Author: Silvio

Compiled by: Saoirse, Foresight News

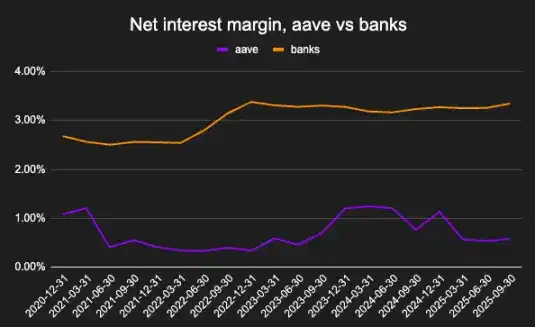

A $1 deposit in a bank generates 10 times more profit for the bank than the same amount of USDC on Aave. This phenomenon may seem unfavorable for the DeFi lending sector, but in reality, it reflects the structural characteristics of the current cryptocurrency market more than the long-term potential of on-chain credit.

Net interest margin is an indicator of deposit profitability. Banks under FIDC, Aave under Blockworks.

This article will explore the following issues: the actual usage patterns of current lending protocols, the structural reasons for their lower profit margins compared to banks, and how this situation might change as lending activities gradually decouple from crypto-native leverage cycles.

The Role of On-Chain Credit

My first job involved analyzing bank books and assessing borrower qualifications. Banks channel credit funds to real businesses, and their profit margins are directly linked to the macroeconomy. Similarly, analyzing the borrowers of decentralized finance protocols helps in understanding the role credit plays in the on-chain economy.

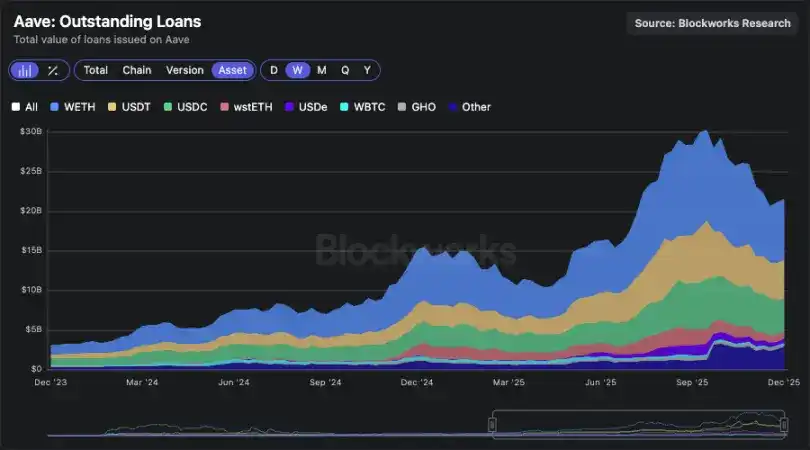

Chart of Aave's outstanding loan data

Aave's outstanding loan amount has exceeded $20 billion, an impressive achievement — but why do people borrow on-chain?

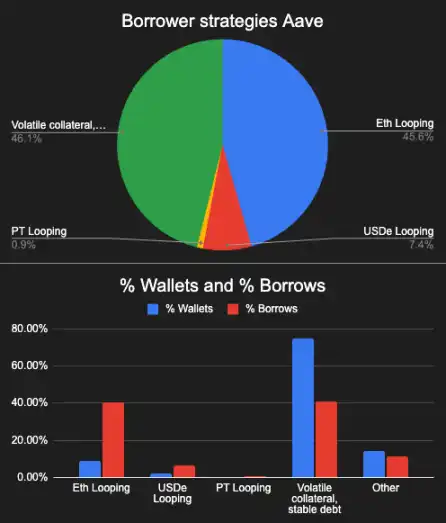

Actual Uses of Aave Borrowers

Borrower strategies can be categorized into four types:

1. Borrowing WETH using interest-bearing ETH as collateral: The yield from staking ETH is typically higher than that of WETH, creating a structural basis trade (essentially "borrowing WETH while earning yield"). Currently, this type of trade accounts for 45% of the total outstanding loans, with most of the funds coming from a few "whales." These wallet accounts are often related to staked ETH issuers (such as the EtherFi platform) and other "recursive stakers." The risk of this strategy is that the WETH borrowing cost may spike, which could quickly cause the collateral health factor to fall below the liquidation threshold.

