Author:Stacy Muur

Compiled by: Deep Tide TechFlow

Summary:

-

Institutions become the marginal buyers of crypto assets.

-

Real-World Assets (RWAs) evolve from a narrative concept to an asset class.

-

Stablecoins become both a "killer app" and a systemic vulnerability.

-

Layer 2 (L2) networks consolidate into a "winner-take-all" landscape.

-

Prediction markets evolve from toy applications into financial infrastructure.

-

AI & Crypto (AI × Crypto) shifts from hype narrative to practical infrastructure.

-

Launchpads industrialize, becoming the internet's capital markets.

-

Tokens with high Fully Diluted Valuation (FDV) and low float prove to be structurally uninvestable.

-

InfoFi experiences a boom, inflation, and then a bust.

-

Consumer crypto returns to the mainstream, but through Neobanks rather than Web3 apps.

-

Global regulation gradually normalizes.

In my view, 2025 is an inflection point for the crypto space: it transitions from a speculative cycle to foundational, institutionally-scaled structures.

We witnessed a repositioning of capital flows, a restructuring of infrastructure, and the maturation or collapse of emerging sectors. Headlines about ETF inflows or token prices are merely the surface. My analysis reveals the deeper structural trends underpinning the new paradigm for 2026.

Below, I will break down the 11 pillars of this transformation, each supported by specific data and events from 2025.

1. Institutions Become the Dominant Force in Crypto Fund Flows

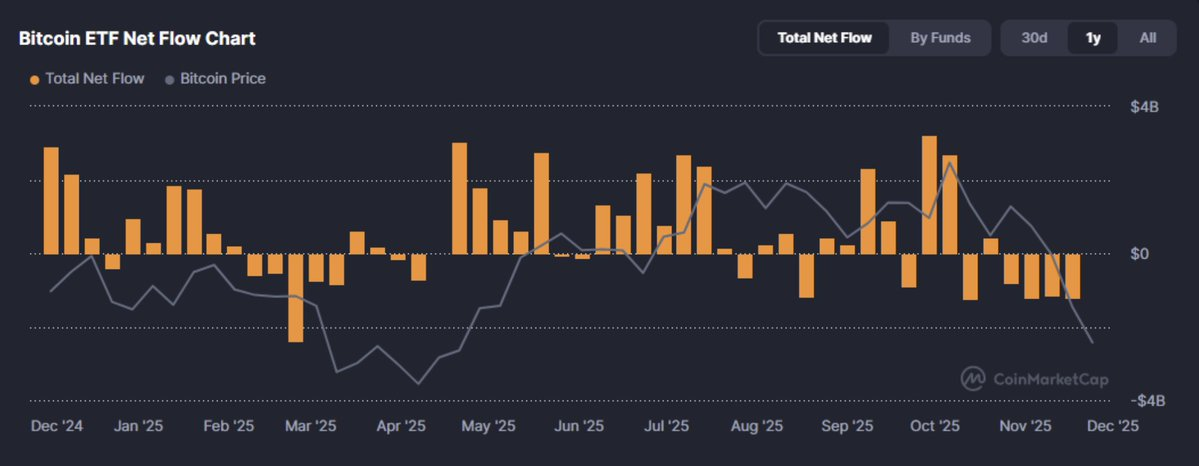

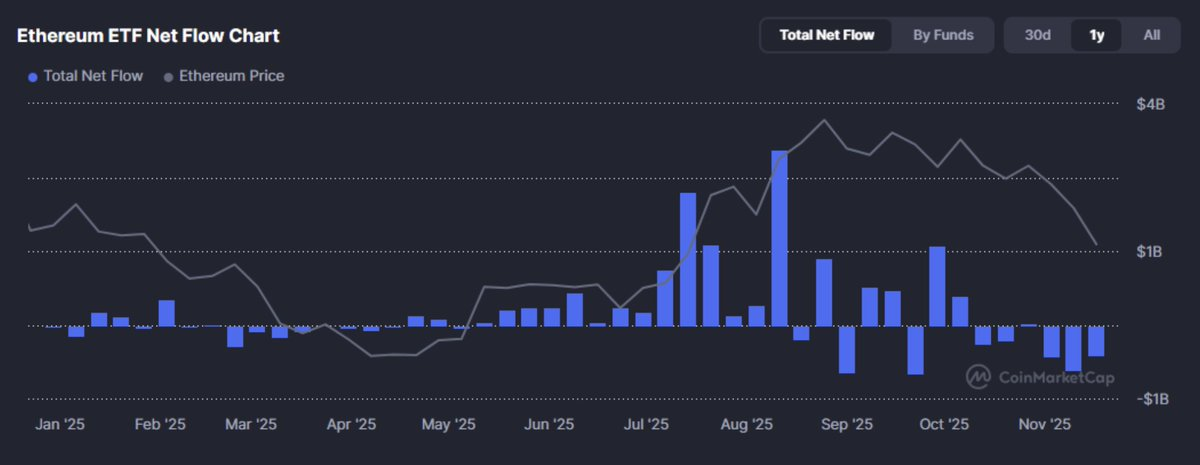

I believe 2025 witnessed institutions taking full control of crypto market liquidity. After years of watching from the sidelines, institutional capital finally surpassed retail to become the market's dominant force.

