随着比特币反弹,加密货币行业在2023年1月出现复苏迹象,绝大多数指标都展现了强劲的上涨态势,下面就让我们一起来看看吧。

“”

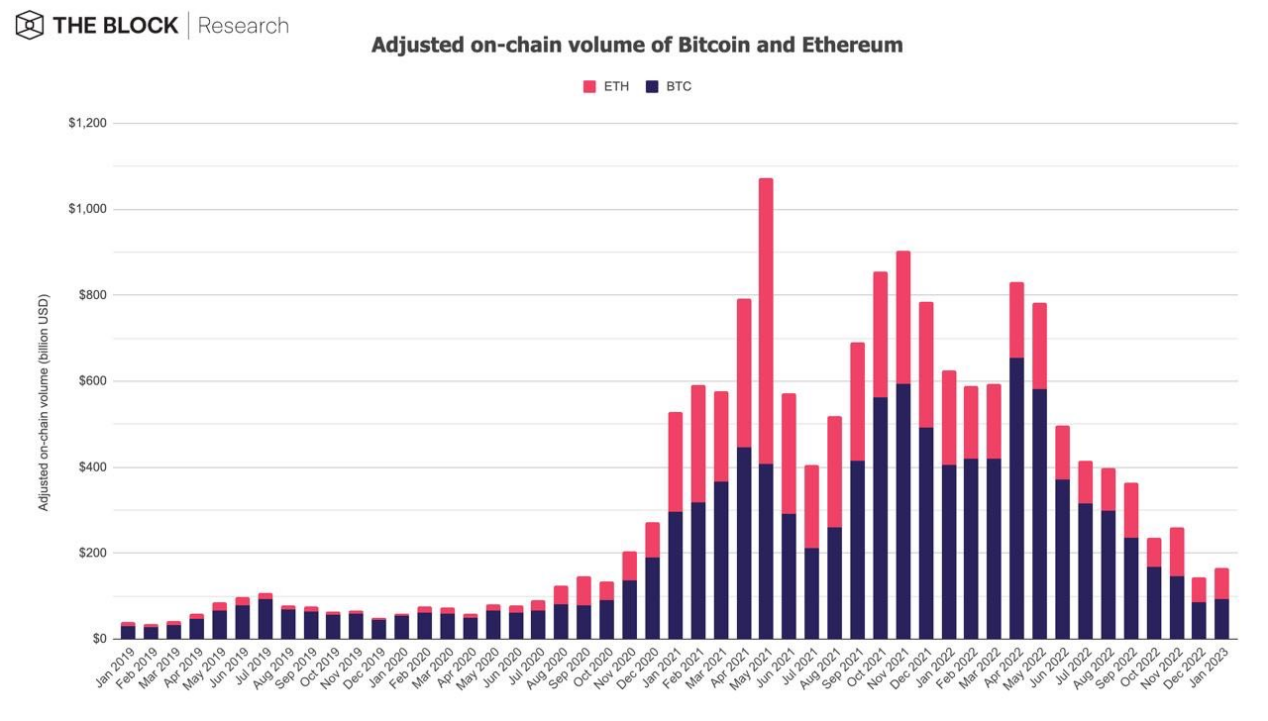

1、调整后链上总交易额增加了 14.6%,达到1650亿美元,其中比特币链上交易额增长8.1%, 以太坊链交易额增长24.1%。

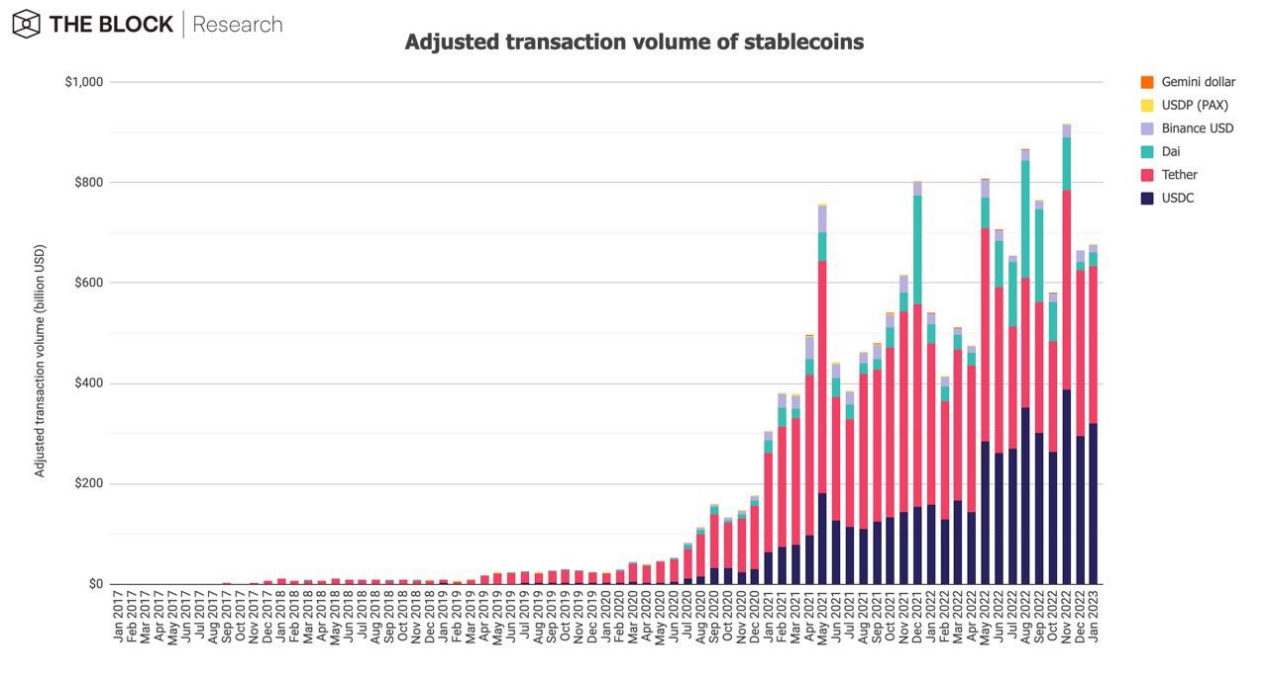

2、调整后的稳定币链上交易额增长至6672亿美元,涨幅约为1.7%;已发行稳定币供应量则进一步收缩至1327亿美元,降幅约为1.9%,其中美元稳定币USDT的市场份额上升至 53.1%,USDC则下降至29.5%。

