市场情绪仍是混沌不明,不同区域的新闻和发展不尽相同;中国推出新的救市计划,预计将通过离岸资本来提供股市买盘支持(回到量化宽松),而一家总部位于亚洲的对冲基金因错误押注中国和日本市场被迫关闭旗下产品,成为头条新闻,该机构的首席投资官是一位拥有数十年市场经验的资深人士,他坦承自己已经失去了信心,这再次提醒我们宏观是非常难以驾驭的,即使经验再丰富也难以匹敌。

说到日本, 10 年期日本公债收益率已从本月低点跳升了 18 个基点,由于日本央行行长 Ueda 明确将 4 月加息列入考虑,收益率在过去两天又出现一波上涨;Ueda 行长周二在记者会上表示,如果“通胀目标在望”,同时工会也一直在劳资谈判中要求更大幅度的加薪,日本央行将“考虑”结束负利率政策,他也认为,日本央行可以避免在终止负利率政策时出现中断,不过交易员也在关注可能随之而来的反驳新闻,这种情况自 Ueda 接任以来经常发生。

回到欧洲和美国,欧洲债券市场发行量创下新高, 1 月份新债发行达 3, 200 亿美元左右,且大部分的市场反应都十分良好,超过 80% 的交易出现利差收窄(即价格上涨)的情况。

