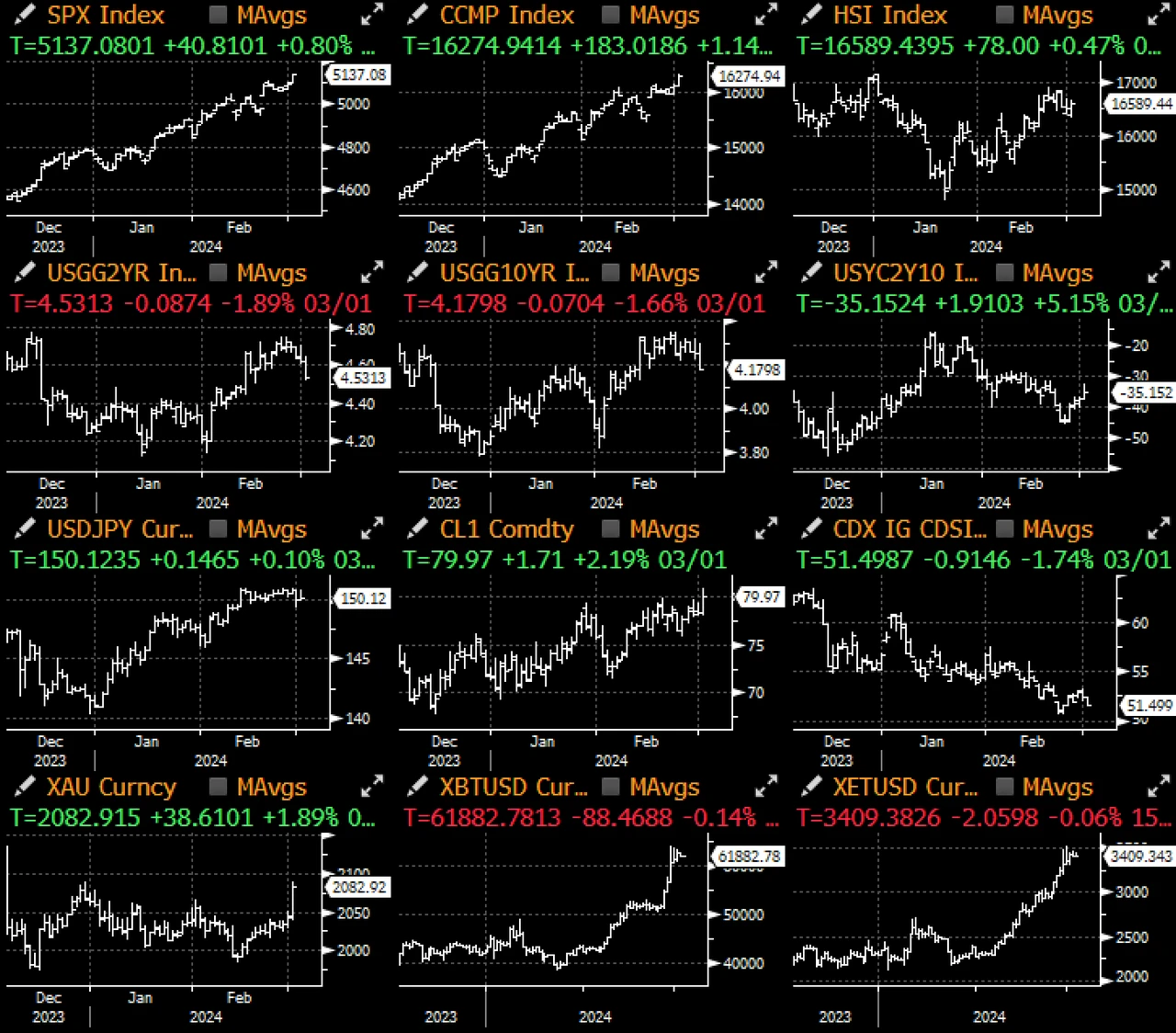

风险资产上周持续反弹,即使又有一家区域性银行传出信贷问题,加上一位著名经济学家宣称美联储在 2024 年不会降息,也无法阻止上涨列车的前进。根据德意志银行的数据,SPX 指数在过去 18 周中上涨了 16 周,这是自 1971 年以来从未出现过的涨势。

