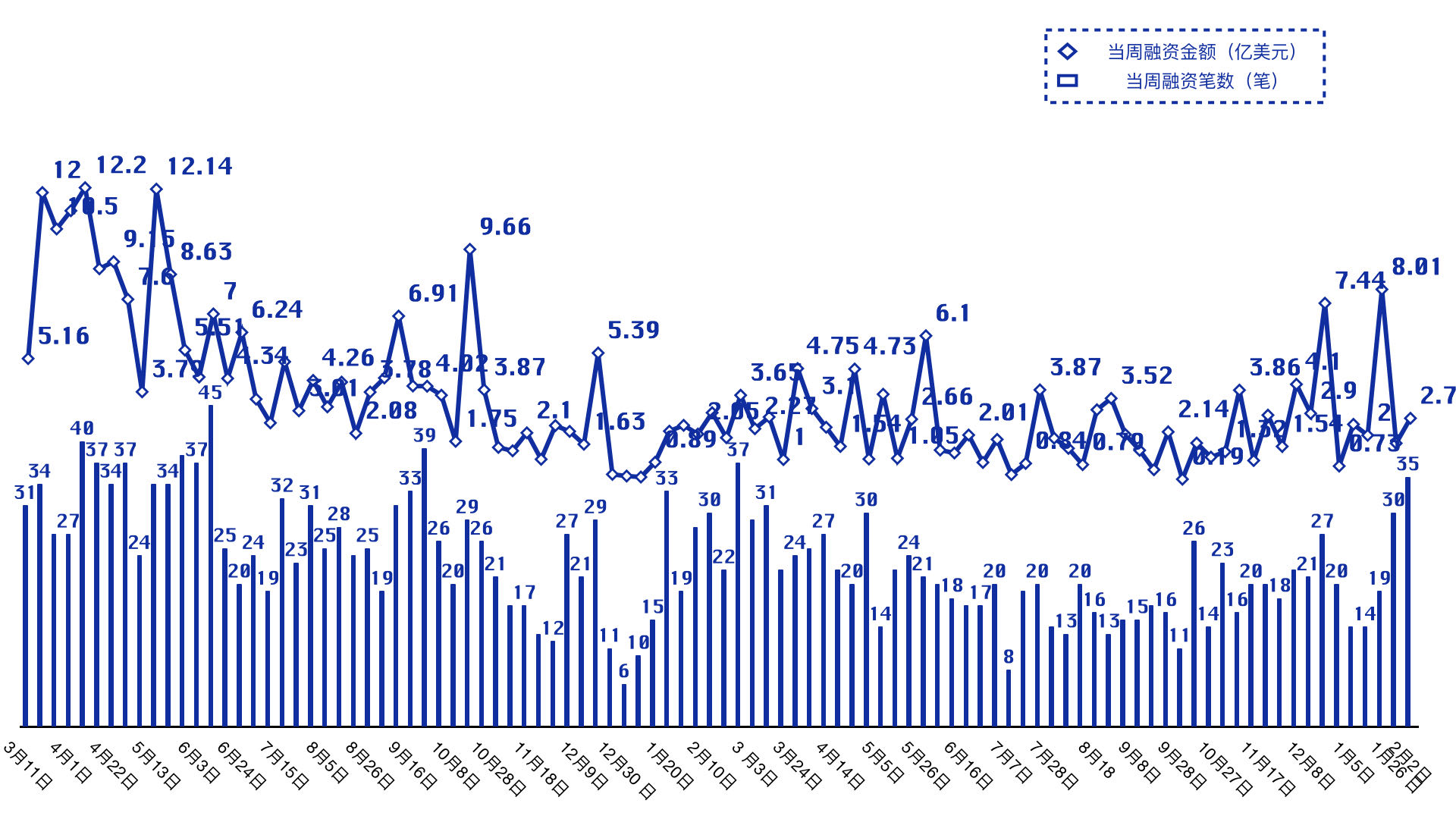

据 Foresight News 统计,2024 年 1 月 27 日至 2024 年 2 月 3 日期间,加密市场共发生 35 笔投融资事件,其中工具和基础设施 14 笔、 DeFi 领域 13 笔、资管领域 1 笔、链游和 NFT 领域 3 笔、Web3 领域 4 笔。已披露投融资总金额约 2.70 亿美元。