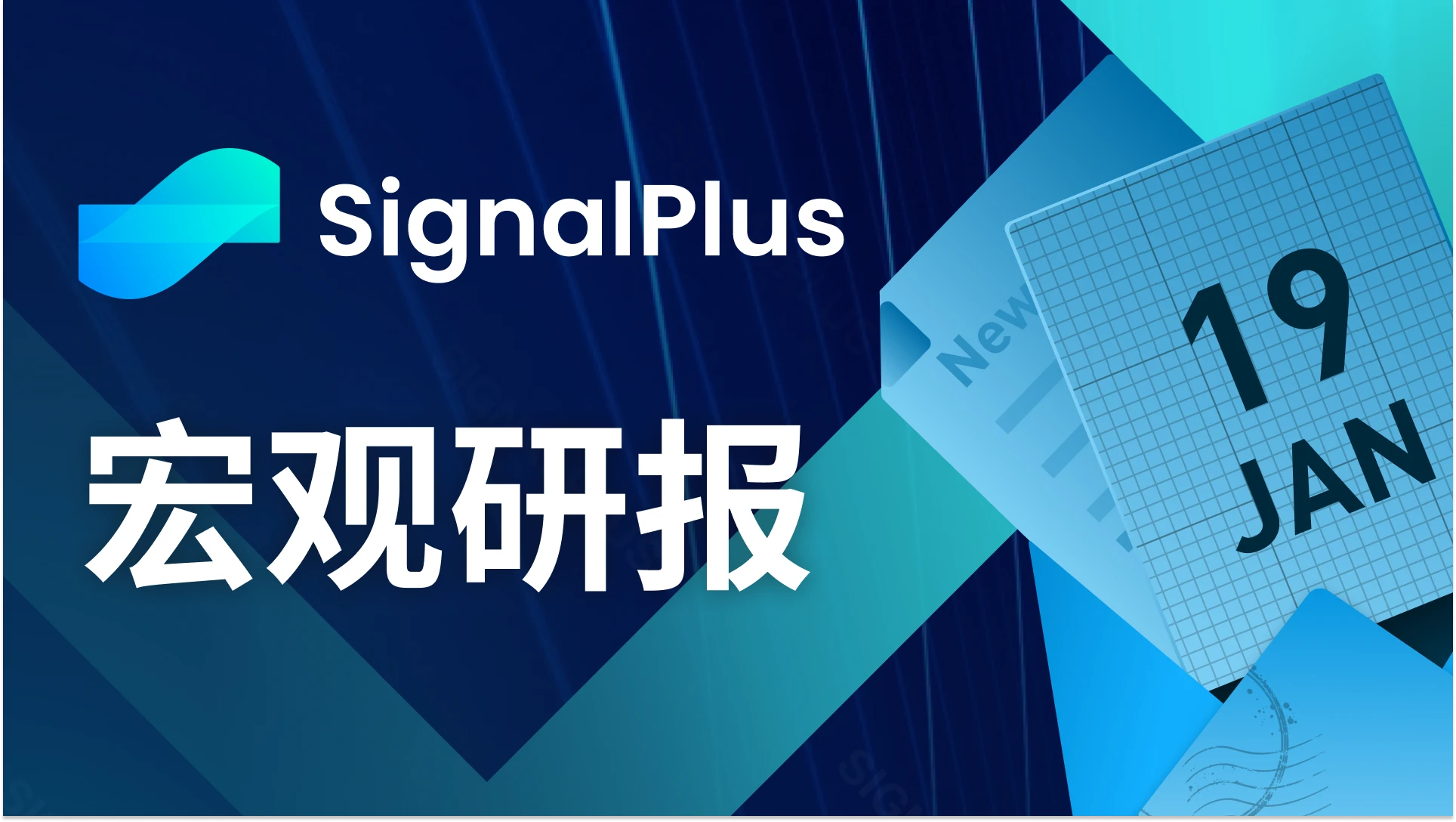

美国方面,创纪录的 2 年期美债拍卖(单次 600 亿美元)的市场需求也不错,发行价格 4.365% 恰好与屏幕价格相符,投标超过 1, 542 亿美元,投标倍数为 2.57 ,交易商占比落至去年 7 月以来最低的 14.8% ,考虑到最近因油价反弹而重新出现的通胀风险,整体拍卖结果相当不错。