In 2025, institutional capital didn't just "enter" the crypto market; it crossed a significant threshold. For the first time, the marginal buyer of crypto assets shifted from retail to asset allocators. In Q4 alone, weekly inflows into US spot Bitcoin ETFs exceeded $3.5 billion, led by products like BlackRock's IBIT.

These flows weren't random but represented a structurally mandated reallocation of risk capital. Bitcoin is no longer seen as a curiosity-driven asset but as a macro tool with portfolio utility: digital gold, a convex inflation hedge, or simply an uncorrelated asset exposure.

However, this shift also has a dual impact.

Institutional flows are less reactive but more sensitive to interest rates. They compress market volatility while also tethering crypto markets to the macroeconomic cycle. As one CIO stated, "Bitcoin is now a liquidity sponge with a compliance wrapper." Its narrative risk as a globally recognized store of value is significantly reduced; however, its interest rate risk remains.

The implications of this flow shift are profound: from fee compression on exchanges to the reshaping of demand curves for yield-bearing stablecoins and tokenized real-world assets (RWAs).

The next question is no longer whether institutions will come, but how protocols, tokens, and products adapt to capital that is driven by Sharpe Ratios rather than market hype.

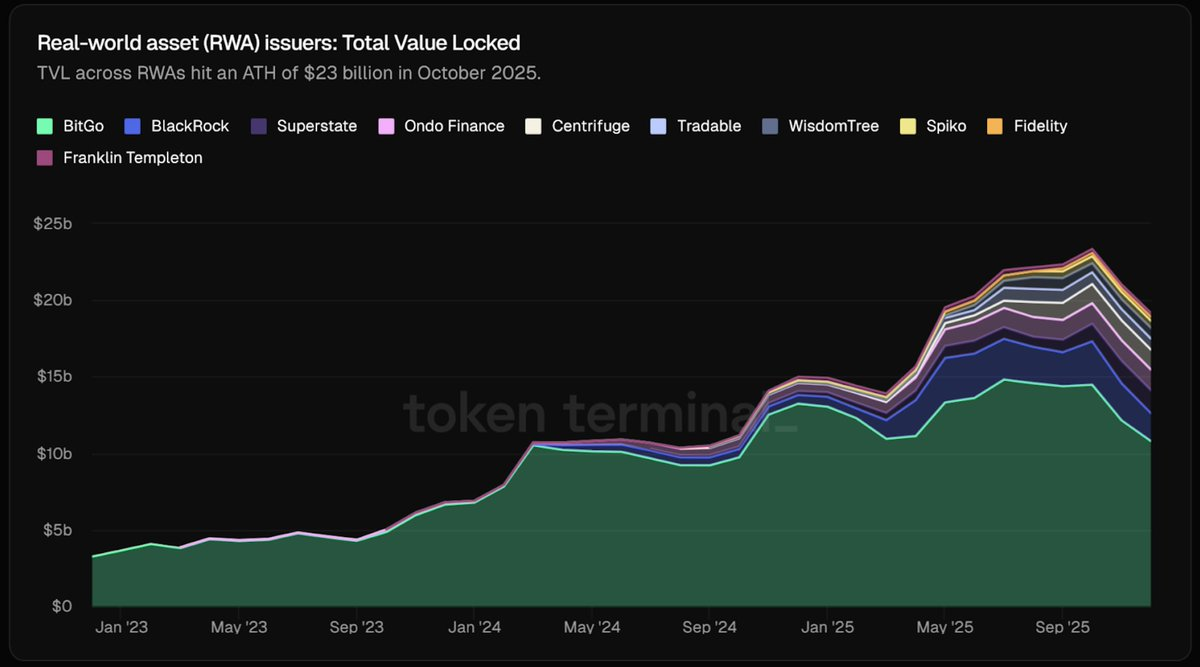

2. Real-World Assets (RWAs) Evolve from Concept to a Real Asset Class

In 2025, tokenized real-world assets (RWAs) transitioned from a concept to capital market infrastructure.

We now see substantial supply: as of October 2025, the total market cap of RWA tokens exceeded $23 billion, a nearly 4x surge year-over-year. Roughly half of this consists of tokenized US Treasuries and money market strategies. With institutions like BlackRock issuing $500 million in Treasuries via BUIDL, this is no longer a marketing gimmick but vaults collateralized by on-chain insured debt, not unbacked code.

Simultaneously, stablecoin issuers began backing reserves with short-term bills, and protocols like Sky (formerly Maker DAO) integrated on-chain commercial paper into their collateral pools.