周级别已披露融资总额及融资笔数汇总图:

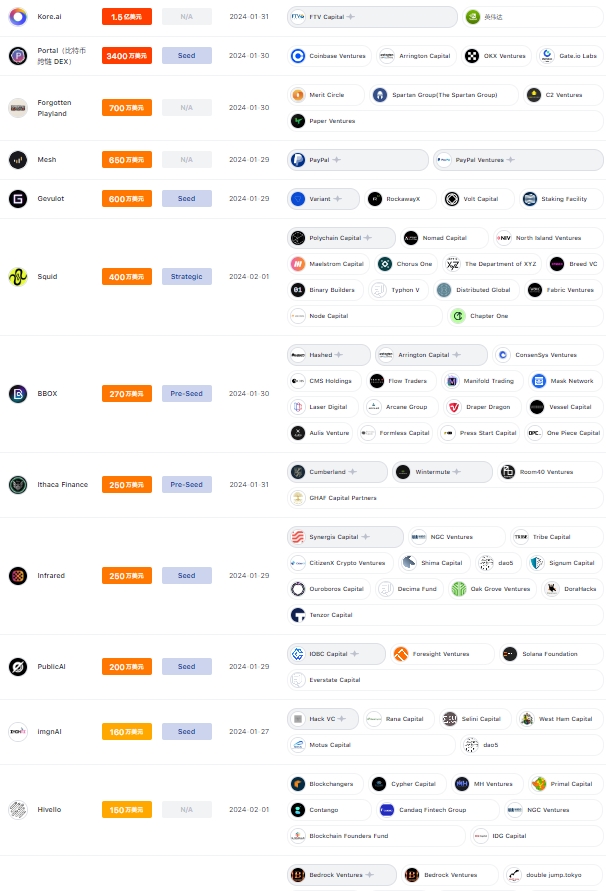

本周投融资项目按融资金额排序如下图:

本周过亿美元融资共 1 笔,AI 聊天机器人开发商 Kore.ai 完成 1.5 亿美元融资,FTV Capital 领投。千万级美元融资共 2 笔,其中包括混合加密交易平台 Cube.Exchange 完成 1200 万美元 A 轮融资,6th Man Ventures 领投;比特币 DEX 项目 Portal 完成 3400 万美元种子轮融资,Coinbase Ventures 等参投。

在投融资细分赛道中,本周 DeFi、工具和基础设施领域均较为火热,资管、NFT 和链游较为低迷。

机构方面,本周活跃机构有 Coinbase Ventures、Animoca Ventures、FTV Capital 等,主要聚焦于 DeFi、工具和基础设施领域。

工具和基础设施

Squid 完成 400 万美元战略轮融资

Squid 是一个跨链基础设施解决方案,为 EVM 和 Cosmos 生态系统中的链及其他链提供支持。

Hivello 完成 150 万美元融资

Hivello 是一个 DePIN 项目。

Exabits.ai 完成种子轮融资

Exabits.ai 是一个去中心化云计算服务提供商,并得到斯坦福区块链加速器、哈佛创新实验室、OV Base Camp、伯克利区块链 Xcelerator 和谷歌云的支持。

Doubler Pro 完成种子轮融资

Doubler Pro 是一个基于开放式智能合约的金融策略工具,宣布推出测试网,并与 Blast 二层网络集成,新资金将用户加速开发和增强用户体验。

Delegate Labs 完成 900 万美元种子轮融资

Delegate Labs 是安全协议 Delegate 背后团队,跨链互操作性协议 LayerZero 合作推出基于区块链的域名协议 Clusters。

专注于 AI 的 Web3 底层协议 KIP Protocol 完成战略轮融资

KIP Protocol 是 AI 模型、应用程序和数据所有者构建的去中心化基础层,可在 Web3 中安全地进行交易和货币化。KIP 使有价值的知识和数据能够作为知识资产得到保护和货币化,确保与人工智能交互而不失去所有权。