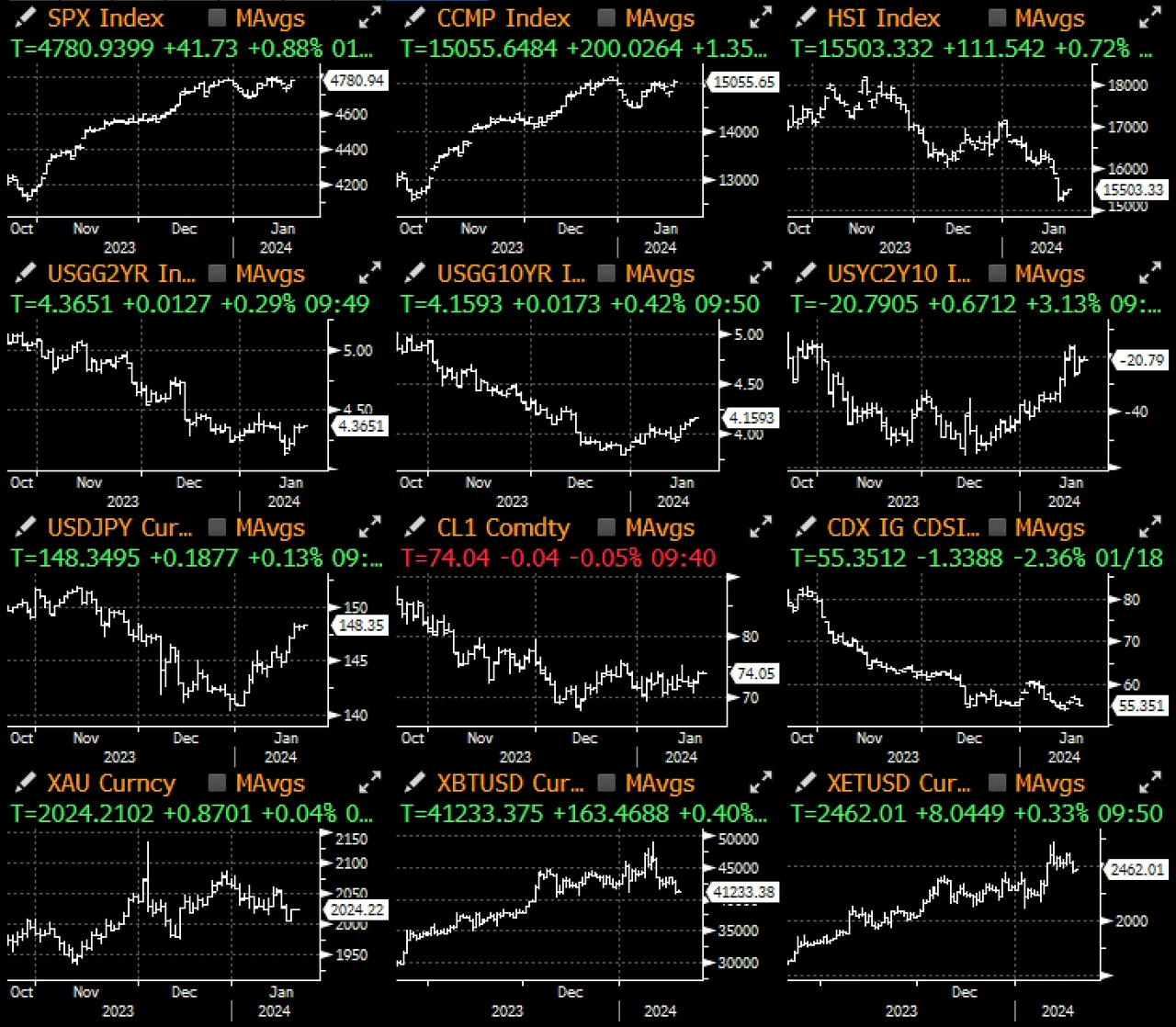

市场整体上较为平静,仍在等待美联储、财政部季度再融资、非农就业数据等结果以及月底的到来,企业财报季也将全面展开,因此交易员本周都较为保守。股票和债券在过去 6 个月的负相关性(多元化投资组合的必要条件)逐渐消失,如果相关性回到零(或更糟,转为正相关)可能会加剧 2 月份的资产价格波动,这让人想起 2023 年第二季度的市场下跌情况,轻松的风险交易似乎即将在短期内结束。

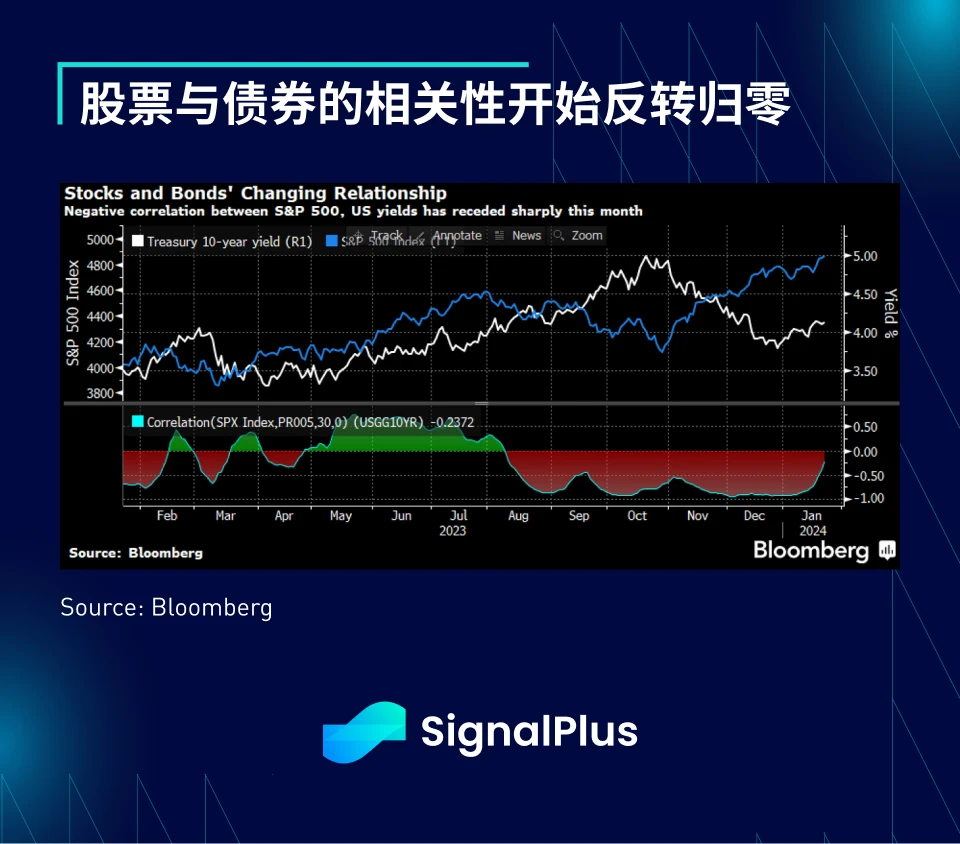

说到蜜月期的结束,GBTC 的资金外流继续对市场造成压力,加密货币价格持续走软,短期内市场缺乏激励因素和资金流入(需要较长期间),导致交易者对短期前景失去信心,过去几天期货多头清算稳步增加。