就在 SVB 倒闭一周年之际,纽约社区银行 (New York Community Bancorp) 管理层称,该银行发现内部贷款审查流程存在重大缺陷,导致 100% 的商誉减值(24 亿美元)以及管理团队的整顿,其股价在上周五出现暴跌。然而,与去年广泛的恐慌情绪不同,华尔街似乎认为这仅是一个个案,该股市净率(约 0.5)的疲软在很大程度上已经充分反映了这些担忧,即便 NYCB 股价在周五暴跌了 20% ,但 KBW 区域银行指数仅出现些微调整(约 0.3% )。

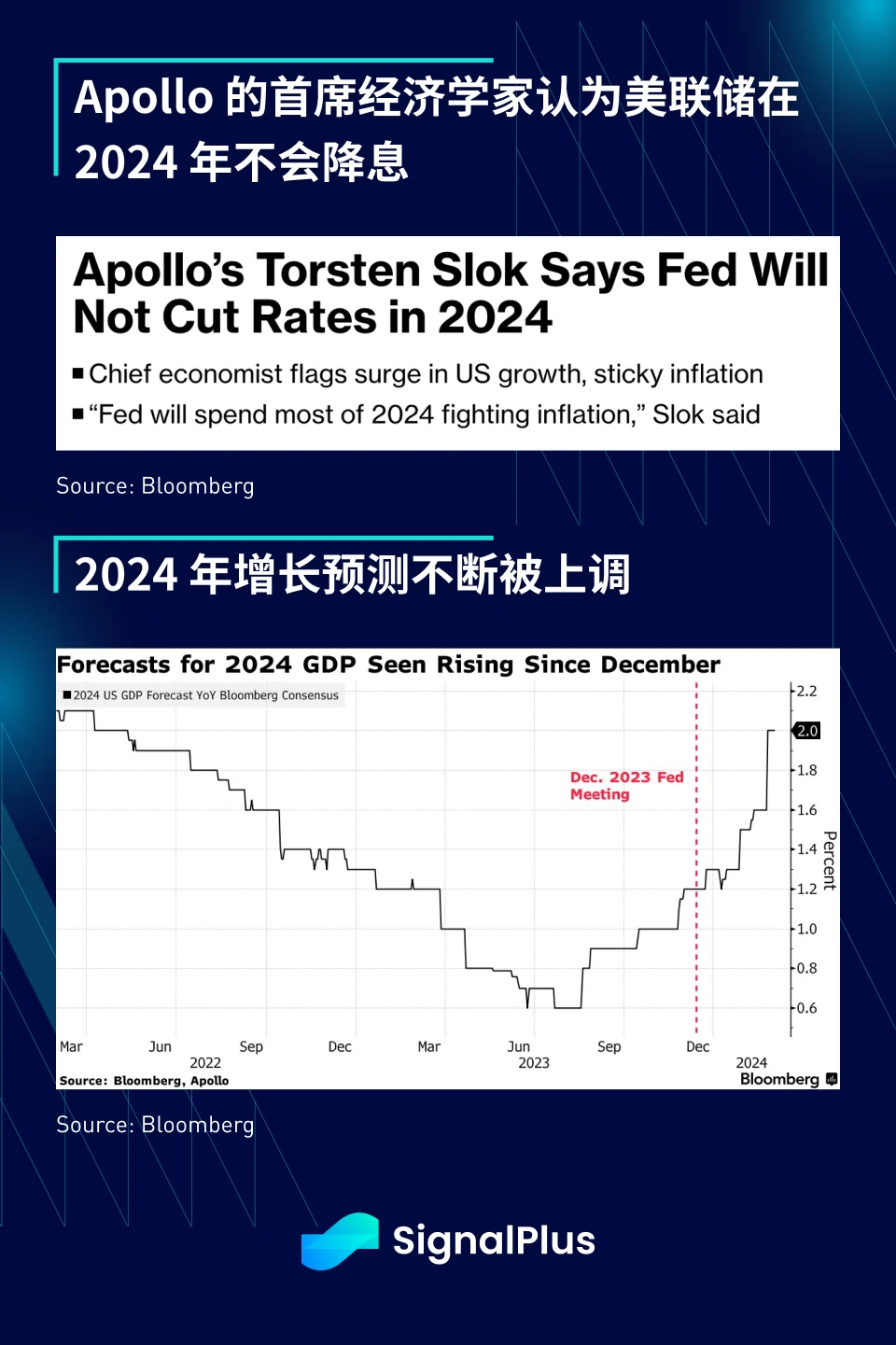

美国经济衰退遥遥无期(亚特兰大联储预估第一季度 GDP 增长约 3% ),美国消费者仍相当强劲(美国银行提到 2 月份消费者支出增长超过 3% ),就业/薪资/通胀增长保持稳定,Apollo 的首席经济学家表示,由于央行将在 2024 年大部分时间里应对通胀并保持高收益率,美联储将不会在 2024 年降息。Slok 指出,美国增长预期大幅上升,就业市场依然紧绷,核心通胀居高不下,加上金融形势过于宽松,这些因素会共同抑制宽松预期,此外,美联储从 2023 年第四季度开始的口头政策转向已经为资产价格提供了足够的推动力。

Powell 主席将于 3 月 7 日向参议院银行委员会提供半年度货币政策更新,届时他将有机会讨论近期美国通胀数据的反弹,并就 12 月鸽派转向的理由接受质询。此外,财报季已经过去,企业盈利可观,也已反映在股票价格中,根据 Bloomberg,SPX 盈利超出季前预测的幅度有机会成为 2021 年第四季度以来最大。不断增长的盈利无疑让华尔街措手不及,策略分析师们急忙上调 SPX 年终目标,仅在过去两周内媒体就报导了超过六次的预测上调。