区块链隐私保护解决方案 BlokID 完成 125 万美元种子轮融资

BlokID 于 2023 年 7 月成立,专注于为数字广告行业量身定制区块链时间戳驱动的安全服务,帮助品牌和机构能够使用先进技术验证和验证其资产。

以太坊基础设施初创公司 Yet Another Company 完成 100 万美元融资

Yet Another Company 旨在解决以太坊生态流动性碎片化和和市场互操作性问题,正在开发一个基于 EigenLayer 的验证和聚合层 Aligned Layer。

AI 聊天机器人开发商 Kore.ai 完成 1.5 亿美元融资

Kore.ai 集成了多个商业和开源大型语言模型,例如由 OpenAI、Google、Meta Platforms Inc、Anthropic 和 Cohere 构建的模型,然后对这些平台进行微调或使用新数据进一步训练它们具体任务。

RWA 生态系统 TProtocol 完成天使轮融资

TProtocol 将发展成为综合性区块链真实世界资产(RWA)聚合器。

零知识证明区块链 Gevulot 完成 600 万美元种子轮融资

Gevulot 计划推出其 Layer1 区块链,使开发人员能够利用 ZK 证明并将计算任务委托给先进的硬件运营商网络。Gevulot 正准备推出其以开发人员为中心的网络(或 devnet),这是一种受限制的测试网络。该网络正在与 P2P.org、Supranational、Staking Facilities 和 RockawayX Infrastructure 等质押验证公司合作实现。

AI×DePIN 项目 EMC 完成百万美元融资

EMC 是万向区块链实验室和 HashKey Capital 共同推出的 Web3 孵化器 Future3 Campus 孵化营项目,旨在建立去中心化 AI 计算能力网络,以及在 GPU 计算能力资产和 AI 应用程序之间架起桥梁的 Web3 平台。

加密原生 AI 图像生成平台 imgnAI 完成 160 万美元种子轮融资

根据其网站,该 AI 图像生成机器人平台于 2022 年底推出,其 imgnAI 加密代币用于解锁高级功能并直接将图像铸造为 NFT,用于这些功能的代币后会被烧毁,从而减少总供应量。

Web3 数据平台 Hyperline 完成 520 万美元种子轮融资

Hyperline 旨在通过创建数据智能功能来帮助开发人员构建数据密集型应用程序。

DeFi

Velar 完成 350 万美元融资,将推出基于比特币网络的永续交换交易所

Velar 计划推出一个利用比特币网络的永续交换交易所。Velar v3 版本将支持合成比特币资产 sBTC 作为抵押品,并进行杠杆交易,v3 版本将于 2024 年第二季度推出。

混合加密交易平台 Cube.Exchange 完成 1200 万美元 A 轮融资

Cube.Exchange 是一个融合传统金融与区块链技术的混合交易平台。

Oddiyana Ventures 已战略投资 Nibiru Chain

Nibiru Chain 是一个 DeFi Hub。

Ordiswap 与 DWF Labs 合作并获得战略投资

Ordiswap 是一个比特币生态 DeFi 项目,为比特币开发 DeFi 基础设施与生态系统。

可组合期权协议 Ithaca 完成 250 万美元融资

Ithaca Finance 在 Arbitrum 测试网上线,在本季度晚些时候全面启动主网之前仅邀请受邀者参与。

去中心化永续合约协议 Zeepr Labs 完成由 Cincubator 领投的一轮融资

Zeepr 是同时支持币本位和 U 本位的去中心化永续合约协议,旨在提供无滑点、无资金费的链上永续合约交易体验。

Binance Labs 投资 LSD 协议 Puffer Finance

Puffer 是一个基于 EigenLayer 构建的去中心化原生 Liquid Restaking 协议 (nLRP),它引入了原生的 Liquid Restaking 代币 (nLRT),可累积 PoS 和质押奖励。