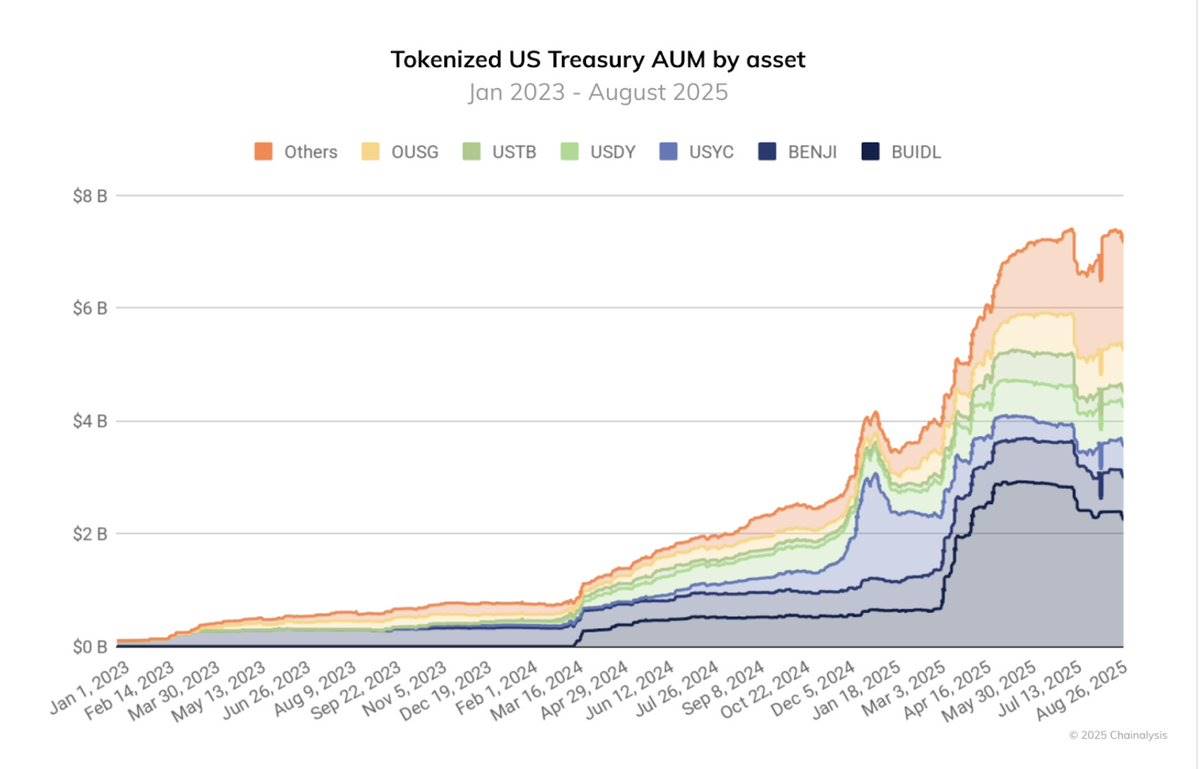

Treasury-backed stablecoins are no longer fringe but foundational to the crypto ecosystem. The Assets Under Management (AUM) of tokenized funds nearly quadrupled in 12 months, from around $2 billion in August 2024 to over $7 billion by August 2025. Meanwhile, RWA infrastructure from institutions like JPMorgan and Goldman Sachs moved from testnets to production environments.

In other words, the line between on-chain liquidity and off-chain asset classes is crumbling. Traditional finance asset allocators no longer need to buy tokens *representing* real assets; they now hold assets issued natively in on-chain form. This shift from synthetic representation to actual tokenization is one of 2025's most impactful structural advances.

