上周五低于预期的非农就业数据以及前值下修再次引发了人们对经济衰退的担忧,导致美股创下 2023 年 3 月以来最差的单周表现,消极的风险情绪也拖累了数字货币的表现,再度印证了来自季节性统计数据的诅咒。与此同时,美债出现牛陡走势, 2/10 s 收益率终于结束了倒挂形态。

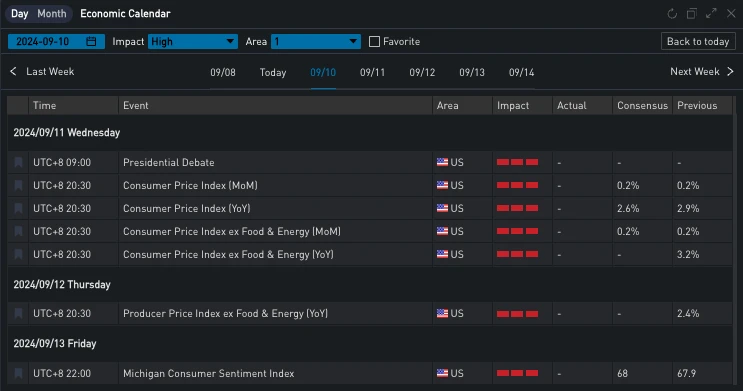

Source: SignalPlus, Economic Calendar

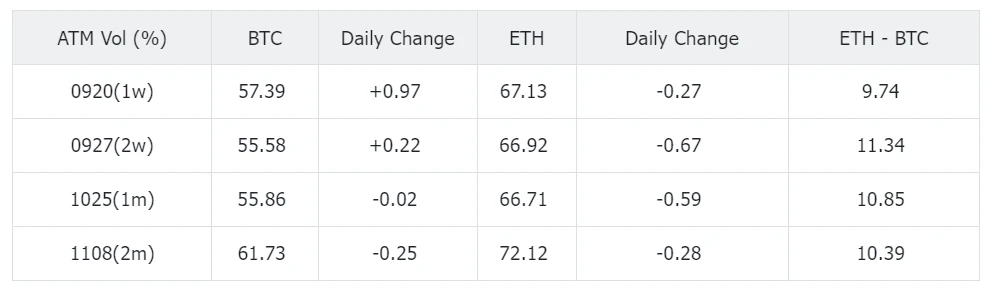

本周加密社区的关注点依然围绕宏观事件,在平静的周末结束后,期权做市商已经悄然拉高了前端的 IV,尽管 Term Structure 上 BTC 和 ETH 十分相似,但细节上略有不同。首先注意到 BTC 前端的峰值在 11 SEP 而 ETH 则是在 12 SEP,两个到期日 Price-In 了非常高的 Vol Premium。

12 SEP 的不确定主要来自 CPI 数据,尽管通胀数据的影响力已经退居就业数据之后,但本周再次成为了金融交易员心中的头等大事,并会许会成为决定美联储是否会在 9 月下旬的 FOMC 上大幅降息 50 个基点的决定性因素。

对购买 11 SEP 的交易员来说,他们主要看中的还是北京时间上午 9 点举行的总统竞选演讲。这场对抗是特朗普和哈里斯第一次,或许也是唯一一次正面交锋的机会,距离正式的选举日已经不到两个月,这迫使他们抓住每个机会来说服选民。有关数字货币的话题势必也会在双方的对话中出现,市场赋予了 BTC 更高的相关性,这也在期限结构上得到了体现。

Source: SignalPlus

期限结构的中段形成了以 25 OCT 为最低点的谷底,不确定性被分配到了 FOMC 会议之前和总统大选的日子上。两币种在 Forward IV 的结构上略有差别,ETH 12 SEP-13 SEP 的这段低点有机会被调平修正,月末 ETH 平坦的斜率以及高出 BTC 10% 的 Vol Premium 或许也能吸引到跨币种的波动率交易。

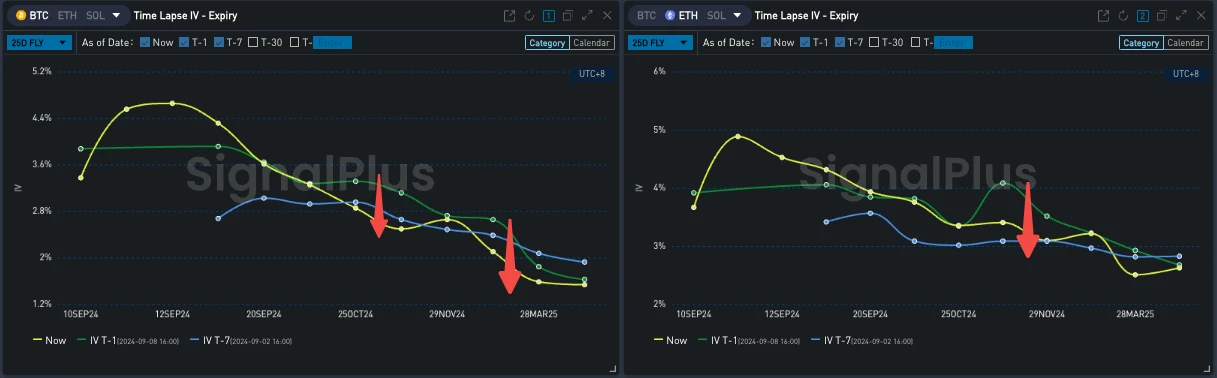

从波动率微笑的曲率上看,远端的 Fly 在经历了短暂的上升后得到重新回调,接近一周前的水平。

Source: Deribit (截至 9 SEP 16: 00 UTC+ 8)

Source: SignalPlus

您可在 t.signalplus.com 使用 SignalPlus 交易风向标功能,获取更多实时加密资讯。如果想即时收到我们的更新,欢迎关注我们的推特账号@SignalPlusCN,或者加入我们的微信群(添加小助手微信:SignalPlus 123)、Telegram 群以及 Discord 社群,和更多朋友一起交流互动。

SignalPlus Official Website:https://www.signalplus.com