Today, crypto trader Jez announced his new protocol, PaperTrade, developed on HyperEVM, sparking heated discussions in the English-speaking crypto community.

Jez is a long-term evangelist for perpetual contracts. He heavily invested in Hyperliquid early on, with his account address ranking high on the airdrop leaderboards of Lighter and Variational. This time, he has taken matters into his own hands, creating a Perp DEX with no fees, no slippage, and no funding rate.

Old-School Gambling House Exiles to the Chain

The mechanism of PaperTrade has a notorious predecessor in financial history: the bucket shops in American small towns in the 1900s. These establishments, operating under the guise of securities firms, would chalk up real-time quotes from the New York Stock Exchange behind their counters, but clients' orders never left the shop owner's drawer. Essentially, it was a gamble between the client and the shop owner. This business was outlawed by New York State legislation in 1909 and largely disappeared by the 1920s.

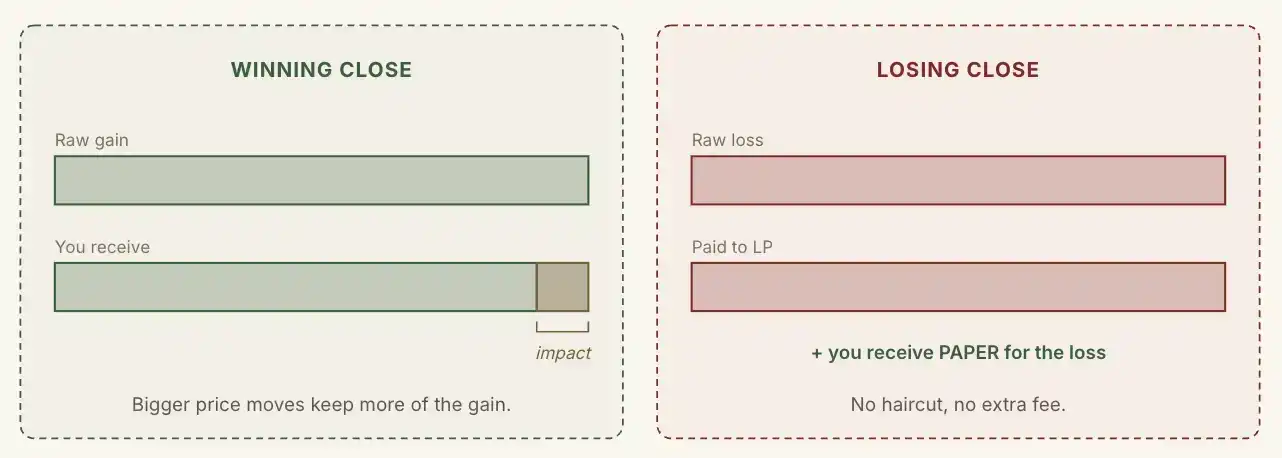

When users open or close a position on PaperTrade, the platform directly reads the order book price from Hyperliquid and settles directly with the public LP pool based on the difference between the opening and closing prices. No orders enter Hyperliquid's matching system during this entire process, and no real perpetual contracts are exchanged. The trading parties are always the user and the LP pool, with no third-party counterparty.

Perpetual Contracts + P2P + DeFi Ponzi

PaperTrade simultaneously borrows models from DeFi mining and P2P lending.

User losses on PaperTrade are placed directly into the protocol's LP pool, while user profits are taxed by the platform. The smaller the price fluctuation, the more profit is taken. In other words, the more users earn, the less the protocol taxes.

Unlike HLP, PaperTrade's LP pool has no team pre-deposit, no VC investment, and does not accept any form of external deposits whatsoever. Its sole source of funds is user-lost margin.

