原文作者:Scof,ChainCatcher

原文编辑:TB,ChainCatcher

近日,Strategy(前称 MicroStrategy)正式向美国证券交易委员会提交文件,计划发行最高 210 亿美元的 8% 系列 A 永续优先股。这一举措引发市场关注,因为它不仅涉及大规模资金筹集,还可能对 Strategy 的比特币购买策略带来深远影响。

据官方文件披露,这些优先股每股面值 100 美元,年化利率为 8% ,每季度支付股息,支付形式可为现金、普通股或两者结合。此外,优先股可按 10: 1 的比例转换为普通股,即每 10 股优先股可转换为 1 股普通股。

此次优先股发行将采用“市场发行计划”模式,即公司可直接在市场上出售优先股,类似于普通股的 ATM 发行。这意味着,Strategy 现已同时拥有普通股和优先股的 ATM 融资渠道。

那么这次优先股的发行与以往有什么不同?这一创新的融资方式是否会为比特币市场带来新的变数?本文将对此做出深入解读。

Strategy 融资方式的演变

在分析 Strategy 最新的融资方式之前,先简单回顾一下其过往购买比特币的方式。

早期阶段,Strategy 作为一家软件公司,使用账面上的闲置现金购入比特币。这个阶段的最初三笔投资买入了 40, 700 枚比特币。

随着公司对比特币的投入加大,他们开始利用可转换优先债券(可转债)进行融资。可转债允许投资者在特定条件下将债券转换为公司股票,既提供了下行保护(债券到期可收回本金和利息),也提供了股价上涨的潜在收益。这个方式买入了 119, 481 枚比特币。

除了可转债,Strategy 还曾发行优先担保债券,这是一种有抵押的债务工具,比可转债风险更低,但收益模式更固定。利用该模式融资,公司买入了 13, 005 枚比特币

随着 MSTR 股价的上涨,从 2021 年开始,公司更多地采用市价股票发行(ATM)方式进行融资。ATM 是一种在美国广泛使用的融资方式,这允许上市公司在公开市场上以当前市场价格直接发行新股,以筹集资金。

而在今年的 2 月 20 日,Strategy 发行了 20 亿美元的可转化优先票据,这种融资方式所需的审查过程比以往更复杂也更耗时,因此当时市场推测 Strategy 购买 BTC 的速度将减慢。

