As the highly anticipated markup of the crypto market structure bill approaches, the White House’s top crypto advisor has slammed the banking industry’s CEOs amid efforts to reopen the stablecoin rewards debate.

ABA CEO Urges Banks To Block Stablecoin Rewards

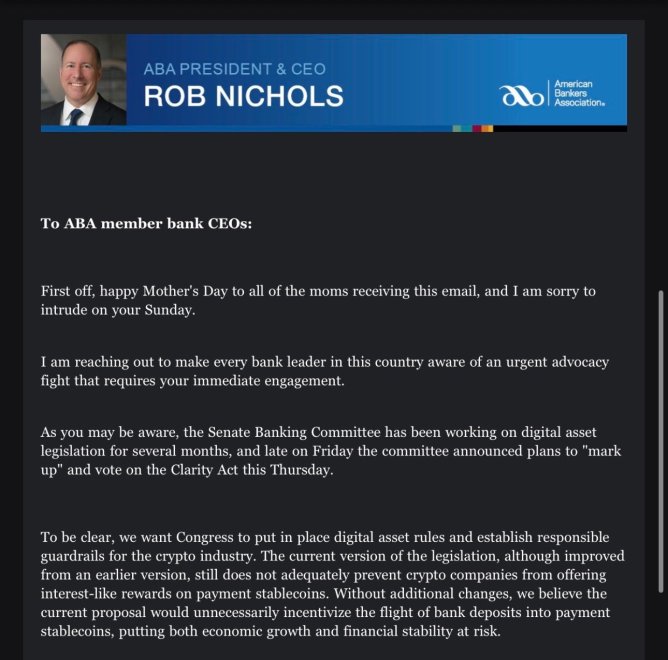

On Sunday, the American Bankers Association (ABA)’s CEO, Rob Nichols, sent a letter urging bank executives to push lawmakers to revisit the language on the crypto market structure bill, known as the CLARITY Act, ahead of its Thursday markup.

Nichols affirmed that he was “reaching out to make every bank leader in this country aware of an urgent advocacy fight that requires your immediate engagement,” adding that he wants Congress to establish digital asset rules and responsible guardrails for the crypto industry.

Nichols letter to bank executives. Source: Brendan Pedersen on X

However, he considers that the latest version of the bill “still does not adequately prevent crypto companies from offering interest-like rewards on payment stablecoins,” which would “unnecessarily incentivize the flight of bank deposits into payment stablecoins, putting both economic growth and financial stability at risk.”

“We believe the committee members may not be fully aware of the risks to the economy posed by the stablecoin loophole. Your immediate engagement can make a difference,” Nichols’ letter read.

For context, the latest version of the CLARITY Act prohibits any activity “economically or functionally equivalent to the payment of interest or yield on an interest-bearing bank deposit” on payment stablecoins.

Nonetheless, the text allows for payment of rewards tied to bona fide activities, including staking, transaction activity, or liquidity provision, aiming to promote a “buy and user” approach.

Last Friday, US banking trade groups, including ABA, sent a letter asking senators to amend the stablecoin yield compromise ahead of the markup, arguing that the language on the current version of the legislation still leaves room for rewards programs that could effectively replicate yield.

White House Crypto Advisor Slams CEOs For Skipping Yield Talks

Patrick Witt, executive director of the US President’s Council of Advisors on Digital Assets, fired back at Nichols and other banking industry CEOs for their recent push to revisit the Senate Banking Committee’s compromise on Stablecoin yield and rewards.

In an X post, Witt reacted to the recent letters, affirming that he had specifically requested that Nichols and other bank trade CEOs attend the White House’s meetings to mediate the stablecoin yield dispute, but that they refused.

As reported by Bitcoinist, the White House held multiple meetings to resolve the disagreement between the crypto and banking industries, which has delayed a vote on the legislation for four months.

Some reports at the time noted that no individual bank representatives attended the February meeting, but that the sector was represented through trade associations, including ABA, the Banking Policy Institute (BPI), and the Independent Community Bankers of America (ICBA).

“I guess the White House was beneath them?” the crypto advisor wrote on Monday. “In their defense, I wouldn’t want to have to defend their position in public either.”

Meanwhile, Senate sources have told journalist Eleanor Terret that the banking trade group effort was “pretty milquetoast,” adding that Committee members have already shifted their focus to wrapping up other outstanding issues in the bill, such as ethics language, which may complicate the sector’s efforts to reopen the debate.

“Still, the issue could resurface once the legislation reaches the Senate floor, where the banking groups may try to win over senators not on the Banking Committee,” Terret pointed out.

The total crypto market capitalization is at $2.7 trillion in the one-week chart. Source: TOTAL on TradingView