作者:cygaar

编译:深潮TechFlow

“账户抽象是加密货币的未来。”

你可能听过这句话很多次,但并不清楚它的具体含义。今天,让我们来解决这个问题。

我将为你介绍账户抽象的初学者指南——它是什么,如何运作,以及它将如何彻底改变加密货币应用。

我们不会深入探讨账户抽象的技术和实现细节(那是以后的话题)。相反,这里将提供一个高层次的概述,并通过实际例子展示账户抽象在过去几年中如何改善了加密货币的用户体验。

简单来说,账户抽象是一套框架和标准,可以大幅提升加密钱包(账户)的功能。

你可以把它想象成给一辆1999年的本田思域加上飞行能力,它仍然可以作为汽车行驶,但现在它还能做更多事情。

你可能会问,为什么加密钱包默认不具备这些强大功能呢?答案是,在一些现代区块链上,它们确实很强大,但对于像以太坊这样的传统区块链,账户是在我们完全理解其所有潜在用途和缺陷之前设计的。

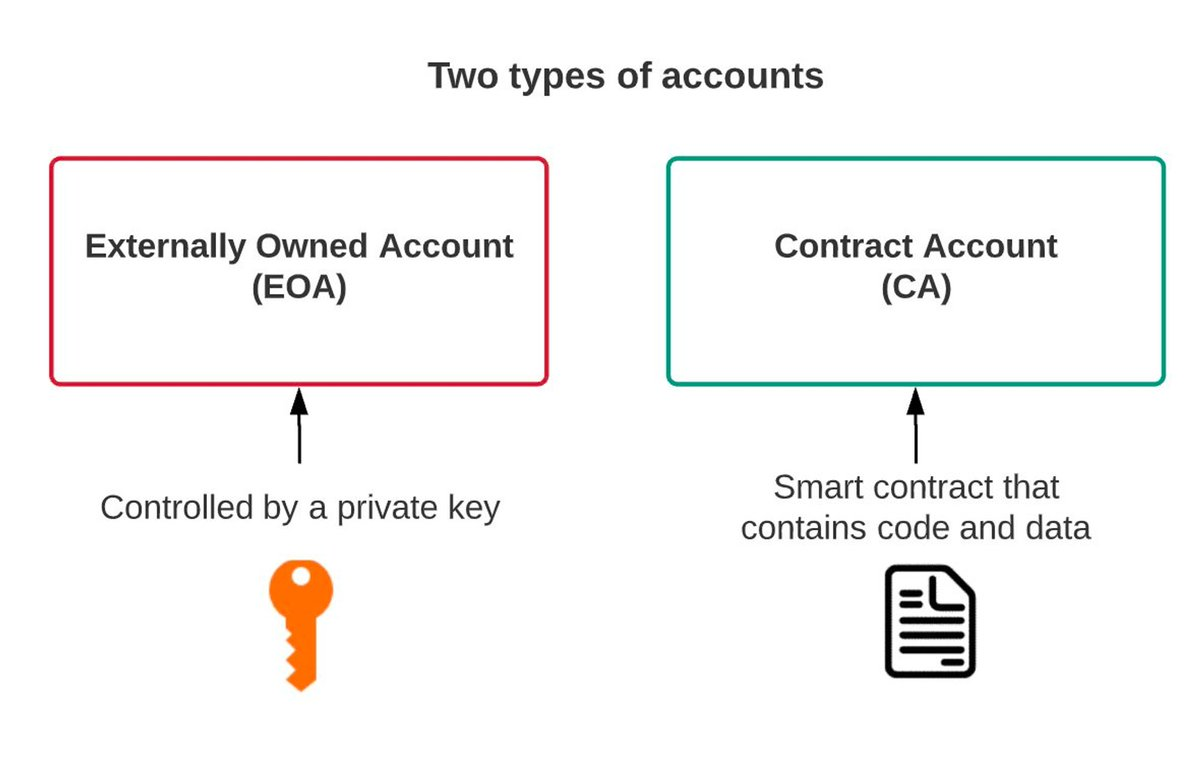

在以太坊(和许多EVM链)上,我们主要使用外部拥有账户(EOAs)。这些是简单的钱包,只能持有资产并发起交易。它们绑定到一个单一的私钥,无法执行复杂操作。

