作者:Builders

编译:深潮TechFlow

代币发行是一个项目历史上的关键时刻。如果搞砸了代币发行,项目可能就此终结。

没有什么比女巫攻击更能迅速摧毁代币发行的信誉了。在这种攻击中,恶意行为者创建多个虚假身份,试图在网络中获得不成比例的影响力和代币分配。

没有人希望看到一个虚假的社区。

接下来,我们将通过两个最近的空投案例:zkSync 和 LayerZero,来探讨女巫攻击如何影响代币发行。

zkSync

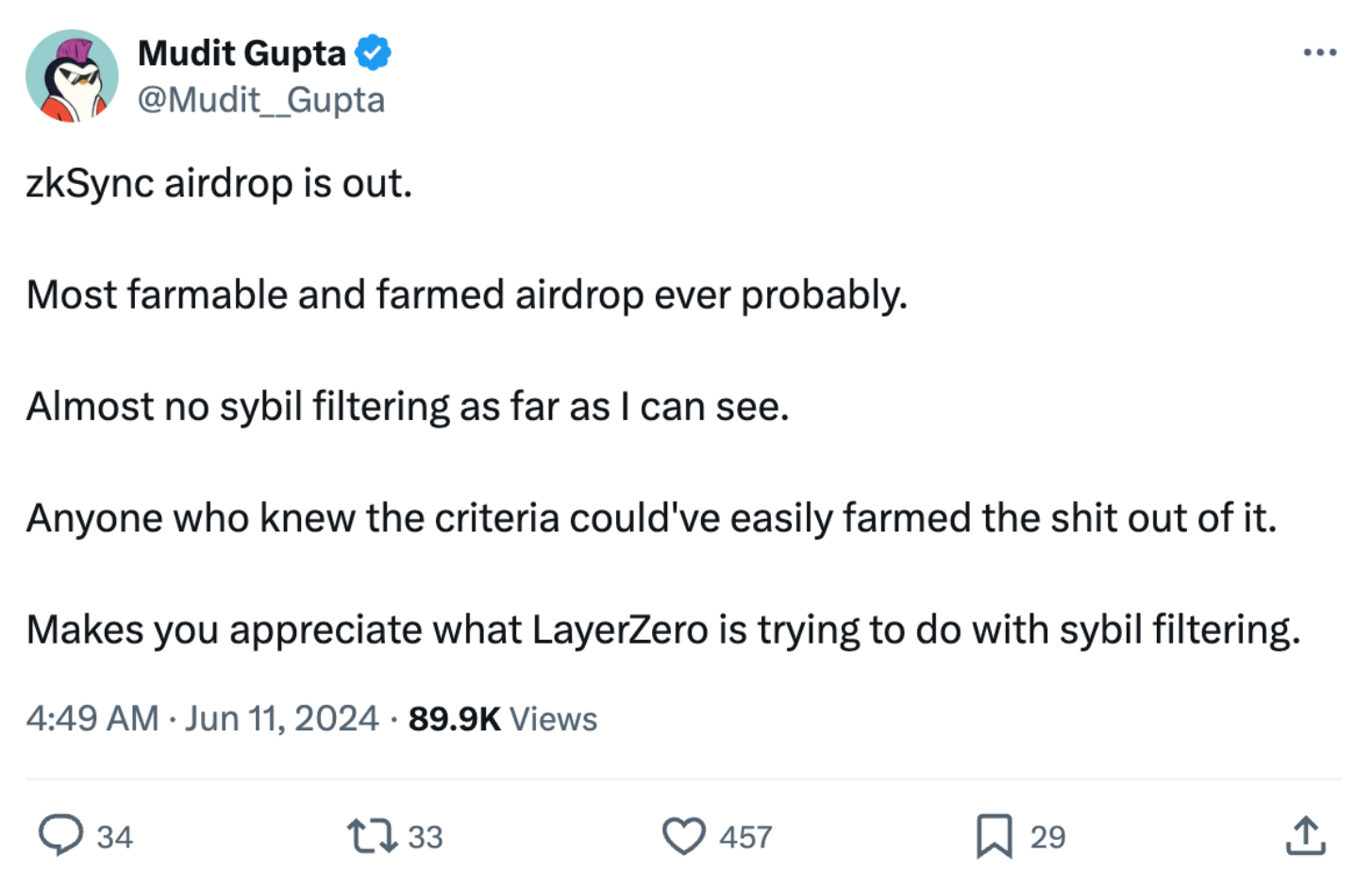

zkSync 是一个使用零知识证明的以太坊 Layer 2 扩展解决方案,曾是 2024 年最受期待的空投之一。然而,由于缺乏女巫防范措施,它受到了不少批评。例如,Polygon Labs 的首席信息安全官 Mudit Gupta 在 X 上评论道:

