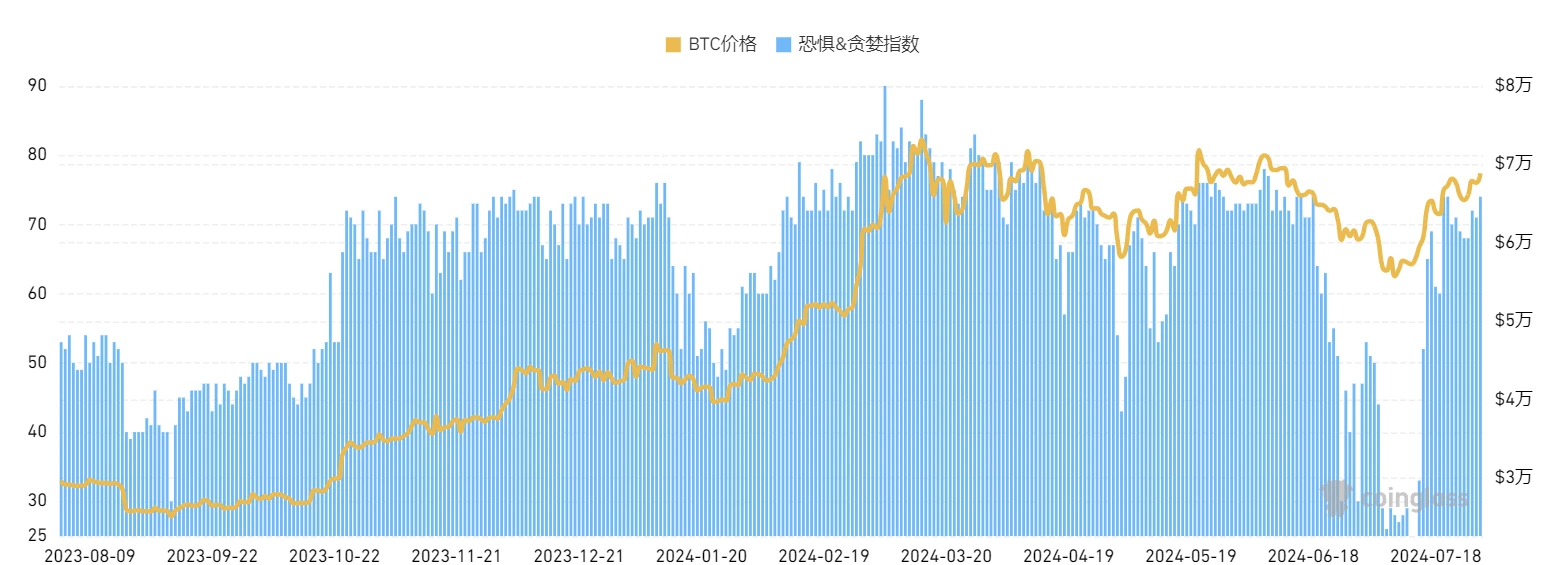

恐慌和贪婪指数

恐慌和贪婪指数现为 74 ,处于贪婪的位置,市场投资情绪较高。6 月下跌中,恐慌和贪婪指数出现较大幅度的下跌, 7 月初跌至 30 以下,是过于一年中最低的数值,之后出现了显著反弹。