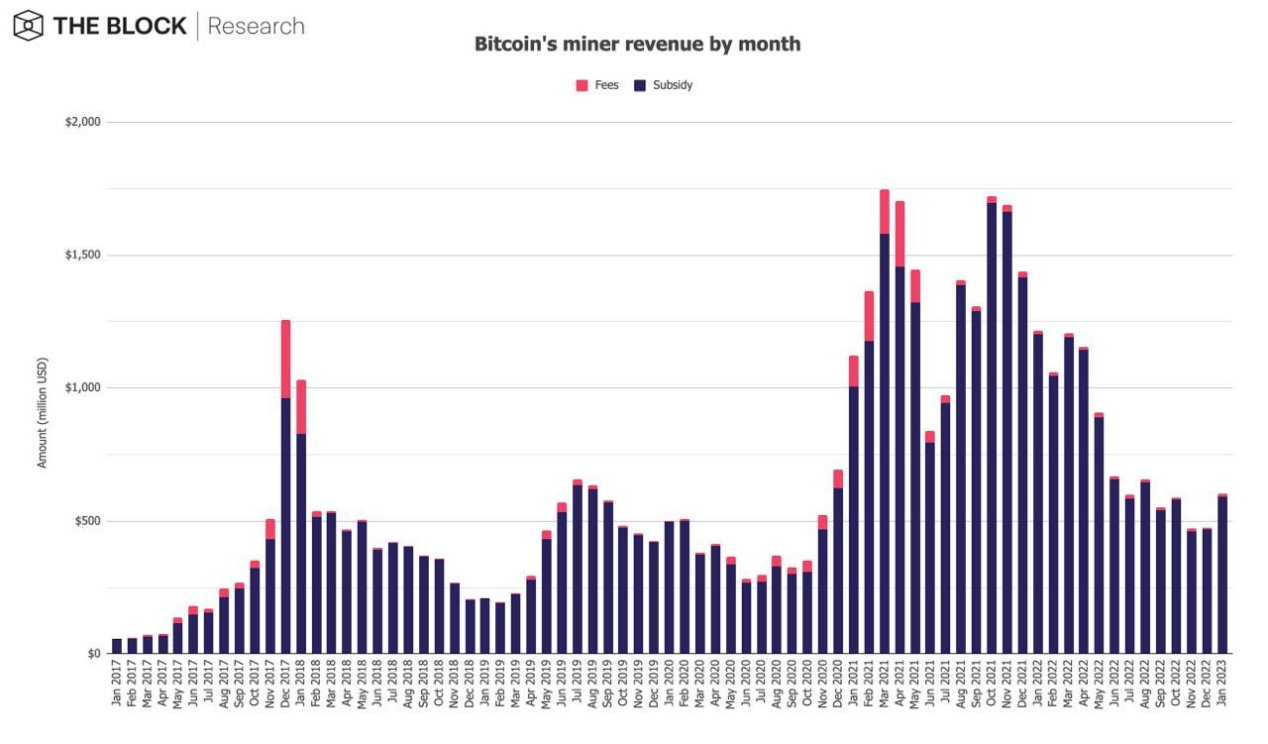

3、比特币矿工收入上涨26.1%至6.012亿美元,以太坊质押收入增长26.7%,达到1.018亿美元。

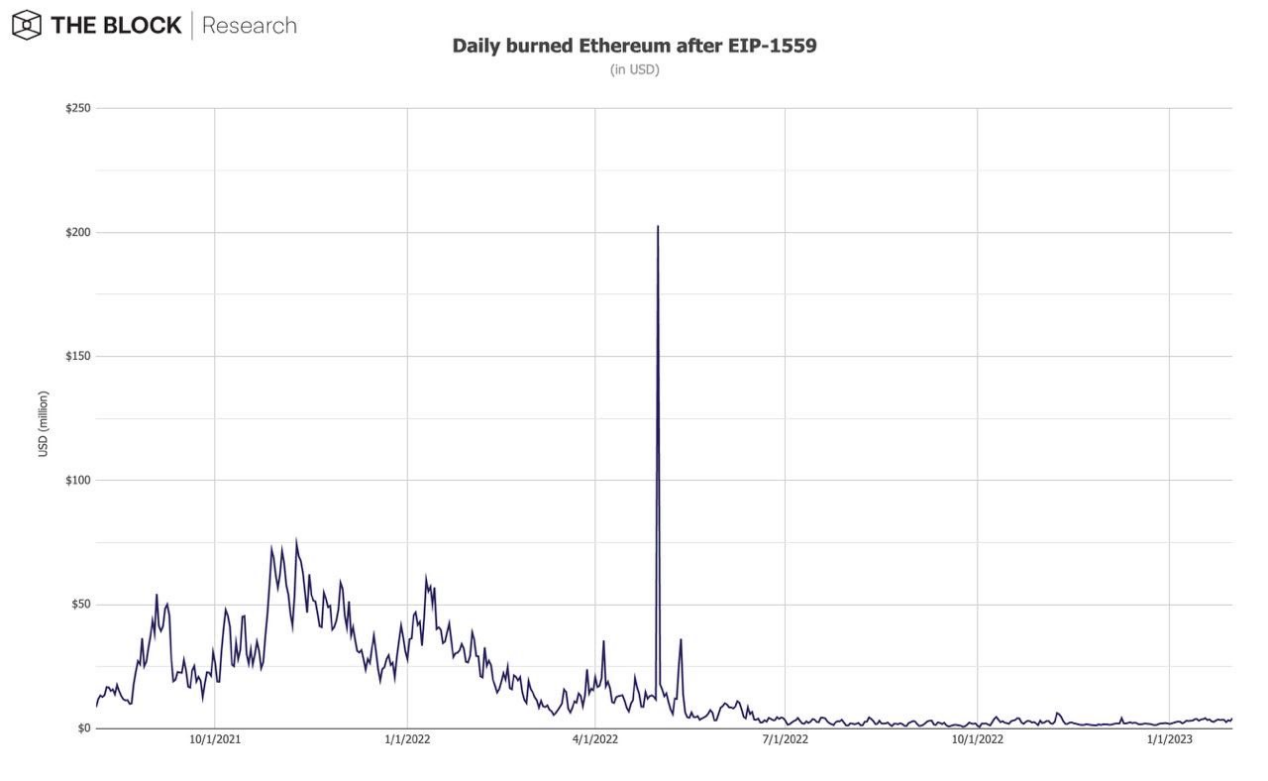

4、一月份以太坊网络共销毁了65,059枚ETH,价值相当于9,570万美元。2022年5月,以太坊网络销毁ETH数量较多是因为YugaLabs元宇宙项目Otherside销售虚拟地块引起的。自2021年8月上旬实施EIP-1559以来,以太坊总计销毁了约286万枚ETH,约合88.8亿美元。

