昨日(20 JUN)宏观方面,美国上周初请失业金人数略超预期(23.5 万)录得 23.8 万人,同时 5 月新屋开工量下降 5.5% ,为四年来最低水平。美债收益率维持小幅震荡行情收跌,三大股指涨跌分化,标普和纳指分别下跌 0.25% 和 0.79% ,道指收涨 0.77% 。

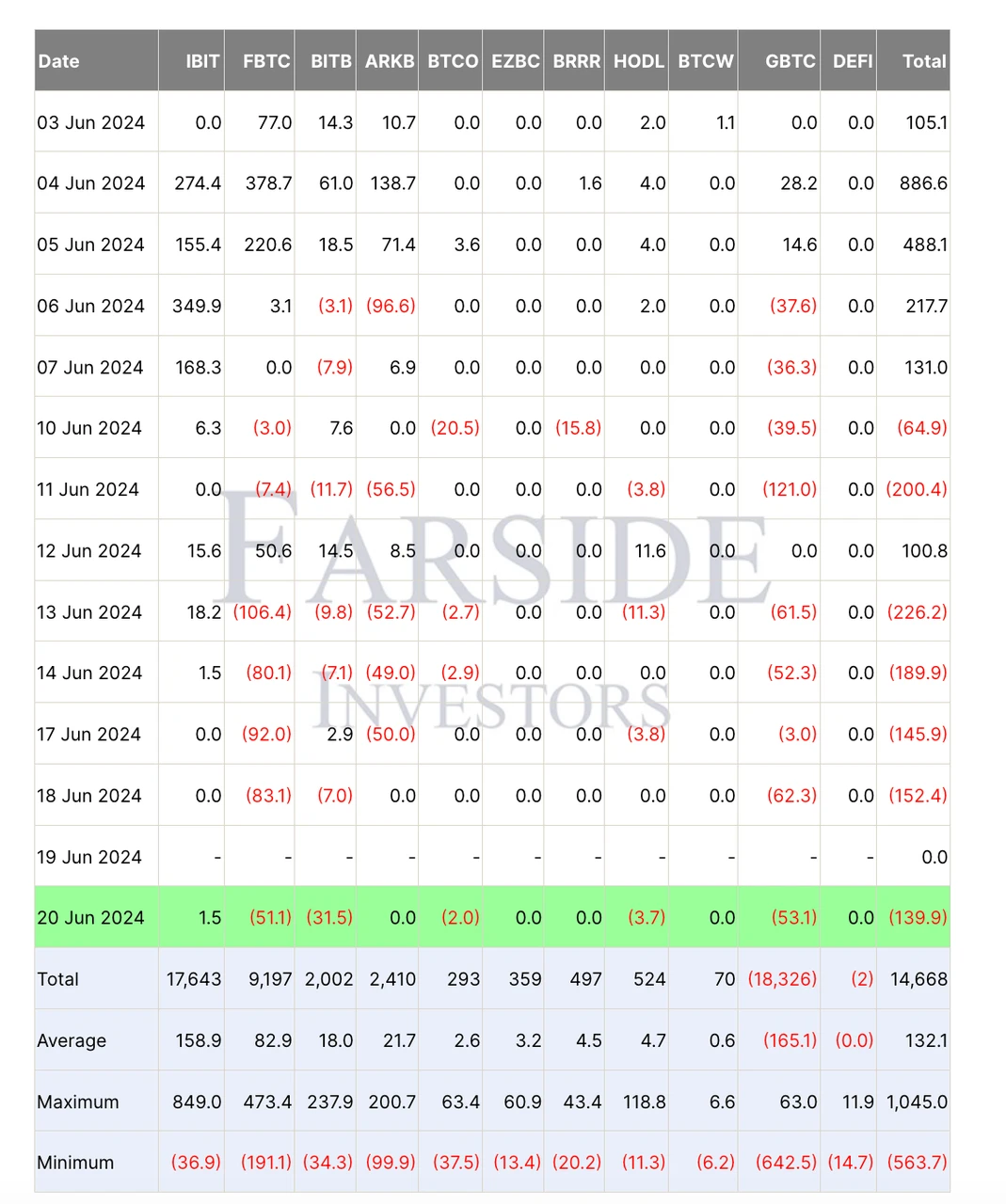