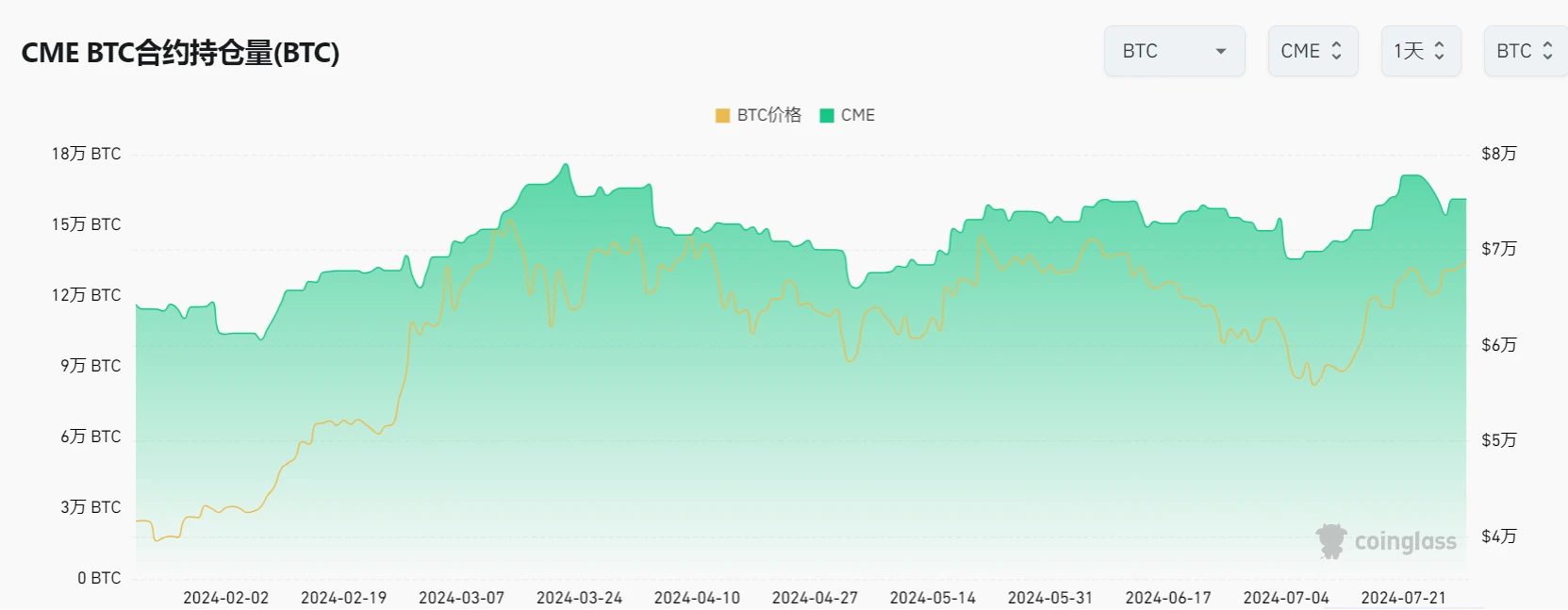

CME BTC 合约持仓

CME 持仓自 7 月 5 日以来出现连续增长,至 7 月 23 日开始有减仓, 7 月 28 日特朗普在比特币大会讲话后仓位又有所增长。

对应的逻辑变化是, 7 月 5 日之后资金看多市场, 7 月 23 日临近压力位以及比特币大会,部分卖事实资金减仓。特朗普讲话后,BTC 出现下跌,但快速反弹拉回,表明卖事实的资金引起的下跌有限,因此又有一部分资金看多后市,重新进场。

