Masayoshi Son is back.

In recent years, when people mention SoftBank, they no longer talk about him being Jack Ma's 'benefactor'. More often, they think of the failed investment in WeWork, the massive losses of the Vision Fund, and the Japanese investor who was repeatedly humbled by the market during the tech bubble.

But today, AI assets are being repriced. The value of Son's shares in Arm and OpenAI is rising. SoftBank's stock price has surged, Son's fortune has climbed back to the top, and he is once again Asia's richest person.

Evaporating $70 Billion

People fear the unknown, so someone who hasn't experienced a bubble bursting might be afraid.

But not Masayoshi Son. At 67, he has experienced the peak of the internet 20 years ago and was left bruised when the bubble burst.

Son was first chosen by fortune in the late 1990s. Back then, the internet was like a newly discovered magic. Yahoo, portals, e-commerce, online trading—anything related to the web was believed by the capital markets to be rewriting the world. SoftBank also changed during that time. It was no longer just a Japanese software company but became a massive basket filled with internet stocks. Son bet on Yahoo and Yahoo Japan, and SoftBank's stock price was pushed to dizzying heights by the bubble.

In early 2000, Son's wealth became unreal. At that time, his net worth could increase by about $10 billion in a week, even briefly surpassing Bill Gates to become the world's richest person for three days. A Japanese entrepreneur of Korean descent from Kyushu, relying on extreme belief in the internet, suddenly stood at the pinnacle of global wealth.

After the dot-com bubble burst, SoftBank's stock plummeted, and Son's personal wealth evaporated by about $70 billion from a peak of roughly $76 billion. However, Son wasn't written off as a failure of that bubble era because he still held Alibaba. In the autumn of 2014, Alibaba listed on the NYSE. With the huge success of this single investment, Son's personal wealth exceeded $58 billion. That's equivalent to Warren Buffett's total investment gains over 70 years.

It was the most important and successful venture capital investment in the history of China's internet. This investment forged Alibaba and also made Masayoshi Son.

Around 2017, the Vision Fund was established with a size close to $100 billion. Son became the person tech startups worldwide most wanted to meet and the most powerful money bag in Silicon Valley.

Armed with funds from the Middle East, Apple, Qualcomm, and others, he traveled through Silicon Valley, China, India, and Southeast Asia, pouring money into ride-sharing, food delivery, fintech, autonomous driving, and co-working spaces. Those companies all talked about scale, network effects, winner-takes-all, and changing the world.

Son Felt He Was Getting Old

Son's fall from grace this time started with WeWork.

An ordinary failed investment at most hurts profits, but WeWork damaged the market's trust in Son's judgment and his acumen.

In early 2019, WeWork's valuation was still as high as $47 billion. Its founder, Adam Neumann, was charismatic and wildly ambitious. He never described his company as just an office rental business but as a lifestyle, a community, a future work order.

Son liked this kind of person because he was one himself. He spent his life searching for founders who framed business on a human scale.

But not everyone bought it.

In August 2019, WeWork filed its IPO prospectus. Details previously obscured in the private financing market by grand visions were now under the spotlight, laid bare before investors.

The company was burning massive cash, weighed down by heavy leases, plagued by governance chaos, and had a founder with excessive power. It claimed to be a tech company, but the more Wall Street looked, the more its core business appeared to be leasing office buildings and subdividing and subletting them. This business could hardly support a $47 billion valuation.

The market began to doubt Son's own abilities, forcing him to reflect on his investment style: Were those who could articulate grand visions more likely to get Son's money? Did he value founder charisma too much and financial discipline too lightly? Why was SoftBank willing to give such high valuations? Why believe a company that hadn't proven profitability could burn cash into a future? Could a founder who was good at saying 'change the world' make Son overlook due diligence, valuation, and business models?

Months later, WeWork withdrew its IPO. Adam Neumann resigned as CEO. The valuation plummeted from $47 billion to around $8 billion.

