加密货币的历史可以追溯到 20 世纪 80 年代的金融繁荣时期,当时的金融文化在《颠倒乾坤》和《华尔街》等电影的映衬下得到升华,1983 年,密码学家先驱 David Chaum 发表了研究成果,为电子支付、区块链和加密货币奠定了基础。

在当时这些都是超时代的想法,多年来加密货币很少在自由市场「自由主义政策」圈子之外被讨论,但在 2009 年出现了拐点——Satoshi Nakotomo 中本聪于 2009 年开发了比特币,2010 年前后的加密市场迎来爆炸式增长。

如今市场上存在数以万计的加密货币,对于无论是投资者还是监管机构来说都是一个充满挑战的市场。许多人认为流通中的 token 种类太多,而将其比作约 25 年前的「互联网泡沫」。

为了分析加密市场,我们对十年来崩盘消失的 token 进行了可视化分析,从失败的 ICO 到人们对市场兴趣的减弱。

我们参考了 Coinopsy 的 2400 多种消失 token 的数据,汇编了每种 token 当前状态的数据,分析了每种 token 在过去 10 年中的表现,并记录了 token 被淘汰的时间和原因。

在整理完这些数据后,我们将其与 CoinMarketCap 每年的历史快照进行了比较,从而为我们提供了曾经在市场上流通的所有 token 的准确数据。

数据总览

在 2017 年,有 704 个现已消失的 token 开始发行流通,比 2016 年的 224 个多。

2018 年是加密行业最危险的一年,有 751 种 token 消失。

2014 年是 token 死亡率最高的一年,793 种 token 中的 76.5% 已不再流通,551 种消失。

2014 的加密崩盘

当回顾加密 token 价格史时,2013 年可以被视为加密第一次大繁荣时代。在无人机到智能手表等新兴技术主导的技术背景下,比特币的价格从 150 美元飙升至 1000 美元,并在 2013 年 11 月达到 1127 美元的高点。在比特币暴涨前,加密市场上只有 14 种 token,截至 2022 年,只有比特币和莱特币留在前 10 名。

比特币价格的飙升导致了一波竞争 token 争夺市场利益的浪潮。数据显示,2013 年有 84 种 token 进入市场,2014 年有 607 种,都是为了利用比特币在 2014 年初的崩盘中获利,当时比特币交易大多与暗网黑市丝绸之路有关。

然而,2014 年新兴加密货币的挤兑并未持续。数据显示,2014 年建立的 token 中有 91% 最终因交易量低或被放弃而消失(当然也有例外,比如狗狗币),许多尝试垄断早期加密市场的机会主义者都以失败告终。

加密货币价格第二次激增

2017 年成为加密历史上的「夏之恋」,所有人都热爱加密,新兴的区块链技术首次吸引到全球商业领袖的注意,导致投资激增。2017 年 7 月,高盛技术分析师 Sheba Jafari 预测,到今年年底,比特币将达 3600 美元。