zkSync 的空投已经发布。

这可能是有史以来最容易被“农场”的空投。

据我所知,几乎没有进行 Sybil 过滤。

任何了解标准的人都可以轻松大量获取。

这让人更加理解 LayerZero 在 Sybil 过滤方面所做的努力。

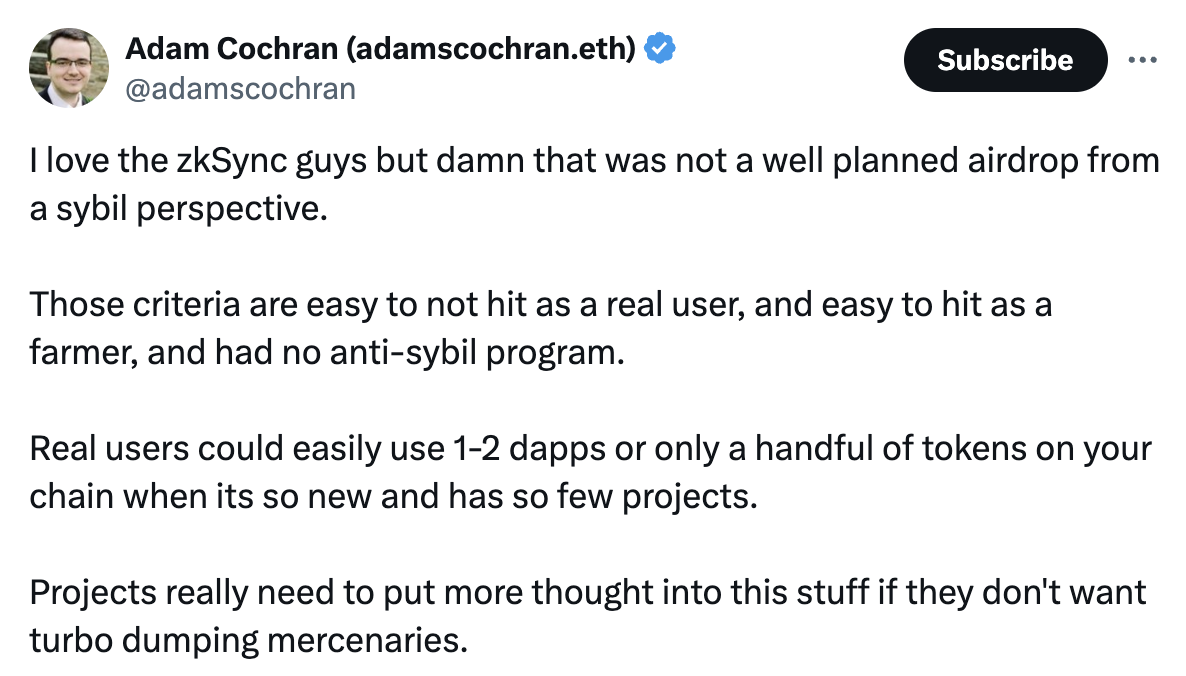

Cinneamhain Ventures 的合伙人 Adam Cochran 也表达了类似的担忧:

我很喜欢 zkSync 的团队,但从 Sybil 防范的角度来看,这次空投计划得确实不太好。

这些标准对真实用户来说很容易错过,而对“农场”用户来说却很容易达成,而且没有任何反 Sybil 措施。

在链上项目如此新且项目数量有限的情况下,真实用户可能只会使用 1-2 个 dapp 或持有少量代币。

如果项目不想要那些快速抛售的“投机者”,就需要在这方面多花些心思。

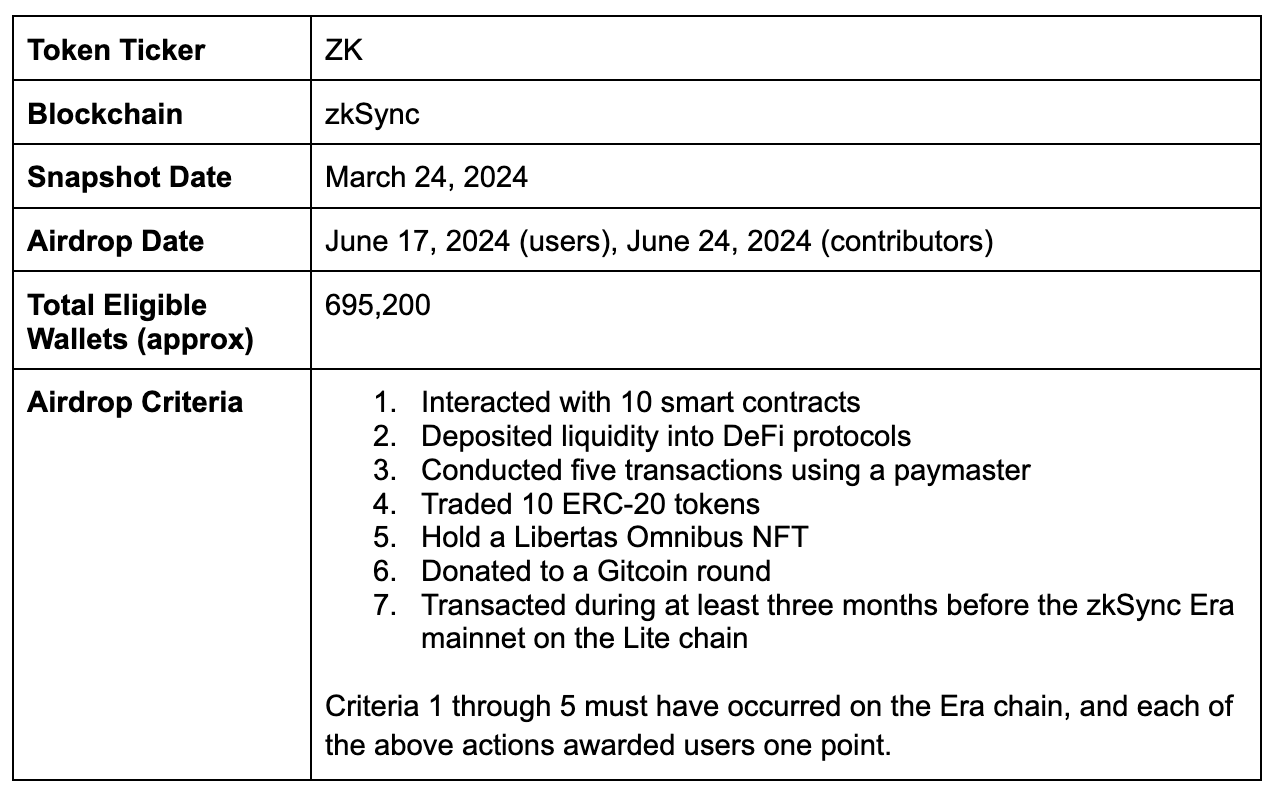

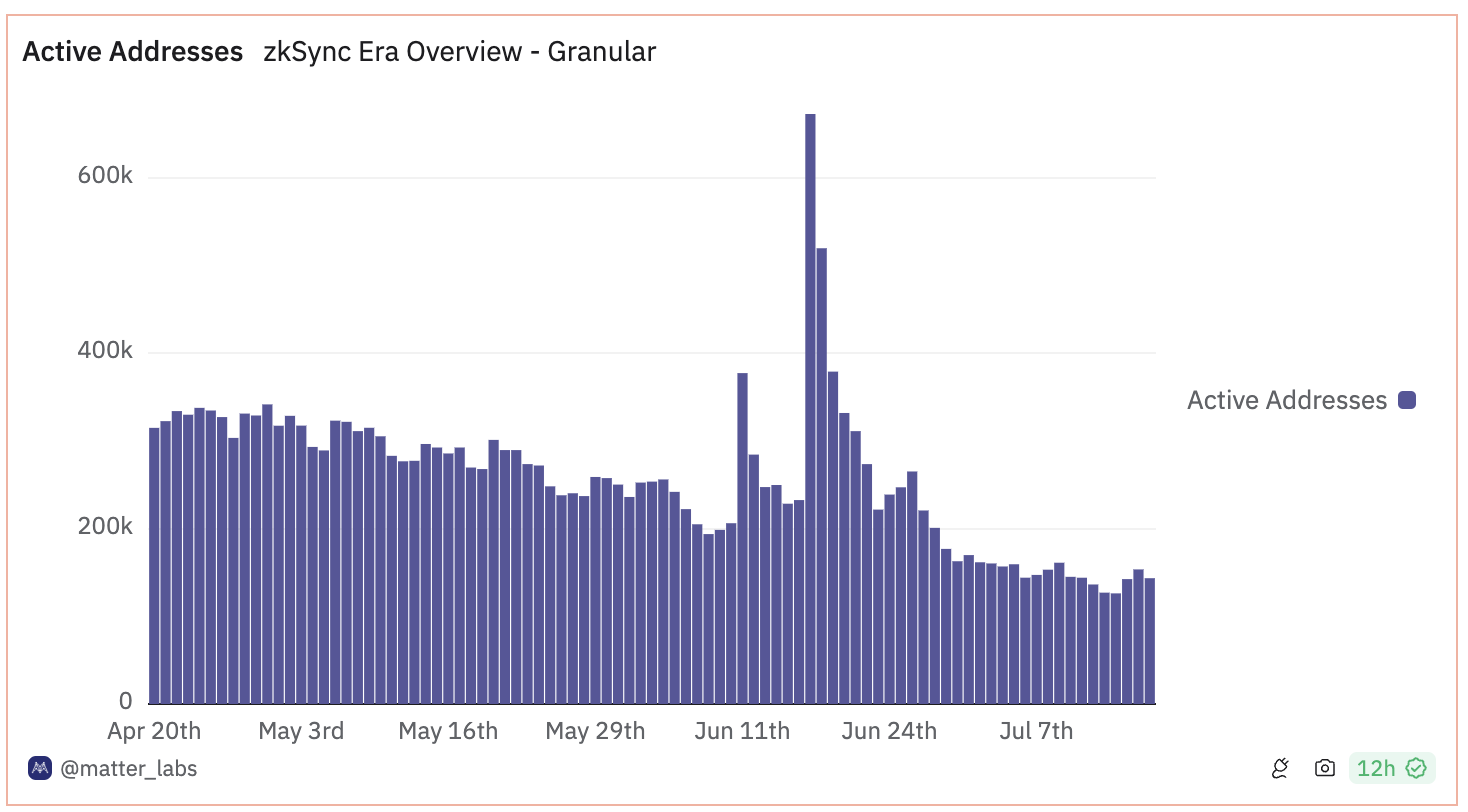

zkSync 的网络活动

在 2024 年 6 月 17 日 zkSync 空投给用户后的一个月内(截至 2024 年 7 月 17 日),网络上的活跃地址数量减少了约 78.7%。这表明,大部分用户只是为了获取空投,随后便放弃了该项目。