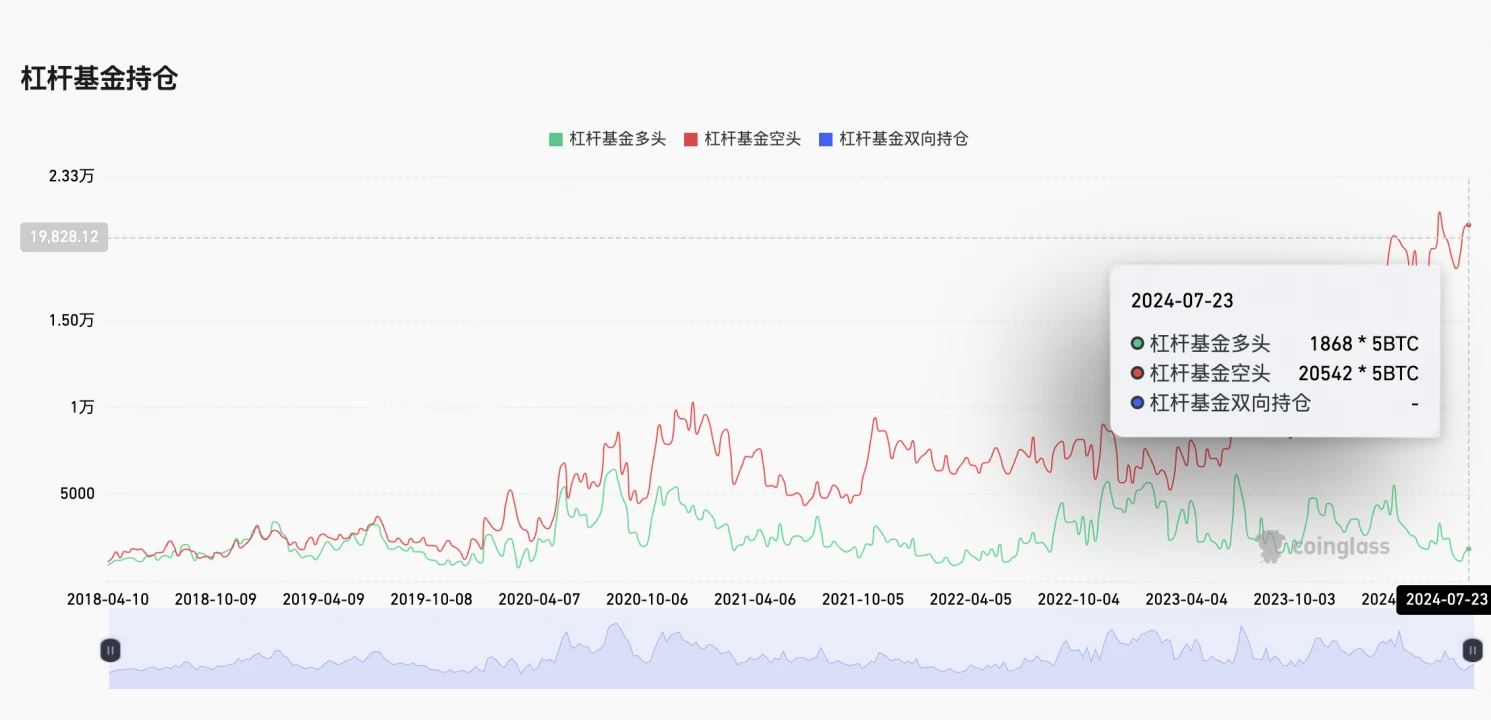

CME BTC Leveraged Funds Short Position

杠杆基金空头在上周(2024/07/16 – 2024/07/23)增加了 103 张, 515 个 BTC,通常这个指标在向上时也意味着套利资金的现货端也在加仓,而指标下降到达拐点指示空头平仓后会有上涨行情。

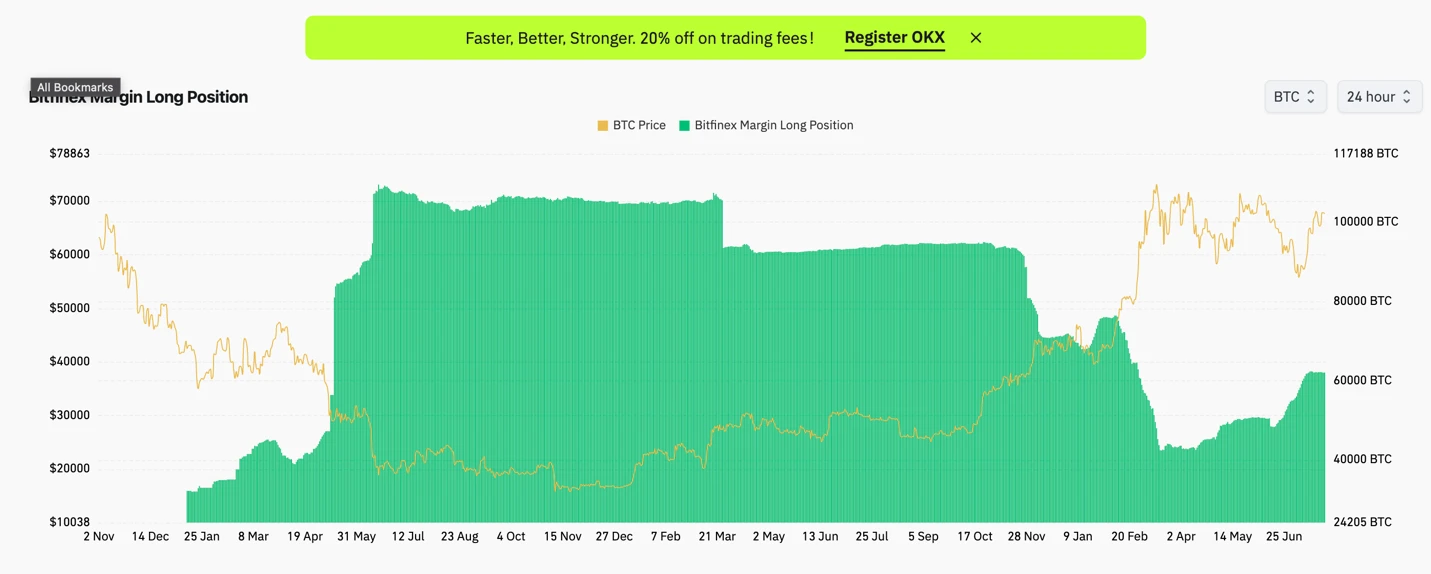

Bitfinex BTC Margin Long Position

Bitfinex 多头持仓在 3 月 16 日平仓到达低点后(对应行情到达高位),随后开始继续累积多头头寸,到目前为止持仓仍在高位,但不再增长。

稳定币供应振荡器(SSRO)

