Author: Four Pillars

Compiled by: Baihua Blockchain

Core Points

-

HIP-3 removes the technical barriers to launching new perpetual contract markets, enabling a demand-driven market creation model. This shifts decentralized exchanges (DEX) from a player-versus-player (PvP) dynamic competing with centralized exchanges (CEX) for existing liquidity to a player-versus-environment (PvE) expansion path extending into non-crypto assets and real-world data.

-

The market is transitioning from narrative-driven growth to a cash flow-driven, sustainability-oriented valuation system. Only a few projects with real revenue flowing to their tokens (like Hyperliquid and Pump.fun) are likely to dominate the next cycle.

-

Prediction markets transform once-private or illegal gambling activities into public on-chain data and serialized data of collective expectations. This creates real-time probability signals and alternative data that financial institutions, data providers, and AI models can use as an economic mechanism for information aggregation and probability estimation.

-

Regulation has created a fragmented regime: Prediction markets are trending towards institutionalization in the West, while being suppressed in Asia. This constitutes a major short-term constraint but also paves the way for prediction markets to evolve into "infrastructure that converts collective beliefs into information and markets."

1. How HIP-3 Enables a PvE-Style New Growth Pattern

The business model of exchanges is undergoing a transformation.

Centralized Exchanges (CEX) maintain their position due to structural advantages based on institutional trust (fiat on/off-ramps, custody, and regulatory access). This makes them the natural entry point for institutional capital and provides stability in terms of liquidity and operational reliability. However, these same regulatory obligations, internal controls, and custody infrastructure also incur high fixed costs. Consequently, CEXs have slower experimentation and decision-making speeds, limiting their pace of innovation.

In contrast, Decentralized Exchanges (DEX) grow through incentive structures. They natively coordinate rewards between LPs, traders, and builders on-chain. But previously, launching a new exchange or market required a team to build a matching engine, margin & liquidation system, and oracle from scratch. This created an extremely high technical barrier to entry.

HIP-3 removes this barrier.

Hyperliquid now allows anyone who stakes 500,000 HYPE to deploy their own perpetual contract market using the same CLOB engine, margin logic, and liquidation system as the main site. The technical burden of building an exchange is eliminated. Market creation becomes a standardized on-chain deployment process; it requires capital and a reliable oracle, not an entire engineering team. The barrier shifts from technical capability to capital and oracle design.

This change is more than just an efficiency improvement; it changes where innovation happens.

Builders can now experiment with different liquidity structures, fee designs, oracle definitions, and leverage limits without rebuilding the backend. The challenge becomes identifying the "demand surface" (i.e., how many people want to speculate on something) and anchoring it to a reliable oracle. Effectively, a market can now be composed of three components: Market + Oracle + Demand.

This expands the range of assets that can be listed.

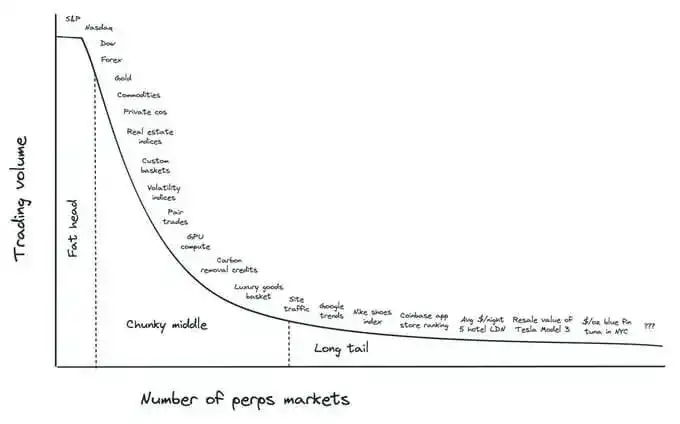

As described by Ventuals founder Alvin Hsia, the "Fat Head" consists of asset classes already covered by traditional finance (index products, forex, commodities); the "Chunky Middle" includes pre-IPO equity, real-world datasets, and commodity indices; and the "Long Tail" extends to niche signals like local real estate prices, product premiums, or cultural trend indices. Traditional finance cannot easily commoditize these data points, but on-chain settlement systems can. HIP-3 essentially enables a demand-driven market creation model.

Source: X (@alvinhsia)

This transforms DEXs from competitors to CEXs into structurally different entities.

Instead of fighting for fixed crypto-native liquidity (a PvP dynamic), HIP-3 allows DEXs to expand into non-crypto assets and real-world data. This brings new traffic, new users, and new forms of demand—a PvE dynamic where the market size increases rather than being redistributed. It also deepens protocol-level revenue.

A clear example is Hyperliquid's XYZ100 market, which accumulated over $13 billion in trading volume within three weeks of launch, demonstrating how quickly new asset classes can scale when infrastructure is standardized.

