Michael Saylor: 110 Reasons to Oppose BIP-110

Michael Saylor presents 110 arguments against Bitcoin Improvement Proposal (BIP) 110, a soft fork aimed at restricting certain non-monetary data storage uses (like inscriptions) on the Bitcoin blockchain.

He acknowledges the proponents' valid concerns—such as node costs, fee pressure, and preserving Bitcoin's monetary focus—but fundamentally disagrees with the proposed solution. Saylor argues that BIP 110 represents a dangerous precedent of using consensus rules to enforce value judgments on transaction validity, moving away from Bitcoin's core principles of neutrality and permissionless innovation.

His key objections are organized into eleven categories: 1) It violates neutrality and hard consensus by banning currently valid transactions. 2) It fails to meet the high burden of proof required for a consensus change, lacking concrete data on the alleged crisis. 3) Its seven bundled technical restrictions are overly broad, targeting generic script functionalities and blocking future upgrade paths. 4) It sacrifices compatibility and future optionality by closing off designed upgrade hooks. 5) Its temporary rules add significant complexity (grandfathering, expiry states) without sufficient justification. 6) The economic and security impacts, particularly on miner revenue and fee markets, are uncertain and unmodeled. 7) Superior, market-based tools (fee markets, relay/mining policies) already exist to manage blockchain load. 8) It stifles innovation by creating a chilling effect for developers. 9) Its modified activation mechanism (55% threshold, forced signaling) is aggressive and risks network splits. 10) The precedent it sets—using consensus to suppress disliked but legal uses—is more dangerous than the problem it aims to solve. 11) A better path exists: improving measurements, refining resource-based policies, and allowing market forces to work.

Saylor concludes that Bitcoin's strength lies in its neutral rules, open markets, and hard consensus. Changing these foundational elements to target specific use cases is an unnecessary and risky "iatrogenic" intervention. He advocates for guarding Bitcoin's neutrality rather than acting as its redeemer.

