原创 | Odaily星球日报

作者 | Azuma

北京时间 3 月 25 日晚间,WSJ 报道表示 FTX 已与二十多个买家达成了一笔总价值 8.84 亿美元的交易,以出售其持仓占比约三分之二的人工智能新锐 Anthropic 的股份。

根据后续披露的法庭文件,FTX 计划向 24 名买家出售 2950 万股 Anthropic 股票,其中最主要的买家为总部位于阿布扎比的 ATIC Third International Investment,该公司计划斥资 5 亿美元购入 1660 万股,此外 Jane Street 亦计划支付 1 亿美元购入 330 万股,富达旗下基金则计划使用 5000 万美元买入 150 万股。

此次交易仍须经法院的最终批准,但鉴于 2 月下旬特拉华州破产法院的 John Dorsey 法官已批准了 FTX 推进出售事宜,预计法庭方面并不会成为该交易最终落地的障碍。

2022 年的无心插柳,已成为了债权人的“救命稻草”

随着人工智能概念的兴起,Anthropic 的估值在过去两年间已实现了大幅增长,考虑到 FTX 方面曾在 Anthropic 的 B 轮融资中以领投身份出资 5 亿美元,因此这笔股权投资的增值期望也被许多 FTX 债权人视为拿回本金的最大希望所在。

关于 Anthropic ,这是一家由 OpenAI 前员工创办的人工智能公司,开发有类似于 ChatGPT 的人工智能聊天应用 Claude,如今已被广泛视为 OpenAI 的最大竞争对手之一。