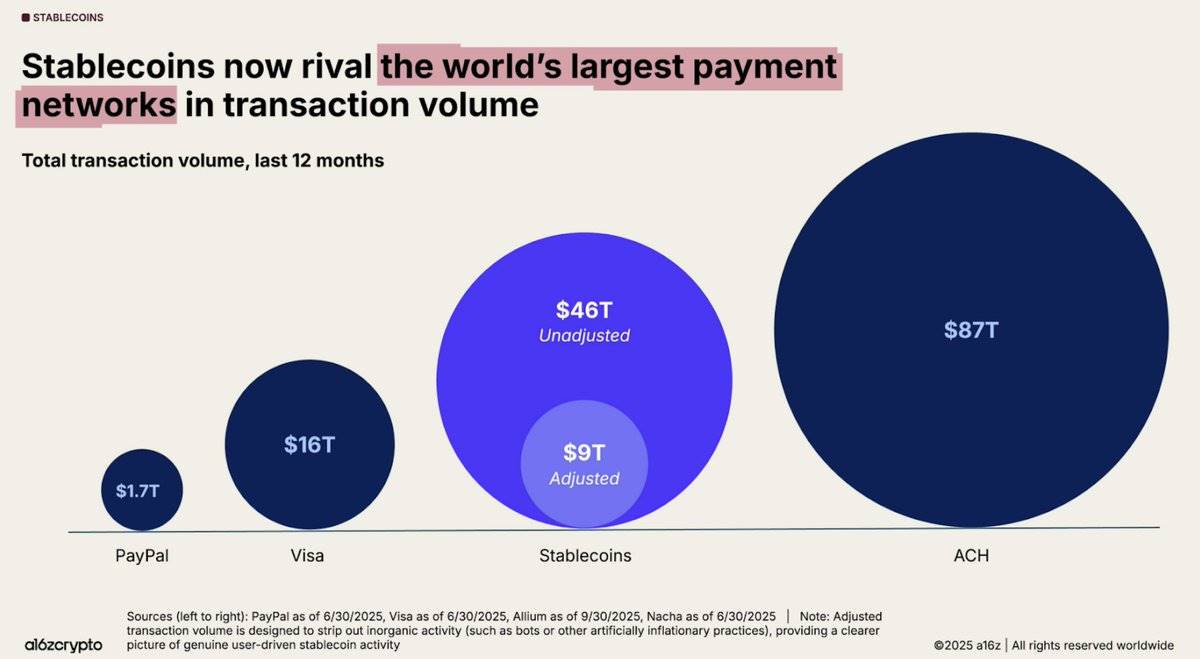

3. Stablecoins: Both a "Killer App" and a Systemic Vulnerability

Stablecoins delivered on their core promise: programmable dollars at scale. Over the past 12 months, on-chain stablecoin volume reached $46 trillion, up 106% year-over-year, averaging nearly $4 trillion per month.

From cross-border settlements to ETF infrastructure to DeFi liquidity, these tokens became the monetary hub of crypto, making blockchains functional dollar networks. Yet, stablecoin success also revealed systemic fragility.

2025 exposed the fault lines in yield-bearing and algorithmic stablecoins, especially those reliant on endogenous leverage for backing. Stream Finance's XUSD crashed to $0.18, vaporizing $93 million in user funds and leaving $285 million in protocol-level debt.

Elixir's deUSD collapsed due to a large loan default. USDx on AVAX fell amid allegations of manipulation. Each case revealed how opaque collateral, rehypothecation, and concentration risks can lead to de-pegging.

The yield chase of 2025 amplified this fragility. Capital flooded into yield-bearing stablecoins, some offering APYs as high as 20%–60% via complex vault strategies. Platforms like @ethena_labs, @sparkdotfi, and @pendle_fi absorbed billions, as traders chased structured yields built on synthetic dollars. Yet, with collapses like deUSD, XUSD, etc., it became clear that DeFi hadn't matured; it had concentrated. Nearly half of Ethereum's Total Value Locked (TVL) is concentrated in @aave and @LidoFinance, while other capital pools cluster around a handful of Yield-Bearing Stablecoin (YBS) strategies. This results in a fragile ecosystem built on over-leverage, recursive money flows, and shallow diversification.

So, while stablecoins power the system, they also stress it. We're not saying stablecoins are "broken"; they are critical to the industry. However, 2025 proved that stablecoin design matters as much as its function. As we move into 2026, the integrity of dollar-denominated assets is a primary concern, not just for DeFi protocols but for everyone allocating capital or building on-chain financial infrastructure.

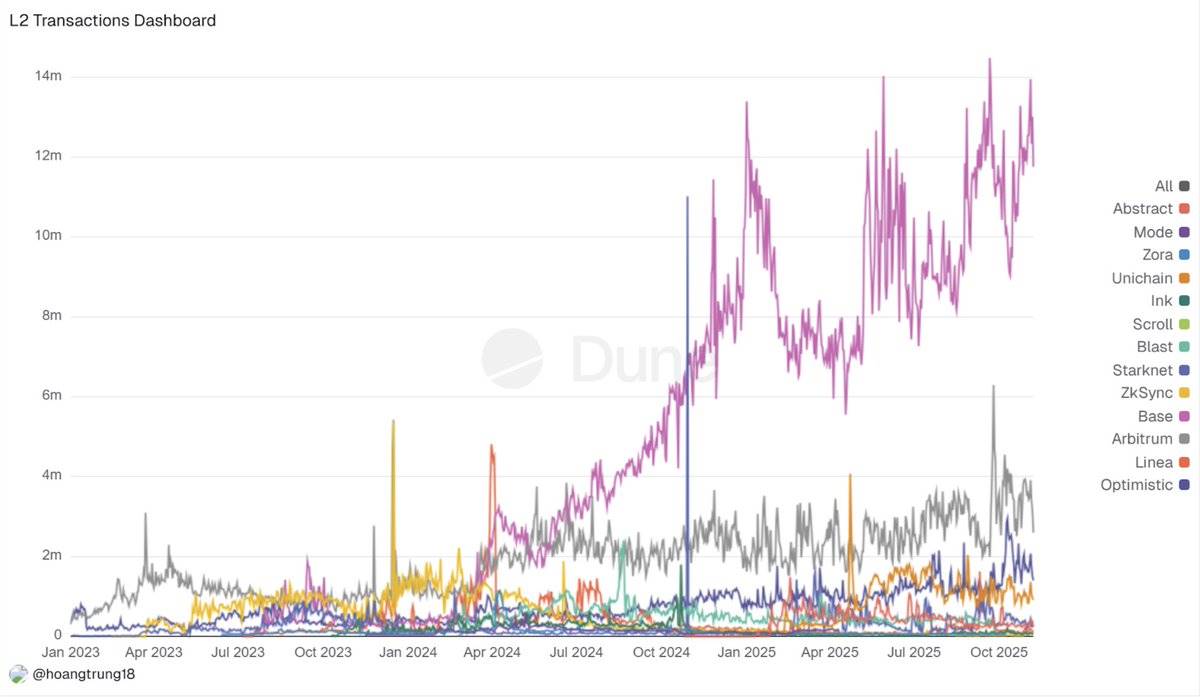

4. L2 Consolidation and the Chain Stack Disillusionment

In 2025, Ethereum's "rollup-centric" roadmap collided with market reality. What was once dozens of L2s on L2Beat evolved into a "winner-take-most" landscape: @arbitrum, @base, and @Optimism captured the majority of new TVL and flows, while smaller rollups saw revenues and activity drop 70%–90% after incentives ended. Liquidity, MEV bots, and arbitrageurs followed depth and tight spreads, reinforcing this flywheel and leaving edge chains with dried-up order flow.