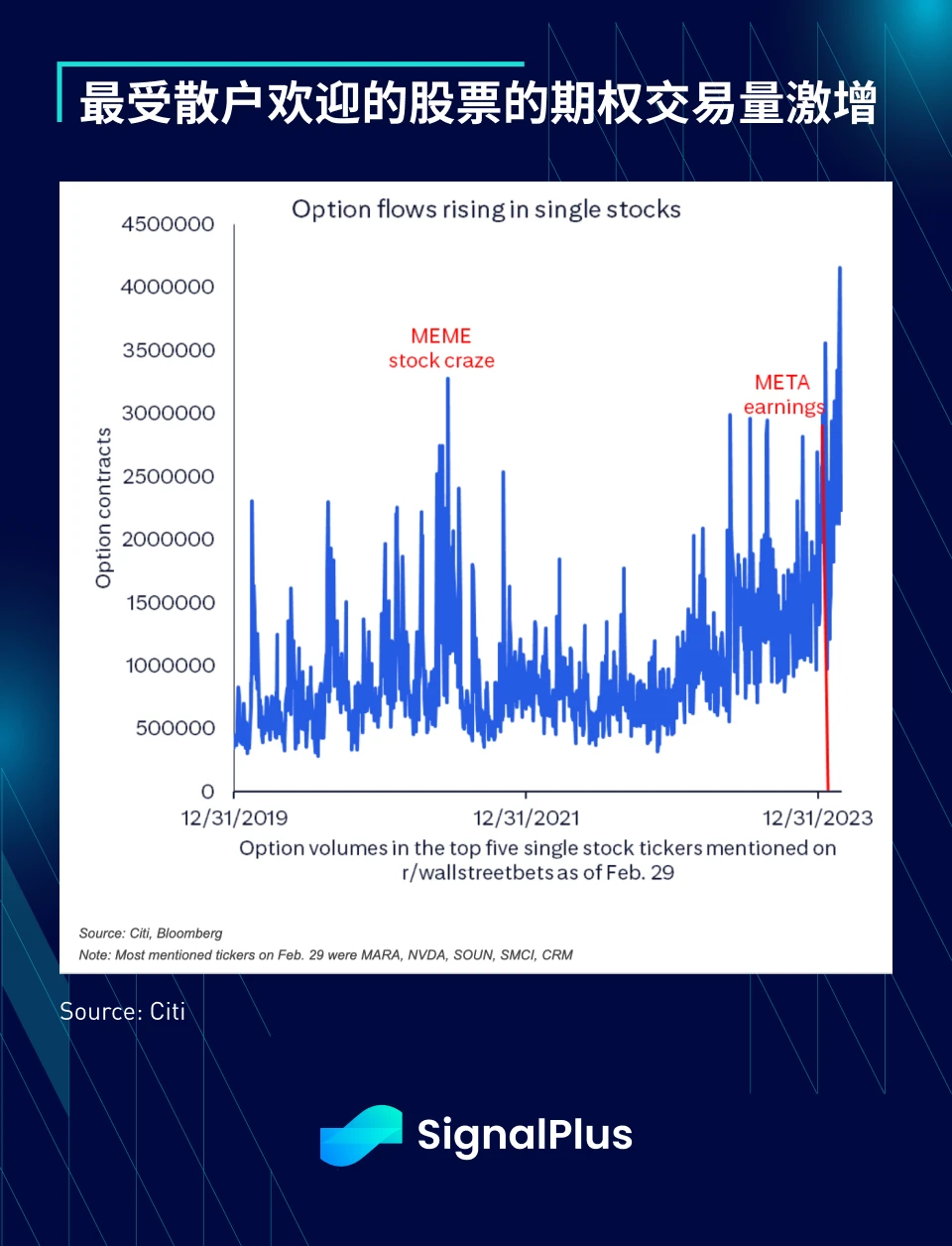

与加密货币类似,散户交易活动激增,个股期权的交易量不断增加,甚至远超过 2021 年的高点,且在 NVDA 和 META 的正向盈利结果后进一步加速。

在中国,股票与债券市场也终于迎来令人振奋的相关性变化,两种资产类别的价格终于开始同步(利率下降=债券价格上升)。中国资产是否迎来了转捩点?人民银行的宽松政策是否终于开始反映在股价上?希望正面的价格走势得以持续...