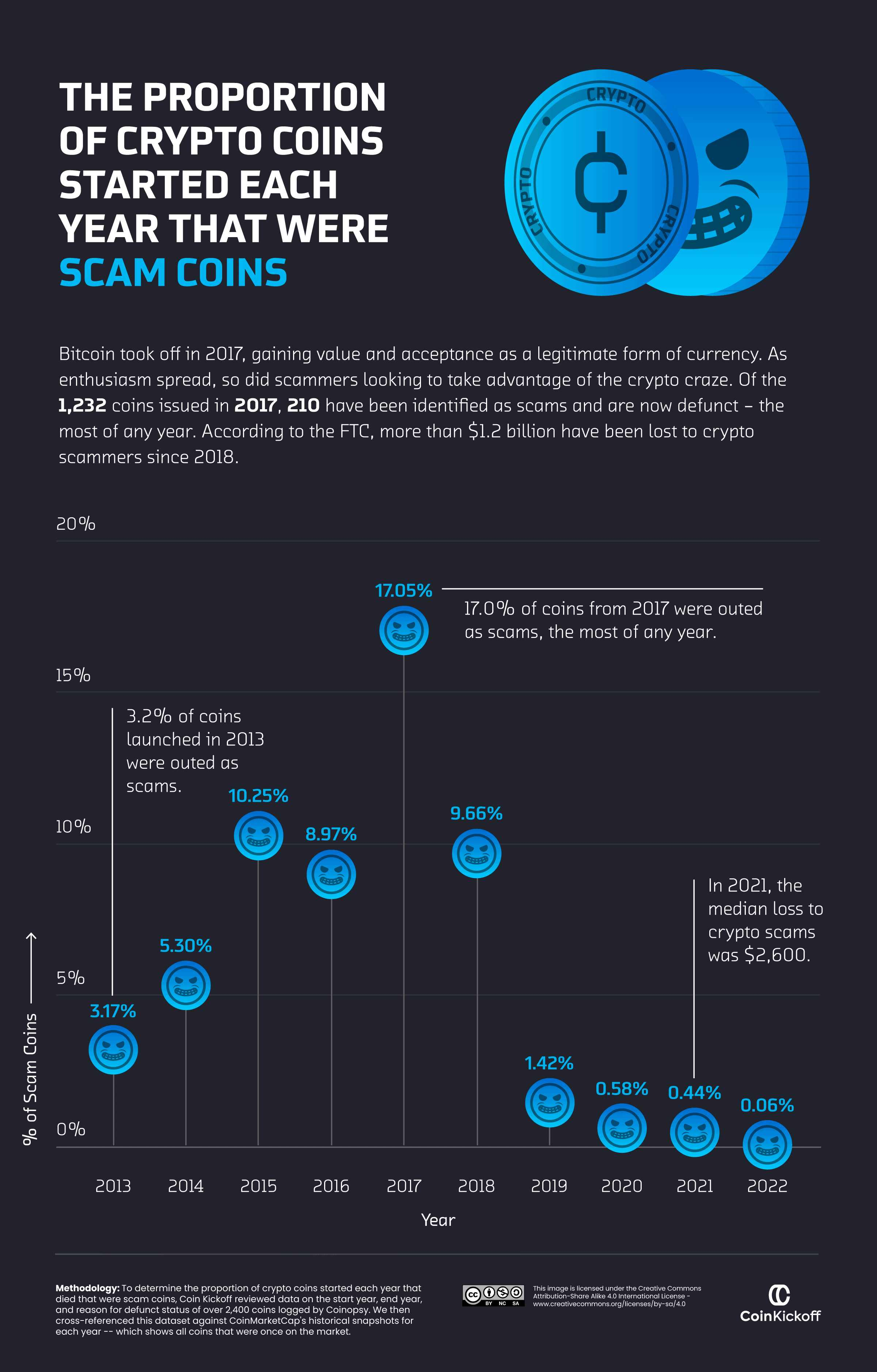

这一年出现了许多利润丰厚的 ICO,其中最著名的是 Filecoin,它积累了 2.57 亿美元。然而,一切并不像看上去的那样,当年有 704 种现已消失的 token 进入加密市场流通,是过去十年中数量最多的一年。ICO 咨询公司 Stasis Group 2018 年的一份报告中称,2017 年 80% 的 ICO 被认定为骗局,共积累了 119 亿美元资产。

我们的研究表明,2018 年死亡的 751 枚硬币中,有 30% 是欺诈性质的,也是过去十年中最高的一年。最著名的 ICO 骗局是越南 token PinCoin 和 iFan。当地记者揭露了该类公司诈骗多达 3.2 万名投资者,金额高达 6.6 亿美元,胡志明市警方当时也对此进行了调查。

2014 年的 token 数据

但其实人们很容易忘记一件事,加密货币仍处于起步阶段。股市的历史却已经有数百年了,第一笔比特币交易是在 2010 年在佛罗里达州的一家披萨店进行的,市场尚未真正站稳脚跟,经济学家们对加密行业的未来也存在较大分歧。

加密市场已经向大家证明加密货币交易和投资是很容易颠覆传统金融体系的,但该行业存在的失败案例也非常普遍。中国信息通信研究院(CAICT)的一份报告表明,迄今为止市场上 92% 的区块链项目处于非活跃状态,平均存活寿命仅为 1.22 年。

