Author: 100y

Translation: Chopper, Foresight News

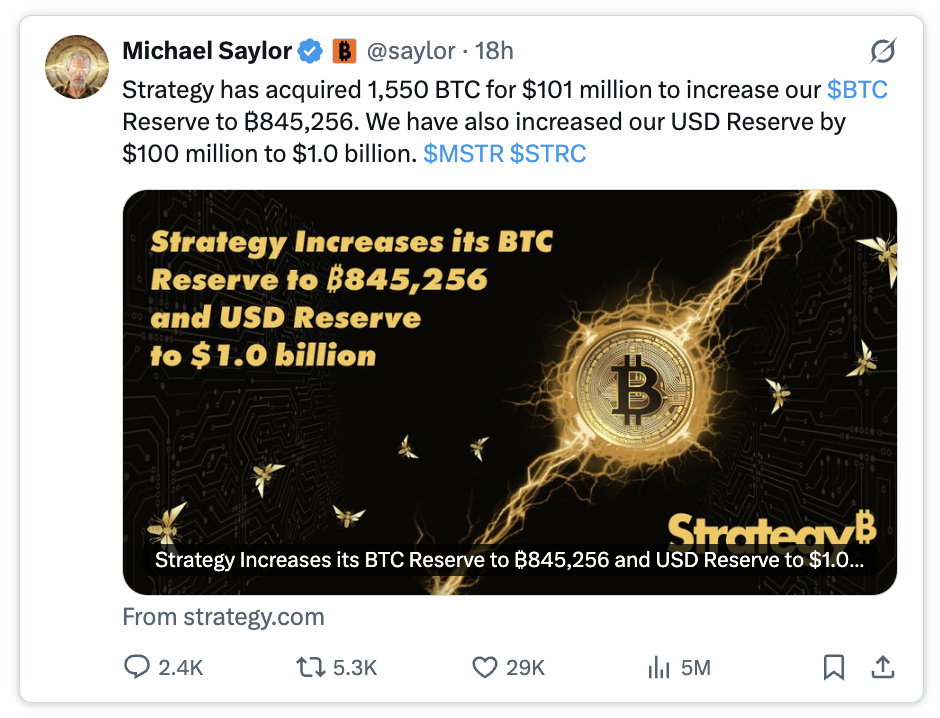

Bitcoin treasury company Strategy first sold 32 bitcoins, and then immediately made a large purchase of 1550 bitcoins.

I do not wish for Strategy (MSTR) to decline, but some truths must be spoken. In my opinion, this is an extremely bad trade.

On the surface, this move appears brilliant. Strategy accumulated a significant number of bitcoins at relatively low prices, while also increasing its dollar reserves for paying preferred dividends from $900 million to $1 billion.

Does this mean Strategy is about to stage a reversal?

If you only see positives in this, it means you haven't truly understood the operational logic of this company.

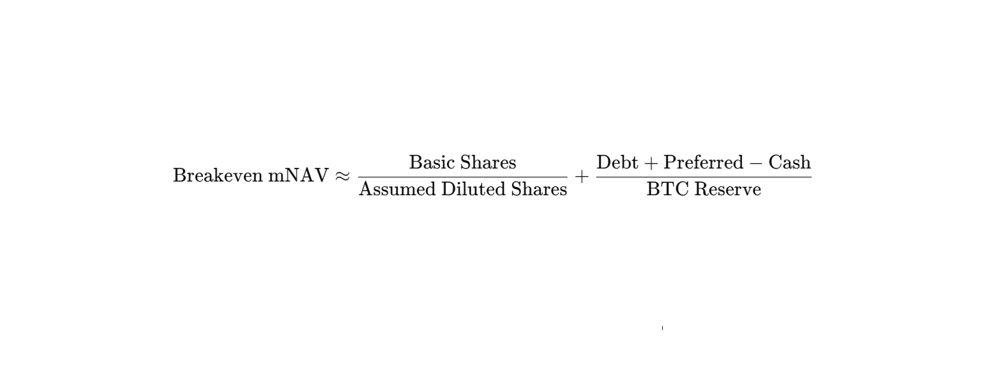

First, Understand the Breakeven Adjusted Net Asset Value (mNAV)

Increasing the number of bitcoins per share (BPS) is a core goal for Strategy to create value for MSTR shareholders.

The logic to increase bitcoins per share is actually very clear: issue common stock at a premium above the market price, and use all the raised funds to buy bitcoin.

So, how high a premium does MSTR need to reach in order to genuinely increase the bitcoins per share through timely stock offerings?

According to information disclosed in the Q1 2026 earnings conference call, the adjusted net asset value (mNAV) must exceed 1.22, a figure also known as the breakeven adjusted net asset value in the industry.

The underlying logic of this standard is simple: the amount of bitcoin that can be purchased with the funds raised from selling 1 share of MSTR stock must be higher than the current bitcoin holdings corresponding to that single share. For the complete derivation process, you can refer to my previous publication. (https://research.4pillars.io/en/research/strategys-magic-number-122)

Ultimately, the calculation method for the breakeven mNAV is as follows:

Let me add here that the breakeven adjusted net asset value is no longer 1.22. Before the execution of this purchase of 1550 bitcoins, calculations showed this value had already risen to 1.30.