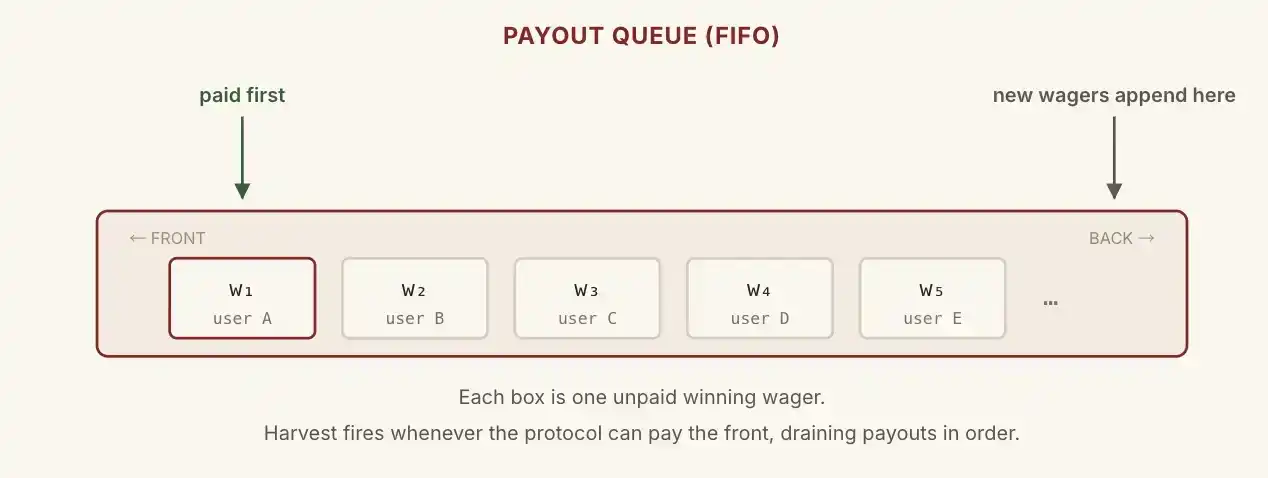

The question arises: if the LP pool only has $100, but a user makes $5,000, how does the protocol pay?

PaperTrade has brought the creditor queue from traditional P2P lending onto the chain.

This $5,000 enters a sequential on-chain queue, waiting for the next losing trade to come in and fill the gap, with payments made in order from the front of the queue. User principal is always returned immediately, only the profit portion is queued.

In theory, the LP can be "bankrupt" in stages, but every winner will eventually be paid in full, unless the losses from losers are insufficient to cover the profits the platform owes the winners.

If the story ended here, this project would be doomed to failure. Because if the LP pool runs out of money, it means winners might have to wait a long time in the queue to receive their profits, naturally losing motivation to trade. As traders leave, even losers disappear, and the money the platform owes winners becomes bad debt.

The essence of PaperTrade lies in its token, PAPER.

For every dollar a user loses, the protocol mints a certain amount of PAPER according to a curve.

When the LP balance is below $2 million, the minting ratio is fixed at 100 PAPER per $1 loss; after the LP exceeds $2 million, the rate begins to decay—the higher the LP balance, the less PAPER is minted.

X-axis: Amount of PAPER obtained per unit of loss; Y-axis: LP Balance (each grid represents 1M)

Staking PAPER yields two parts of dividends: first, the protocol's fee income; second, when the balance exceeds $5 million, all excess funds are allocated entirely to stakers.

In other words, the LP pool's scale is designed with a $5 million ceiling. Beyond this size, user losses are fully returned to PAPER holders. This forms a closed loop: "Losers get platform shares, winners take losers' money, the platform taxes winners to subsidize losers."

Therefore, a reasonable participation strategy can be summarized as: betting to lose money to mint PAPER when the LP pool's TVL is low, and staking PAPER to collect dividends when the LP pool's TVL is high.

A Stress Test for HyperEVM

In my opinion, the biggest uncertainty for PaperTrade lies in the HyperEVM on which it is deployed.

PaperTrade merely uses Hyperliquid's quotes as a free, native oracle, with all remaining logic residing in the contracts on HyperEVM.

This means any high-performance chain with similar capabilities could replicate PaperTrade's entire mechanism on its own chain, as long as it is willing to integrate an external price oracle. The replicator could even offer things HyperEVM cannot: lower gas fees, higher TPS, more generous early subsidies, more aggressive token incentives.

During the HyperEVM meme season in Q1 of last year, there was a period of slow on-chain speeds and high gas fees. The launch of PaperTrade is another test for HyperEVM.