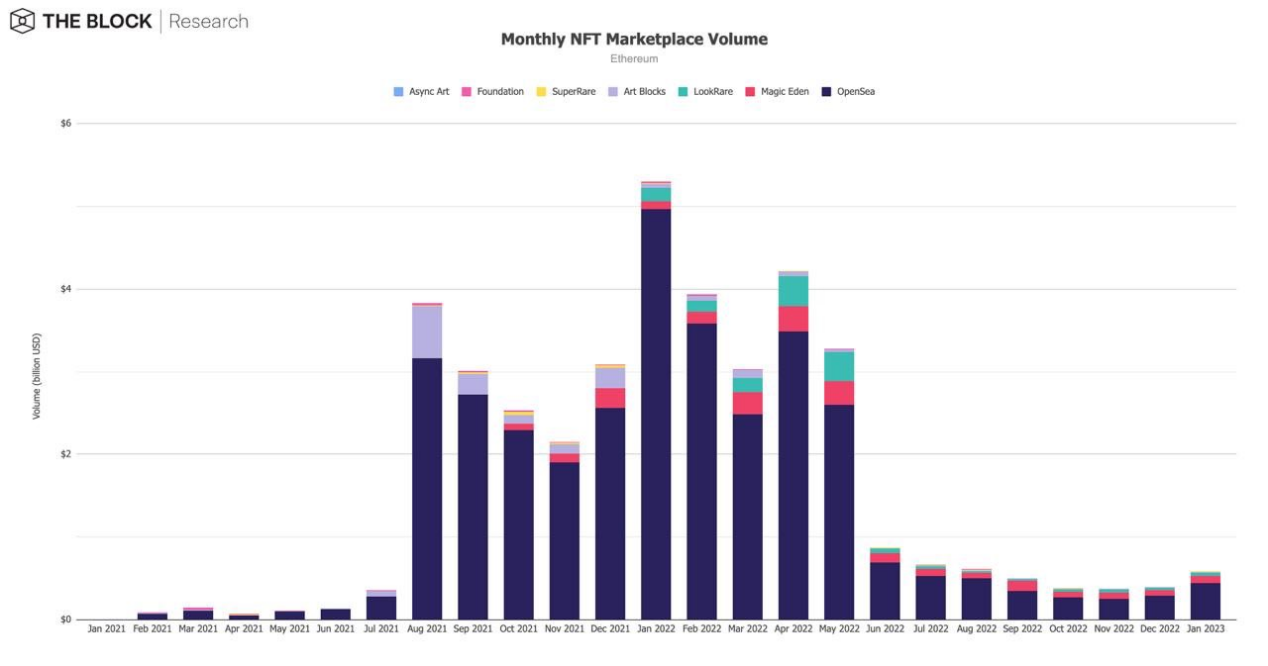

5、1月以太坊链上NFT市场交易额接近6亿美元(5.89亿美元)涨幅达到46.8%。

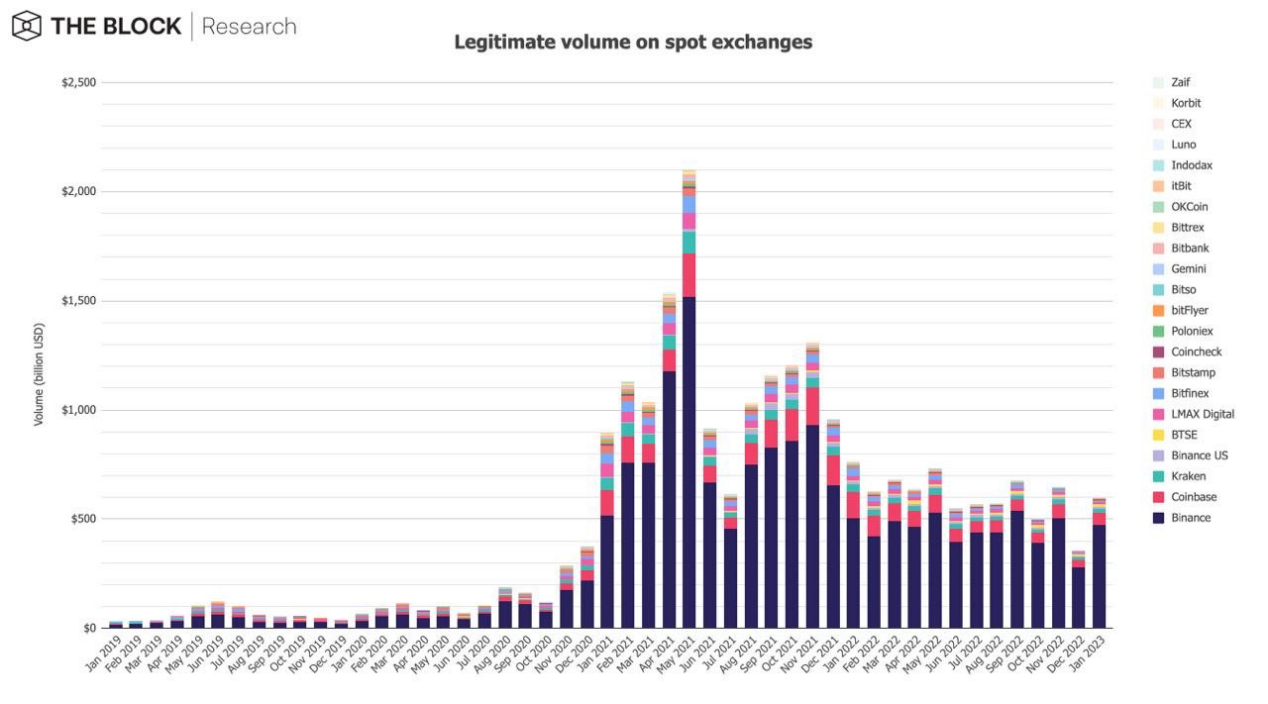

6、合规中心化交易所(CEX)的现货量在一月份增加了67.2%,达到约5976亿美元。