Source: Farside Investors

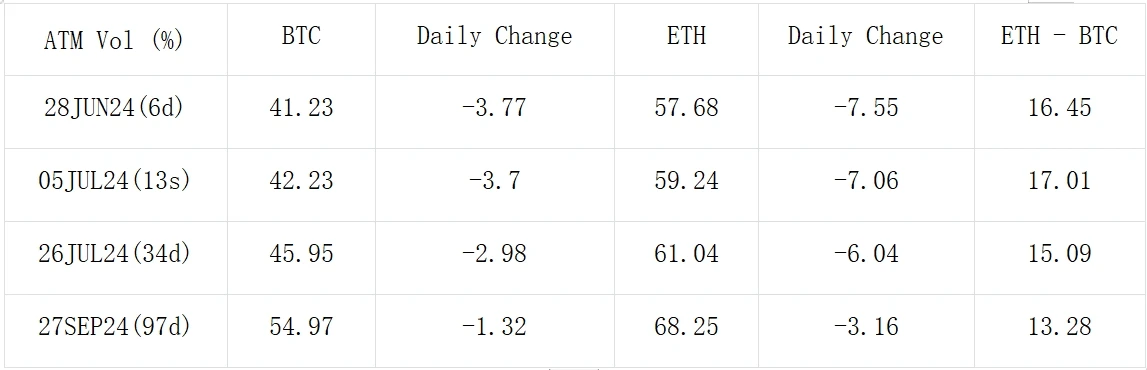

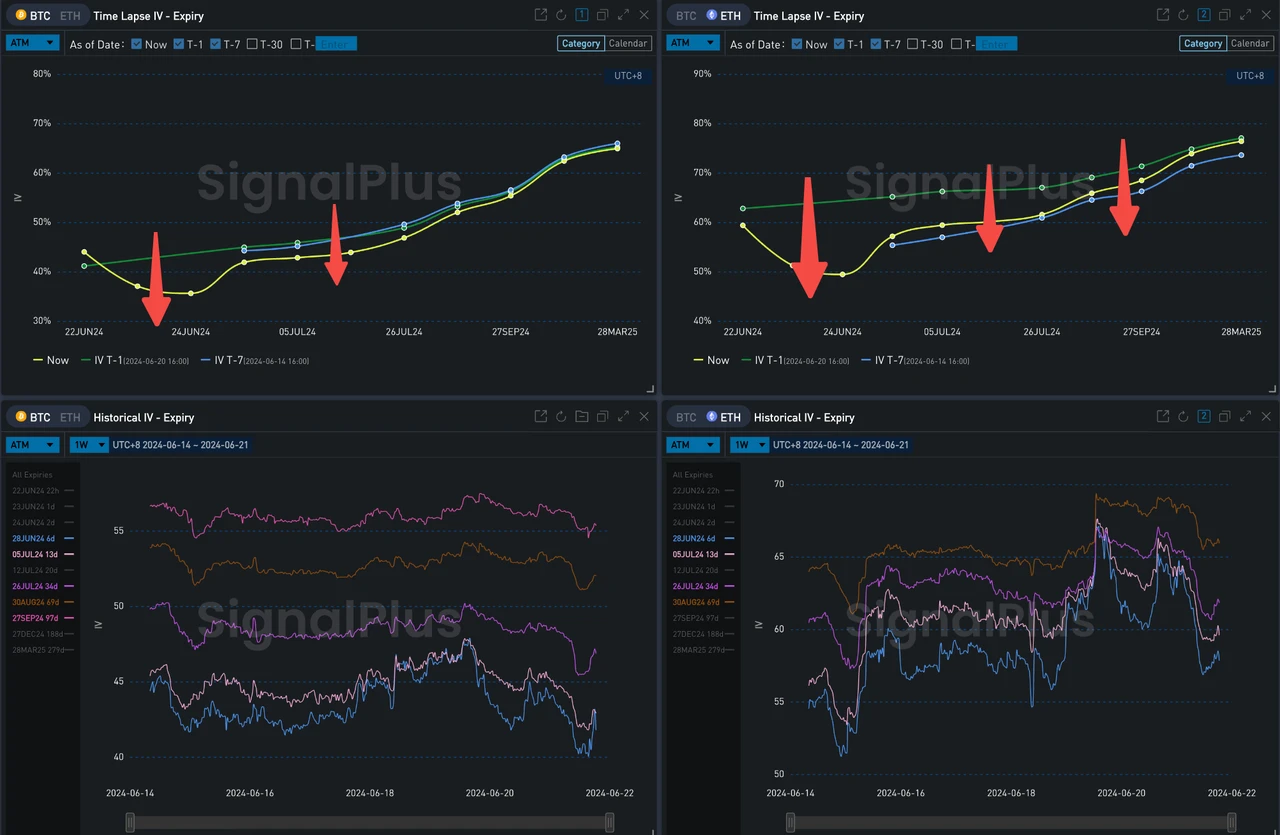

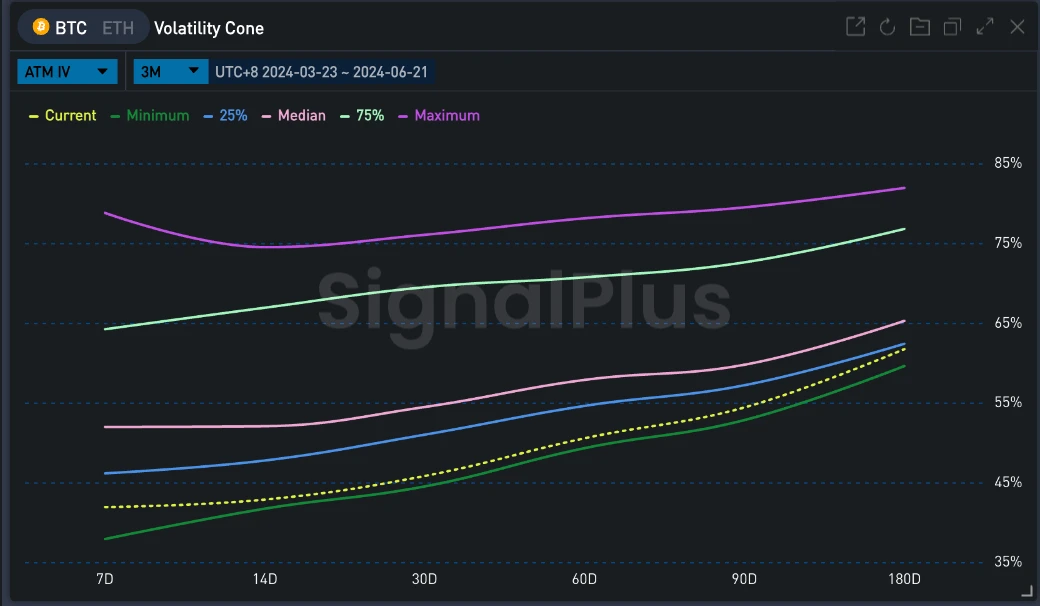