自成立以来,Anthropic 已通过多轮融资获得了数十亿美元的风投注资。

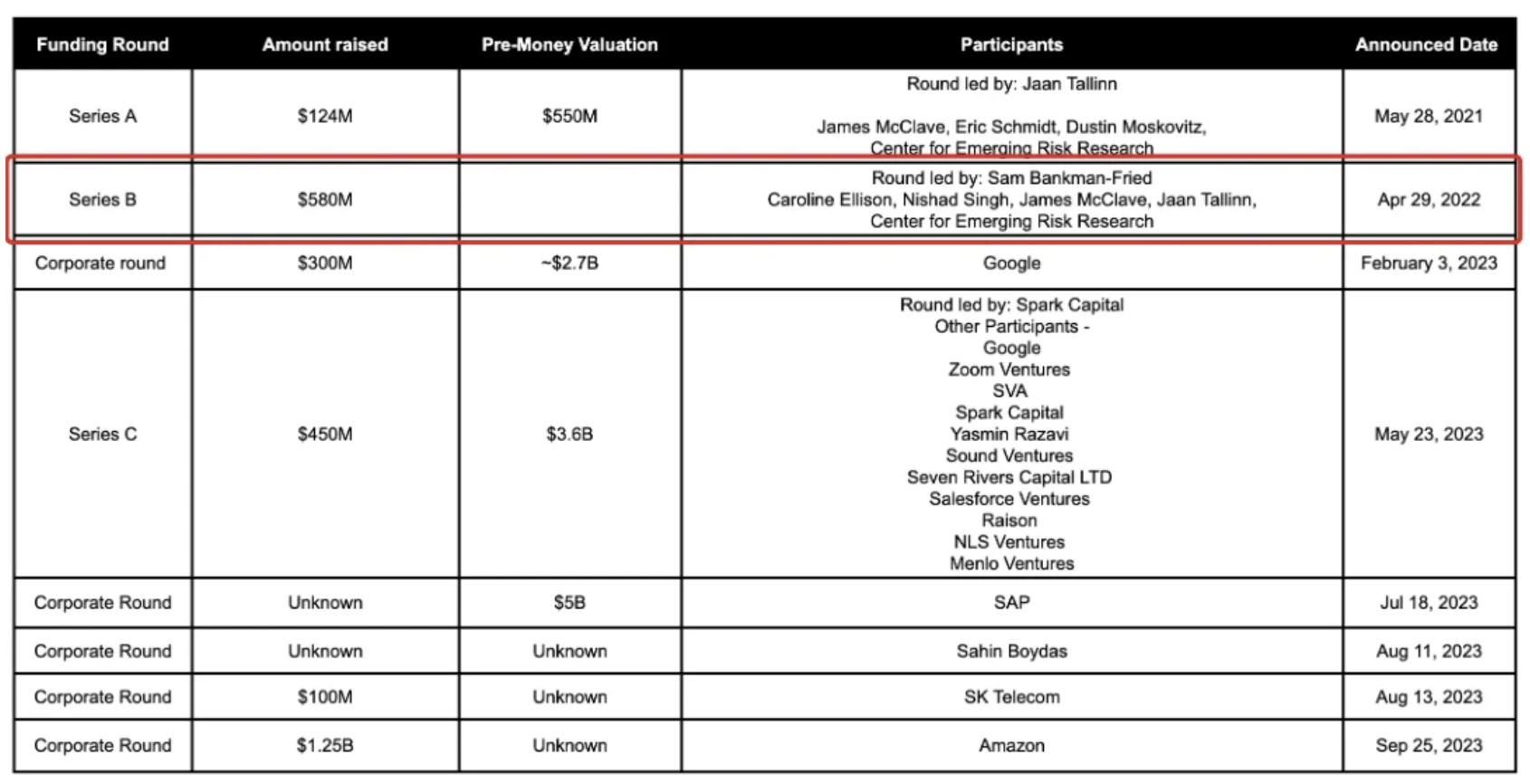

2022 年 4 月,Anthropic 完成了 5.8 亿美元的 B 轮,其中 FTX 方面合计出资 5 亿美元,包括 SBF 本人的领投,以及 FTX 联席首席工程师 Nishad Singh 和 Alameda 前首席执行官 Caroline Ellison 等高管的参投。

此前较长一段时间,关于 B 轮融资的估值情况并无可信披露,因此市场此前也无法获悉 FTX 的具体交易价格和持股比例,但今年 2 月 FTX 在推进 Anthropic 股权出售事宜时已披露了确切的数据 —— 持股比例约为 7.84% 。

去年年底,包括 The Information 在内的多家媒体均报道表示,Anthropic 计划以超过 180 亿美元的估值融资 7.5 万美元,以此价格计算,FTX 所持有的约 7.84% 股权估值超过了 14 亿美元,这一数据与 FTX 当前正在推进的出售价格基本吻合。

回到 FTX 本身的债务问题上。

在 FTX 申请破产之时,其资产缺口约为 90 亿美元,而 2023 年 5 月时 FTX 曾提交资料指出 “迄今已收回了约 70 亿美元的流动资金”。虽然我们并不清楚 FTX 持仓及记账的具体方式(缺口和流动资金均存在因资产价值波动而变化的可能性),但如果用“刻舟求剑”的方式去计算静态数据,Anthropic 的股权价值已可填补剩余的大部分窟窿。此外,考虑到加密货币市场的整体上行,从一些已被标记为 FTX 相关地址的链上数据来看,FTX 一直持有着大量非稳定币资产,这部分资产的价值也会随着市场上行而增长。