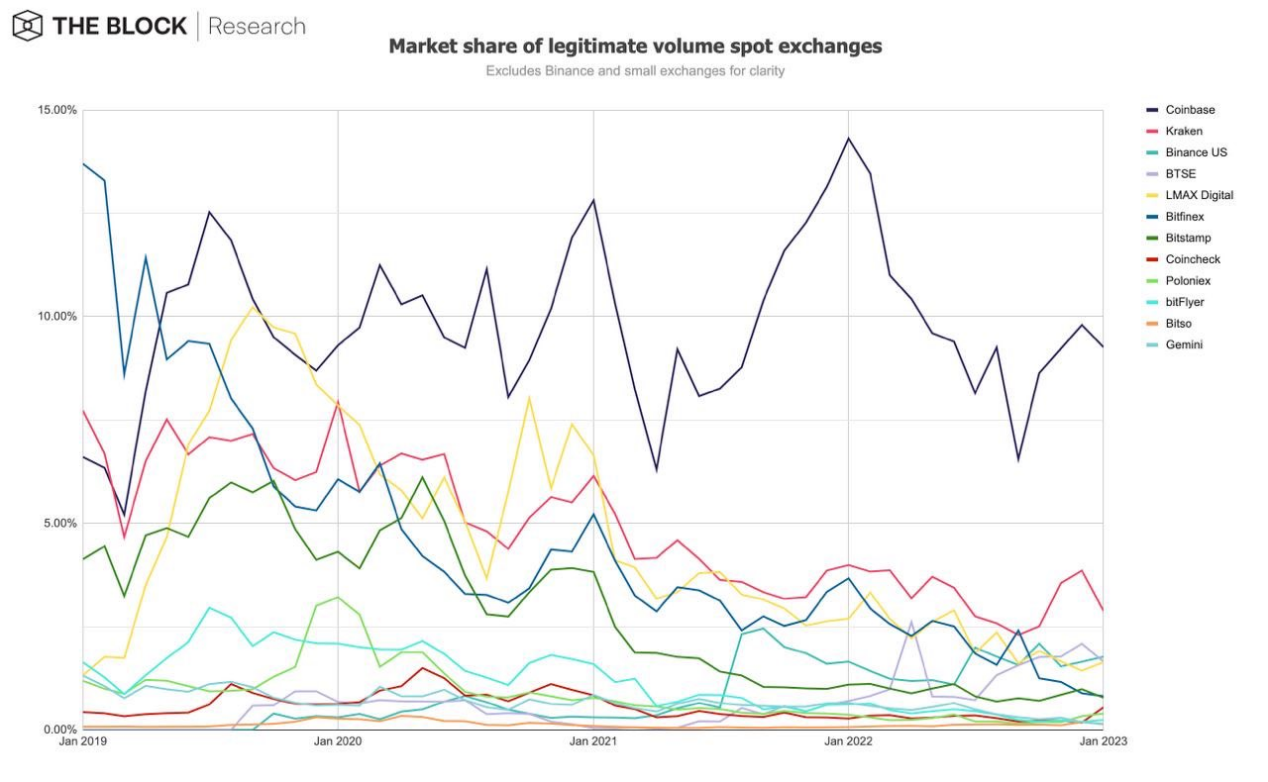

7、加密货币交易所的市场份额变化值得关注:Binance在一月份的市场份额达到79.3%,Coinbase为9.3%,Kraken为2.9%,Binance US为1.8%。