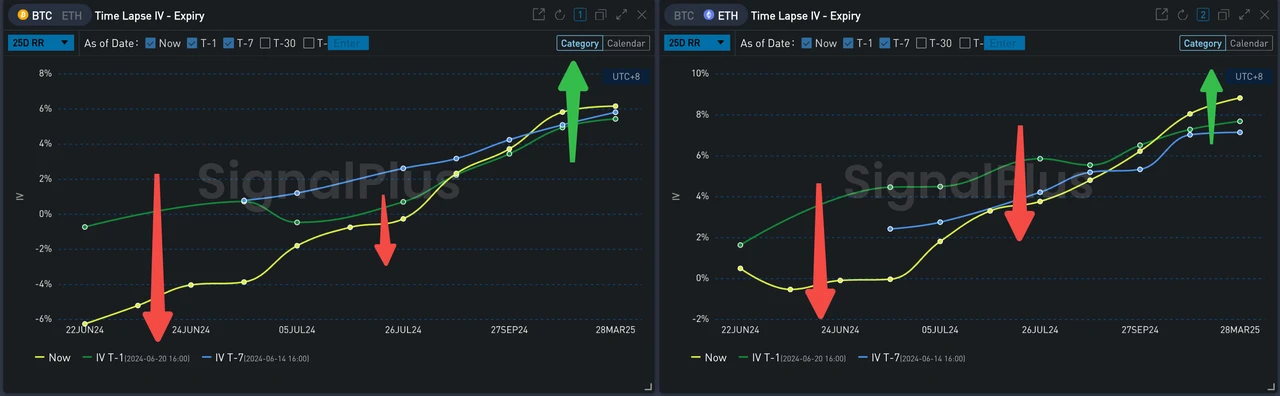

数字货币方面,BTC 现货 ETF 连续数日大量流出,币价延续跌势,下破 64800 美元支撑位,当前围绕在 64000 附近震荡。期权市场情绪不佳,BTC 六月底显著地出现买 put 卖 call 的 Long Risky Flow,ETH 七月底同样也反映出强烈的看涨期权卖压,带动市场整体的 Vol Skew 向下移动。与此同时,隐含波动率水平也在下降,BTC/ETH 分别走低了 3% /7% 左右,从过去三个月的数据上看,BTC ATM IV 已经接近历史最低点。

Source: Deribit (截至 21 JUN 16: 00 UTC+ 8)