SSRO 在 7 月 9 日触底时已经低于去年 8 – 9 月的低点,表明场内资金的参与热度在急速下降。但这也形成拐点,从低点反弹。这个位置相对的低位对于山寨来说是比较好的反弹条件。

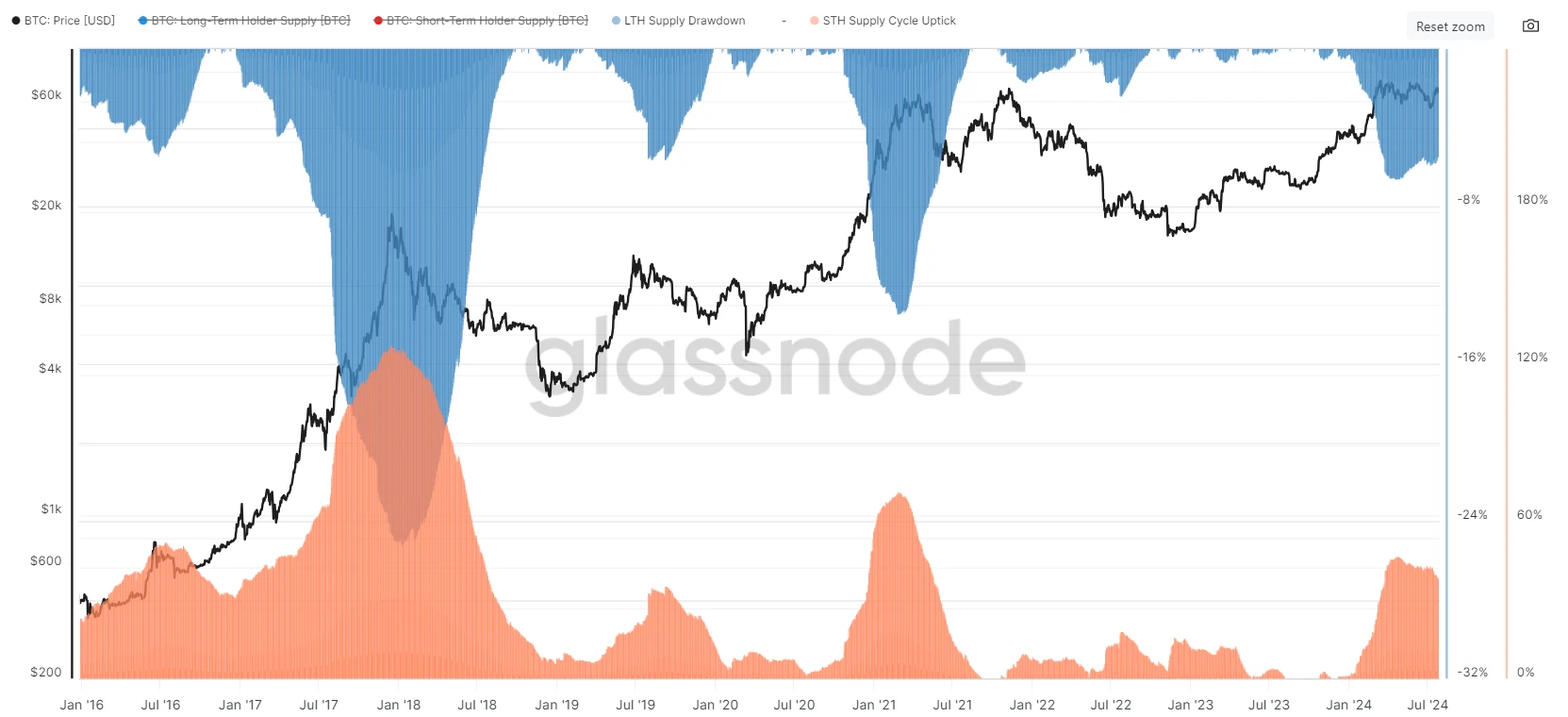

BTC 长短期持有者占比变化

蓝色部分为 BTC 长期持有者持币占比变化。按照此前 2017 年和 2021 年的两轮牛市,会出现两次 BTC 长期持有者持币占比的降低,第二次降低的幅度要大于第一次。