Meanwhile, bridge volumes surged, hitting $56.1 billion in July 2025 alone, making it clear that "everything is a rollup" still meant "everything is fragmented." Users still juggled isolated balances, L2-native assets, and duplicated liquidity.

To be clear, this isn't failure; it's consolidation. Fusaka achieved 5–8x blob throughput, zk-appchains like @Lighter_xyz hit 24,000 TPS, and emerging specialized solutions (e.g., Aztec/Ten for privacy, MegaETH for hyper-performance) all show that a few execution environments are pulling ahead.

The rest go into "hibernation mode" until they can prove a moat deep enough that leaders can't simply fork their advantages.

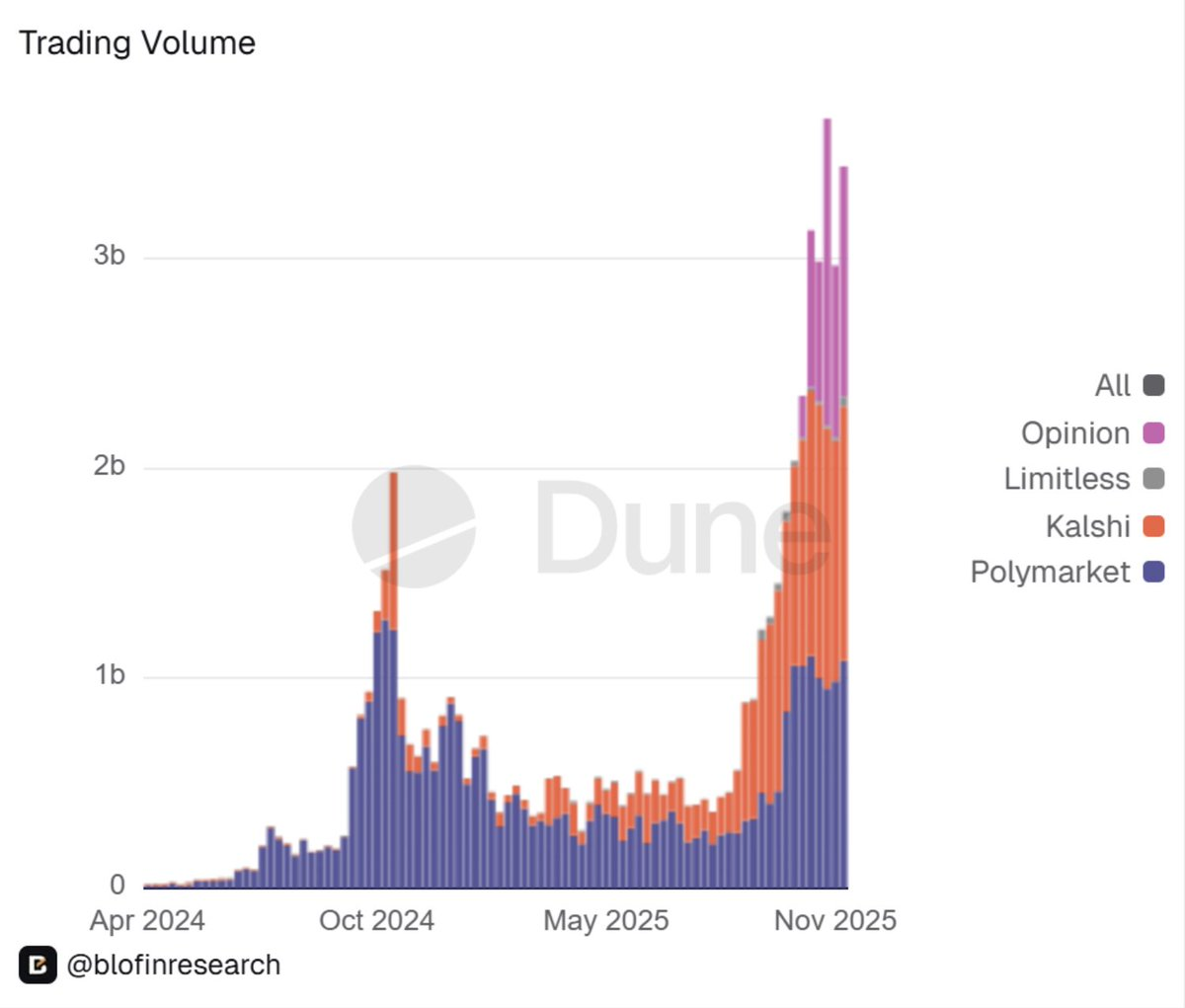

5. The Rise of Prediction Markets: From Fringe Tool to Financial Infrastructure

Another major surprise of 2025 was the formal legitimization of prediction markets.