In short, CEXs continue to provide stability and regulatory access, but HIP-3-based perpetual DEXs gain an advantage in speed, experimentation, and asset expansion. They are not substitutes but distinct growth paths. The competitive advantage of exchanges will shift from backend engineering to market design and user experience, and leadership will depend on which protocol can translate this into sustainable value.

2. From Narrative-Driven Valuation to Cash Flow-Driven Valuation

The market in 2025 is fundamentally different from previous cycles.

The environment of abundant liquidity that once lifted all assets is gone. Capital is now selective. Prices reflect actual performance more than narratives, and projects that cannot generate revenue are being naturally weeded out. Most altcoins have not recovered their 2021 highs, while protocols with clear revenue streams have shown relative strength even during market pullbacks.

The arrival of institutional capital has solidified this shift.

Traditional Finance (TradFi) frameworks are being directly applied to crypto. Revenue, net profit, fee generation, user activity, and profit distribution are becoming primary metrics for project evaluation. The market is moving away from valuing projects based on "storytelling" or anticipated growth. Only projects with real revenue flowing back to their tokens will command higher market valuations.

In this context, Uniswap's recent proposal to activate the Fee Switch is symbolic. A flagship DeFi protocol explicitly choosing to link cash flow to token value signals that fundamentals (not narratives) are now at the core of market pricing.

A group of clear front-runners has emerged.

Hyperliquid (HYPE) and Pump.fun (PUMP) are classic cases:

-

Hyperliquid is the largest perpetual DEX by volume, open interest (OI), and number of traders. As of November 2025, cumulative trading volume reached $3.1 trillion, with open interest at $9 billion. Notably, Hyperliquid uses 99% of perpetual contract fees to buy back HYPE, directly linking protocol cash flow to token value. Total buybacks have reached 34.4 million HYPE (approx. $1.3 billion), accounting for about 10% of the circulating supply.

-

Pump.fun is the leading memecoin trading platform, generating approximately $1.1 billion in cumulative fees. Its buyback program has purchased about 830,000 SOL (approx. $165 million), equivalent to 10.3% of its (inferred) circulating value.

Other projects also show strong revenue momentum:

-

Aave (AAVE) and Jupiter (JUP) consistently post stable and growing cash flows. Aave's annual revenue grew from $29.75 million in 2023 to $99.39 million in 2025. Jupiter's revenue growth is even more dramatic, soaring from $1.42 million in 2023 to $246 million in 2025.

-

Coinbase (COIN), although a public stock, also benefits from the increasingly clear path to token issuance for the Base chain. Coinbase has broadened its revenue structure: Q3 2025 subscription and services revenue reached $746.7 million (up 13.9% quarter-over-quarter).

This shift is spreading from individual dApps to L1 and L2 ecosystems. Technical prowess or investor backing alone is no longer sufficient. Chains with real users, real transactions, and protocol-level revenue are gaining stronger market recognition. The core evaluation metric is becoming the sustainability of economic activity.

In summary, the market is undergoing a structural transformation. The 2026 market is likely to reorganize around these performance-backed participants.

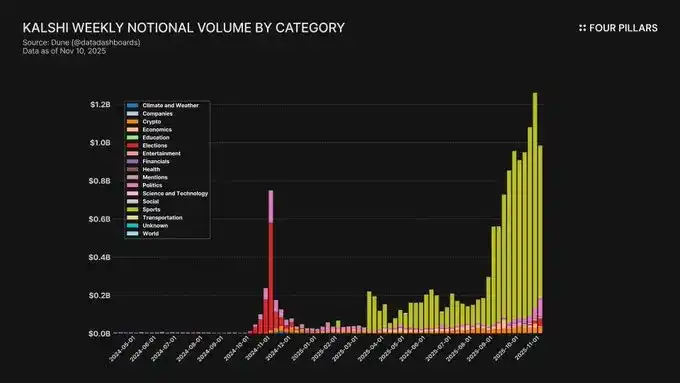

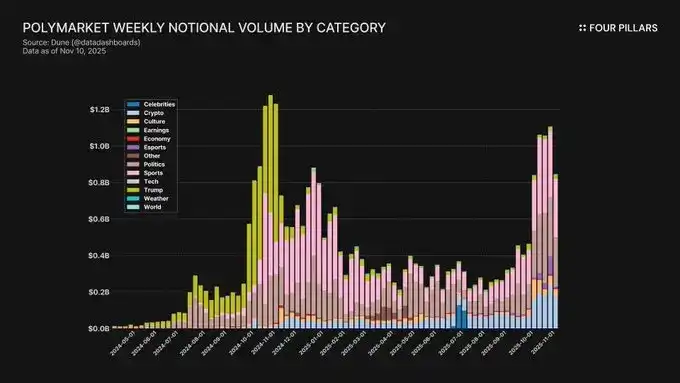

3. Quantifying Market Expectations Through Prediction Markets

Prediction markets are an experiment that transforms once-private or illegal gambling activities into public on-chain data. The core idea is that they quantify the probability people assign to future events by having them put real skin in the game for their beliefs. This makes them not just venues for speculation, but economic mechanisms for aggregating information and estimating probabilities.

