Первая криптовалюта скоро вступит в «сезон безумия», в ходе которого котировки взлетят до $150 000 к концу 2024 года. Об этом заявил аналитик Real Vision Джейми Коуттс.

Unless something fundamentally has changed, we are entering what @RaoulGMI refers to as the 🍌zone, or what I would describe as #Bitcoin batshit season. pic.twitter.com/pMxk49ATtq

— Jamie Coutts CMT (@Jamie1Coutts) August 26, 2024

Специалист отметил перспективы вхождения цены в так называемую «банановую зону» — таким термином основатель и CEO фирмы Раулем Палом обозначает эйфорию. Это произойдет, «если ничего принципиально не изменится», добавил эксперт.

На графике Коуттс отметил, что в предыдущих двух бычьих циклах биткоин обновлял исторический максимум в течение 365 дней после прохождения пика индексом доллара США.

Согласно расчетам, при сохранении предыдущих моделей, рост цифрового золота может превысить 100% с $64 000 и достичь $150 000 к концу 2024 года.

CEO Trendstorm Филипп Свифт обратил внимание на возврат спотовой цены первой криптовалюты выше средней стоимости покупки краткосрочными инвесторами, что следует воспринимать как сигнал для продолжения восходящей динамики.

Back where we belong.$BTC now back above Short-Term Holder Realized Price, the cost basis of short-term investors. Bullish. pic.twitter.com/9EYt9FPlOU

— Philip Swift (@PositiveCrypto) August 26, 2024

Аргументы медведей

В CryptoQuant усомнились в реализации бычьего сценария в ближайшее время ввиду активизации крупных медведей, ориентированных на краткосрочную перспективу.

Согласно наблюдениям аналитиков, на фоне ралли на предыдущей неделе, некоторые «застойные метрики» снова начали проявлять признаки оживления.

«Спекулянты с удержанием монет в диапазоне от недели до месяца перевели 33 155 BTC. Замедление роста цены говорит, что котировки способны перейти к свободному откату», — написали специалисты.

Эксперты предложили «проявлять особую осторожность» из-за рисков усиления потенциальной распродажи.

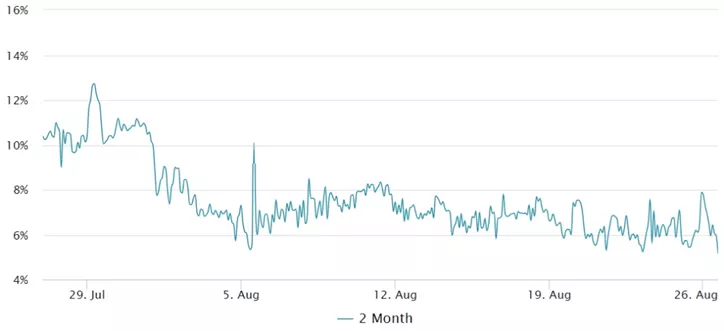

Рынок биткоин-фьючерсов также демонстрирует осторожность трейдеров. Премия по двухмесячным контрактам к спотовой цене в течение последнего месяца в пересчете на годовые темпы оставалась на уровне около 6%, отражая неготовность к наращиванию левериджа.

Напомним, в QCP Capital спрогнозировали, что курс первой криптовалюты останется в узком коридоре от $62 000 до $67 000 в ближайшей перспективе, о чем говорит нерешительность в опционах.

Ранее аналитики зафиксировали значительные покупки декабрьских коллов.