Once seen as fringe curiosities, prediction markets are now integrating into financial infrastructure. Long-time industry leader @Polymarket re-entered the US in a regulated form: its US arm gained CFTC approval as a Designated Contract Market. Additionally, ICE reportedly deployed tens of capital, nearing a $10 billion valuation. The flows followed.

Prediction markets jumped from "fun niche" to billions in weekly volume, with @Kalshi alone processing hundreds of billions in event contracts in 2025.

I see this as markets on blockchains transitioning from "toys" to genuine financial infrastructure.

Mainstream sportsbooks, hedge funds, and native DeFi managers now treat Polymarket and Kalshi as prediction tools, not entertainment. Crypto projects and DAOs are starting to use these order books for real-time governance and risk signals.

However, this "weaponization" of DeFi is a double-edged sword. Regulatory scrutiny will intensify, liquidity remains highly concentrated around specific events, and the correlation between "prediction markets as signals" and real-world outcomes remains unproven under stress.

Looking to 2026, it's clear: event markets are now in the institutional purview alongside options and perps. Portfolios will need a clear view on whether—and how—to allocate to such exposures.

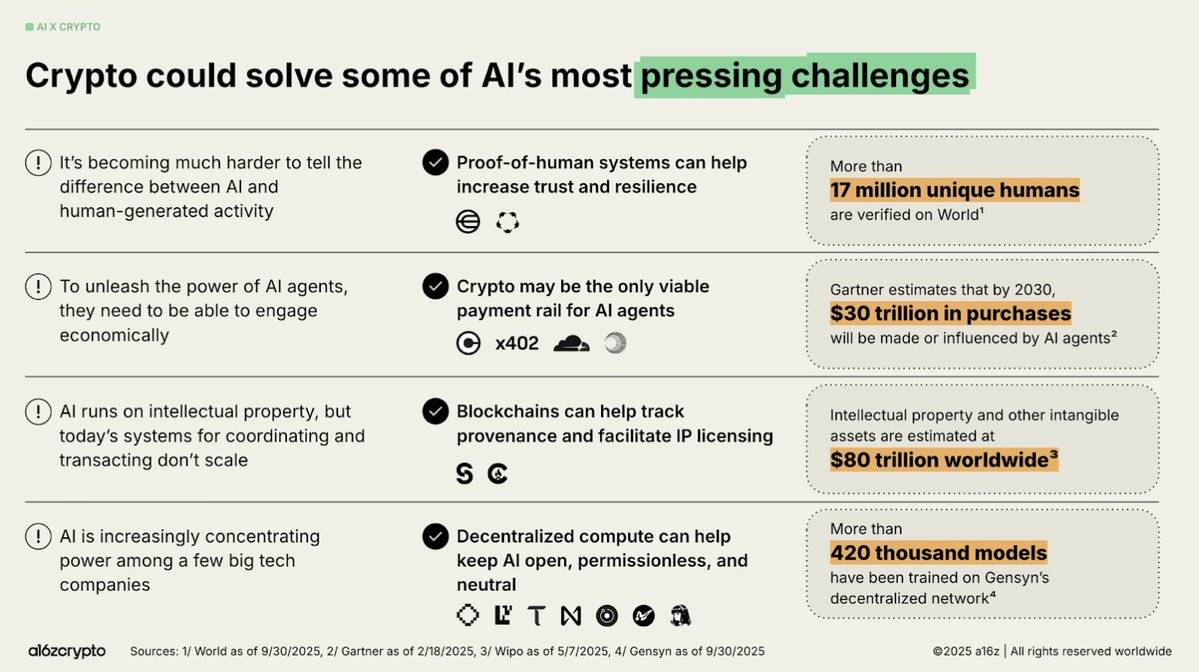

6. AI & Crypto Convergence: From Hype to Practical Infrastructure

In 2025, the intersection of AI and crypto moved from noisy narrative to structured, practical application.

I see three themes defining the year:

First, the Agentic Economy shifted from a speculative concept to an operational reality. Protocols like x402 enabled AI agents to trade autonomously for stablecoins. Circle's USDC integrations, plus the rise of orchestration frameworks, reputation layers, and verifiable systems (e.g., EigenAI, Virtuals) showed that useful AI agents need to collaborate, not just reason.

Second, decentralized AI infrastructure became a core pillar of the space. Bittensor's Dynamic TAO upgrade and December halving re-established it as "Bitcoin for AI"; NEAR's chain abstraction drove real intent volume; and @rendernetwork, ICP, and @SentientAGI validated decentralized compute, model provenance, and hybrid AI networks. Clearly, infrastructure commanded a premium, while "AI-wrapper" value decayed.

Third, vertical integration of utility accelerated.

@almanak's AI swarms deployed quant-grade DeFi strategies, @virtuals_io generated $2.6M in fees on Base, and bots, prediction markets, and geospatial networks became credible agent environments.

The shift from "AI-wrapping" to verifiable agents and bot integrations suggests product-market fit is maturing. However, trust infrastructure remains a critical missing piece, and hallucination risk is still a cloud over autonomous trading.

