Stablecoins anchored market liquidity, with total supply near $315.85 billion and USD Coin [USDC] accounting for about $78.7 billion.

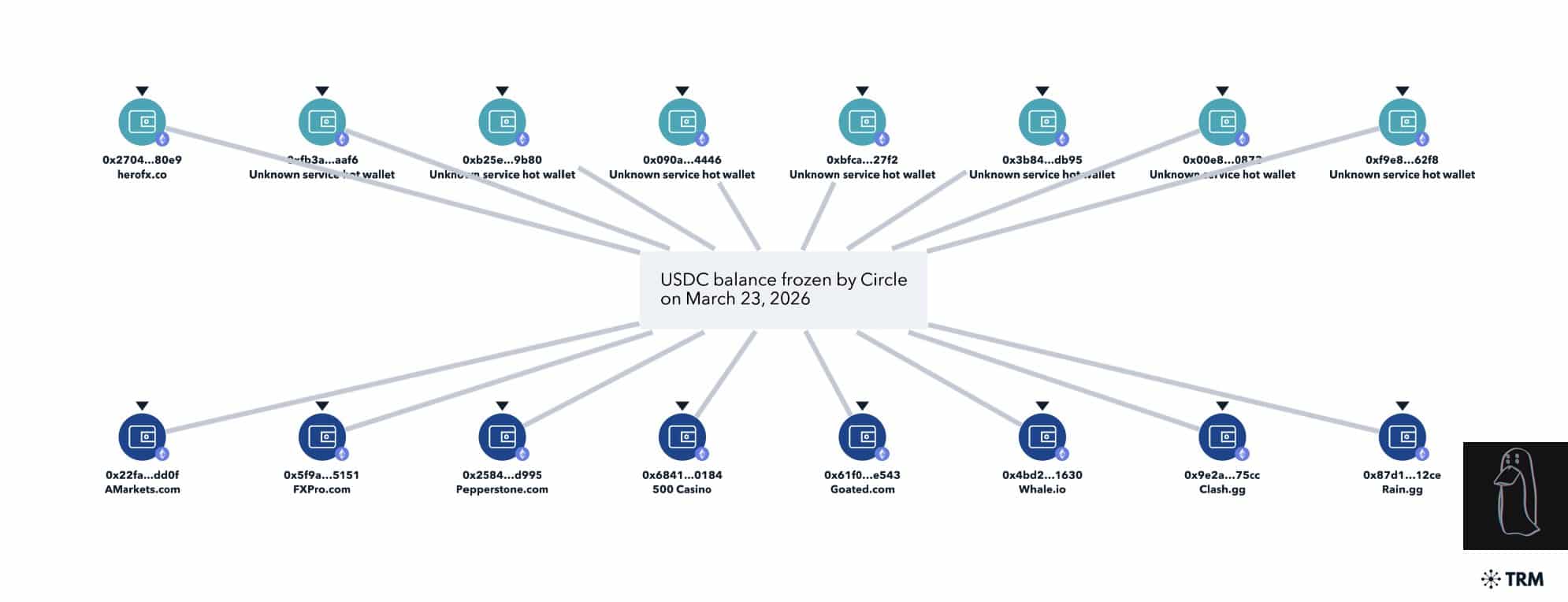

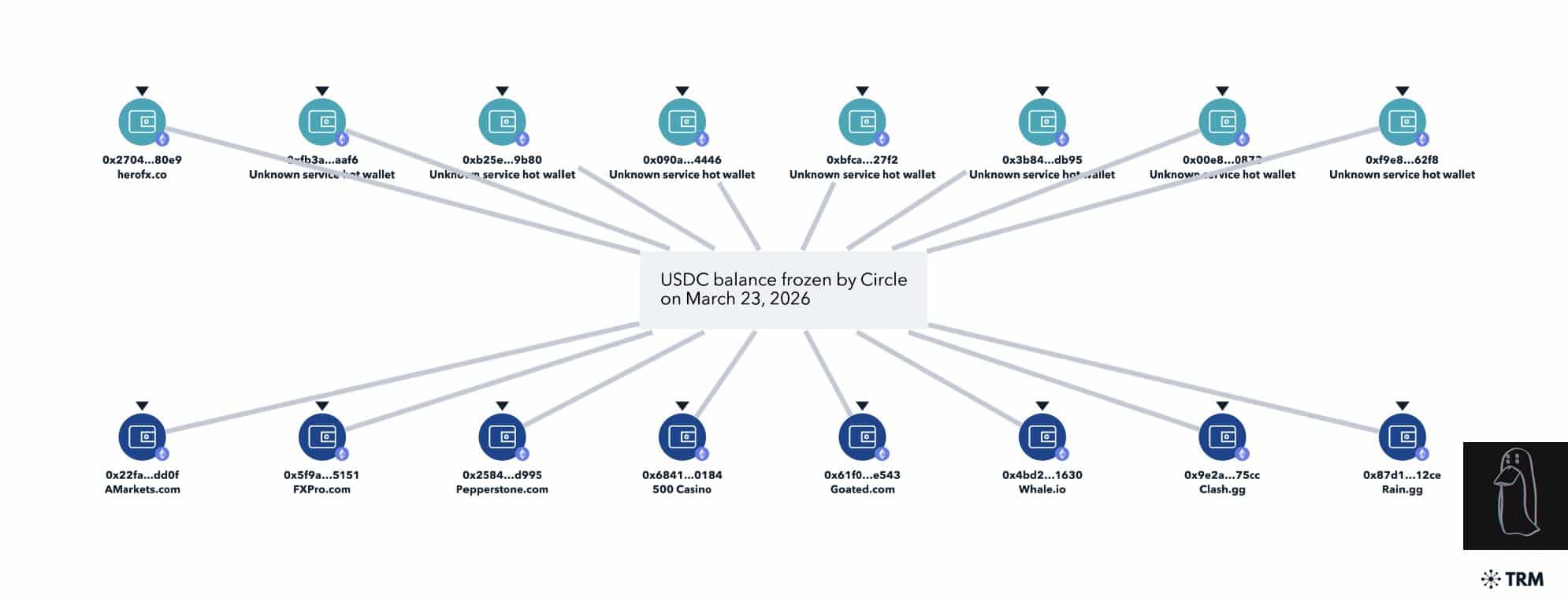

USDC wallet freezes drew scrutiny after on-chain investigator ZachXBT flagged multiple exchange-linked wallets affected on the 23rd of March 2026.

However, recent USDC wallet freezes disrupted that expectation, as compliance actions extended beyond intended targets. Reports suggested at least 16 unrelated hot wallets were frozen, disrupting transactions across bridging and settlement flows.

That shift set up a broader concern. Focus moved from isolated enforcement to systemic reliability risks.

This raised a key question: Why were operational exchange wallets affected?

USDC wallet freezes spill into exchange and bridge flows

ZachXBT noted that several frozen wallets showed normal operational activity, raising concerns around targeting accuracy.

Reports suggested that exchange-linked hot wallets were flagged alongside intended addresses, extending the impact beyond enforcement targets.

Circle later reversed some freezes, including the Goated wallet, indicating a correction rather than a final decision.

That sequence showed how compliance actions can misfire when applied across interconnected wallet systems.