Source: SignalPlus,IV 整体水平下跌,BTC 降至历史低点

Source: SignalPlus,受日内交易影响,中前端 Vol Skew 垮塌,远期微升

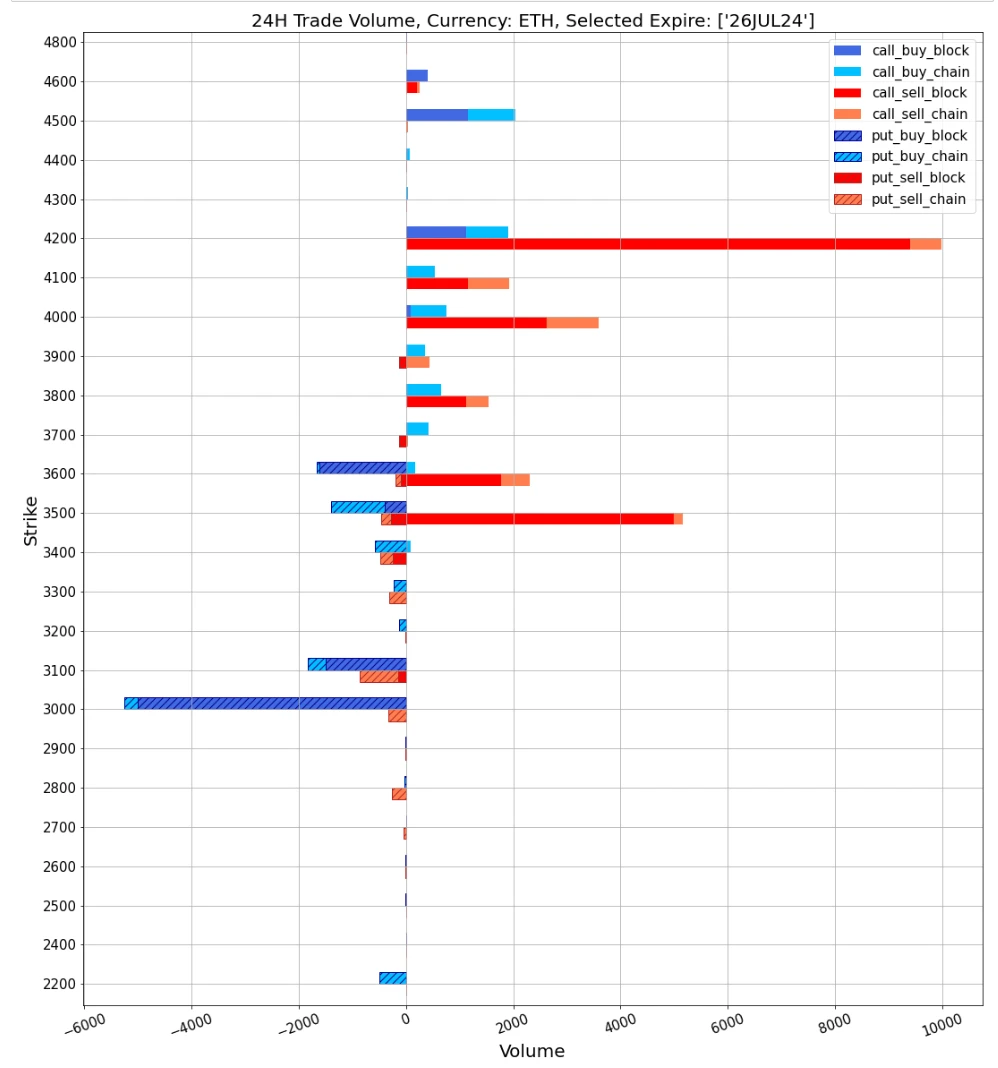

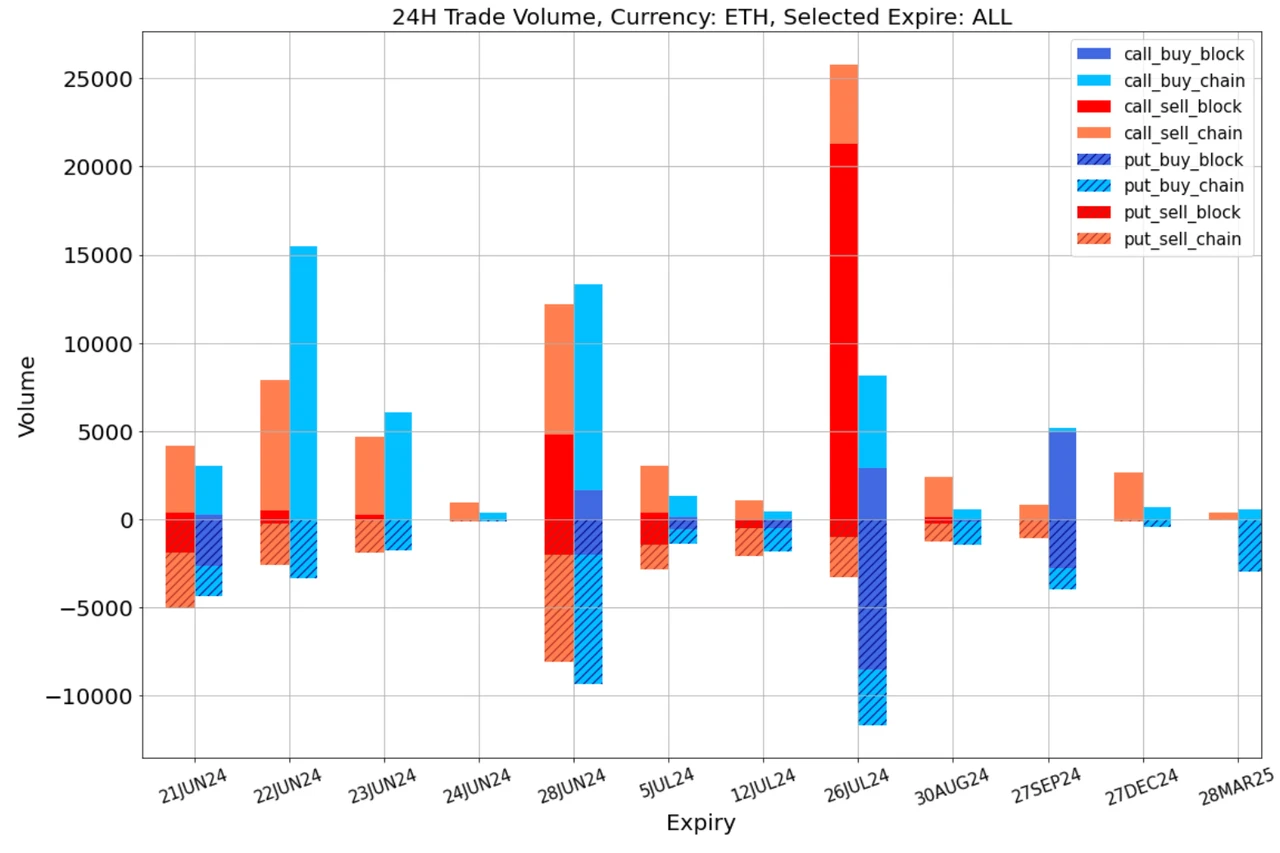