去中心化衍生品交易平台 BBO Exchange(BBOX)完成 270 万美元 Pre-Seed 轮融资

BBOX 曾是 Binance Labs 孵化器第 6 期的 12 个项目之一,通过拍卖机制解决预言机报价延迟问题,同时 BBOX AMM 引入了多资产支持和基于市场信号的动态管理系统,旨在为链上交易者和流动性提供者提供更高的资本利用效率以及收入。

流动性聚合投资策略协议 Doubler 完成种子轮融资

Doubler 是一个开放式的 DeFi 协议,采用马丁格尔策略来聚合市场流动性,将零损失对冲需求与投机者的收益投注需求相结合,同时保持开放性和互操作性。

比特币 DEX 项目 Portal 完成 3400 万美元种子轮融资

Portal 是一个基于比特币的跨链原子交换协议。它的两个主要产品是去中心化交易平台和钱包。据悉,此轮融资的结构是简单的未来股权协议 (SAFE) 和可转换票据的组合。

流动性证明协议 Infrared 完成 250 万美元种子轮融资

Infrared 旨在 Proof-of-Liquidity(PoL)的背景下支持 Berachain 生态的流动性质押。这些资金将用于推进其基础设施发展,包括验证者网络、PoL 保险库以及原生流动性质押代币(LST)iBGT。

Bmaker 完成 120 万美元 Pre-Seed 轮融资

Bmaker 是一个比特币超额抵押稳定币协议。

bitSmiley 完成第一轮代币融资

比特币 DeFi 生态项目 bitSmiley,将推出名为 bitRC-20 的新 DeFi 铭文协议,首个资产为 OG PASS NFT,也称为 bitDisc。

资管

Mesh 获 PayPal 650 万美元投资

Mesh 是一个加密转账和支付服务初创公司,前身为 Front Finance。

NFT 和链游

Yooldo 完成 150 万美元融资

Yooldo 是一个链游平台。

Forgotten Playland 完成 700 万美元融资

Forgotten Playland 是一个 Web3 社交游戏,将于 2024 年第一季度发布产品,其中包含一系列迷你游戏。

Web3 去中心化游戏 IP 系统 Pixelmon 完成 800 万美元种子轮融资

Pixelmon 为去中心化 Web3 游戏 IP,通过其 IP 碎片化系统为 Pixelmon 系列 NFT 持有者提供资产所有权和收益权。

Web3

Web3 分布式 AI 训练网络 PublicAI 完成 200 万美元种子轮融资

PublicAI 致力于用区块链技术规模化生产海量的优质训练数据,以解决人工智能迄今面临的所有难题,让全人类参与到人工智能的共建中并分享其收益。

Web3 游戏公司 Saltwater 完成 550 万美元种子轮融资

Saltwater 已收购游戏开发商 Maze Theory、Nexus Labs 和 Quantum Interactive,这些游戏开发商开发了《神秘博士》和《浴血黑帮》等游戏。

游戏化社交平台 SoulLand 完成百万美元融资

SoulLand 是一款游戏化社交订阅平台,已上线 App Store 和 Google Play。SoulLand 通过引入游戏化元素来解决 Web3 下沉式资讯及社交需求。

Web3 无代码生态系统 Forward Protocol 完成 125 万美元融资

Forward Protocol 旨在通过为价值驱动型经济创建开源 Web3 工具包,以实现区块链的大规模应用。

其他

Uncorlated Ventures 筹集 3.15 亿美元新基金,20% 将用于支持加密初创公司

Uncorrelated Ventures 创始人 Salil Deshpande 认为区块链技术在存储和计算领域仍具价值。Uncorrelated Ventures 目前管理资产超过 7 亿美元,专注于美国和全球市场,特别是印度市场。