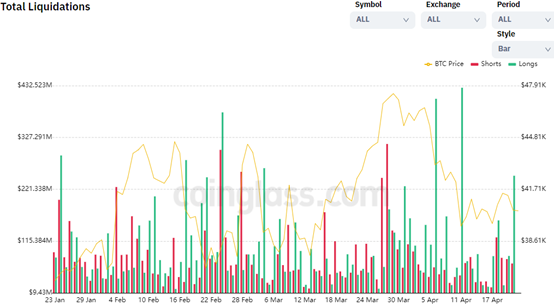

1. Market trend: long positions increased and the market was shaky

The overall market explosion scale maintains a high level. Especially after March 31, 2022, the explosion scale of bulls is always significantly higher than that of bears, indicating that the overall market trend is weak. Recently, the size of bulls in the overall market was up to US $400 million. On April 21, bulls were exposed to US $248 million, while bears were exposed to US $69 million. It can be seen that the frequent losses of bulls mean that the possibility of breaking the current market is still very high.

In terms of daily K-line, the price of BTC shows a shock decline. At present, the moving average is very effective in suppressing BTC. The 120 day moving average can prevent BTC from rebounding upward. In terms of range fluctuation, BTC operates above the US $36077 corresponding to 50% of Fibonacci. Considering that the recent trading volume shows the characteristics of fragmentation, bulls have not organized an effective offensive, which is a high probability event of price decline during the sideways trading period.

2. Interpretation of panic index:

The panic index operates at a position lower than 30. At present, the fluctuation space is very small and has lasted for several trading days. Therefore, the panic index also constitutes the adjustment form of a local triangle. After leaving the triangle area, the unilateral trend of mainstream currencies such as BTC will continue. The panic index has remained below 50 since 2022, indicating that the strength of bulls is not dominant, the panic may spread at any time, and the future price decline is also expected.

3. Dragon and tiger list:

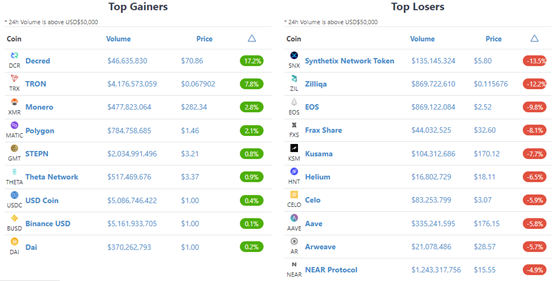

During the overall withdrawal of mainstream currencies, the rising currencies decreased significantly. Among the top 100 currencies in terms of market value, the stable and platform currencies with the highest growth were more resistant to decline, while Dai, usdc, bus and other stable currencies rebounded slightly. Among the rising currencies, DCR has a large increase, while other currencies have a limited increase.

Increase list

DCR

As a cottage version of BTC, the trading volume of DCR is relatively low, and the short-term volume is not enough to attract large funds to enter the market. In the context of the poor performance of most mainstream currencies, the rise of DCR is only a case, so the tracking risk is high and it is not suitable to invest more funds to buy.

Matic

Matic is a protocol and framework for building and connecting Ethereum compatible blockchain networks. Aggregate scalable solutions on Ethereum to support multi chain Ethereum ecosystem.

Matic network is a second layer extensible platform, which realizes fast, simple and safe off chain transactions. It can not only pay transactions, but also realize generalized off chain smart contracts. Matic network is an important contributor to the Ethereum ecosystem. It is committed to the implementation of plasma MVP (minimum running plasma), walletconnect protocol and Ethereum event reminder engine dagger, and has made outstanding contributions. Matic tokens are used for equity bets and participate in the proof consensus mechanism of the side chain network.

Matic's price is stable, and its lock up volume fluctuates slightly. From the perspective of price trend, matic has obvious interval fluctuation characteristics. Therefore, in the case of poor market, matic's short-term fluctuation will appear. In the interval shock stage, the mild trend of matic may continue. The daily trading volume is small, and the price may remain stable.

Decline list

In the decline list, SNx, ZIL and EOS are all currencies with strong short-term performance, and there has been a contraction callback. Therefore, the current market is in the stage of long-term wait-and-see and strong short strength. The bottom will further confirm that BTC and mainstream currencies will stabilize and rise.