预估赔付率逐步攀升,涨幅堪比 Solana

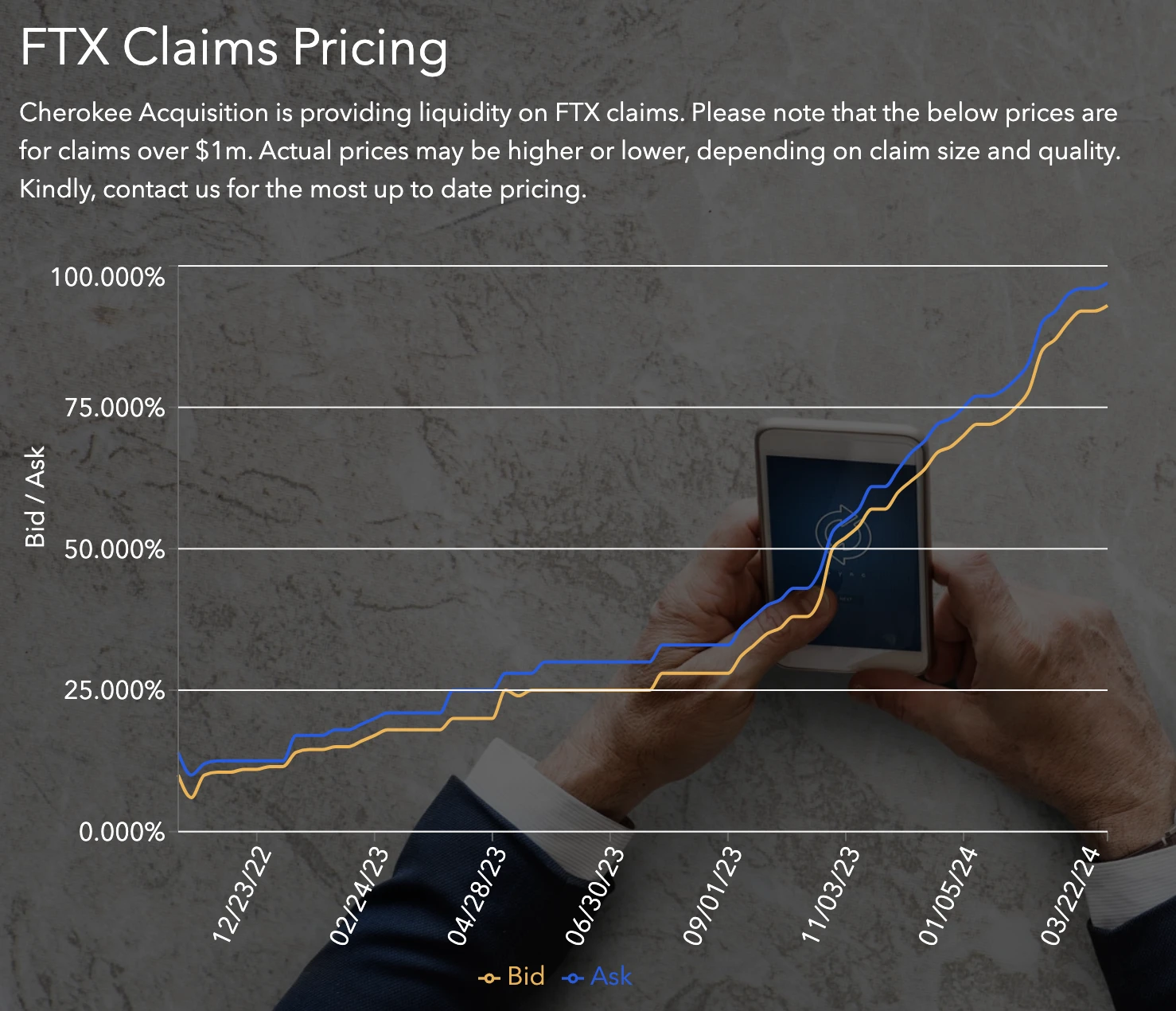

根据专门从事破产索赔并提供 FTX 债权流动性的投资银行 Cherokee Acquisition 所整理的数据,截至 3 月 22 日,FTX 债权的预估赔付率(债权面额估值)已上升至 93% (Bid)至 97% (Ask)之间。

值得一提的是, Cherokee Acquisition 的数据每周更新一次,鉴于 FTX 出售 Anthropic 股份一事已有了确切进展,预计其债权面额估值将在下一次更新数据时(3 月 29 日)继续上涨。

回看 FTX 债权面额估值过去一年多以来的增长态势,从 2022 年 11 月 18 日时 Bid 报价仅有 6% 起,直到今日该债权面额估值已实现了逾 15 倍的增值,这一增长幅度堪比 SBF 曾经的最爱 Solana(SOL)。

从债权交易情绪来看,当前市场对于 FTX 最终将完成近乎全额的债务赔付持有着相当乐观的态度,对于每一个因 FTX 事件而受损的用户而言,这或许就是最好的结果了吧。

文章的最后,聊一个小插曲吧。

2023 年 6 月时,FTX 也曾险些“卖飞” Anthropic。

知情人士曾透露称负责处理 FTX 破产案的投资银行 Perella Weinberg 一直在考虑出售 FTX 所持有的 Anthropic 股权,当时 Anthropic 刚刚完成的 C 轮融资估值“仅”为 41 亿美元……不过在对潜在的竞标者进行了为期数月的调查后,Perella Weinberg 最终还是选择了 HODL。

如今的市场走势已验证了这一决断的正确性。