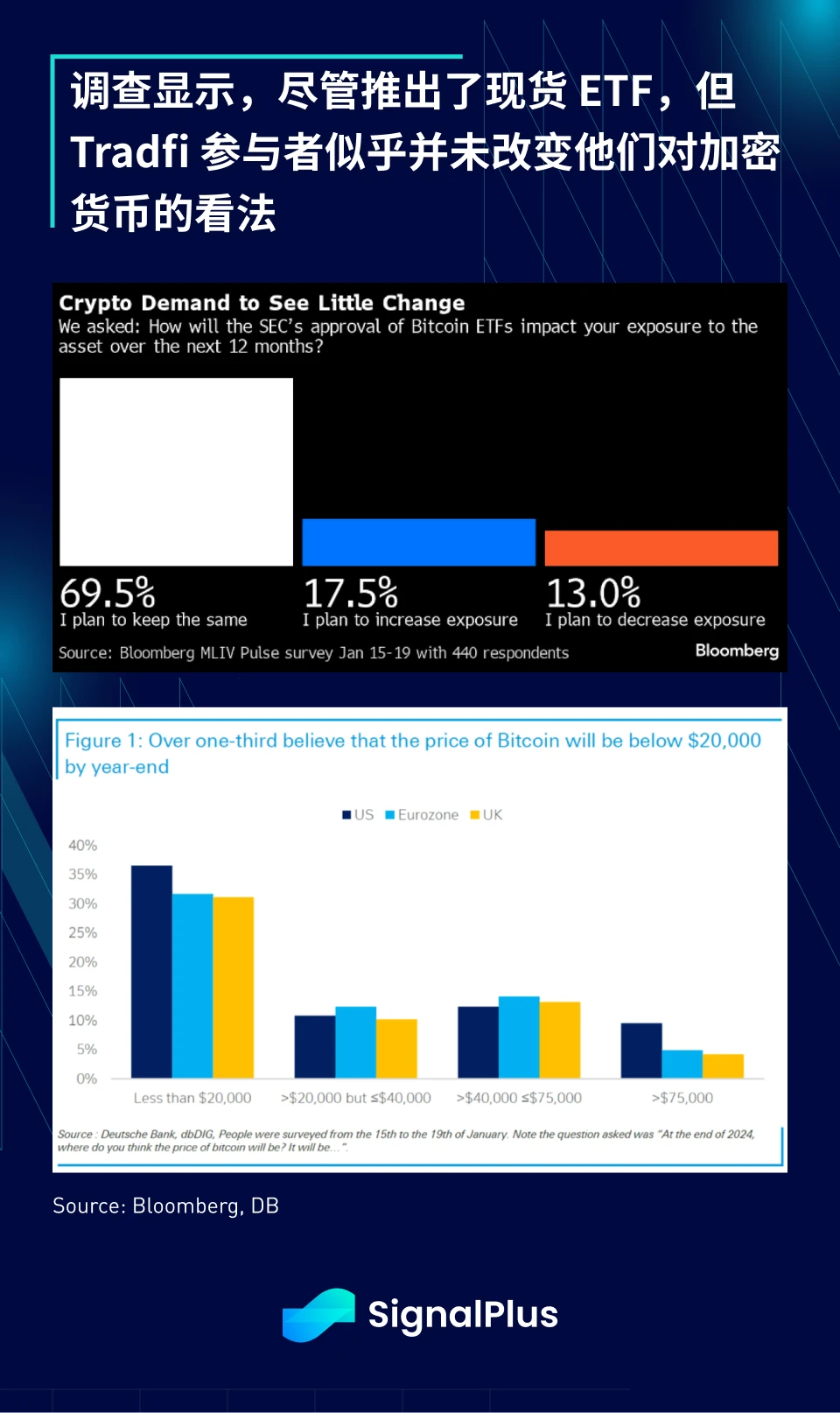

此外,Bloomberg 和一些券商的调查显示,主流群体对加密货币的需求或投资情绪在短期内的变化不大,虽然 ETF 的推出增加了加密货币的合法性,但没有增加虚拟资产的参与度;Deutsche Bank 的一项调查显示, 1/3 的受访者认为 BTC 到年底前将跌至 2 万以下(应该买一些便宜的看跌期权),这与行业参与者的预期非常不同,看来前面的道路仍然漫长!

您可在 ChatGPT 4.0 的 Plugin Store 搜索 SignalPlus ,获取实时加密资讯。如果想即时收到我们的更新,欢迎关注我们的推特账号@SignalPlus_Web3 ,或者加入我们的微信群(添加小助手微信:SignalPlus 123 )、Telegram 群以及 Discord 社群,和更多朋友一起交流互动。

SignalPlus Official Website:https://www.signalplus.com