Overall, end-2025 sentiment is bullish on infrastructure, cautious on agent utility, and broadly expects 2026 could be the year of verifiable, economically valuable on-chain AI breakthroughs.

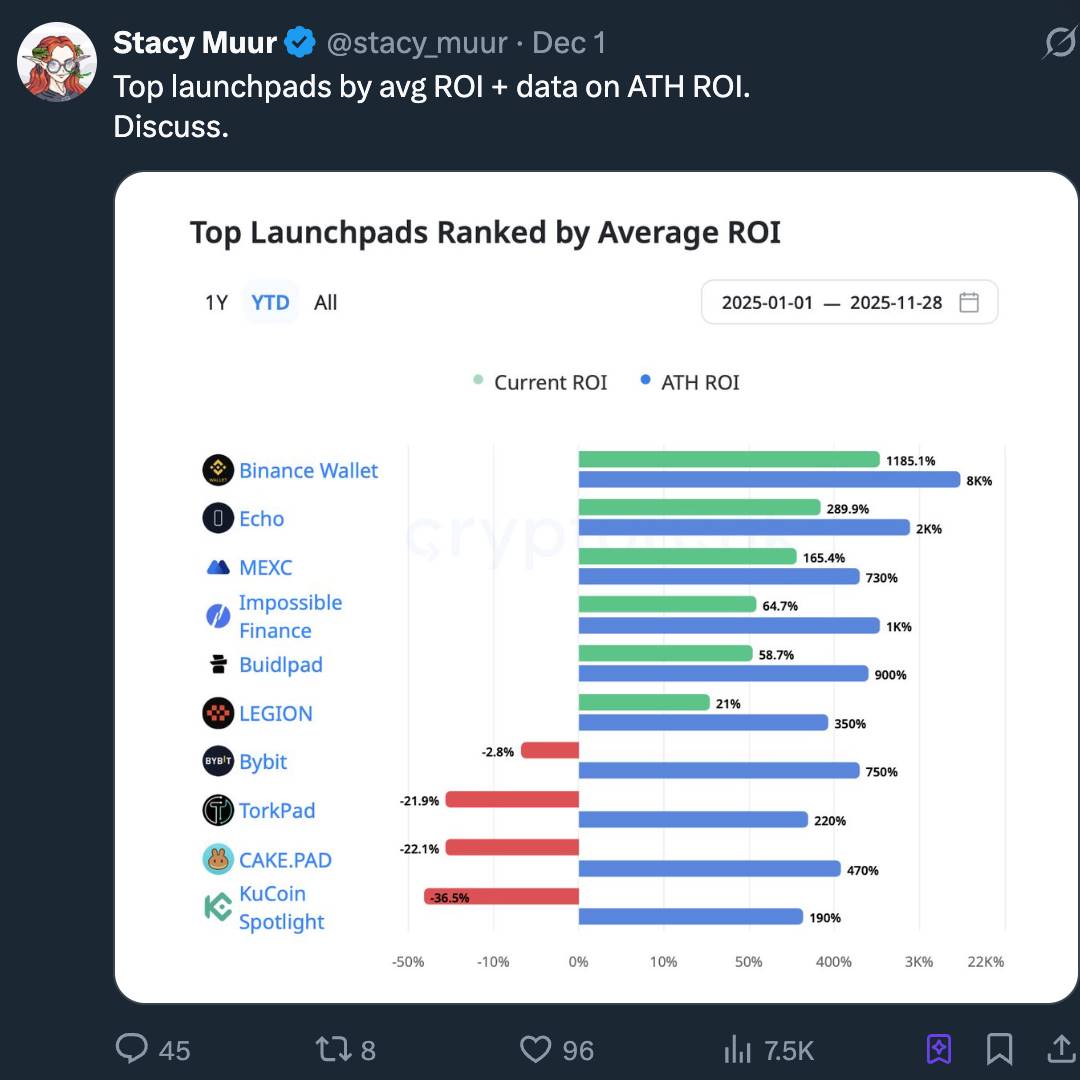

7. The Return of Launchpads: A New Era for Retail Capital

We view the 2025 launchpad boom not as an "ICO comeback" but as the industrialization of ICOs. What the market called "ICO 2.0" was actually the maturation of the crypto capital formation stack, evolving into Internet Capital Markets (ICM): a programmable, regulated, 24/7 underwriting rail, not just "lottery-style" token sales.

Regulatory clarity accelerated by SAB 121 repeal meant tokens became financial instruments with vesting, disclosures, and recourse, not just emissions. Platforms like Alignerz baked fairness into the mechanism layer: hashed bids, refund windows, token vesting schedules based on lock-up periods not insider channels. "No VC dumps, no insider gains" became an architectural choice, not a slogan.

Meanwhile, we noted launchpads consolidating into exchanges, a sign of structural shift: Coinbase, Binance, OKX, and Kraken-affiliated platforms offered KYC/AML compliance, liquidity assurance, and curated issuance pipelines accessible to institutions. Independent launchpads were forced to niche down into verticals (e.g., gaming, memes, early infrastructure).

