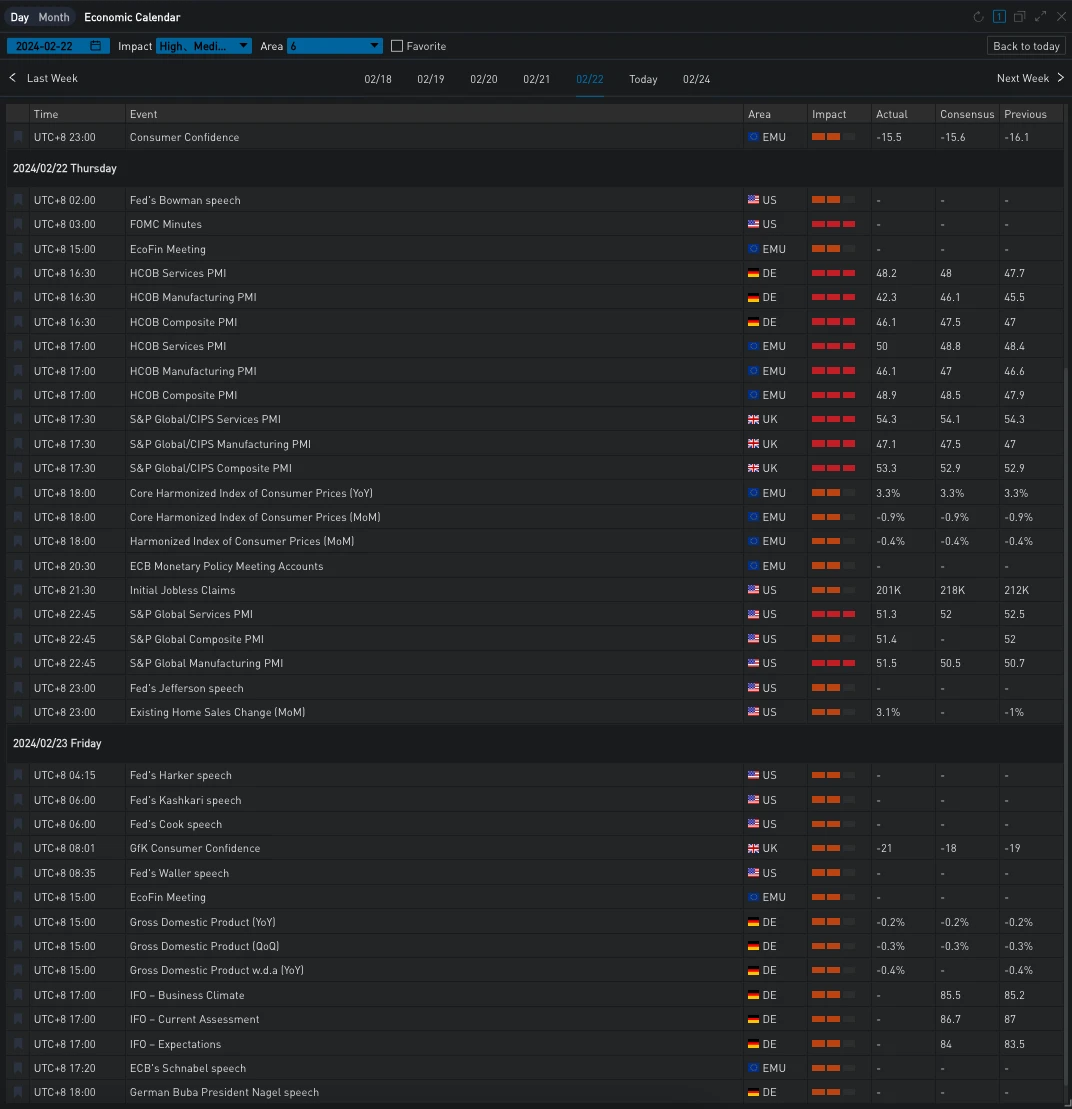

昨日(22 FEB)美国经济数据表现强劲,美联储官员也在持续为近期降息的预期泼冷水:当周初请失业金人数录得 20.1 万人,低于预期 21.8 万人,Markit 制造业 PMI 意外攀升至 51.5 ,高于预期的 50.5 ;费城联储主席哈克发出警告:最大的风险是过早降息,暂无降息的紧迫性;美联储杰斐逊同样表示了对过度宽松的政策可能导致通胀逆转或停滞的担忧,认为今年晚些时候降息可能是适当的。美债收益率因此逐步上行,两年期/十年期现分别报 4.739% /4.343% 。美国三大股指受英伟达超预期财报数据的提振上行,道指/标普/纳指分别收涨 1.18% /2.11% /2.96% 。

