2 月 23 日上午,Web3 安全团队 Ancilia.nc 在社交媒体表示,监测到价值超过 3000 ETH 的 RON 被短时间内从 Ronin 桥中提取并存入 Tornado。疑似黑客地址的关联钱包(0x 73、0x 39、0x a 4)在 Tornado 预存了 0.1 ETH,并在相同时间内提取总计 3250 枚 ETH。

Ronin 又被盗了?社区的反应更多是不敢相信,「我刚刚开始看好他」,还有人调侃「那是不是可以趁低价买入,他们应该不会遭受第三次攻击了」。

消息发酵后,RON 从 3.16 美元的位置断崖式下跌, 10 分钟内下跌至 2.74 美元,跌幅超 13% 。

左图源@WazzCrypto

被盗鲸鱼地址是 Axie Infinity 联创

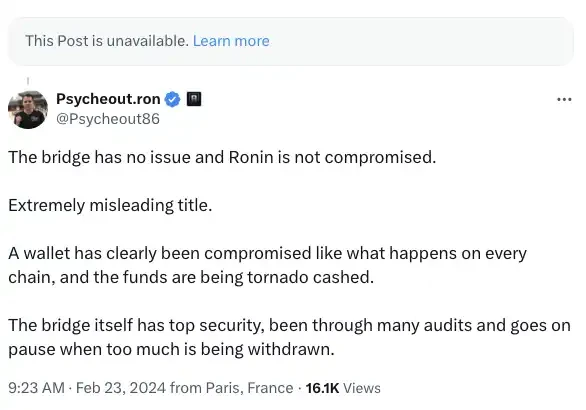

二十分钟后,Ronin 联合创始人 Psycheout 在该条推特下回复表示,Ronin 和跨链桥都没有问题,这只是一个鲸鱼钱包被盗,并通过 Tornado Cash 混走。「Ronin 桥拥有很高的安全性,经过了多次审核,当监测到有大量资产撤走时就会暂停提取」。

Psycheout 还继续追加评论,要求 Ancilia 团队删除推文。

但令社区没想到的是,这位被盗的鲸鱼竟是 Axie Infinity 和 Ronin Network 的联合创始人 Jihoz。

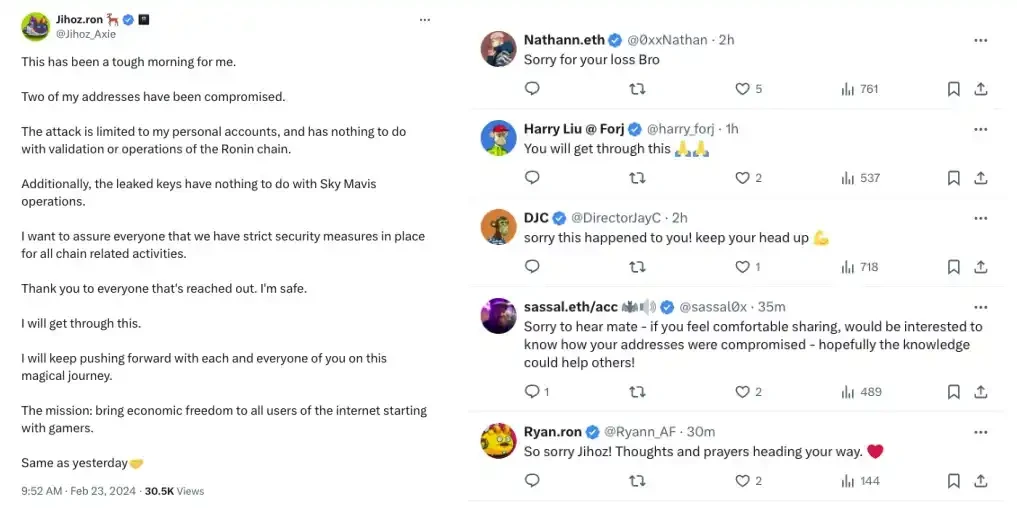

在社区的被盗疑问发出一小时后,Jihoz 发布了一条推文,表示其两个个人地址遭到安全攻击。Jihoz 强调,此次攻击仅限于其个人账户,与 Ronin 链的验证或运营活动无关。同时,泄露的密钥与 Sky Mavis 的运营也没有任何联系。「我想向大家保证,我们对所有链上相关活动都采取了严格的安全措施」。

Pixels 创始人 Luke Barwikowski 和 Ronin 联创 Psycheout,以及 Ronin 社区成员都在 Jihoz 的动态下表示了安慰。此次「被盗乌龙」宣告结束,截止撰稿时,RON 已经回升至 3 美元附近,短时跌幅收窄至 5% 。

「被盗 PTSD」, 2 年前的 6 亿阴影

其实私钥被盗是常发生的事情, 300 万 RON 的价值体量也不算太大,只占流通量的 0.1% 。上个月,Ripple 陷入被盗 2.13 亿枚 XRP (约合 1.12 亿美元)」危机时,XRP 短时跌近 4% ,而此次 Ronin 事件中的流失资产价值在 1000 万美元左右,却在 10 分钟内引起了 13% 的跌幅?这样的敏感和恐慌情绪很大程度上是源于 2 年前 Ronin 被盗 6 亿的阴影。

2022 年 3 月 23 日,Ronin 网络的九个验证节点中的四个 Ronin 验证器和一个由 Axie DAO 运行的第三方验证器被黑客控制。而 Ronin 官方团队在被黑客攻击 7 日后意识到这个安全漏洞,在这期间攻击者使用被黑的私钥来伪造假提款,从 Ronin 跨链桥中提取了 173, 600 个 ETH 和 2550 万美元的 USDC,价值 6 亿美元。

相关阅读:《Ronin 被盗官方梳理: 6 天前发现漏洞, 5 个私钥被盗》

在团队宣布被盗后,RON 在一天内跌去 20% ,并在之后的一个月里持续下跌,缩水 84% 。2022 年的绝大部分时间,RON 的价格都在 1 美元以下。有这样的惨痛经历,在发现 Ronin 上的资产有可疑动向后,社区的第一反应肯定是「Ronin 又被盗了?」

不过此时的 Ronin 已经不同往日,近一年,随着 Ronin 不断完善其基础设施和实力链游 Pixel 的加入,社区目睹了 Ronin 从低谷走向复苏。2 月 9 日,RON 上线 Binance 交易对,在社区眼中,这是 Ronin 生态被资本肯定的信号。

相关阅读:《被盗 6 亿六百天后,Ronin 再登场》

除了生态,Ronin 的安全性曾因「被盗金额达 6 亿、黑客攻击 5 日后才发现」这两点而备受社区质疑,但随着 Ronin 近年来将 9 个验证节点增加至 22 个,并在 2023 年 4 月推出委托权益证明 (DPoS) 后,其安全性已经大大提升。截止撰稿时,已经有 1.9 亿枚 RON 参与了质押。