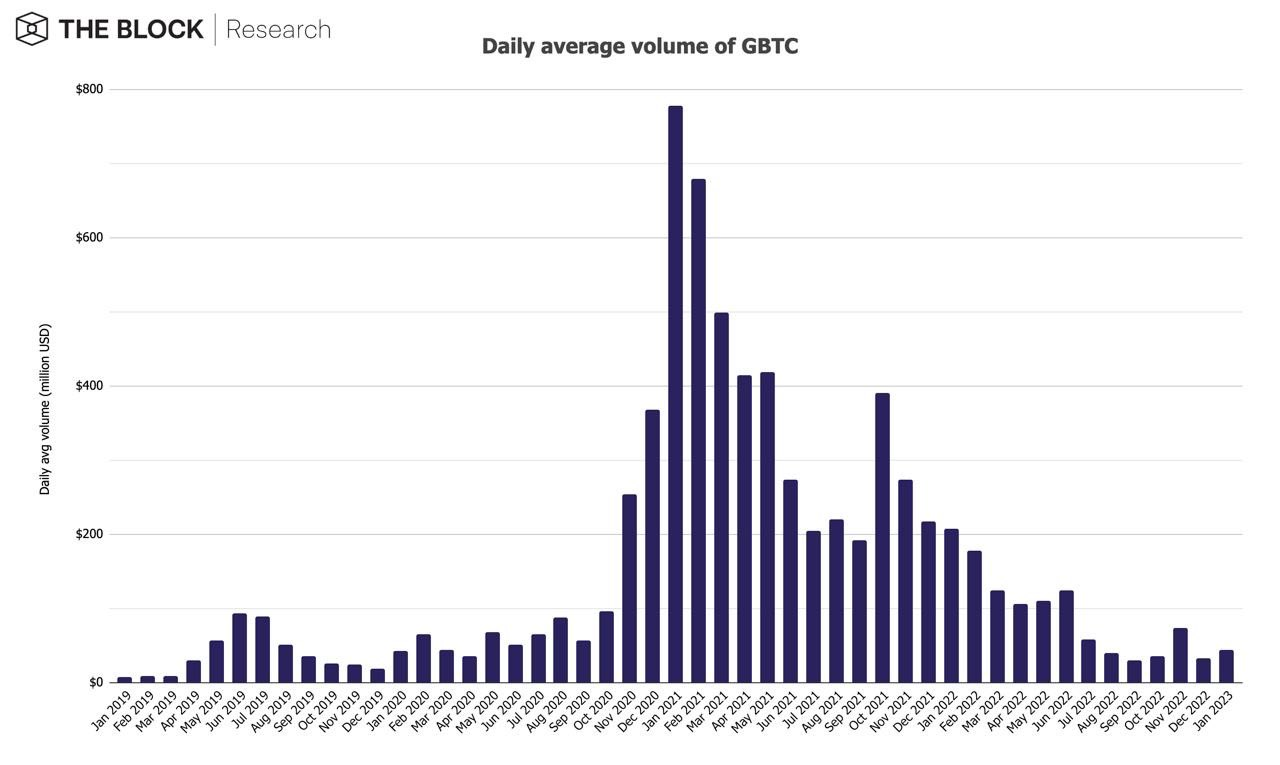

8、灰度的比特币信托近GBTC日均交易额在一月增长了32.4%,升至4400万美元。

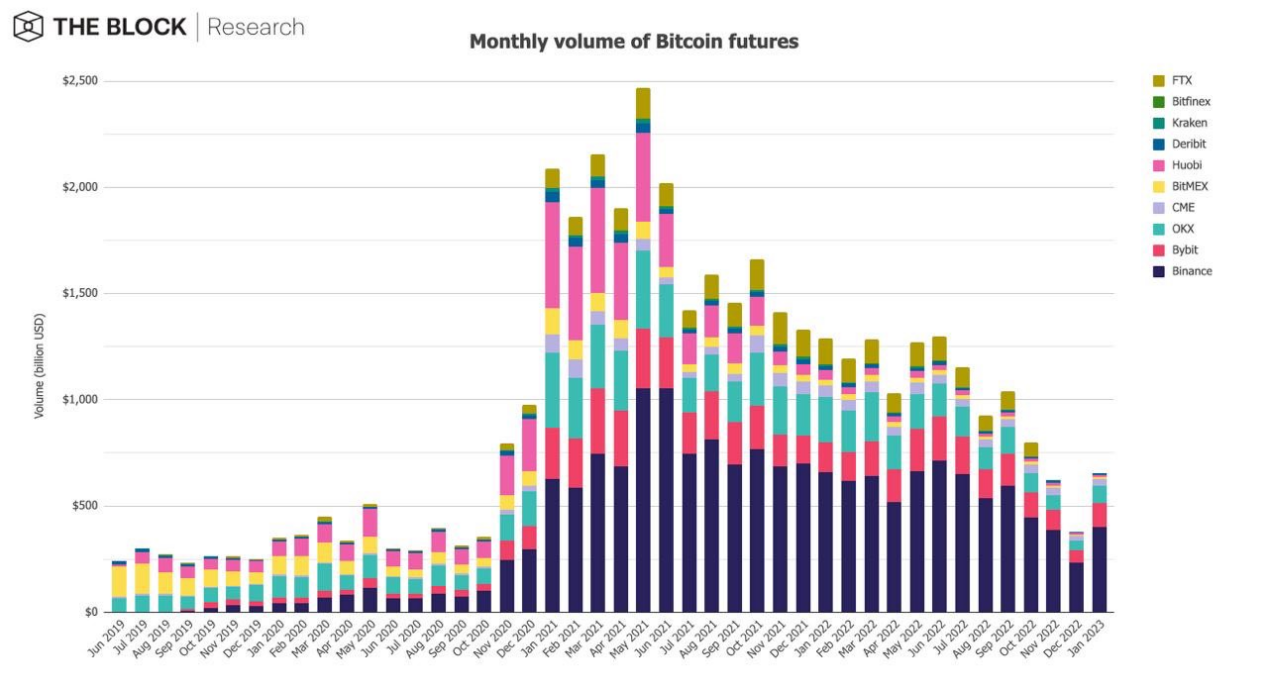

9、在加密期货方面,比特币和以太坊期货持仓量均出现上涨,其中比特币期货持仓量上涨21.3%,以太坊期货持仓量上涨15.9%;在期货交易额方面,比特币和以太坊期货交易额也出现上涨,其中比特币期货交易额在1月增加73%达到6560亿美元。