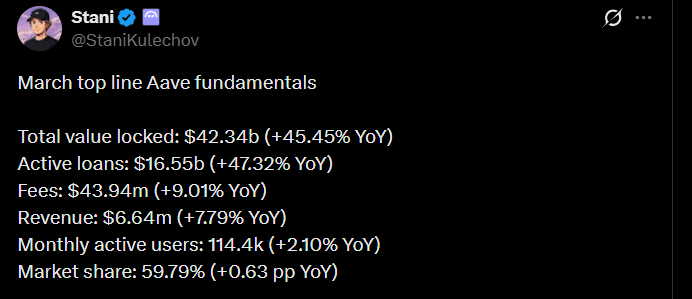

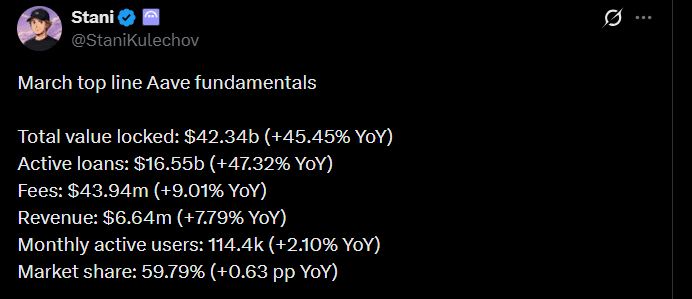

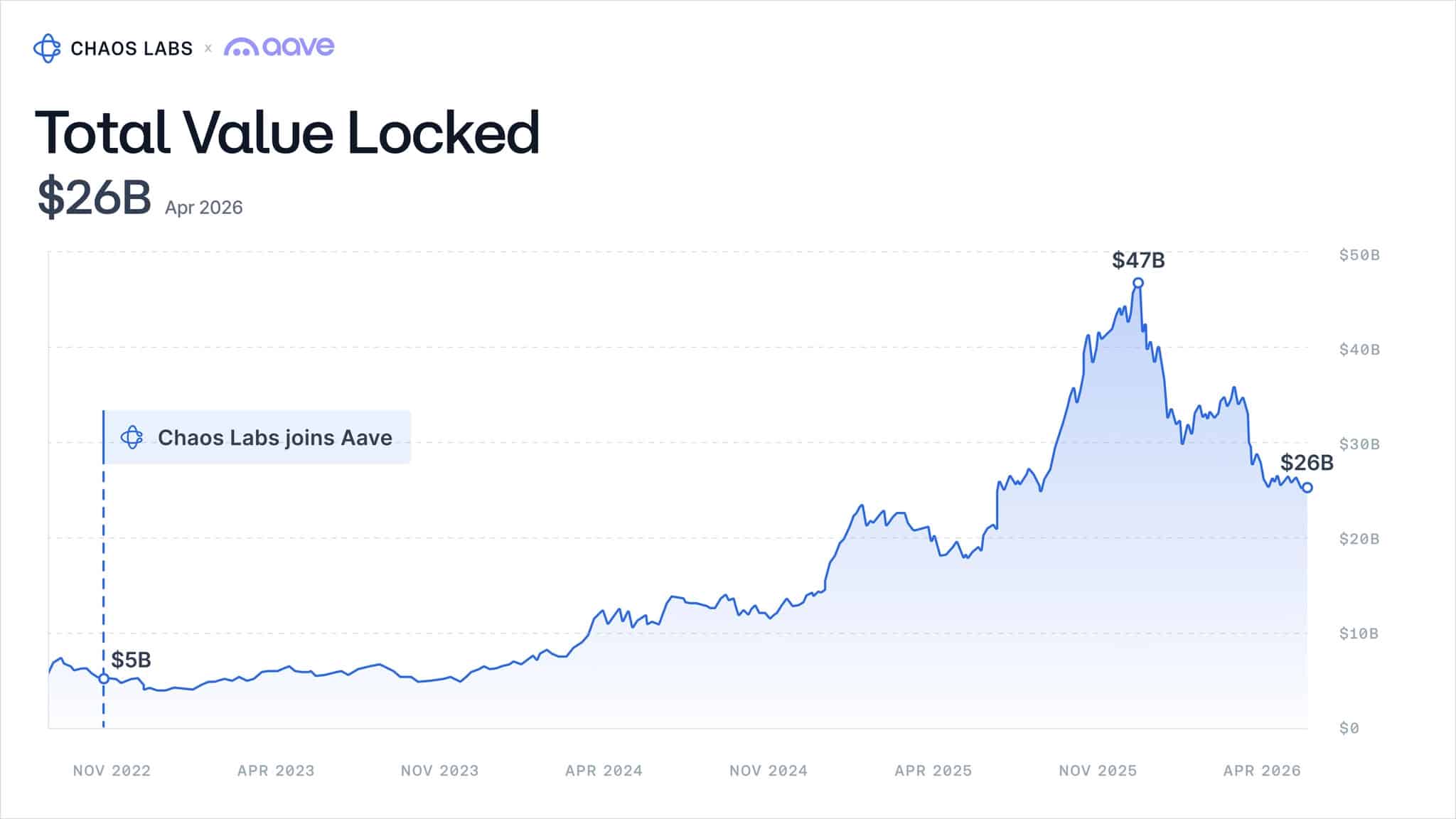

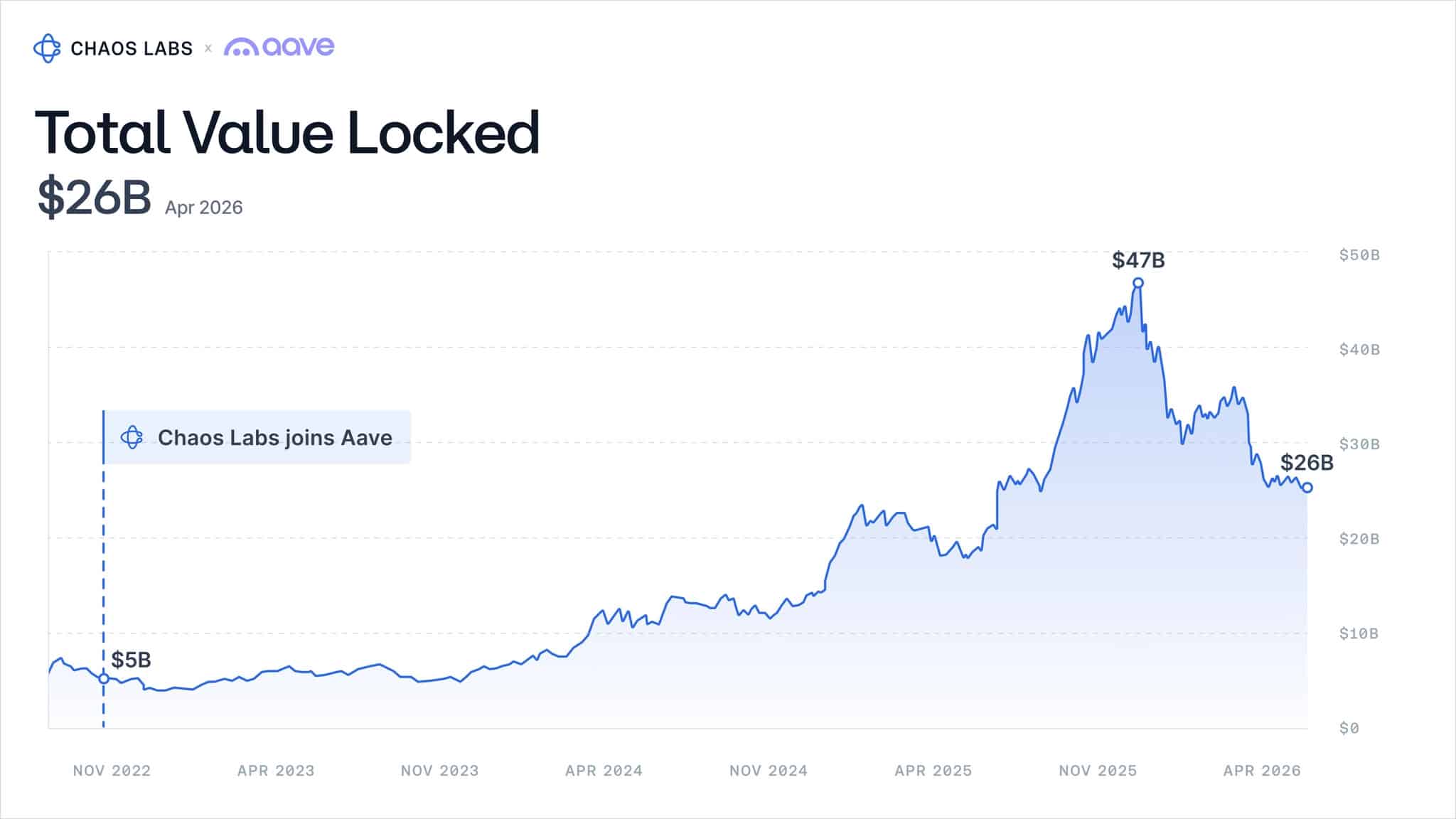

marsbitHá 16m