Presumed WETH borrowing rate chart: If the rate remains below 2.5%, the basis trade is profitable.

2. Stablecoin and PT recursive stakers: A similar basis trade can be formed with interest-bearing assets (such as USDe), where the yield may be higher than the borrowing cost of USDC. Before October 11, this strategy was very popular. Although structurally attractive, this strategy is highly sensitive to changes in funding rates and protocol incentive policies — which explains why the scale of such trades shrinks rapidly when market conditions change.

3. Volatile collateral + stablecoin debt: This is the most popular strategy among users, suitable for two types of demand: one is to increase exposure to cryptocurrencies through leverage, and the other is to reinvest borrowed stablecoins into high-yield "liquidity mining" for basis trading. This strategy is directly related to mining yield opportunities and is also the main source of stablecoin borrowing demand.

4. Other remaining types: Including "stable collateral + volatile debt" (for shorting assets) and "volatile collateral + volatile debt" (for currency pair trading).

1) Weight distribution of Aave wallet borrowing strategies; 2) Distribution of wallets corresponding to each strategy

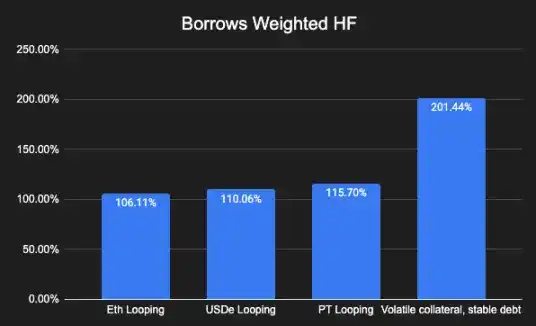

Chart of collateral health factor weighted by borrowing amount

For each of these strategies, there is a value chain composed of multiple protocols: these protocols integrate the trading process using Aave and distribute yields to retail users. Today, this integration capability is the core competitive barrier in the cryptocurrency lending market.

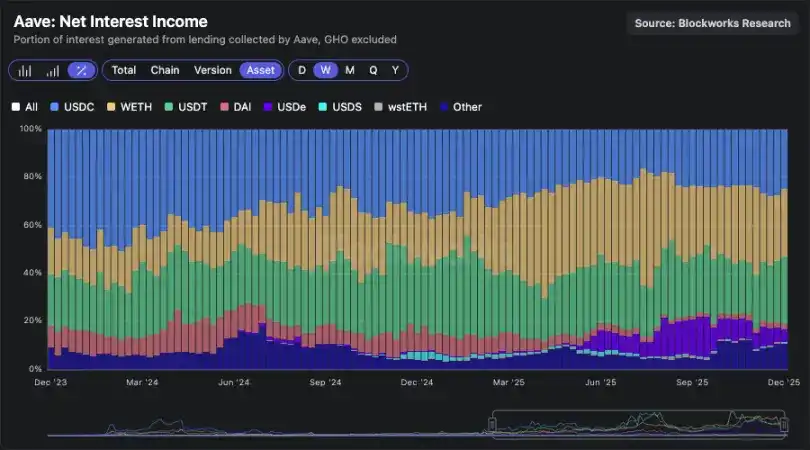

Among these, the "volatile collateral + stablecoin debt" strategy contributes the most to interest income (borrowing revenue from USDC and USDT accounts for over 50% of total revenue).

Chart of interest income share by asset type

Although some businesses or individuals do use cryptocurrency loans to finance operational activities or real-life expenses, the scale of such practical uses is very limited compared to the purpose of "leveraging on-chain leverage/yield differential arbitrage."

Three core factors driving the growth of lending protocols:

- On-chain yield opportunities: Such as new project launches, liquidity mining (e.g., Plasma platform mining activities);

- Structural basis trades with deep liquidity: Such as ETH/wstETH trading pairs and stablecoin-related trades;

- Partnerships with major issuers: These partnerships can help open up new markets (e.g., the combination of pyUSD stablecoin and RWA).