早期加密市场的情况对许多有抱负的 token 来说是致命的。根据我们的研究,在 2013 年至 2018 年间,每年推出的 token 中,有一半以上已经不复存在。2014 年,在加密货币第一次大繁荣的背景下发行的 token 中,超过四分之三(76.5%)已经消失。

数据转好,2020 年以来只有 16 种 token 被放弃

根据区块链研究平台 LongHash 的数据,63.1% 的加密货币消失是因为被投资者放弃,导致了价格暴跌崩盘。在一个拥有 12,000 多种 token 的饱和市场中,善意的项目自然无法吸引人们的兴趣。Coinopsy 总结了一种 token 可能被抛弃的原因,从过时的区块链设计到开发者的个人情况。

比如,3 个月内交易量低于 1000 美元,或者项目网站停止更新等,都会被视为已死的 token。

数据显示,加密货币在 2013 年第一次价格飙升后,一些 token 消失的概率开始增加。2013 年 61.1% 的 token 和 2014 年 69.5% 的 token 消失了。然而在那之后的数据上看,token 被抛弃消失的比率越来越低,也说明了人们对加密货币失去兴趣的频率在变小。自 2020 年以来,由于缺乏投资,只有 16 种 token 从市场上除名。尽管如此,人们还是担心 2022 年加密货币价值的大幅下跌将导致未来更多的 token 被抛弃。

2017 年是加密骗局的高峰期

由于加密市场缺乏监管,欺诈计划和机会主义骗局在加密市场存在至今并且占了很大比例。除了这些为诈骗而生的 token 外,犯罪分子还可以使用比特币和以太坊等主流币来欺骗投资者。

联邦贸易委员会报告称,自 2021 年初以来,已有超过 4.6 万人成为加密货币骗局的受害者,总计损失超过 10 亿美元。Chainanalysis 的数据显示,在 2021 年最新的价格飙升后,人们对该市场的兴趣再次高涨,导致了一波加密货币犯罪热潮,涉及金额高达 140 亿美元。

尽管如此,自 2019 年以来发行的 token 中只有不到 2% 被揭露为诈骗 token。2017 年是加密诈骗的顶峰,当时 17% 的 token 是欺诈性的(1232 种 token 中 210 种被认为是诈骗币现已消失),欺诈者在 2017 年的 ICO 热潮期间赚取了 4.9 亿美元。

当公司变得足够大,可以在股市上交易时,它们会发起 IPO,从公众投资者那里筹集资金。相比之下,ICO 是一个吸引人们对新推出的加密货币购买的主要渠道,投资者购买 token,但他们也可以提供与公司产品相关的更广泛的利益关系,包括公司本身的股份。

