付费,实现高效率的链上用户增长。

合作伙伴遍布主流生态,技术与信任双重验证

目前,Layer3 已与多个顶尖生态系建立合作关系,包括:

• L2 公链与技术层: Mantle, Linea, Optimism、Arbitrum、Polygon、Base、Starknet

• 跨链基础设施: LayerZero、Axelar、Across

• 协议与应用层: Uniswap、Aave、Jito

这些合作多为长期、持续性导流计划,显示 Layer3 在用户增长策略中扮演的关键角色,并获得市场广泛认可。

展望亚洲市场,强化代币经济设计

Layer3 已着手启动面向亚洲区的策略推进,包含:

• 地区专属任务模块

• 本地化合作推广活动

• 与亚洲链与社区建立策略联盟

平台代币 $L3 将持续在任务激励、参与门槛、声誉积分与 DAO 治理等方面发挥核心作用。团队也预计推出包括质押奖励、代币销毁机制等价值捕捉设计,以建立更健康的代币经济循环。

Co-founder 库马尔表示: 「我们正在证明:加密世界既能坚守使命,亦可实现财务稳健,我们的盈利模式,正是实用价值可规模化落地的有力佐证。」

Layer3 将继续以稳健营收为基础,强化全球化布局,并通过可持续的代币模型与任务平台设计,为Web3的长期用户增长提供最可信赖的基础设施。