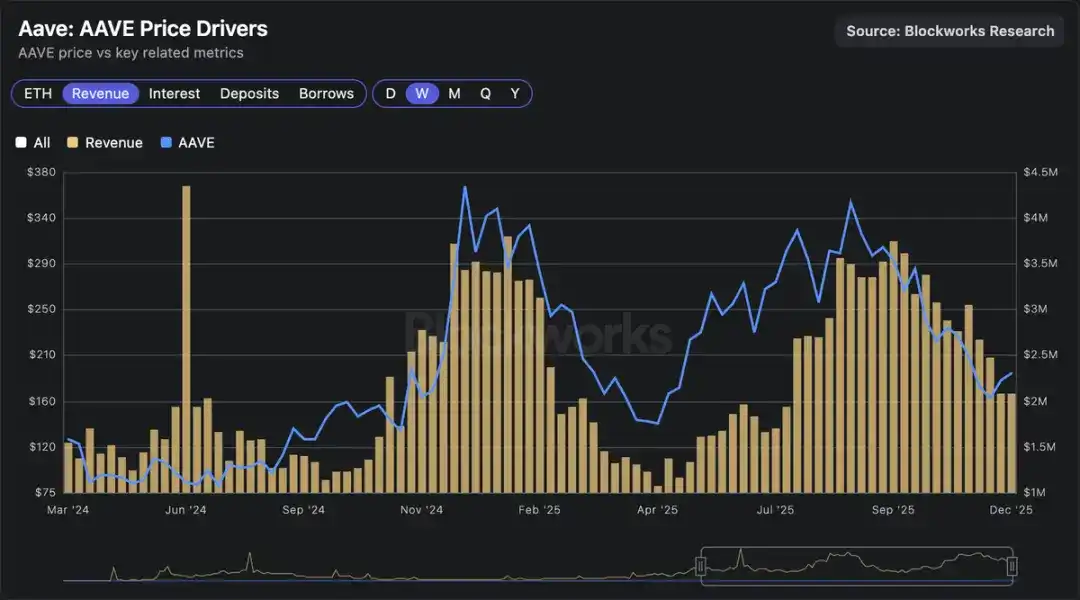

The lending market is mechanistically directly linked to "crypto GDP" (exhibiting Beta correlation), just as banks are essentially barometers of "real-world GDP." When cryptocurrency prices rise, yield opportunities increase, the scale of interest-bearing stablecoins expands, and issuers adopt more aggressive strategies — ultimately driving lending protocol revenue growth, increased token buybacks, and pushing up the price of Aave tokens.

Chart of correlation between lending market valuation and revenue: Lending market valuation is directly correlated with revenue.

Comparison Between Banks and On-Chain Lending Markets

As mentioned earlier, $1 in a bank is 10 times more efficient in generating profit than $1 of USDC on Aave. Some see this as a bearish signal for on-chain lending, but in my view, this is essentially an inevitable result of market structure, for three reasons:

- Higher financing costs in the crypto space: Banks' financing costs are benchmarked against the Federal Reserve's base rate (lower than Treasury yields), while the deposit rate for USDC on Aave is typically slightly higher than Treasury yields;

- Traditional commercial banks engage in more complex risk transformation activities and deserve higher premiums: Large banks manage billions of dollars in unsecured loans to businesses (e.g., financing data center construction). This risk management is far more difficult than "managing the collateral value of ETH recursive staking" and therefore deserves higher returns;

- Regulatory environment and market dominance: The banking industry is an oligopoly, with high user switching costs and industry entry barriers.

Decoupling Lending from Cryptocurrency's "Cycle Binding"

Those successful cryptocurrency sectors are gradually decoupling from the boom-bust cycles of the crypto market itself. For example, the open interest of prediction markets continues to grow even amid price fluctuations; the same is true for stablecoin supply, whose volatility is much lower than other assets in the crypto market.

To move closer to the operational model of the broader credit market, lending protocols are gradually incorporating new risk types and collateral, such as:

- Tokenized RWA and stocks;

- On-chain credit originating from off-chain institutions;

- Using stocks or real-world assets as collateral;

- Structured underwriting through crypto-native credit scoring.

Asset tokenization creates the conditions for lending businesses to become the "natural endpoint" in the crypto space. When credit activities decouple from price cycles, their profit margins and valuations will also break free from cyclical constraints. I expect this transformation to begin manifesting in 2026.