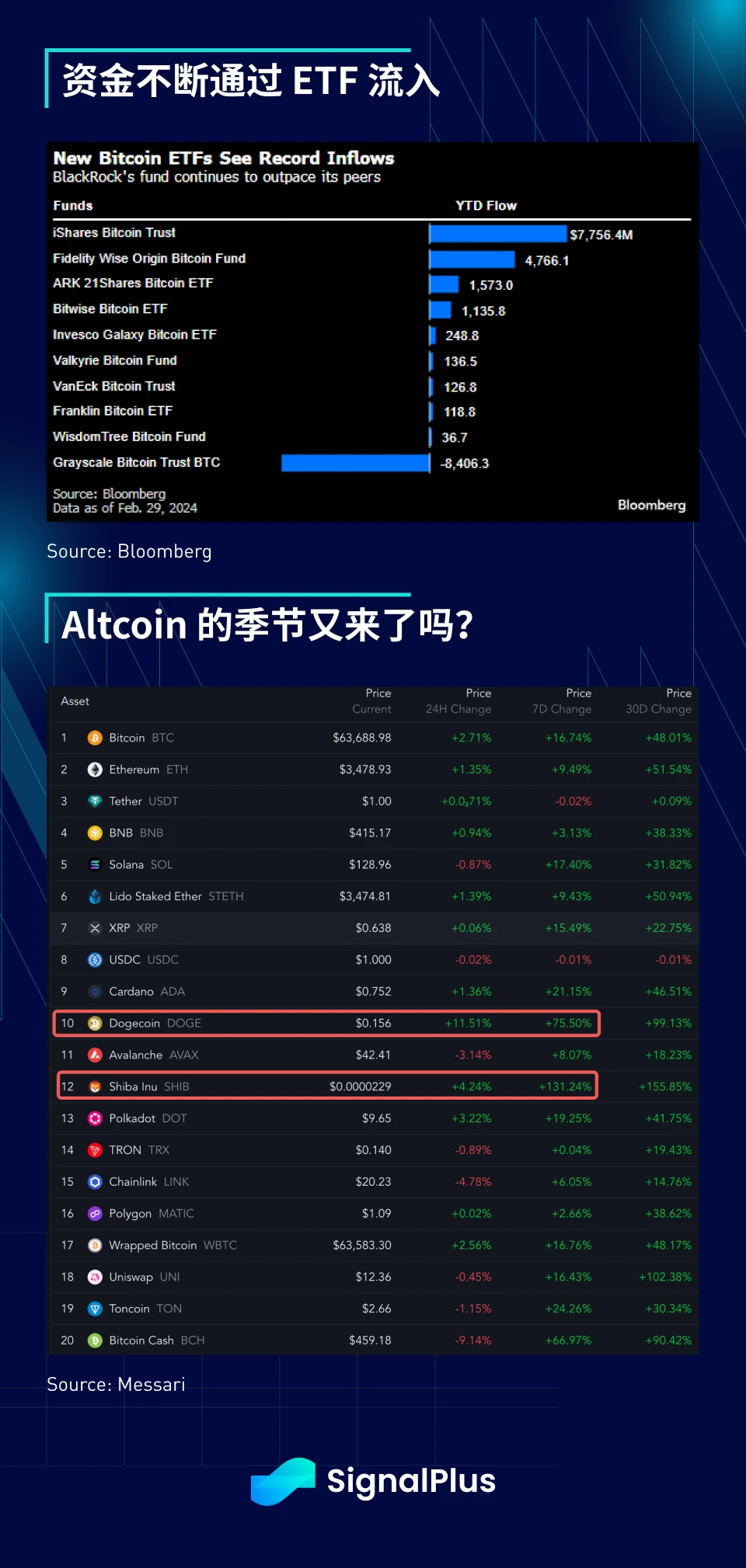

在加密货币方面,创纪录的资金仍不断通过 ETF 流入,正面的市场情绪似乎也蔓延到了 altcoins 以及 memecoin, SOL (+ 17% )、XPR (+ 16% )、Cardano (+ 21% ) 、Polkadot (+ 19% )、Doge (+ 7% ) 和 Shiba (+ 131% ) 在过去 7 天都在加速上涨。