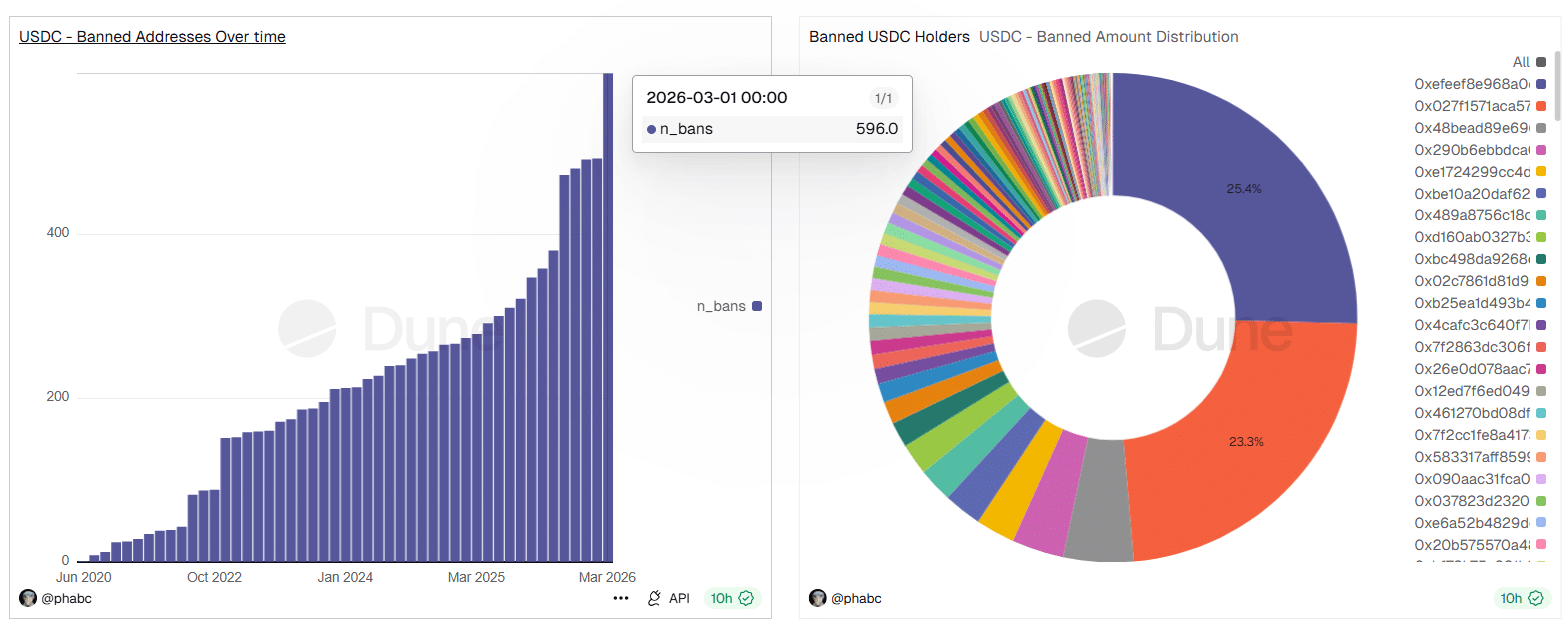

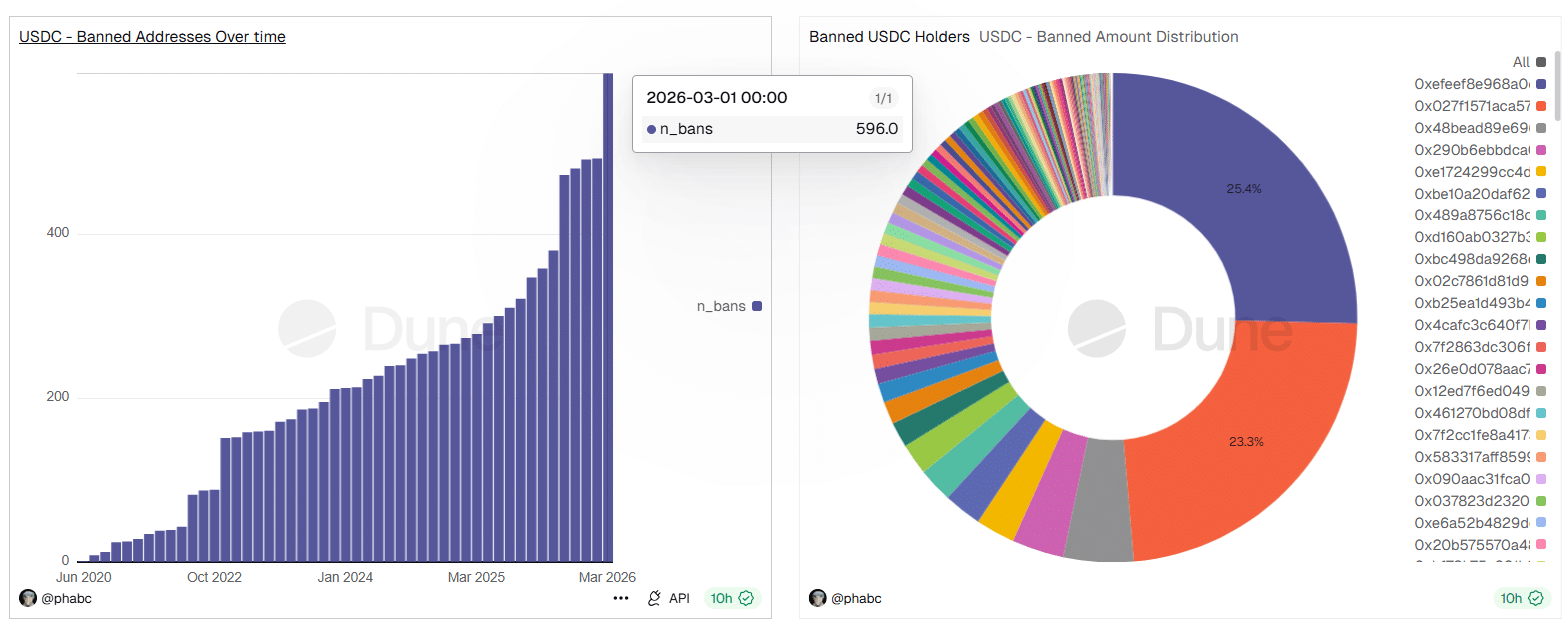

USDC blacklist count hits 596 as compliance tightens

USDC’s control structure became clearer as enforcement activity increased across the network. Blacklisted addresses reached 596, reflecting steady growth rather than isolated actions.

That move aligned with deeper regulatory integration into stablecoin infrastructure, rising from near zero levels in 2020.

On top of that, distribution data showed concentration among a few large holders. This amplified the impact of each freeze.

When key wallets were affected, liquidity disruptions extended beyond individual users into broader market flows. That explained settlement failures across exchanges and bridges.

This left traders focused on a structural shift. USDC operated less like neutral infrastructure and more like a controlled settlement layer.

USDC outflows drive liquidity shift toward USDT dominance

The market reaction showed a subtle shift beneath stable price action. USDC held near $78.7 billion, yet declined 0.90% weekly, signaling selective capital movement.

At the same time, total stablecoin supply rose 0.04%, showing funds rotated rather than exited.

By contrast, Tether [USDT] expanded its lead to 58.29% dominance at $184.1 billion, absorbing redirected liquidity.

That move reflected a search for perceived stability rather than a rejection of stablecoins entirely.

Confidence remained, yet behavior shifted. Partial reversals exposed operational strain, while unintended freezes raised concerns around exposure.

This implied trust weakened at the margins, which could fragment liquidity and reshape capital allocation across stablecoin ecosystems.

Final Summary

- USD Coin [USDC] freezes expose centralized control risks, with rising blacklists and failed settlements weakening neutrality and shaping liquidity flows.

- Tether [USDT] absorbs rotation with 58% dominance, signaling trust shifts rather than exits, as stablecoin liquidity fragments across ecosystems.