Data Source: Deribit, ETH 交易总体分布

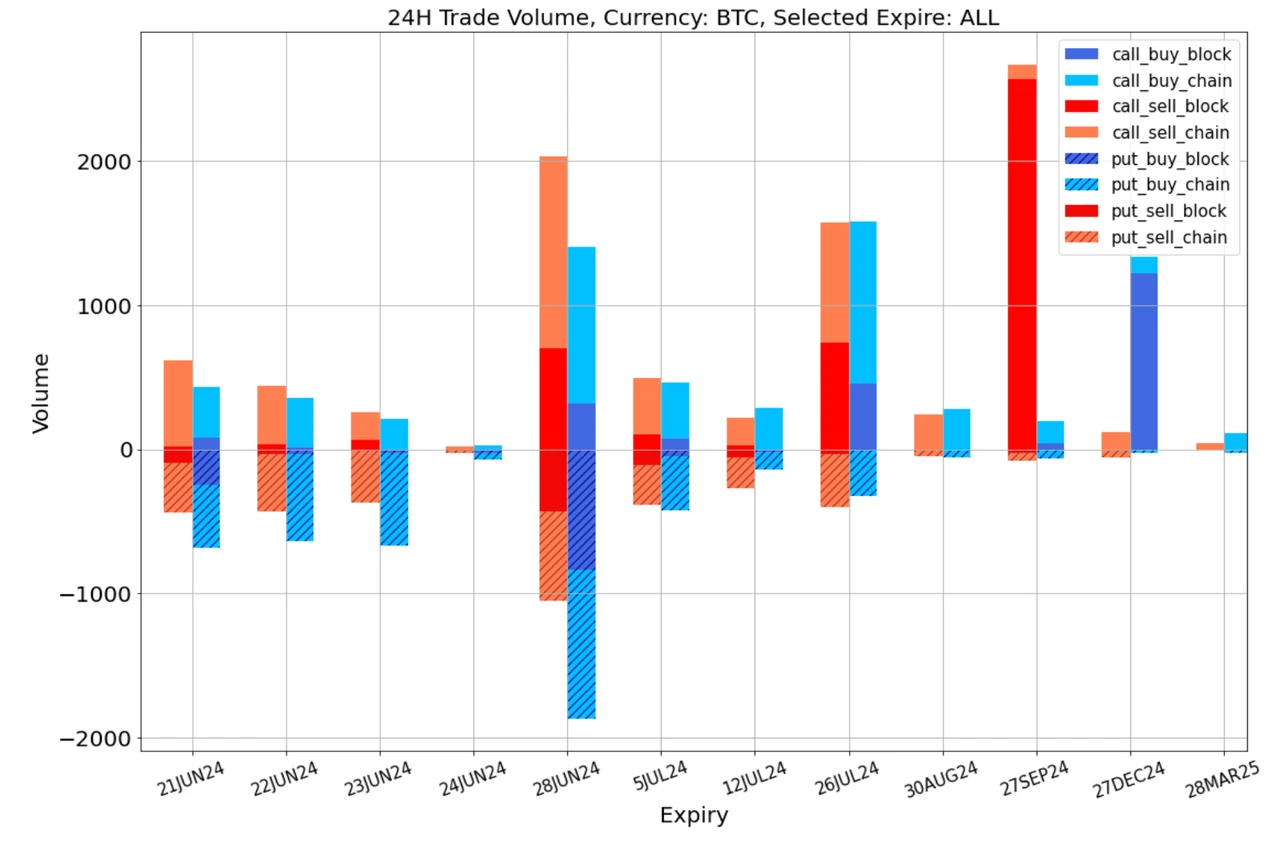

Data Source: Deribit,BTC 交易总体分布;28 JUN 24 Risky Flow

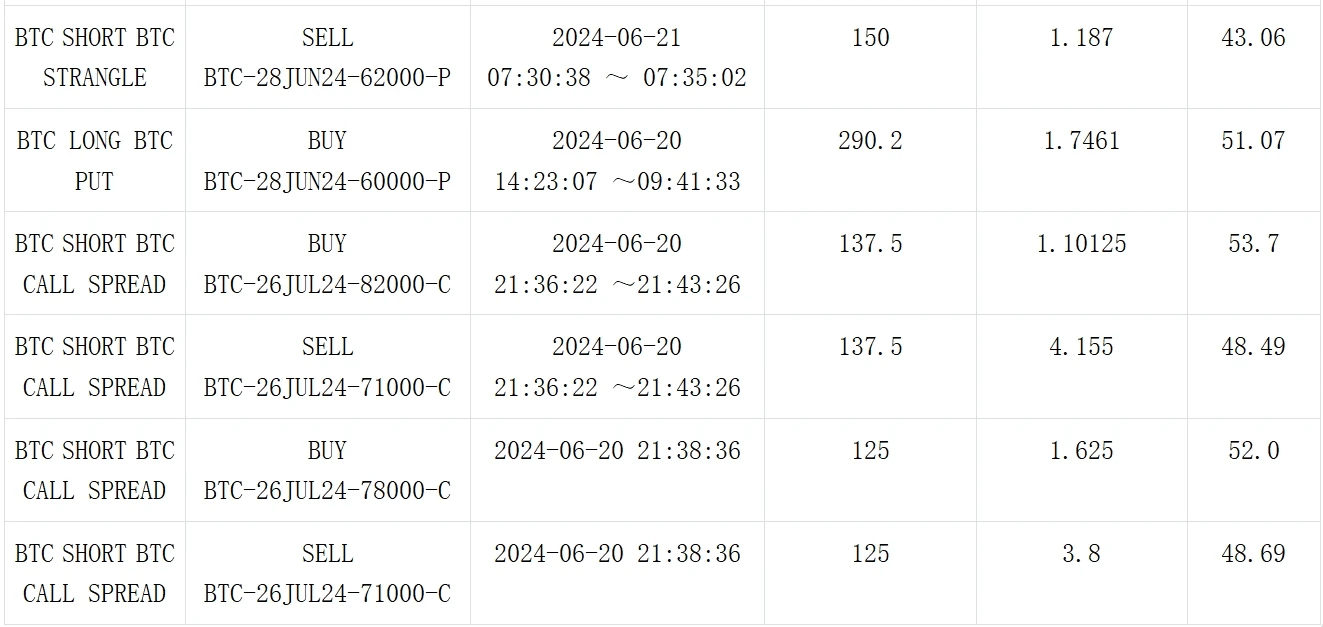

Source: Deribit Block Trade