2023 年 12 月至 2024 年 4 月,在 BTC 主升浪的期间,BTC 长期持有者在持续卖出。4 月以来,BTC 进入宽幅震荡区间,长期持有者停止了卖出的行为,倾向于继续持有 BTC。

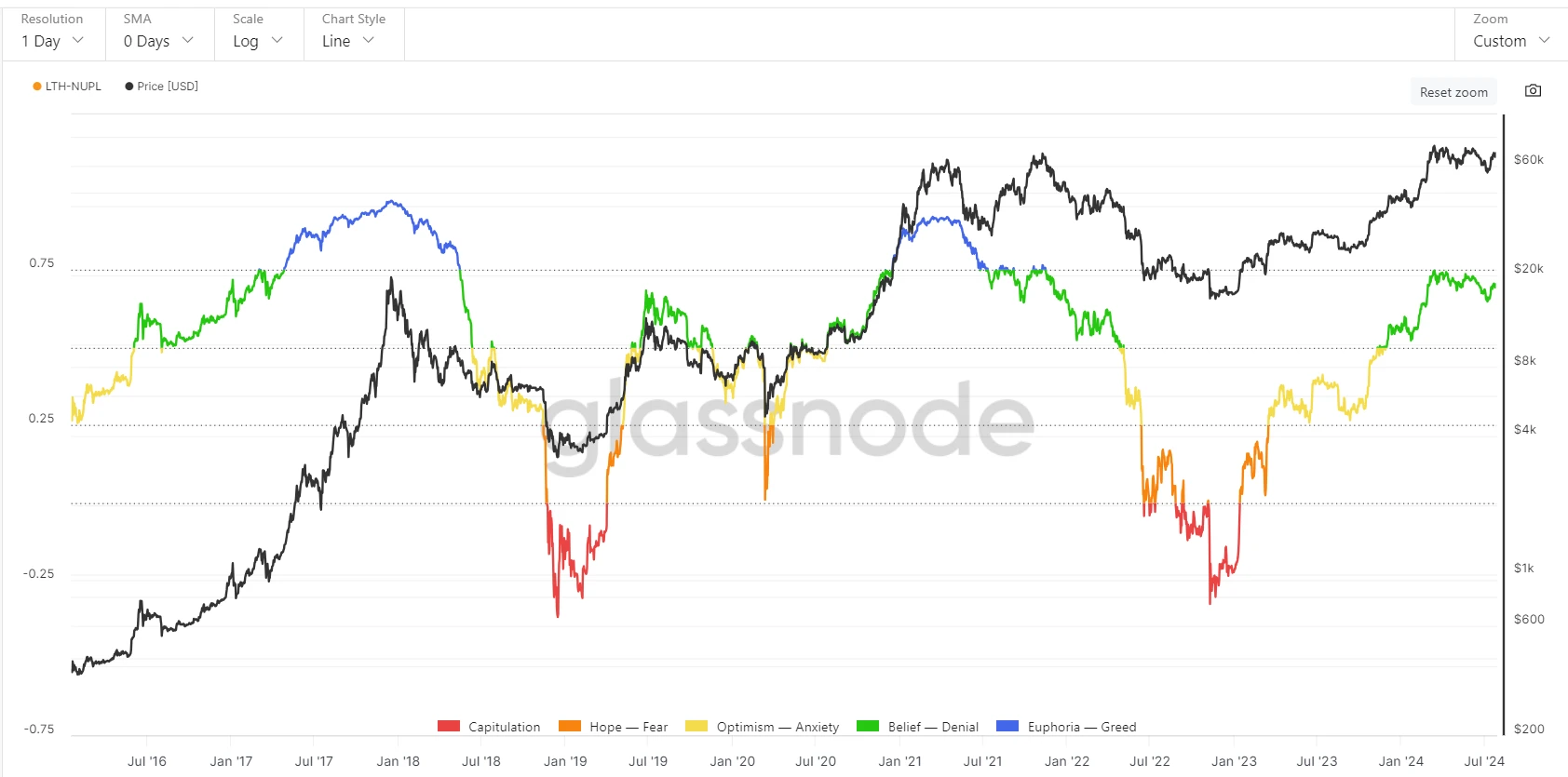

BTC 长期持币者未实现净损益

在 2017 年、 2021 年两轮周期中,BTC 长期持币者未实现净损益都进入了蓝色区域,超过了 0.75 。本轮行情以来,该指标尚未进入蓝色区域,目前仍在绿色区域运行。认为后续该指标应进入蓝色区域后运行一段时间,形成本轮行情的顶部。