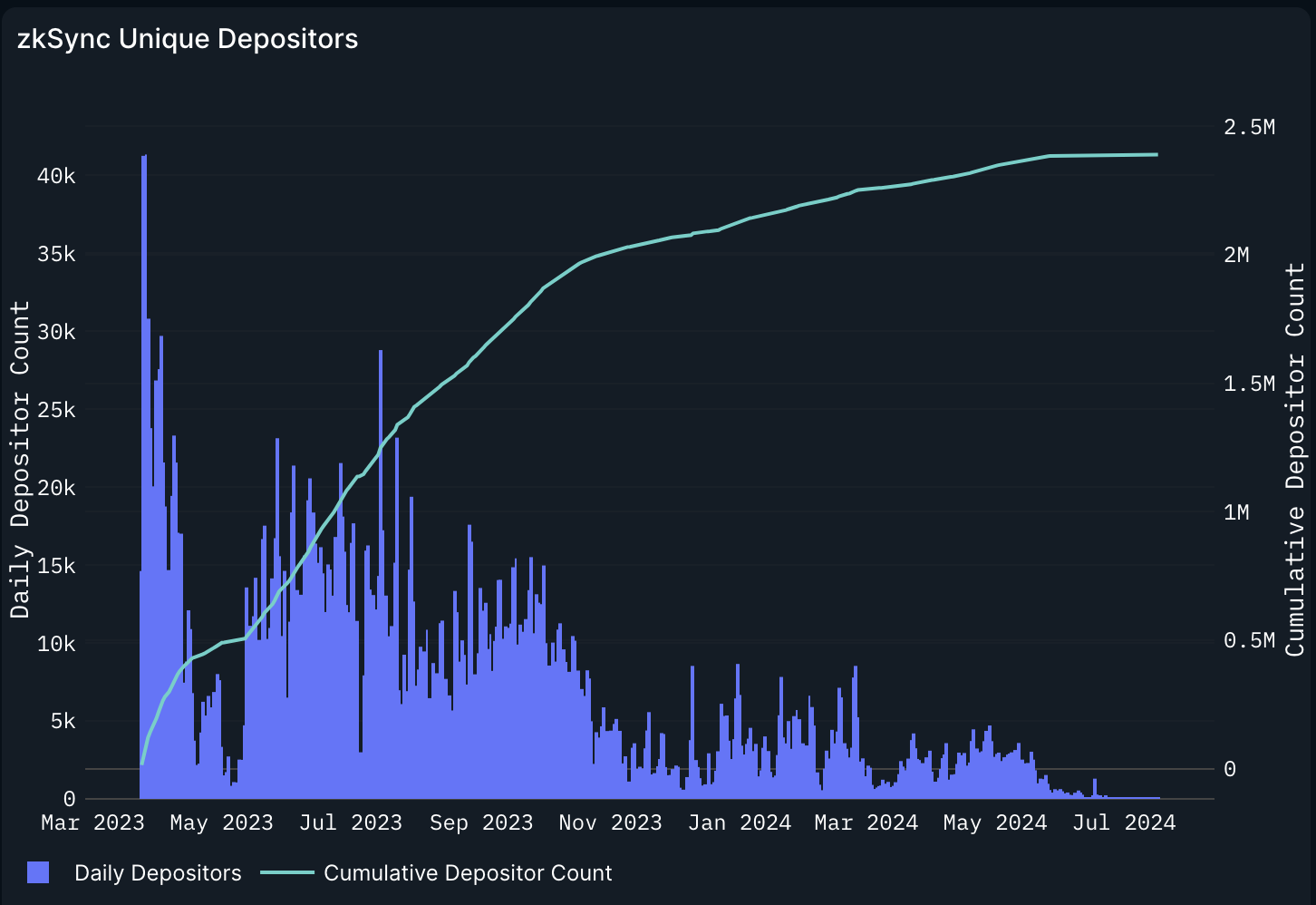

每日存款者数量也显示了类似的趋势——在 2024 年 7 月 17 日,仅有 32 个存款者,而在 2023 年 3 月 25 日的峰值为 41,257。

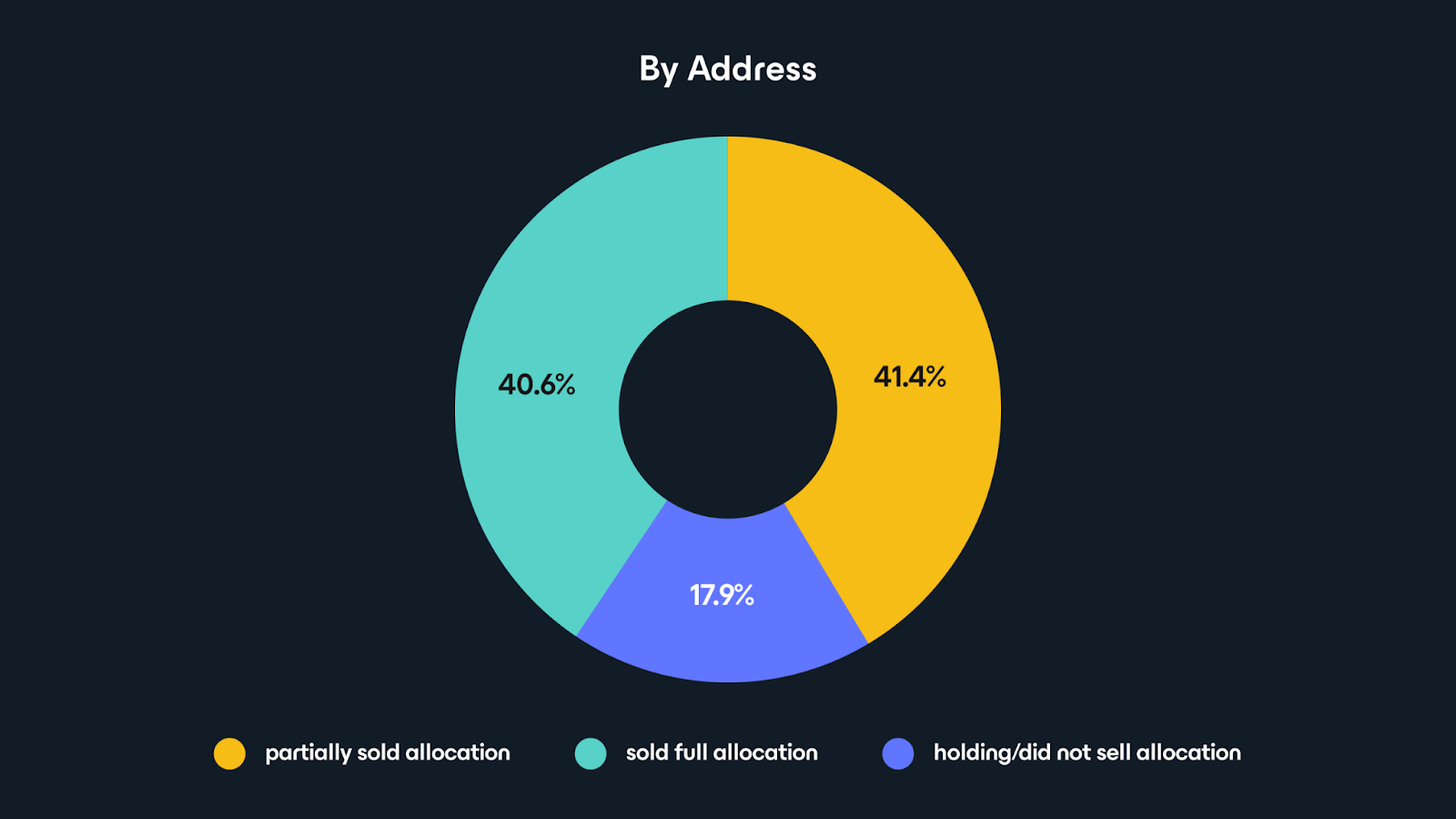

空投之后,超过 40% 的 zkSync 主要接收者出售了全部分配的代币,41.4% 出售了部分分配。目前,这些主要接收者中只有 17.9% 仍持有他们的代币。根据 @CryptusChrist 的数据,746 名已知的女巫攻击者在空投中获得了约 690 万美元的 ZK 代币。

ZK 价格走势

不幸的是,ZK 的抛售——很可能是由女巫攻击者策划的——加剧了市场的卖压,导致代币价格在用户空投日期(2024 年 6 月 17 日)到 2024 年 7 月 23 日之间大约下降了 39.29%。

那么,zkSync 到底出了什么问题?首先,团队的空投资格标准相对容易被女巫攻击者利用,并且缺乏有效的女巫防范措施。此外,zkSync 还排除了某些合法用户,例如那些在 zkSync ERA 上构建并直接为其生态系统做出贡献的项目。