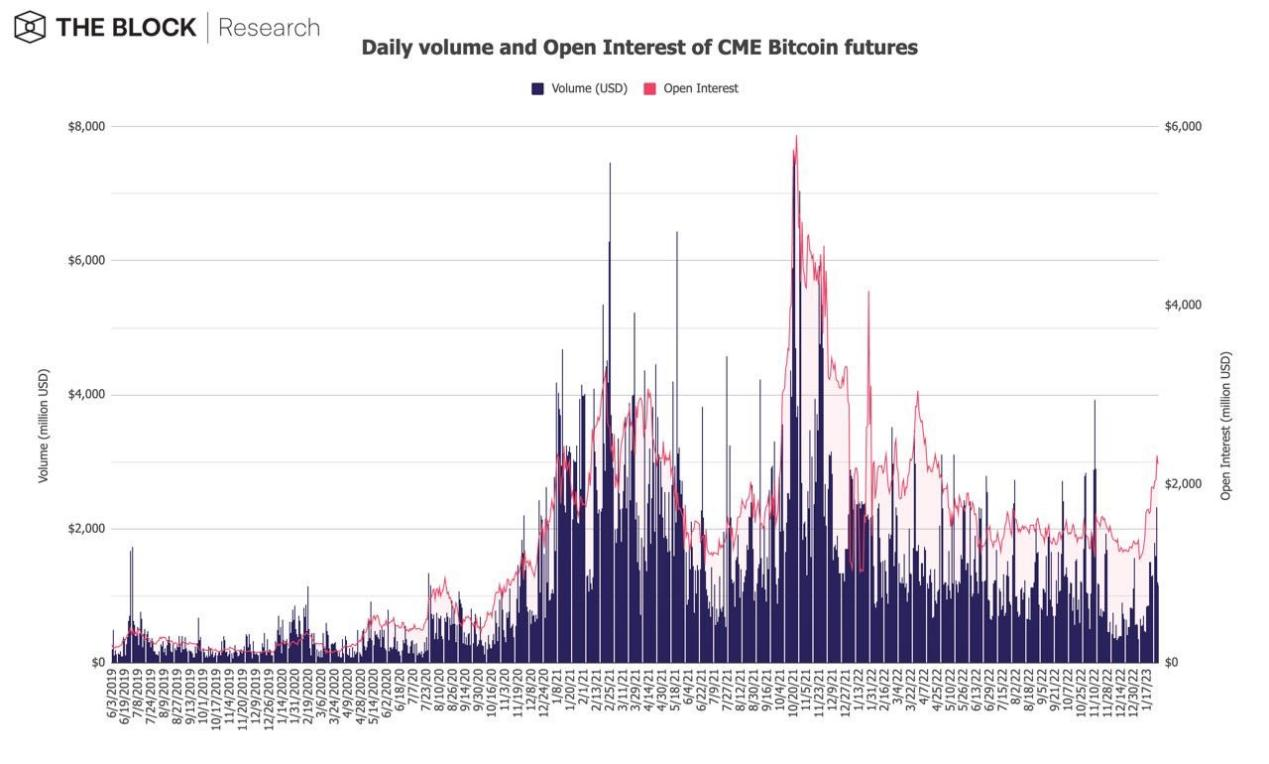

10、芝商所一月比特币期货持仓量增加了63.2%,达到22.2亿美元,日均成交金额涨幅达到55.8%,升至9.85亿美元。

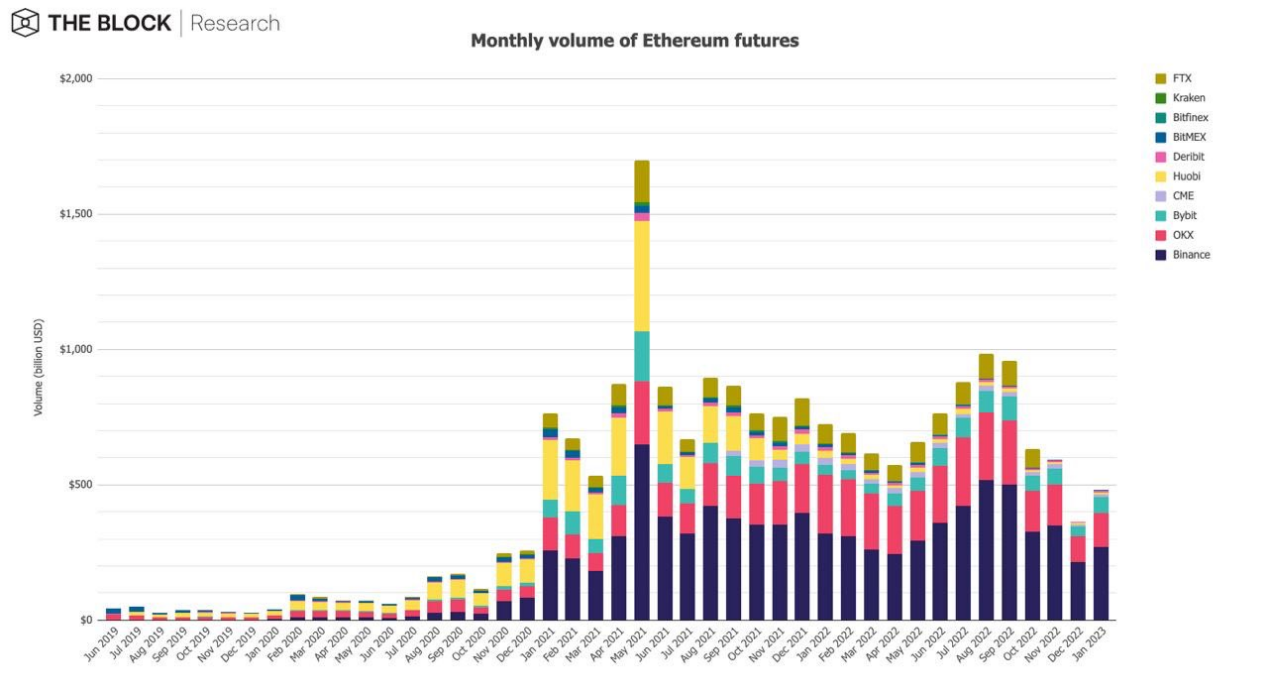

11、在以太坊期货方面,月均交易额达到4810亿美元,涨幅为32.1%。