Prediction markets have grown rapidly since 2024: As of October 2025, weekly nominal trading volume is approximately $2.5 billion, with over 8 million weekly trades. Polymarket commands 70–75% of the activity share, while Kalshi's share has climbed to around 20% after receiving CFTC approval and expanding into sports and political markets.

The uniqueness of prediction market data lies in: Polls, social media sentiment, and institutional research are often slow and costly. Prediction markets price expectations in real-time. For example, Polymarket reflected an increase in Donald Trump's 2024 election win probability significantly earlier than traditional polls.

Effectively, prediction markets create serialized data of collective expectations. These curves serve as real-time probability signals for political, economic, sporting, and technological events. Financial institutions and AI models are increasingly viewing these markets as alternative data sources (Alt-data) for quantifying expectations.

Source: Grayscale Research

From an institutional perspective, prediction markets represent not the "digitization of gambling" but the "financialization of uncertainty." Since prices reflect consensus probabilities, macro traders can use them for risk management. Kalshi already offers markets tied to inflation, employment data, and interest rate decisions, attracting significant hedging interest.

As prediction markets mature, they create a new value chain: Market (generates signal) → Oracle (resolves outcome) → Data (standardized dataset) → Application (consumed by finance, media, AI).

The current main obstacle is regulation:

-

Asia: Regions like South Korea, Singapore, and Thailand mostly take a prohibitive stance, classifying them as illegal gambling and penalizing users.

-

West: The US regulates prediction markets as "event contracts" under the CFTC. Kalshi operates legally with a DCM license, and Polymarket plans to re-enter the US market in 2025 through the acquisition of QCX.

This regulatory difference creates a split: The West moves towards institutionalization, while suppression occurs in Asia. Although this is a short-term constraint, in the long run, prediction markets will evolve into infrastructure that converts collective beliefs into information. They will shift from "markets that interpret information" to "markets that produce information," reinforcing a world where "price becomes the primary expression of collective expectation."

Related Questions

QWhat is the core innovation introduced by HIP-3 on Hyperliquid, and how does it change the dynamics for DEXs?![]()

AHIP-3 removes the technical barriers to launching new perpetual markets by allowing anyone staking 500,000 HYPE to deploy their own perpetual contract market using Hyperliquid's existing CLOB engine, margin logic, and清算 system. This shifts market creation from a technical challenge to a capital and oracle design challenge, enabling a demand-driven model. It transforms DEXs from competing with CEXs in a PvP (player vs. player) dynamic for existing crypto liquidity to a PvE (player vs. environment) expansion into non-crypto assets and real-world data, thereby growing the total market size.

QHow is the market's valuation paradigm shifting according to the article, and which projects are leading this change?![]()

AThe market is shifting from a narrative-driven valuation paradigm to a cash flow-driven, sustainability-oriented one. Valuation is now based on real revenue, profit, fee generation, and user activity, with capital flowing selectively to projects that demonstrate actual performance. Leading projects include Hyperliquid (HYPE), which directs 99% of perpetual fees to buy back HYPE, and Pump.fun (PUMP), which uses fees to buy back SOL. Other strong performers include Aave, Jupiter, and Coinbase, all of which show substantial and growing protocol revenue.

QWhat unique value do prediction markets provide beyond speculation, and how are they being used by institutions?![]()

APrediction markets quantify the probability of future events by allowing people to stake money on their beliefs, transforming private or illegal gambling activities into public, on-chain data. They generate real-time probability signals and serialized data on collective expectations, serving as an alternative data source (alt-data) for金融机构, data providers, and AI models. Institutions use them for risk management, hedging (e.g., against inflation or employment data), and as a mechanism for information aggregation and probability estimation, making them a tool for the 'financialization of uncertainty.'

QWhat is the current regulatory landscape for prediction markets, and how does it differ between regions?![]()

AThe regulatory landscape is split. In Asia, countries like Korea, Singapore, and Thailand largely suppress prediction markets, categorizing them as illegal gambling and penalizing users. In the West, particularly the US, prediction markets are regulated as 'event contracts' by the CFTC. Kalshi operates legally with a DCM license, and Polymarket plans to re-enter the US market in 2025 by acquiring QCX. This creates a divergence where Western markets are becoming institutionalized, while Asian markets face suppression.

QHow does the article characterize the new competitive advantage for DEXs following innovations like HIP-3?![]()

AFollowing innovations like HIP-3, the competitive advantage for DEXs shifts from backend engineering and technical prowess to market design, user experience, and the ability to identify and capitalize on 'demand surfaces.' The key is to recognize what assets people want to speculate on (e.g., niche real-world data, local indices) and pair them with reliable oracles. Leadership will depend on which protocol can best convert these innovations into sustainable value through experimentation with liquidity structures, fee designs, and leverage limits, all while expanding into new asset classes.