编译:深潮TechFlow

我对我们行业的未来充满信心,但我并不期待会出现像四年前那样的泡沫。我相信许多优质资产会在未来几年表现良好,因此我将所有资本都投入在这个预期上。然而,行业中存在一个奇怪的观念,即即使是毫无价值的资产,也应该在每四年交易时达到天文数字的估值。这种情况曾在2017年和2021年发生,因此有些人认为2025年也会如此。我认为这个观念是错误的,并且正在阻碍行业的发展。

我们可以将行业分为两种范式——基本面范式和周期性狂热范式。基本面范式意味着你相信行业的长期愿景,但不期待代币的交易价格会高于其内在价值。在这一范式下,投资者有动力与优秀团队合作,建立盈利的业务,而建设者则专注于产品、客户和业务的基本经济学。

相对而言,周期性狂热范式意味着投资者相信每四年就会出现一次泡沫,因此不再关注基本面。在这种情况下,投资者的自然动机是把握市场时机,尽可能多地投资于具有叙事价值的代币,而不必考虑团队是否在为长期发展而努力。

我认为,很多投资者仍然在周期性狂热范式下运作,这将导致他们在未来几年感到失望,因为基本面策略将表现良好,而叙事代币却可能表现不佳。市场上卖家过多,买家不足,难以重现2020年至2021年的情况。

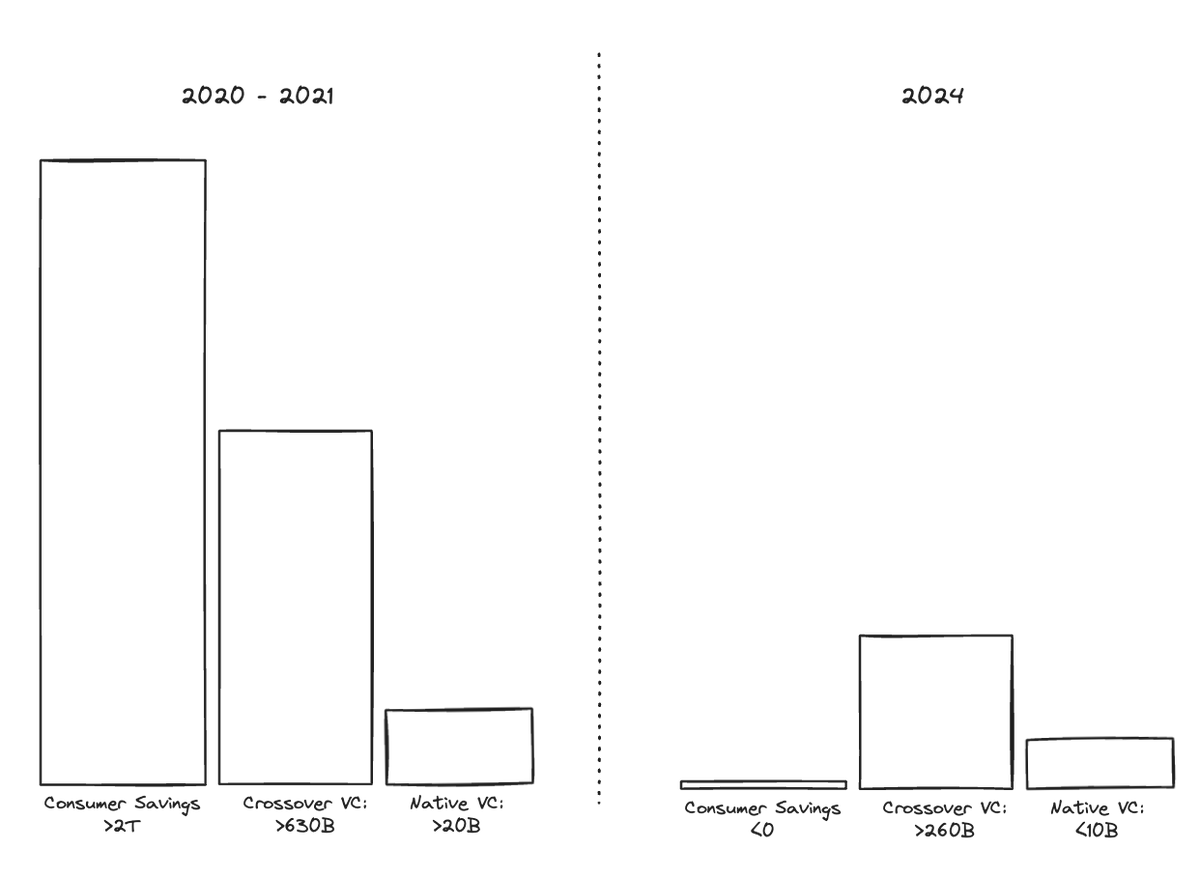

2021年我们经历了一次泡沫,原因在于多个缺乏弹性的买家在几乎没有供应的市场中相遇。当时,本土风险投资基金在2021年筹集了超过200亿美元,并迅速将这些资金投入市场。跨界基金在2020年至2021年期间筹集了6300亿美元,基于2010年至2020年科技牛市的十多年良好表现,并积极投资于加密货币。