But by then, SoftBank and WeWork were in the same boat, unable to disembark. SoftBank had no choice but to bail it out.

Heaven abhors excess; human affairs avoid perfection. The company once lifted to the clouds by Son suddenly became the most glaring loss on SoftBank's books.

In November 2019, SoftBank posted its first quarterly loss in 14 years. The Vision Fund alone lost nearly $9 billion in a single quarter. Son admitted his misjudgment and that he had turned a blind eye to WeWork's governance issues. Because he wanted so desperately to find the next Alibaba, to replicate that victory of betting early when everyone else couldn't see.

In 2020, the wounds widened. The pandemic hit global markets. Uber underperformed its original myth. Oyo fell into layoffs and governance controversies. OneWeb filed for bankruptcy. Wirecard imploded, and later Greensill collapsed.

The money Son scattered had basically turned into shattered fragments.

Then, in 2021, fortune briefly glanced his way again. DoorDash, Coupang, and others went public. SoftBank's stock surged, and buybacks pushed the price higher. That year, Son returned to the top of Japan's wealth list. For a while, the outside world thought WeWork was just an ugly interlude, and the Vision Fund could eventually cover its losses with a few big wins. Son seemed about to prove once more that he wasn't wrong, just early to the market again.

But it was just a brief recovery. Starting in the second half of 2021, the winds changed. China tightened internet regulations, US inflation heated up, interest rates rose, and global tech stocks receded. The market was no longer willing to pay infinite money for 'will be big in the future.' Companies reliant on financing, scale, and imagination to support their valuations suddenly had to answer the same old question: When exactly will you make money?

Heaven and Earth have cycles; life has its ups and downs. Observing the way of Heaven and acting accordingly—that is all.

In 2022, Son truly fell into the biggest trough of his life.

The SoftBank Vision Fund lost about $27.5 billion in the 2021 fiscal year. In August 2022, SoftBank announced a net loss of about $23.4 billion for a single quarter.

He said he cried for two whole weeks. "For two weeks, I cried every day. I did nothing. I was anxious, didn't know what to do."

Recalling that period later, Son left a sincere monologue: "I thought about how I am already old, my remaining life is limited, but I haven't achieved anything. I cried a lot. I asked myself, am I really going to grow old like this and then die? People call me a successful businessman? Entrepreneur? Business guru? But I really felt sorry for myself."

SoftBank also began to shrink. New investments slowed dramatically. The Vision Fund team faced layoffs. Assets were continuously monetized. Alibaba, the功臣 that once helped Son turn his fortunes, was also gradually sold off by SoftBank to improve its financial structure. Son's business empire was under siege from all sides, and his father was taken by cancer.

In recent years, the companies that excited Son became strings of write-downs and losses. He said, "I would rather accept my own stupidity and ignorance, accept the wrong decisions I made, so I can learn from them." He admitted that he was too happy when he saw huge profits in the past and now felt ashamed. He also said that if he had been more selective and invested better at the time, the damage wouldn't have been so great.

Many said that Son during those years was not like the Son they knew. He grew quiet and rarely reappeared in the public eye.

He said SoftBank would enter "defense mode," and he would focus on Arm in the coming years.

Looking back today, this was another great investment by Son.

AI Has Forgiven Son

But initially, Arm didn't seem like a destined success; the deal put Son under immense pressure.

In the summer of 2016, SoftBank spent a whopping $32 billion in cash to acquire a 90% stake in Arm, a 40% premium.

Arm was, of course, a good company then. But most of the funds for the acquisition came from bank loans—leverage of 1.5 times raised by an already debt-laden SoftBank. Many investors doubted if Arm was really worth it. Even after being taken private by SoftBank, Arm's increased investments led to falling profit margins and severe performance declines at one point. SoftBank nearly sold Arm to Nvidia.