Why This is a Bad Trade

Let's look back at this acquisition of 1550 bitcoins.

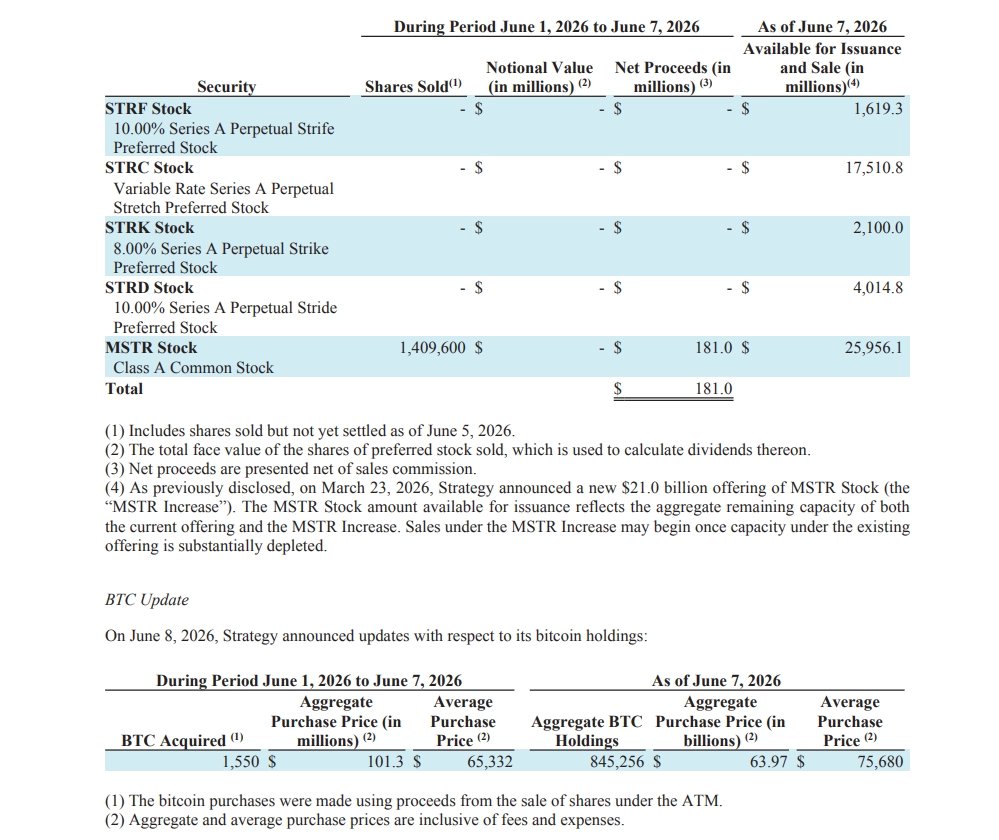

Strategy raised a total of $181 million through MSTR's at-the-market (ATM) offering program, then used $101.3 million of it to purchase 1550 bitcoins. This operation has two core issues:

First, at the time of this MSTR stock ATM offering, the corresponding adjusted net asset value (mNAV) was below the 1.30 breakeven point. If stock is issued when mNAV is below the breakeven level and the raised funds are used to buy bitcoin, it not only fails to increase the bitcoins per share but actually causes this metric to decline.

Second, and more critically, the funds raised from this offering were not used 100% to purchase bitcoin. The calculation logic for the breakeven adjusted net asset value is based on the premise that all raised funds are used to buy bitcoin. Even if mNAV is at a high level, as long as only a portion of the funds are directed towards bitcoin, it will ultimately lower the bitcoins per share.

Reportedly, the remaining funds from this offering that were not used for buying bitcoin were allocated to the company's dollar reserves.

In other words, Strategy sacrificed the equity value and bitcoins per share of MSTR shareholders to ensure the normal operation of its STRC-related business.

Calculations show that after completing this transaction, the company's bitcoins per share decreased by approximately 0.19% compared to before. And what was gained in return? The runway for the company's dollar reserves to sustain operations only extended from about 6.3 months to 7 months.

A Big Gamble by Strategy

Michael Saylor stated in the Q1 2026 earnings conference call: "Our core goal is to increase the bitcoins per share, and we will use every means possible to achieve this goal."

However, as seen from this trade, for the development of STRC, Strategy chose to sacrifice MSTR's core metric of bitcoins per share. This is nothing short of a gamble.

If sacrificing MSTR leads to improved market sentiment, stabilization and recovery of STRC's price, and pushes the adjusted net asset value back to a reasonable range, then the company can continue to rely on the ATM offering channels of MSTR and STRC to raise funds, allowing the entire system to operate healthily.

But if market sentiment does not improve, the situation will deteriorate rapidly. Strategy would then likely be forced to continue sacrificing MSTR's interests to stay afloat.

The worst-case scenarios would follow one after another: the company might be forced to delay STRC dividend payments, or gradually decline amidst ongoing internal consumption.

Finally, I hope the prices of Bitcoin, MSTR, and STRC all recover.