Source: SignalPlus, Economic Calendar

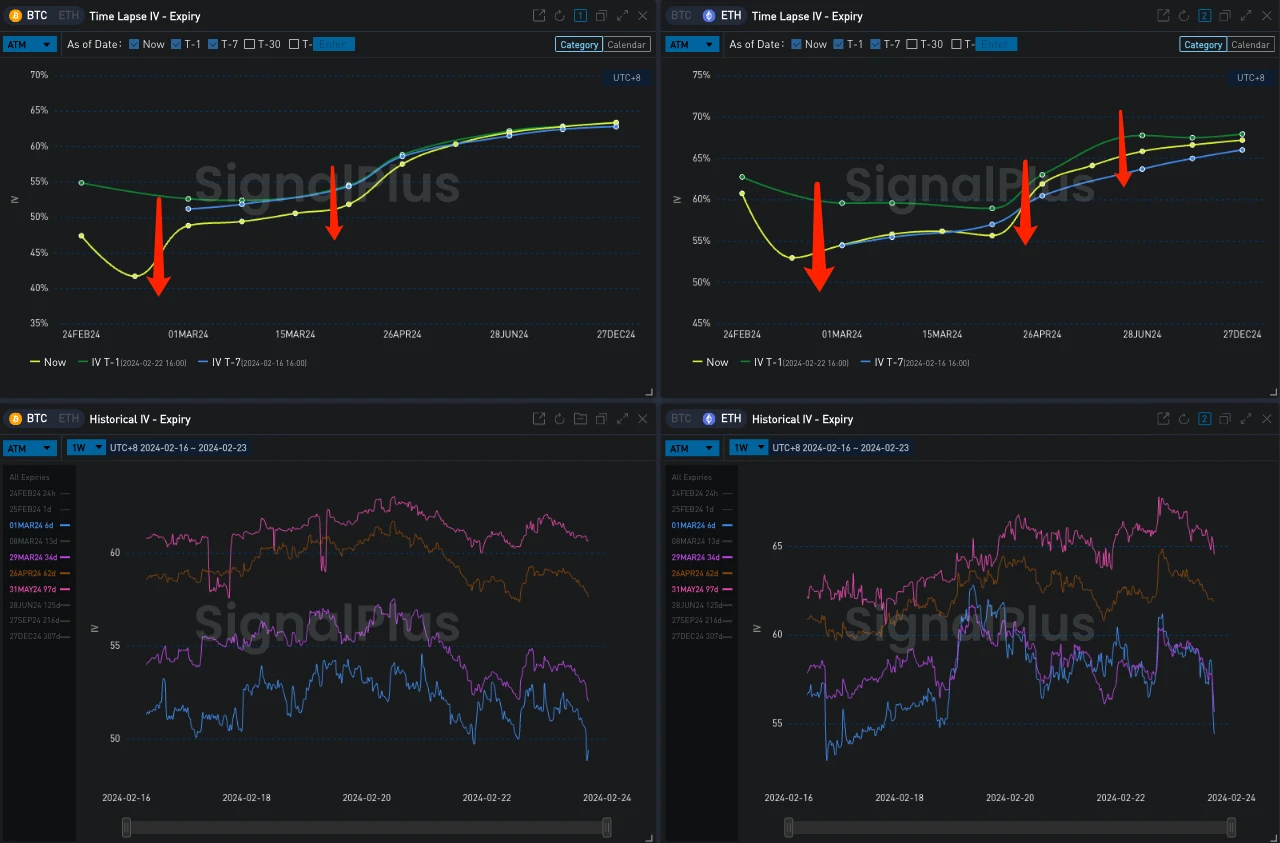

Source: Binance & TradingView,ETH 再度从 3000 点向下回调

数字货币方面,今日迎来了二月末期权/期货的交割日,释放了本轮上涨行情锁住的大量保证金,BTC/ETH 价格出现轻微回调,收报 51000 (-1.6% )/2933 (-1.8% )。

