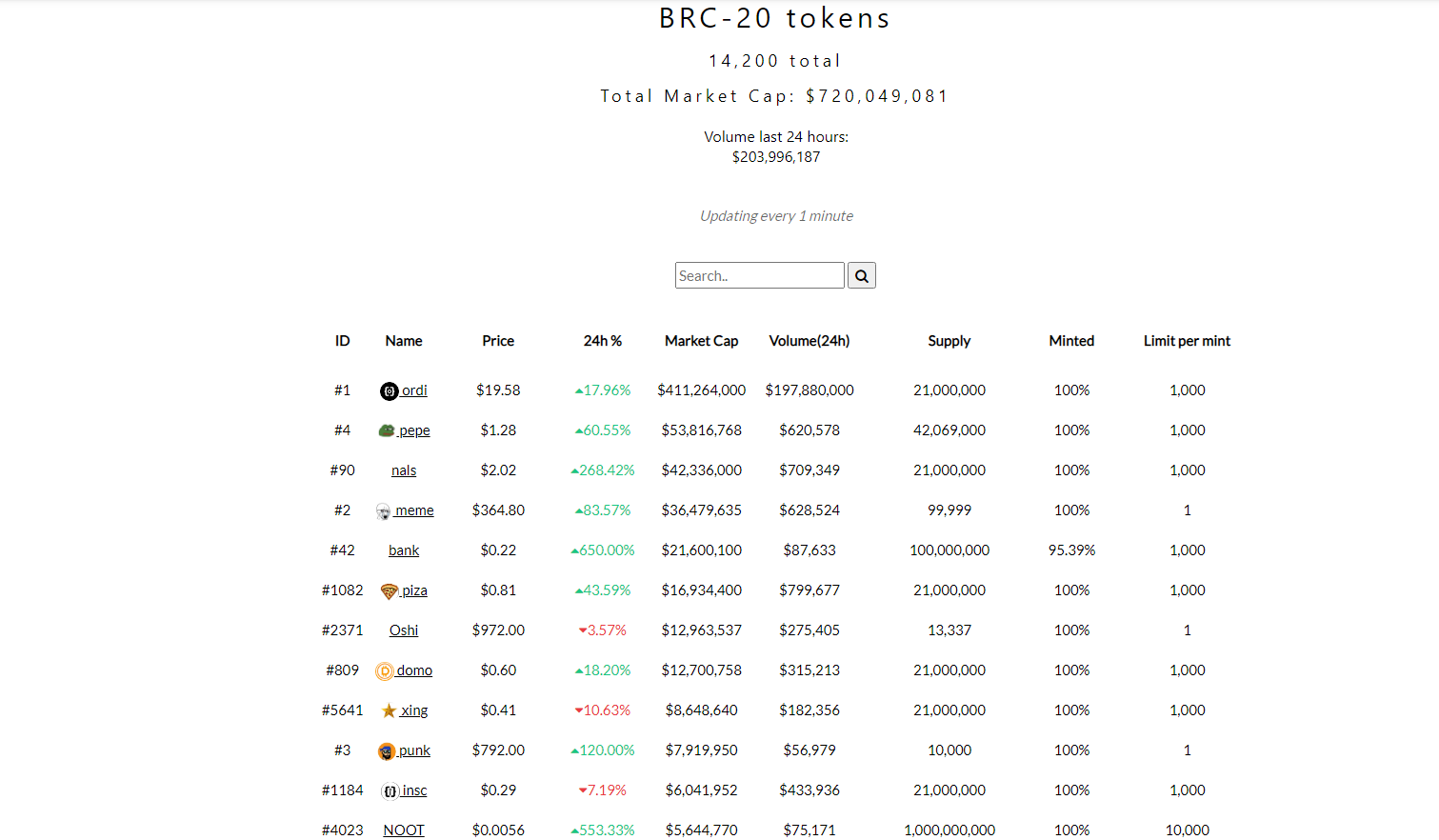

BRC-20 代币市值已“接近”触及 10 亿美元大关,比特币上铸造了 14,200 个代币。其中,Ordinals(ORDI)以4.11亿美元的总市值领跑潮流。

根据网站brc-20.io和Ordspace的数据,比特币网络上的 BRC-20 代币曾经“濒临”达到 10 亿美元的市值,目前又回到了 7 亿美元的区域。 .

BRC-20 拥有 14,200 个代币,其中大部分是模因币,正在蓬勃发展并吸引了加密社区的关注。目前,Ordinals (ORDI) 是上升趋势中领先的 memecoin,稀释价值接近 50 亿美元。

自 4 月初至今,ORDI 强劲爆发,在持续的 memecoin 热潮中竖立了 22,5000%(从 0.11 美元到 25 美元)的柱子。此外,ORDI于5月8日刚刚上线Gate.io和Crypto.com。这两家交易所很可能希望赶上 BRC-20 浪潮。

📣 #Gateio新上市: $ORDI

🔸交易对: $ORDI / $USDT

🔸交易开始时间:5 月 8 日凌晨 02:00(UTC)

贸易:https: //t.co/ExBA5etVlI

存款:https: //t.co/HfIxOcAgML

更多: https ://t.co/2RcrH9D77F pic.twitter.com/mPx63DTwnw

- Gate.io (@gate_io)2023 年 5 月 7 日

在撰写本文时,ORDI 价格已从 29.58 美元的峰值大幅下跌,交易价格约为 15-20 美元。

BRC-20板块中,紧随ORDI之后的是PEPE代币(区别于以太坊上大热的同名memecoin)、MEME、DOMO、NALS……市值从1200万美元到4200万美元不等。

据报道,BRC-20 是 Ordinals 协议最近开发的一种代币标准,目前处于比特币网络的测试阶段。序数允许开发人员将信息分配给网络中的每个卫星,这一过程称为铭文。本质上,BRC-20 代币不使用智能合约,而是需要比特币钱包来铸造和交易代币。

当 Ordinals 团队在比特币上创建 NFT 铸造方法时,推特帐户@domodata 的开发人员于 3 月 8 日推出了 BRC-20,这是建立在 Ordinals 上的新代币标准。

也正是因为社区的好奇心,造就了目前的BRC-20热潮,助推比特币交易手续费屡创新高,甚至造成网络拥堵,迫使币安多次停止提现。。根据 Dune Analytics 的统计,65% 的比特币交易来自 BRC-20。

目前,自 2022 年 12 月底以来,比特币网络的每日交易量翻了一番,达到 534,000 笔交易。最近区块被 BRC-20 交易填充,每笔交易的汽油费一度高达 20 美元,比之前的 1-2 美元框架增加了 800%。