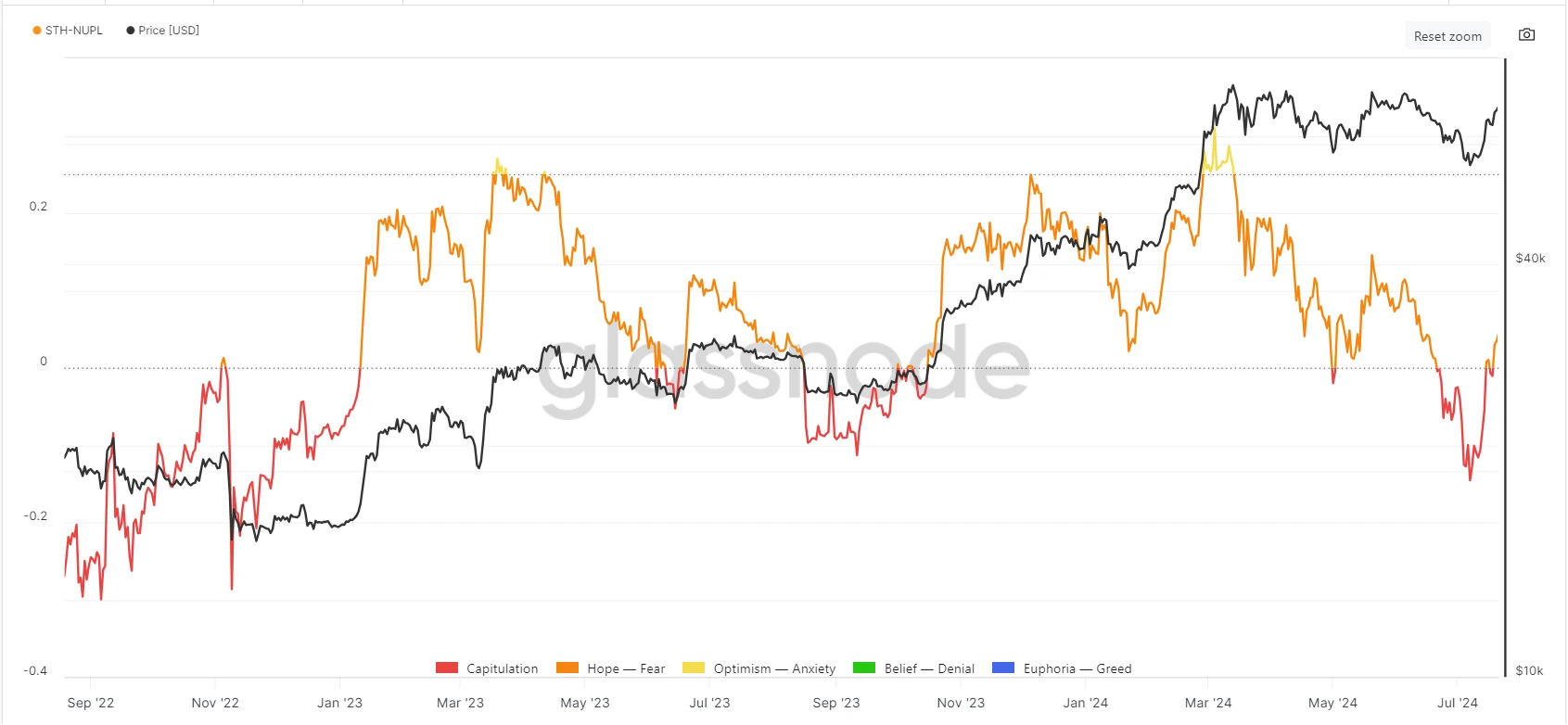

BTC 短期持币者未实现净损益

在牛市中,BTC 短期持币者未实现净损益接近 0 或者 0 以下时,会形成相对的阶段性底部。在 2023 年出现过 2 次低于 0 的情况,在 2024 年也出现了 2 次。2024 年 6 月底至 7 月初,短期持币者未实现净损益位于 0 以下, 7 月 15 日恢复到 0 以上,参考 2023 年 9 月走势,后续可能形成主升。