但此次提交审核的 210 亿美元永续优先股又重新让市场对 Strategy 回到“买买买”模式的期待值拉满。

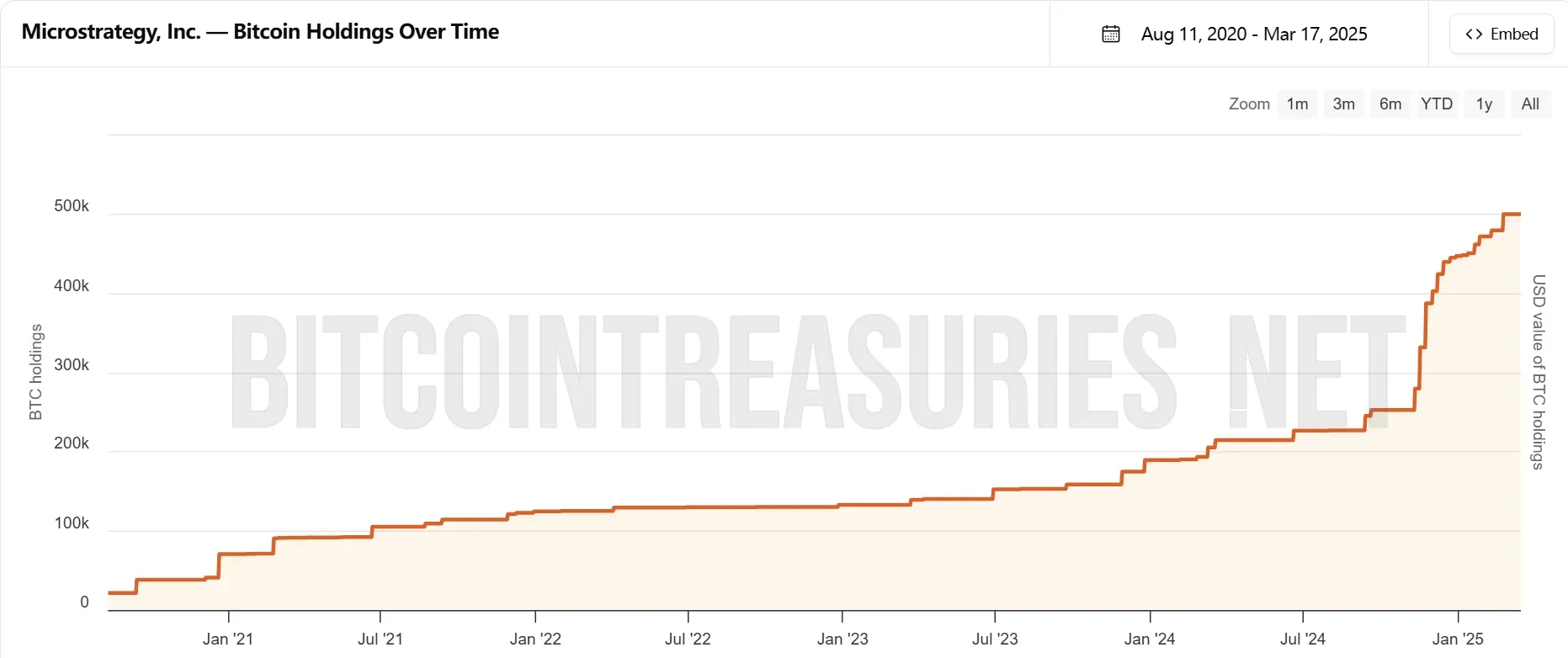

Strategy 持有的 BTC 数量。来源:bitcointreasuries.net

优先股有何不同?

与以往的融资方式相比,Strategy 此次申请的永续优先股在结构上有明显不同。过去,公司主要依靠债务融资和股票增发来获取资金,而这次的优先股发行,则在传统股权融资与债务融资之间找到了一种新的平衡。

优先股与普通股最大的区别在于,它既不完全依赖公司业绩,也无固定到期日和还本要求。它更像是一种“介于两者之间”的金融工具,持有人可以定期获得固定的股息收益,同时在特定条件下转换为普通股。

对于 Strategy 而言,这意味着它可以通过增发优先股持续筹集资金,而无需承担传统债务融资的到期偿还压力。相比于此前发行的可转债和优先担保债券,这种融资方式提供了更大的灵活性,也降低了短期财务负担。

当然,这一模式并非没有代价。优先股的年化利率设定为 8% ,相比 Strategy 过去发行的 0% -0.75% 的可转债以及 6.125% 的优先担保债券,融资成本显然更高。市场对此的核心疑问在于,公司如何支付这笔不小的股息成本。

分析师推测,Strategy 可能通过 ATM 增发普通股弥补资金缺口,甚至直接用新增股票支付股息。这种模式虽然让公司能够短时间内筹资,但也可能带来普通股股东权益被稀释的问题。

是下注的好时机吗?

若 Strategy 的永续优先股获批,无疑将会为比特币市场带来新的动力。

简单来说,这种优先股相当于公司找了一种更灵活、更持久的方式来融资,而这些钱最终会用于买入比特币。

相比过去发行债券或直接卖股票筹钱,永续优先股没有固定的到期日,公司可以一直用它来融资,不需要像还债一样定期归还本金。同时,由于这次的优先股采用了类似普通股增发的模式,Strategy 可以随时根据市场情况出售优先股筹集资金,而不需要像债券融资那样等待审批或寻找特定投资人。

这意味着,Strategy 未来买比特币的速度可能会变快,甚至可以更加稳定地持续买入。

但在目前这样低迷的行情下,启动这样一个较为激进的融资方式是否合适?

高盛高级分析师 James Carter 表示,“Strategy 的 210 亿美元优先股发行计划显示了塞勒对比特币的极度乐观,但在当前市场低迷环境下,如此高杠杆操作可能加剧波动风险。”

花旗集团的金融科技研究员 Michael Evans 则认为,“在加密货币市场整体承压的背景下,Strategy 的选择显示了其对未来趋势的判断。若市场回暖,其回报可能惊人,但当前需关注资金流动及市场情绪变化。”

由于永续优先股融资结构复杂,SEC 审批可能耗时数月。ChainCatcher 编辑部将持续跟进进展。