现在,他们的团队需要加倍努力,重新吸引那些被女巫攻击者虚假活动所驱动的显著价格投机。

LayerZero

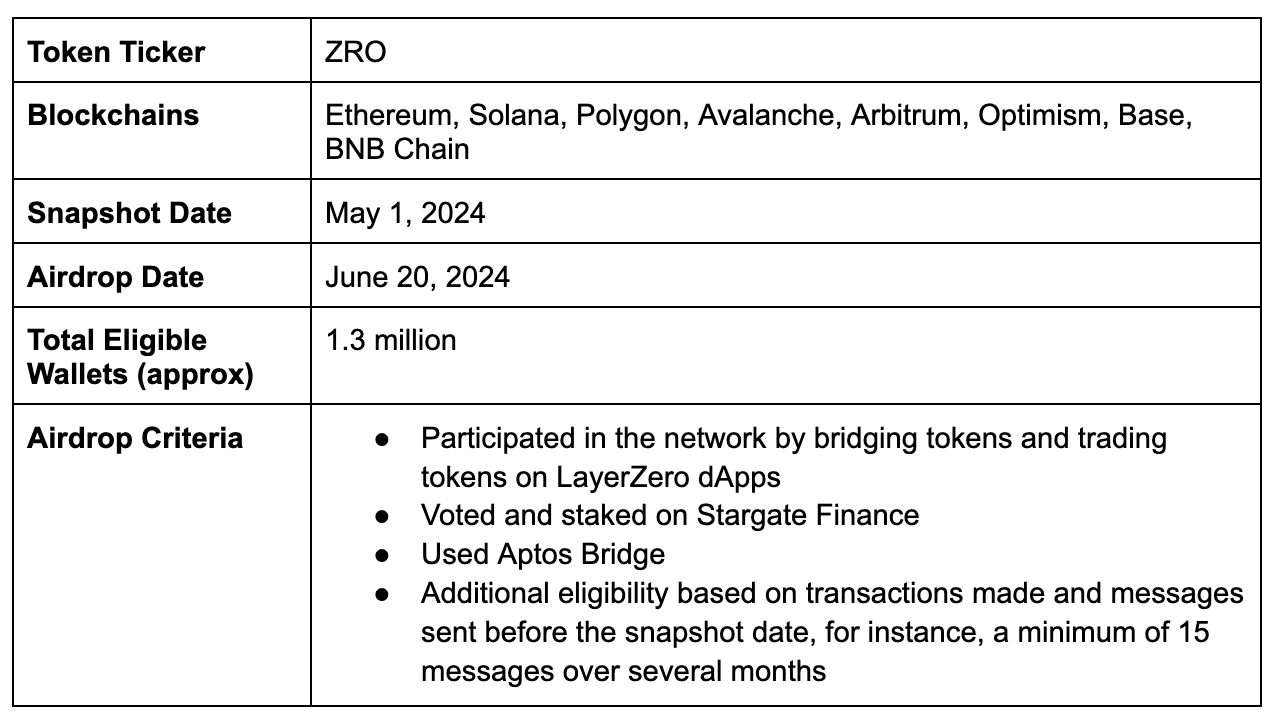

LayerZero 是一个旨在促进不同区块链之间无缝通信和资产转移的互操作性协议,与上述两个例子不同,LayerZero 实施了强有力的女巫防范措施。

根据 LayerZero Labs 的首席执行官 Bryan Pellegrino 的说法,团队在女巫自我报告和分析阶段最终识别出了 110 万到 130 万个独特的女巫钱包,并且他们的团队继续参与并奖励社区报告女巫攻击者。