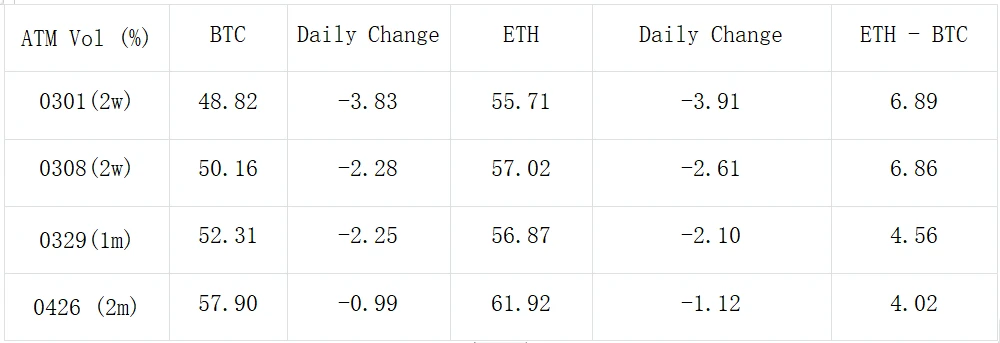

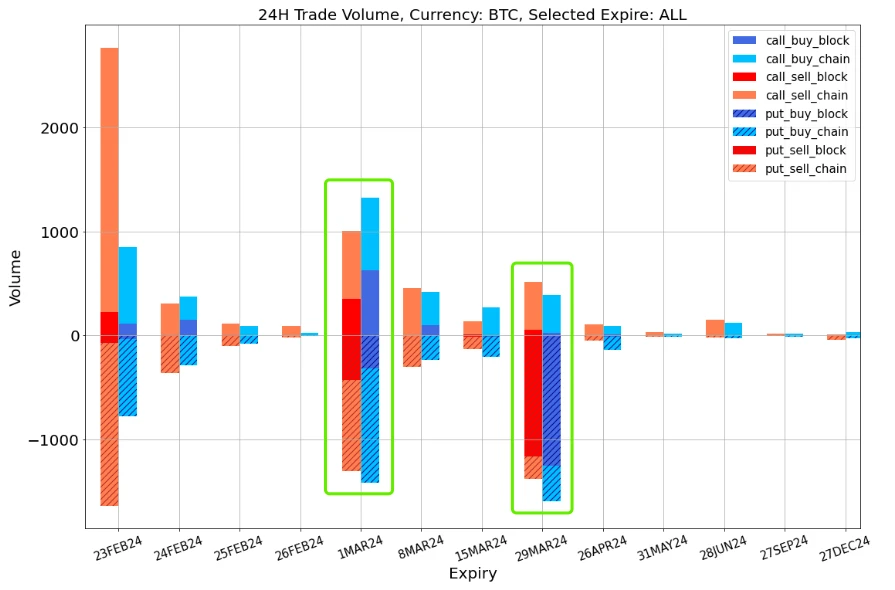

期权方面,隐含波动率曲线走陡下行,ETH 相对 BTC 的 Vol Premium 维持不变。从交易上看,BTC 成交集中在 1 MAR/29 MAR,其中看跌期权成交比例大幅上涨,主要由 1 MAR 50000/49000 Long Put Spread 和 29 MAR 的两组碟式看跌价差策略组成,文末附图展示了两组策略的损益变化。ETH 大多数成交也都集中在三月,净流入最为明显的是 3100/3200 买入看涨以及 3000 买入看跌。

Source: Deribit (截至 23 FEB 16: 00 UTC+ 8)

Source: SignalPlus,隐含波动率走陡下行

Data Source: Deribit,过去一日 BTC 成交集中在 1 MAR/29 MAR

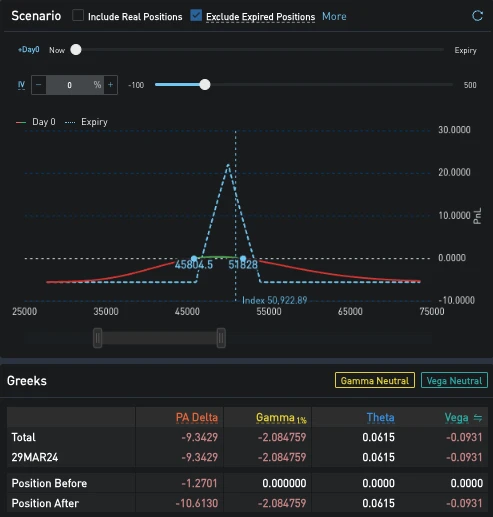

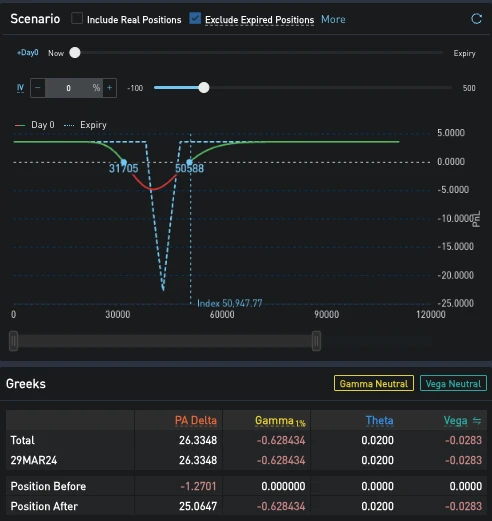

Source: SignalPlus,Short 48000/43000/38000 PutFly 损益变化;Long 54000/50000/46000 PutFly 损益变化

Source: Deribit Block Trade

Source: Deribit Block Trade

您可在 ChatGPT 4.0 的 Plugin Store 搜索 SignalPlus ,获取实时加密资讯。如果想即时收到我们的更新,欢迎关注我们的推特账号@SignalPlus_Web3 ,或者加入我们的微信群(添加小助手微信:SignalPlus 123)、Telegram 群以及 Discord 社群,和更多朋友一起交流互动。

SignalPlus Official Website:https://www.signalplus.com