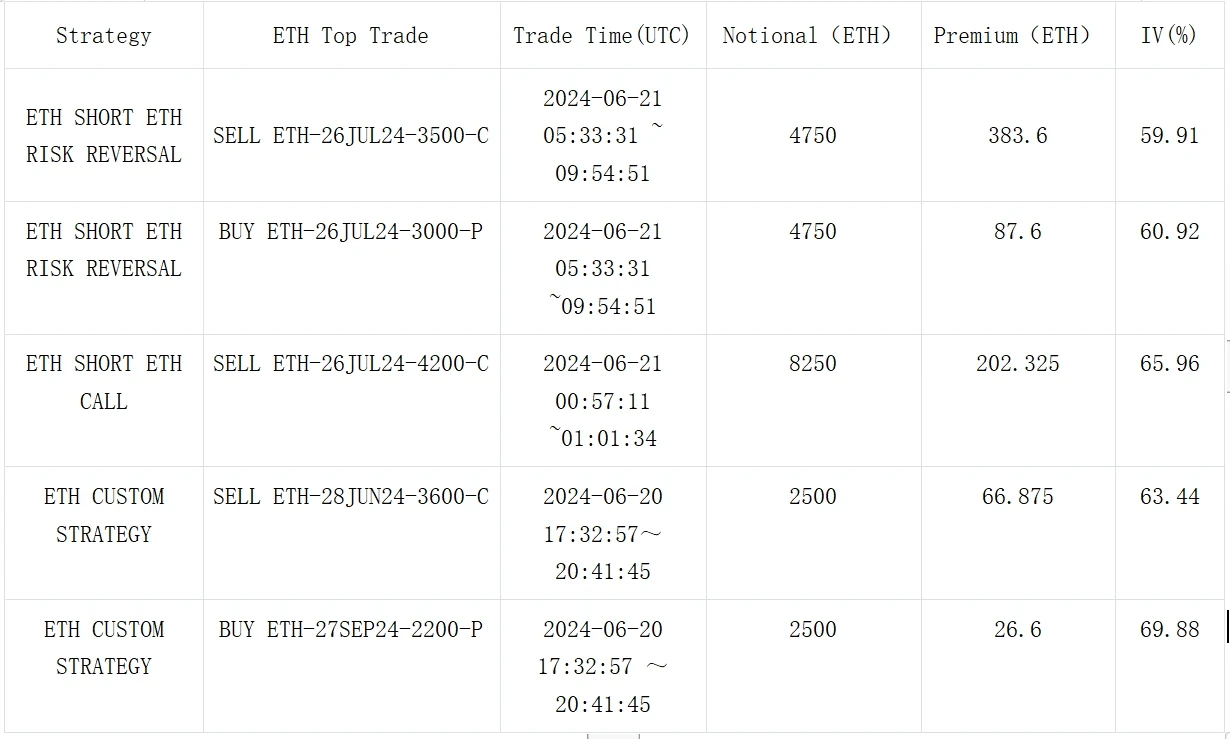

Source: Deribit Block Trade

您可在 ChatGPT 4.0 的 Plugin Store 搜索 SignalPlus ,获取实时加密资讯。如果想即时收到我们的更新,欢迎关注我们的推特账号@SignalPlus_Web3 ,或者加入我们的微信群(添加小助手微信:SignalPlus 123)、Telegram 群以及 Discord 社群,和更多朋友一起交流互动。SignalPlus Official Website:https://d1x7dwosqaosdj.cloudfront.net/images/2024-06-21/4410aefa68c6367ea94a8b85bcb8730b