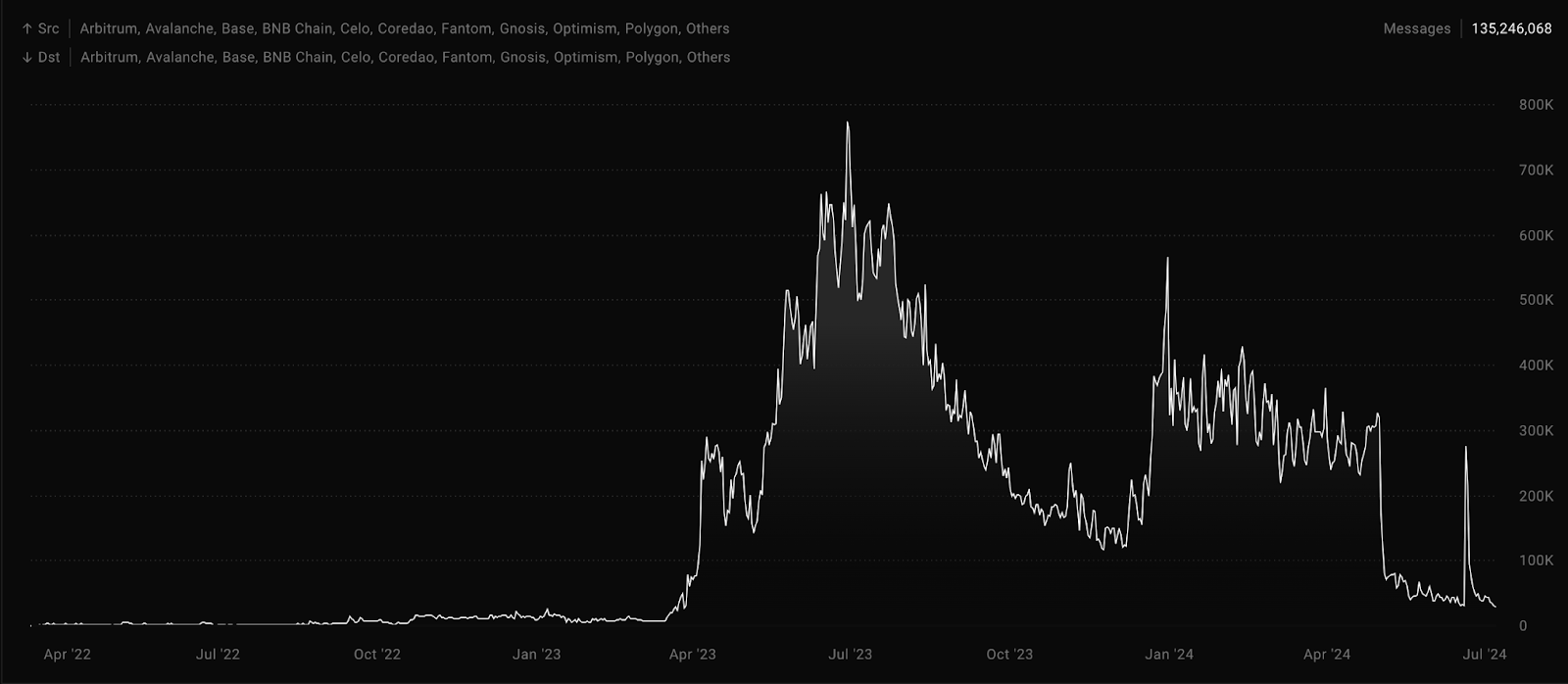

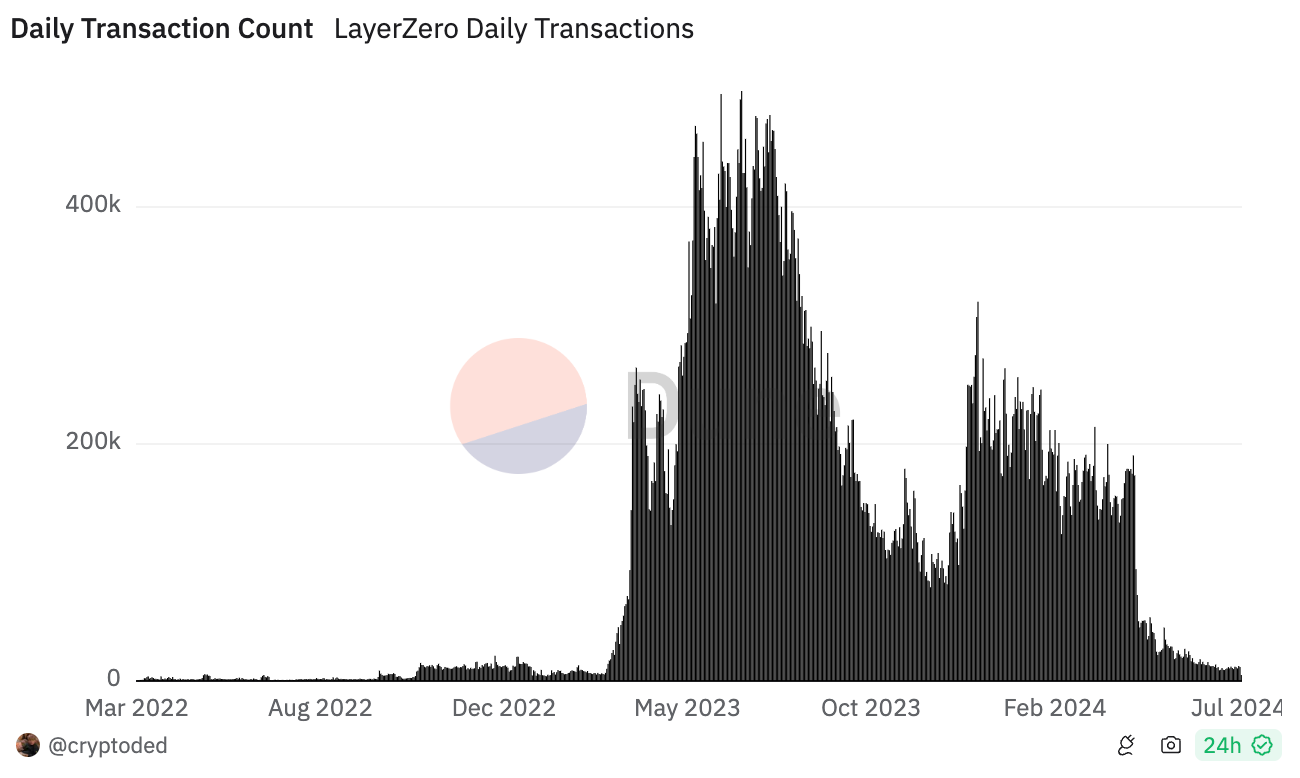

LayerZero 的网络活动

在 2024 年 4 月 30 日(快照日期的前一天)到 2024 年 7 月 7 日之间,LayerZero 上的消息数量下降了 91.5%。

同样,每日交易数量在快照日期和空投日期之间也下降了超过 92%。

这种下降部分是因为用户在快照日期之后通常停止活动,因为他们不再需要交易以获得空投资格。然而,上述团队的女巫防范方法也可能影响了这一下降,使他们能够在更少的女巫攻击者的情况下进行空投。

ZRO 价格走势

从 2024 年 6 月 20 日(空投日期)到 2024 年 7 月 18 日,LayerZero 的原生代币 ZRO 的价格从 $4.79 下降到 $4,约下降了 16%。这一降幅显著低于 ZK 在相似时间段内的 39% 下降。值得注意的是,尽管 LayerZero 的网络活动有所下降,但 ZRO 的价格最终超过了其初始上市价格。

虽然很难确定 LayerZero 价格相对稳定的所有因素,但其女巫防范技术可能起到了作用。

为什么建设者应该关心女巫防范?

在短期内,女巫攻击可能看起来对项目有利,因为它们可以人为地提升数据并产生即时利润。

然而,如上述例子所示,引入女巫攻击可能导致代币抛压和网络活动下降——这两者都会侵蚀项目的长期可持续性。

当女巫攻击者被移除时,合法参与者有更多机会参与和贡献,因为欺诈实体的移除释放了宝贵的位置。

大多数通过空投启动的团队需要加倍努力,重新吸引那些由虚假活动推动的显著价格投机和网络活动。没有人希望看到一个虚假的社区。