Narratively, AI, RWA, and DePIN dominated issuance channels, with launchpads acting more as narrative routers than hype machines. The real story is that crypto is quietly building an ICM layer for institutional-grade issuance and long-term alignment, not replaying 2017 nostalgia.

8. The Structural Uninvestability of High-FDV Projects

For much of 2025, we saw a simple rule play out repeatedly: high-FDV (Fully Diluted Valuation), low-float projects are structurally uninvestable.

Many projects—especially new L1s, sidechains, and "real yield" tokens—entered the market with multi-billion dollar FDVs and single-digit circulating supplies.

As one research firm put it, "High FDV, low float is a liquidity time bomb"; any meaningful selling from early buyers would instantly crater the order book.

The results were predictable. These tokens pumped on listing, then bled out as unlocks hit and insiders exited. Cobie's quip—"refuse to buy overpriced FDV tokens"—went from meme to risk assessment framework. Market makers widened spreads, retail simply stopped participating, and many such tokens went virtually nowhere for the rest of the year.

In contrast, tokens with actual utility, deflationary mechanics, or cash flow linkage structurally outperformed peers whose only selling point was "high FDV."

I believe 2025 permanently reshaped buyer tolerance for "tokenomic theater." FDV and float are now seen as hard constraints, not footnotes. Looking to 2026, if a project's token supply can't be digested by exchange order books without destroying price action, that project is effectively uninvestable.

9. InfoFi: Rise, Mania, and Collapse

I see the 2025 InfoFi boom and bust as the clearest cyclical stress test of "tokenized attention."

InfoFi platforms like @KaitoAI, @cookiedotfun, @stayloudio promised to pay analysts, creators, and community managers for "knowledge work" via points and tokens. For a brief window, this became a hot VC theme, with Sequoia, Pantera, Spartan, and others deploying significant capital.

Crypto's information overload plus the trendy AI+DeFi narrative made on-chain content curation seem like an obvious missing primitive.

Yet, the design choice to meter attention was a double-edged sword: as attention became the core metric, content quality collapsed. Loud and peers were flooded with AI-generated slop, bot farms, and engagement cartels; a few accounts captured most rewards, while the long tail realized the game was rigged against them.

Multiple tokens saw 80–90% drawdowns, with some outright collapsing (e.g., WAGMI Hub imploding post a 9-figure raise after a major exploit), further damaging the sector's credibility.

The takeaway is that InfoFi's first attempts were structurally unstable. While the core idea—monetizing valuable crypto signals—remains compelling, incentives need redesigning around priced, verified contributions, not just clicks.

I believe by 2026, a next generation of projects will learn these lessons and iterate.

10. The Return of Consumer Crypto: Led by a New Paradigm via Neobanks

In 2025, the return of consumer crypto is increasingly seen as a structural shift driven by Neobanks, not native Web2 apps.

I see this pivot reflecting a deeper realization: adoption accelerates when users onboard via financial primitives they already understand (e.g., deposits, yield), while the underlying settlement, yield, and liquidity rails quietly migrate on-chain.

The result is a Hybrid Banking Stack where Neobanks abstract away gas, custody, and bridge complexity while giving users direct access to stablecoin yields, tokenized Treasuries, and global payment rails. The result is a consumer funnel that can onboard millions "deeper on-chain" without making them think like power users.

Industry-wide sentiment suggests Neobanks are becoming the de facto standard interface for mainstream crypto demand.

Platforms like @ether_fi, @Plasma, @UR_global, @SolidYield, @raincards, and the Metamask Card epitomize this shift: they offer instant on-ramps, 3–4% cashback cards, 5–16% APY via tokenized Treasuries, and self-custody smart accounts, all wrapped in compliant, KYC'd environments.

These apps benefited from 2025's regulatory reset, including SAB 121 repeal, stablecoin frameworks, and clearer guidance for tokenized funds. These changes reduced operational friction and expanded their TAM in emerging economies, especially where yield, FX savings, and remittances are real pain points.

11. The Normalization of Global Crypto Regulation

I believe 2025 is the year crypto regulation finally normalized.

Conflicting regulatory directives coalesced into three recognizable regulatory models:

-

European Framework: MiCA + DORA, with 50+ MiCA licenses issued, stablecoin issuers treated as e-money institutions.

-

US Framework: Stablecoin laws like the GENIUS Act, SEC/CFTC guidance, and spot Bitcoin ETF approvals.

-

Asia-Pacific Patchwork: Hong Kong's full-reserve stablecoin rules, Singapore's licensing refinements, and broader FATF Travel Rule adoption.

This isn't superficial; it fundamentally reshapes risk models.

Stablecoins went from "shadow banking" to regulated cash equivalents; banks like Citi and BoA can now run tokenized cash pilots under clear rules; platforms like Polymarket can relaunch under CFTC oversight; US spot Bitcoin ETFs can attract $35B+ in sticky inflows without existential risk.

Compliance went from a drag to a moat: those with strong regtech architecture, clean cap tables, and auditable reserves suddenly enjoyed lower cost of capital and faster institutional onboarding.

In 2025, crypto went from grey-zone curiosity to regulated object. Looking to 2026, the argument has shifted from "is this industry allowed to exist" to "how to implement specific structures, disclosures, and risk controls."