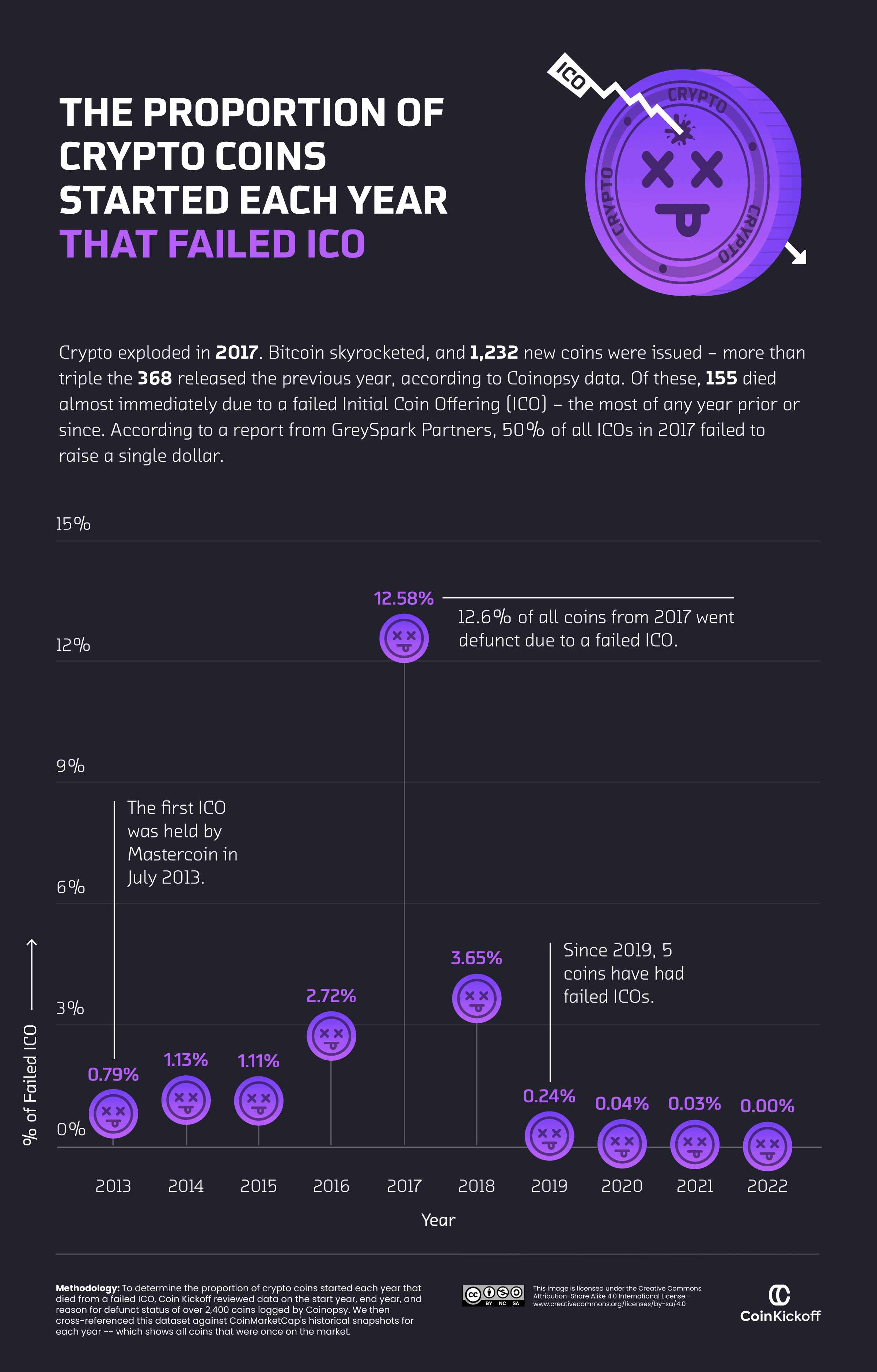

Mastercoin 是首个在 2013 年推出 ICO 的项目,随着主流对加密货币的兴趣随着其价格的上涨而增长,这种做法在 2017 年迎来巅峰。尽管如此,我们的研究表明,当年推出的所有 token 中有 12.6% 由于 ICO 失败而失效——比过去十年中的任何其他年份都要多。

咨询公司 GreySpark Partners 的研究发现,2017 年和 2018 年推出的所有 ICO 中有近一半未能筹集到任何资金,而且这种做法容易受到欺诈,最终导致监管加强,对该行业的违规行为进行严厉处罚。因此,我们的数据显示,只有 5 种 token 的 ICO 失败了。加密货币经历了第一个动荡的十年后,接下来会发生什么?

加密货币市场正在以前所未有的速度增长,快速进步的技术正在带来新的投资机会——最引人注目的是 2021 年的 NFT 热潮。比特币仍然占据市场主导地位,一些投资者预测到 2023 年其价格可能会达到 10 万美元。然而 2021 年,以太坊的价值增长了 409%。尽管俄罗斯入侵乌克兰导致全球不稳定,导致全球经济低迷,但分析师预计到 2030 年,以太坊将为加密行业带来 49 亿美元的价值。

许多专家将加密货币的增长与 2000 年代初的「互联网泡沫」进行了类比,当时的创新导致互联网公司和投资者激增,寻找下一个亚马逊或 eBay。相比之下,2013 年和 2017 年加密货币投资激增,新货币充斥市场,投资者竞相从「下一件大事」中获利。

虽然其中许多 token 因缺乏投资、ICO 失败或诈骗而消失,市场在监管加密货币以保护投资者上也面临着众多挑战。但投资界已经对加密行业重视起来了,加密货币在过去十年中已经证明了其颠覆传统金融市场的能力。