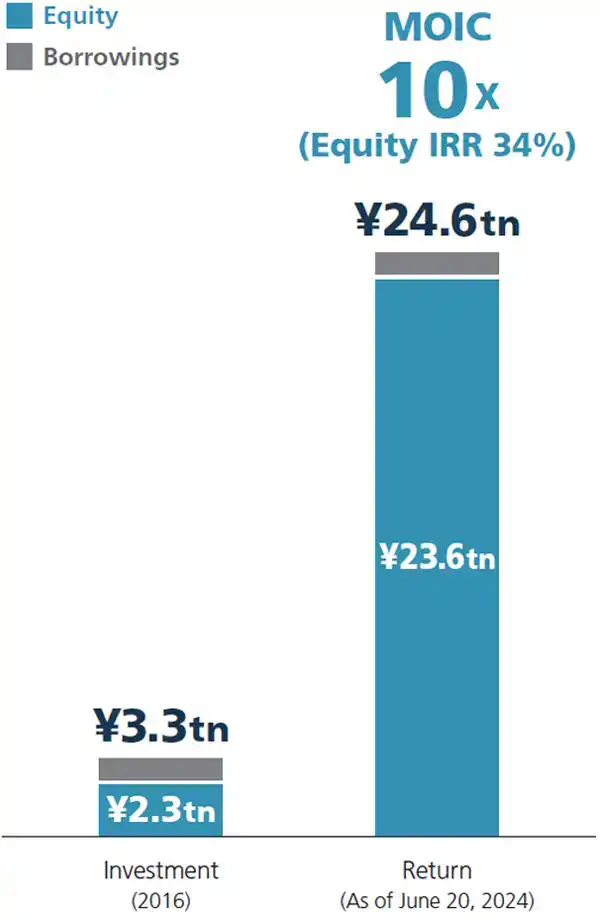

It wasn't until after ChatGPT that the market re-understood computing power. The vast rivers of artificial intelligence made Arm shine brightly. In September 2023, Arm listed on Nasdaq with an IPO valuation of about $54.5 billion. From about 14 trillion yen at the end of March 2023, SoftBank's NAV rose to about 34 trillion yen in June 2024. Arm now constitutes the bulk of SoftBank's shareholding value. SoftBank stated in its annual report that Arm has delivered returns of 24.6 trillion yen to group shareholders, roughly a 10x return.

If Arm gave Son a pull out of the mud, then OpenAI might be his comeback battle.

In January 2025, OpenAI, SoftBank, Oracle, and MGX announced the Stargate project, planning to build large-scale AI infrastructure in the US, with potential investments up to $500 billion over the next four years.

Subsequently, SoftBank's investments in OpenAI became very aggressive.

In 2025, SoftBank completed an investment of about $30 billion in OpenAI. By February 2026, SoftBank signed an additional $30 billion investment agreement with OpenAI. According to SoftBank's announcement, upon completion of the top-up, SoftBank's cumulative investment in OpenAI is expected to reach $64.6 billion for an approximately 13% stake. In April 2026, SoftBank executed the first tranche of this additional investment, amounting to $10 billion.

In March 2026, SoftBank secured a $40 billion bridge loan, primarily for the subsequent OpenAI investment. It is also selling or monetizing other assets, using Arm shares, SoftBank telecom assets, etc., as financing leverage.

This investment is classic Son. Once again, he is putting SoftBank's most valuable assets on the line to buy a ticket to the next round of the future.

In the internet era, he bet himself on Yahoo and Alibaba; in the mobile internet era, he heavily invested in telecoms, Sprint, Arm; in the Vision Fund era, he scattered money to startups telling huge stories. And in the AI era, he is pushing SoftBank towards OpenAI and AI infrastructure.

At the end of March this year, SoftBank disclosed its OpenAI investment cost at about $34.6 billion, with a fair value of about $79.6 billion, resulting in cumulative investment gains of about $45 billion.

Recently, SoftBank's stock soared, its market cap once surpassing Toyota, making it one of Japan's most sought-after companies. Son also reclaimed his title as Asia's richest person.

Fortune is once again on Son's side.