同时,我们还有智能合约,在区块链上自动执行的代码。智能合约几乎可以被编程来执行任何任务。

如果我们能将智能合约的灵活性添加到每个人的加密钱包中,那不是很酷吗?这就是合约账户(CAs)登场的地方——它们是账户抽象的核心部分。

合约账户将智能合约的无限功能融入钱包中,使其功能大幅增强。这些钱包仍然可以持有资金,但不再依赖于单一的私钥。

过去,如果你丢失了私钥,就相当于丢失了钱包。

这对于非加密货币用户来说,体验非常糟糕。而有了合约账户,钱包可以通过多种认证方式进行操作,而不再需要传统的私钥签名。

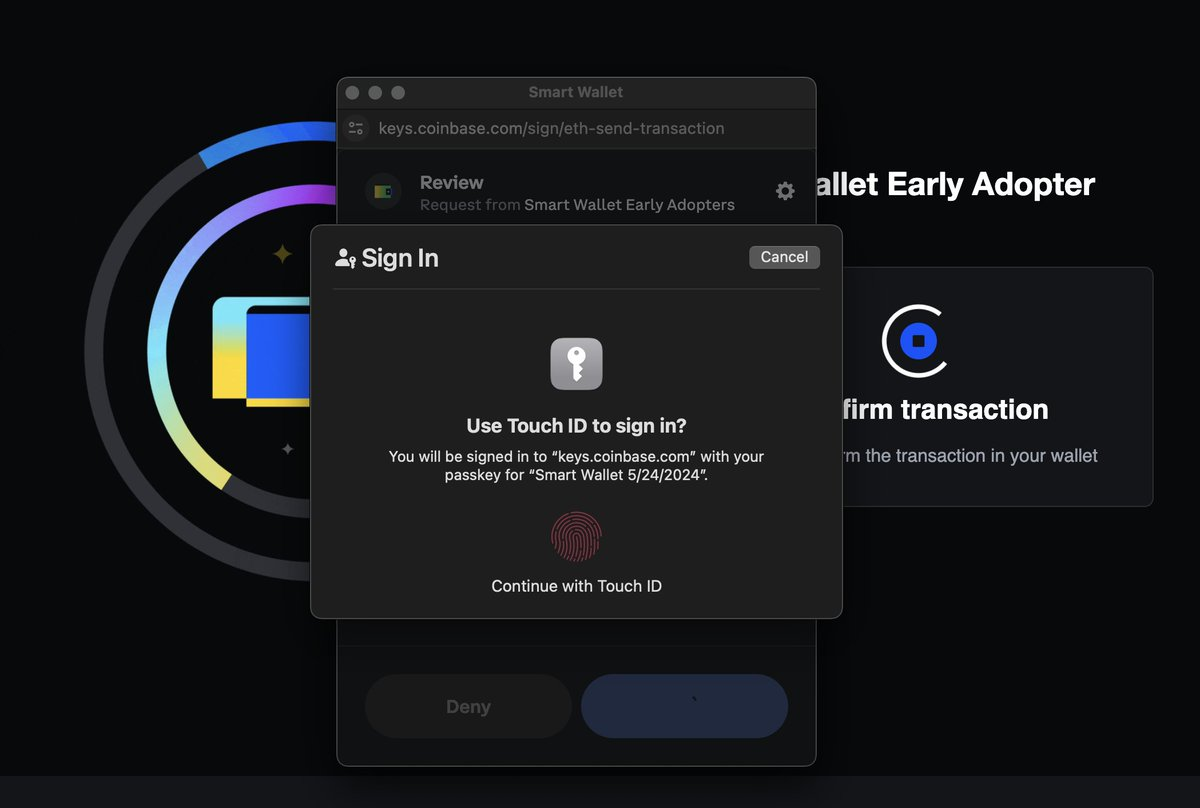

你可以使用指纹识别、第三方提供商(如Google、Apple)、多重签名或不同的签名方案来进行认证。

即使你真的丢失了原始私钥,也可以通过设定的方法恢复账户。

构建账户验证的方法有很多。这些方法不仅能提升钱包的安全性,账户抽象(AA)还赋予钱包新的功能。

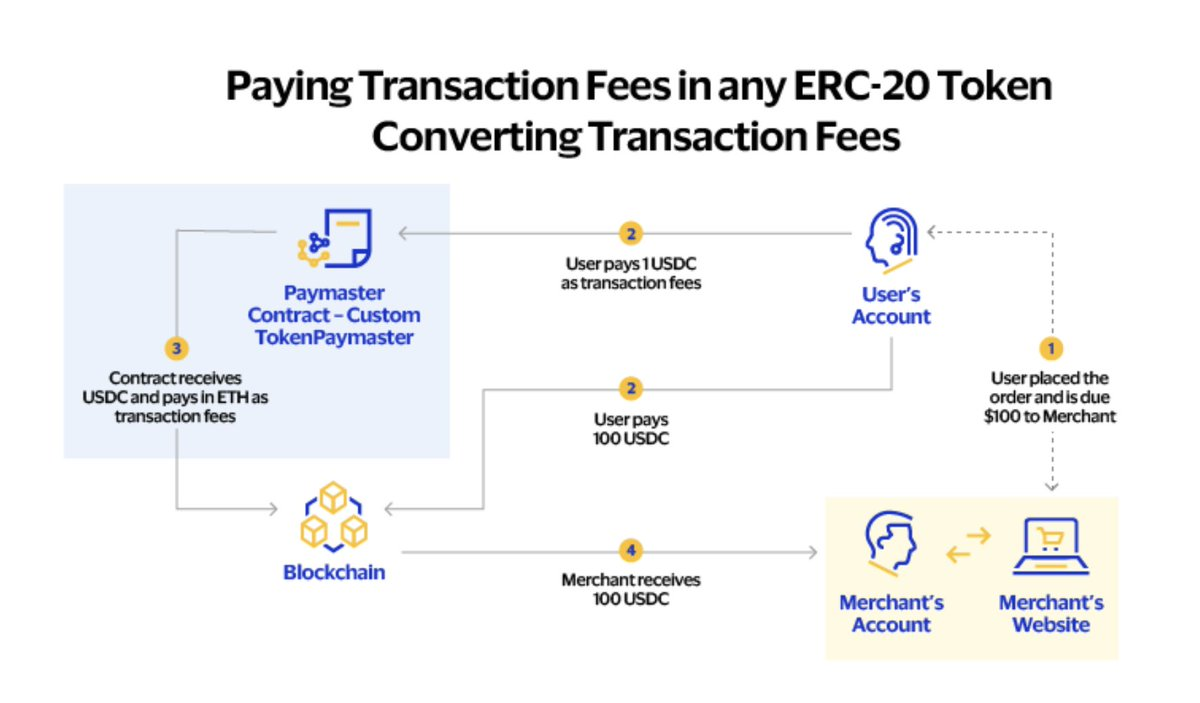

在外部拥有账户(EOAs)中,所有交易必须使用链上的原生燃料代币支付,并且必须由发起者支付。此外,一次只能进行一笔交易。

但有了AA:

-

交易可以完全由第三方(通常是应用程序)赞助

-

交易可以用不同的代币支付(例如,用USDC支付而不是ETH)

-

交易可以批量处理,节省 gas 费,并允许在不需要单独批准的情况下进行代币交换

由此可见,AA 能够显著改善加密应用的用户体验。之前,我们被僵化的结构束缚,使得加密货币的入门变得繁琐和困难。而现在,有了 AA,我们可以创造出与传统 Web2 应用媲美甚至超越的用户体验。

需要强调的是,这些智能合约账户仍然完全由用户自己掌控,没有第三方能够访问用户的资金——所有资产仍然是自我托管的。

那么,AA 的现状如何呢?

在 EVM 上,我们有 ERC-4337 和 EIP-7702 等提案,为AA奠定了基础。

如今,我提到的许多功能已经实现。然而,将现有钱包转变为合约钱包仍需要大量工作。

未来,我会发布一份详细的账户抽象指南,介绍更多细节。

目前,你只需知道 AA 是我们实现简单、安全和强大用户体验的关键,它将迎接下一波加密用户的到来。