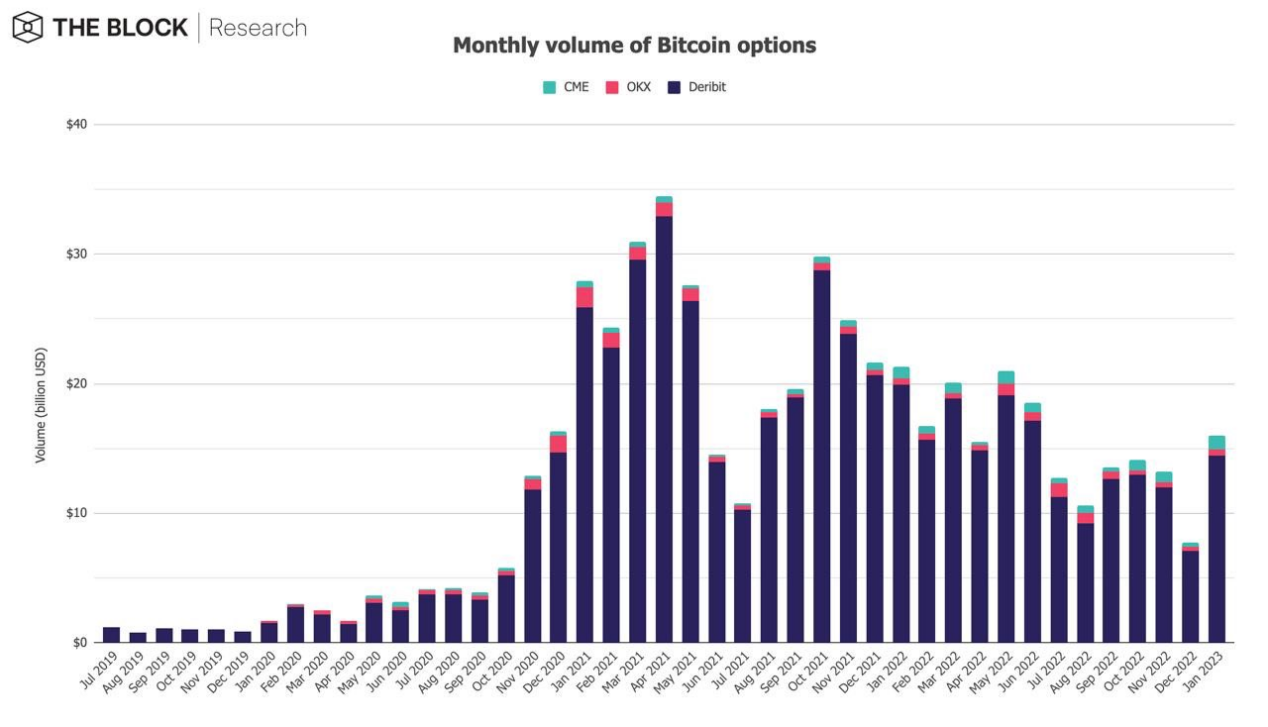

12、在加密货币期权方面,比特币和以太坊期权持仓量也都出现上涨,其中比特币期权持仓量涨幅达到116.5%,以太坊期权持仓量涨幅为71.7%。比特币和以太坊期权交易额同样普涨,其中比特币期权交易额在1月份增长了107.8%,达到160亿美元;以太坊期权交易额在1月份增长了54.5,达到85亿美元。