空头仍在斥资数十亿美元押注数字货币相关股票的涨势最终将结束,哪怕比特币已带动该板块大幅上涨。

根据S3 Partners LLC本周的一份报告,今年做空数字货币股票的头寸总额已增至近110亿美元,其中80%以上的头寸是做空微策略(MicroStrategy)(MSTR.O)和Coinbase(COIN.O)的。

目前,这些“顽固空头”的账面亏损已达到近60亿美元,因为比特币年初至今上涨65%以上,提振了该板块的整体表现。尽管如此,空头仍在加倍押注下跌。S3公司预测分析部门董事总经理Ihor Dusaniwsky表示:

“数字货币股票卖空者一直在涨势中做空——要么押注比特币涨势回调,要么利用空头头寸对冲实际持有比特币的风险。”

在过去30天里,数字货币相关股票的空头继续增加头寸,尤其是针对微策略公司,即使其股价仍在上涨。交易员已投入9.74亿美元押注这家企业软件制造商将倒闭。根据S3的数据,这足以抵消同期Coinbase、Marathon Digital Holdings Inc.(MARA.O)和Hive Digital Technologies Ltd. (HIVE.O)股票的空头回补数量。

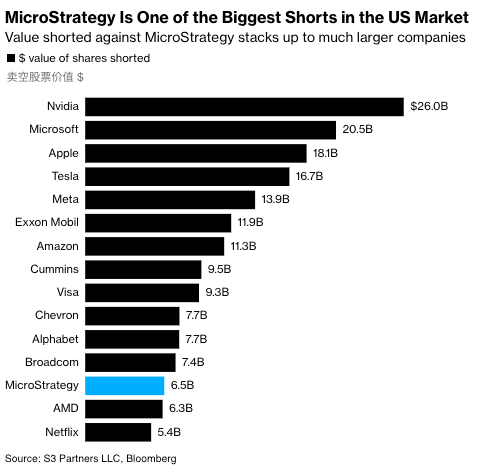

空头头寸已经占微策略股票总流通量的20%以上,使该公司成为美国市场上最受做空的股票之一,与英伟达、微软和苹果等规模大得多的公司相媲美。

当然,如果空头对数字货币相关股票的押注不正确,他们可能会面临更多痛苦。S3报告显示,鉴于微策略、Coinbase和Cleanspark Inc.(CLSK.O) 股价大幅反弹以及可供做空的股票数量有限,许多空头都将面临轧空,也就是被迫买回股票以退出亏损的空头头寸。这会反过来推高做空标的的股价,进一步给其他交易者带来压力。

今年到目前为止,微策略股价上涨了近200%,而Coinbase和Cleanspark分别上涨了约60%和115%。