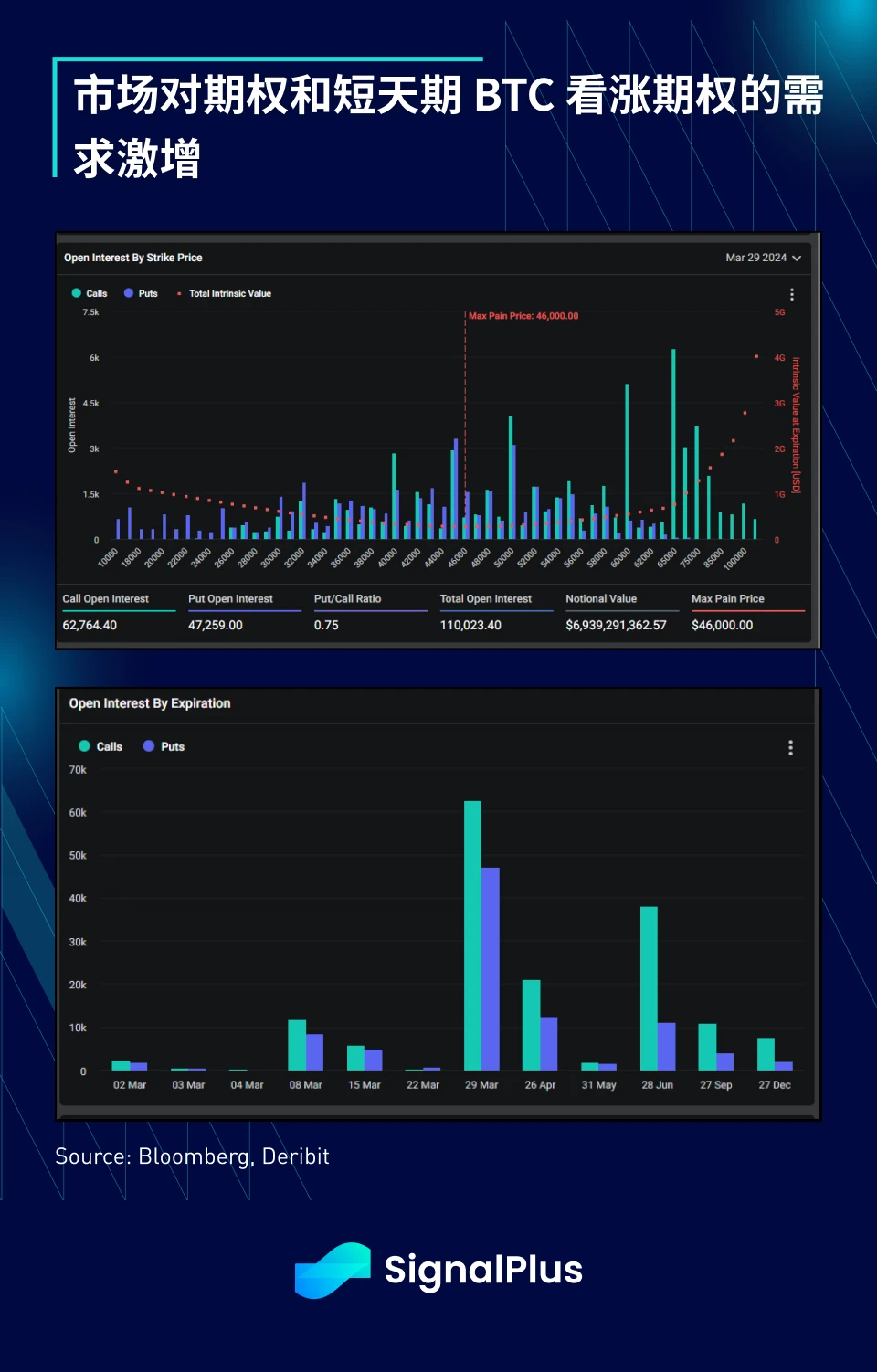

在期权方面,短天期期权需求激增,未平仓量集中在 6.5 至 7.5 万美元的水平附近。期权交易所 Deribit 上周公布了创纪录的交易量, 24 小时交易量超过 124 亿美元,未平仓量超过 270 亿美元。市场对短天期看涨期权的巨大兴趣正在推高隐含波动率,并导致期权卖方出现小型 gamma 挤压,其中大部分敞口将于 3 月 29 日到期,因此预计本月大部分时间里价格将反复波动(上下震荡),享受上涨的同时请务必谨慎管理风险。

您可在 ChatGPT 4.0 的 Plugin Store 搜索 SignalPlus ,获取实时加密资讯。如果想即时收到我们的更新,欢迎关注我们的推特账号@SignalPlus_Web3 ,或者加入我们的微信群(添加小助手微信:SignalPlus 123)、Telegram 群以及 Discord 社群,和更多朋友一起交流互动。

SignalPlus Official Website:https://www.signalplus.com