普通市场充满了约8150亿美元的刺激支票,消费者对行业充满信心。由于BTC、ETH和SOL等资产价格的快速上涨,鲸鱼们也获得了1.5万亿美元的新资本。这些投资者相信行业会兑现其承诺,认为链上金融将在未来几年内颠覆高盛,并且到本十年中期,所有的业务都会建立在区块链上。

在这一需求面前,几乎没有卖家。只有创始人和少数早期风险投资者在这一时期持有大量代币,他们无法出售这些代币——部分是由于锁仓,部分是因为他们相信这个故事,并且有新资本可以投入。

市场资本化的逻辑是:如果90股被锁定,而10股以双倍于上次价格的价格交易,市场资本化就会假设所有股份的价格都翻了一番。因此,前一次泡沫中市场资本化的上涨,主要是由于太多买家从少数卖家那里购买了太少的代币。

今天市场的结构完全不同。对于本土基金来说,筹集新资本变得更加困难。2023年的筹资额下降了85%,而2024年几乎没有恢复(例如,Paradigm 在2024年以8亿美元结束筹资,而在2021年筹集了25亿美元)。跨界基金的回归将会缓慢,而普通市场基本消失,因为消费者储蓄从2021年的超过2万亿美元减少到2024年的负值。剩余的普通参与者更愿意投资于 meme 币,而不是复杂的基础设施叙事和嵌入的风险投资解锁。鲸鱼们的投资偏好也发生了变化,从叙事代币转向对使他们致富的核心资产(如 BTC、ETH 和 SOL)的收益。虽然有一小部分流动资金愿意购买代币,但与整体市场相比,它们的规模很小,而我们不想以高估值购买低质量资产。

谁会购买你的叙事代币?

市场上存在一种轻微的强迫卖家动态。在风险投资中,有两个核心收益指标——总价值支付比(Total Value to Paid-In, "TVPI")和分配支付比(Distributions Paid-In, "DPI")。TVPI 包括已售资产的实现收益和尚未出售但已增值资产的未实现收益。而 DPI 则是你为每一美元投资者投入的资金所返还的金额。

2019年之前筹集的风险投资基金在这两个指标上表现良好,但大多数收益仍然只是纸面上的。这些大型基金正进入法律上的生命周期结束阶段,这意味着他们需要出售剩余的持仓,以向基金投资者返还资本。2019年后筹集的风险投资基金仍然有充足的生命周期,但 DPI 的返还却不多(大多数情况下低于0.10x),而基金投资者在分配到下一个基金之前要求 DPI。行业中最大的单一持有者在未来几年似乎将成为净卖家。

2021年和2022年的基金有动机出售解锁,以展示 DPI 并筹集新资金。

在2023年底和2024年初,许多投资者试图提前布局另一波狂热,叙事代币的价格因此上涨。问题在于,大多数人购买的是他们并不相信的资产,希望其他人能以更高的价格从他们手中购买这些资产。这种愚蠢的资本并没有出现,市场拒绝了叙事代币进行适当牛市的尝试。这些买家不会出现,叙事代币在未来几年将继续表现不佳。

即使在强劲的势头下,也没有足够的买家来支撑一篮子叙事代币。

我们需要向基本面观点的范式转变。我们这些相信互联网金融系统基础愿景的人明白,我们仍处于资本主义历史上最大现金流机会之一的开端。你所需要做的就是努力工作,专注于基本面。

我希望我们的行业在2001年之后能更加像硅谷。过去几十年,整个行业蓬勃发展,这一切都源于努力工作、产品与市场的契合以及合理的风险评估。随着市场逐渐转向基于基本原则和经济学原理的估值,像“每次点击价格”(Price-to-Clicks)和“每只眼球价格”(Price-to-Eyeballs)这样的不切实际的估值方法逐渐失去了效用。在这个过程中,亚马逊、苹果和谷歌等公司成功地建立了全球最盈利的企业,几乎所有努力工作并专注于基本面的人都获得了成功。