自 4 月初以来,Pepe 代币价格 (PEPE) 的涨幅一直领先于整个加密货币市场。然而,从 5 月 5 日开始的急剧下跌抹去了这些收益的很大一部分。

尽管下跌,但今天 MEME 价格反弹,可能开启另一轮牛市。这将是对历史高位的看涨逆转,还是只是小幅反弹?继续阅读下文以了解有关 PEPE 价格预测的更多信息。

Pepe 引领了“表情包季节”,14 天内上涨了 2400%。上涨趋势导致 5 月 5 日创下 0.000044 美元的历史新高。

然而,PEPE 此后下跌,导致 5 月 8 日的最低价格为 0.000018 美元,触及 0.618 长期斐波拉契回撤支撑位。如果下跌只是修正,则该水平通常充当底部。

相对强度指数 (RSI) 给出了混合结果。通过使用 RSI 作为动量指标,交易者可以XEM处于超买或超卖状态,从而决定是增持还是卖出资产。

如果RSI在50以上且呈上升趋势,则多头有优势,但如果指标在50以下,则相反。虽然该指标目前低于 50,但该指标正在向上移动。

此外,它在达到 25(绿色符号)的超卖水平后恢复。因此,该指标并不能确定数字资产XEM处于上升趋势还是下降趋势。

PEPE/USDT 2小时图|资料来源: TradingView

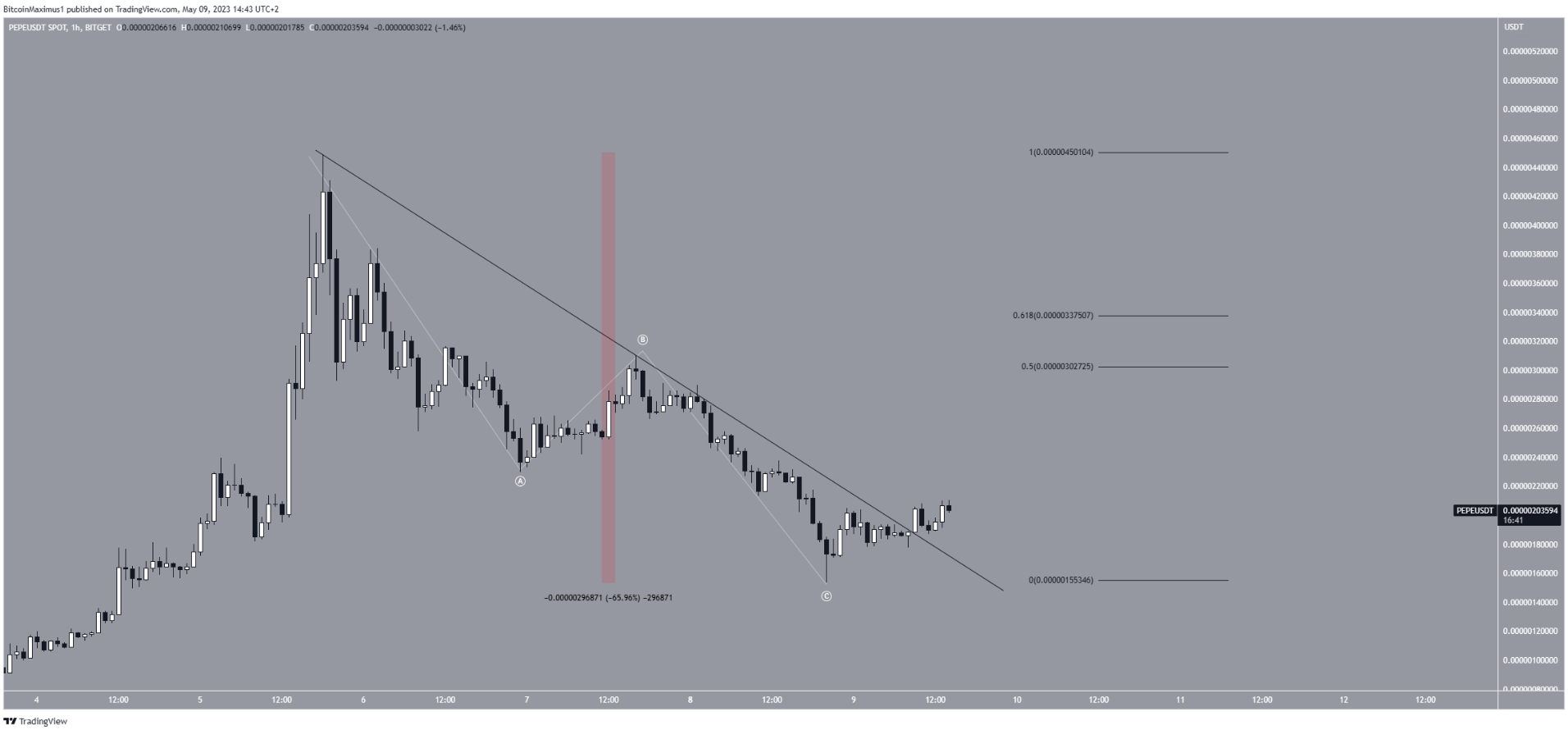

短期小时图的技术分析提供了更乐观的 PEPE 价格预测。这是由于艾略特波浪理论和价格行为。

浪数表明价格已经完成了ABC修正结构(白色)。下行趋势恰好在 0.618 斐波拉契回撤支撑处结束,这一事实与正在进行的修正一致。

接下来,价格突破历史高点形成的下行阻力线。这更符合 PEPE 价格调整已经结束并且牛市已经开始的可能性。

如果是,价格将反弹至 0.5-0.618 斐波拉契回撤阻力区域 0.000030-0.0000034 美元。

达到该水平后的反应可能会决定反弹XEM小幅反弹还是新的向上运动,这将使价格再创历史新高。

每小时PEPE/USDT图表|资料来源: TradingView

然而,跌破 5 月 8 日低点将使这一看涨预测无效。

在这种情况下,PEPE 价格可能会跌至下一个支撑位 0.000010 美元。