Author: Wenser, Odaily Planet Daily

Editor: Hao Fangzhou

Original Title: Spreads Exceeding 50%, The Pre-Market Crypto-Stock Arbitrage Market to Become a New Business in the Crypto Bear Market

Not long ago, Mysten Labs CEO evan.sui shared his views on the "bear market." He mentioned that he does not agree with the so-called "the bear market is great, keep building" argument. In fact, the bear market is not "great"; packaging it as good for everyone overlooks the real costs (such as discouraging builders and users). Many retail investors and excellent teams will face cash flow breaks and have to exit, ultimately harming the long-term development of the crypto industry.

However, data evidence is inconsistent with this view. A report released by Lattice VC in October 2024 showed that at that time, over 80% of crypto startups that announced seed round financing during the 2022 bear market were still building. In other words, if project parties can ensure relative stability in personnel and funds, the bear market is indeed more conducive to project construction and development. As for the reasons, perhaps it's because project parties focus more on product development and experience optimization during a bear market; or perhaps the bear market trains project parties in various abilities to survive. In short, being in a crypto bear market, project parties determined to start a business might instead find a way out of desperation and carve their own path of development.

In view of this, we will explore the potential employment tracks and project directions in this cycle through a series of articles titled "Crypto Bear Market Startup Guide." If crypto projects are born and grow rapidly in the future as a result, Odaily Planet Daily also welcomes project parties to discuss cooperation.

Today, let's first talk about the hottest potential entrepreneurial direction at the moment besides prediction markets—the pre-market price difference market for crypto and stocks.

The Real Demand of the Pre-Market Crypto-Stock Market: Platform Differentiation and Liquidity Bridge

As an intermediate bridge connecting the crypto market and the traditional financial market, crypto-stock trading platforms have not only received high attention and active participation from crypto project parties, but global leading securities platforms including Nasdaq and the New York Stock Exchange have also ventured into it, aiming to capture the incremental market while further activating liquidity in the traditional financial market.

Furthermore, not only have listed cryptocurrency concept stocks undergone tokenization and on-chain contract transformation, but many hot concept stocks that have not yet IPOed have also been highly sought after by both the crypto market and the traditional financial market, thus giving rise to several pre-market stock tokenization trading platforms.

Considering that the capital market is about to welcome a wave of US listings this year, including OpenAI, Anthropic, SpaceX (xAI), Kalshi, Polymarket, OKX, Kraken, and a series of AI model companies, commercial aerospace companies, prediction market platforms, and crypto exchanges, 2026 is undoubtedly a "big year for IPOs."

Against the backdrop of the crypto market falling intermittently with occasional rebounds and the stock market rising everywhere节节攀升, the heat of the pre-market stock trading market further corroborates the above view—there is strong demand for pre-market trading of hot concept stocks in both the crypto market and the traditional financial market.

This is the main reason for the emergence of pre-market stock trading platforms such as PreStocks, Jarsy, and Tessera. Additionally, compared to pre-market stock trading markets in the traditional financial market such as Hiive and Nasdaq Private Market, the trading methods, purchase quotas, and entry barriers of the crypto pre-market trading market are more flexible, and the premiums are relatively higher, so many users participate enthusiastically.

But just as the same token can have different degrees of price differences on different exchanges, before the pre-market stock market temporarily introduces a mechanism similar to an oracle, whatever the reason, we can clearly see that the pricing of the same underlying stock on the different platforms mentioned above has certain price differences.

Based on the above information, we can make a judgment—the crypto market still lacks one or more "bridge platforms between pre-market stock trading markets."

This is probably a necessary step to push stock tokenization and pre-market stock tokenization further forward—a unified comprehensive platform covering pre-market trading in both traditional financial markets and crypto markets.

Below, we will take the 2 leading prediction market platforms Kalshi and Polymarket, which are recently seeking $20 billion in financing, and SpaceX (xAI), valued at $1.25 trillion, as examples to discuss the feasibility and real demand of this "entrepreneurial direction."

Comparing Pre-Market Spreads of PreStocks, Jarsy, Tessera 3 Major Platforms: Maximum Spread Rate Exceeds 50%, Price Difference Up to Nearly $150

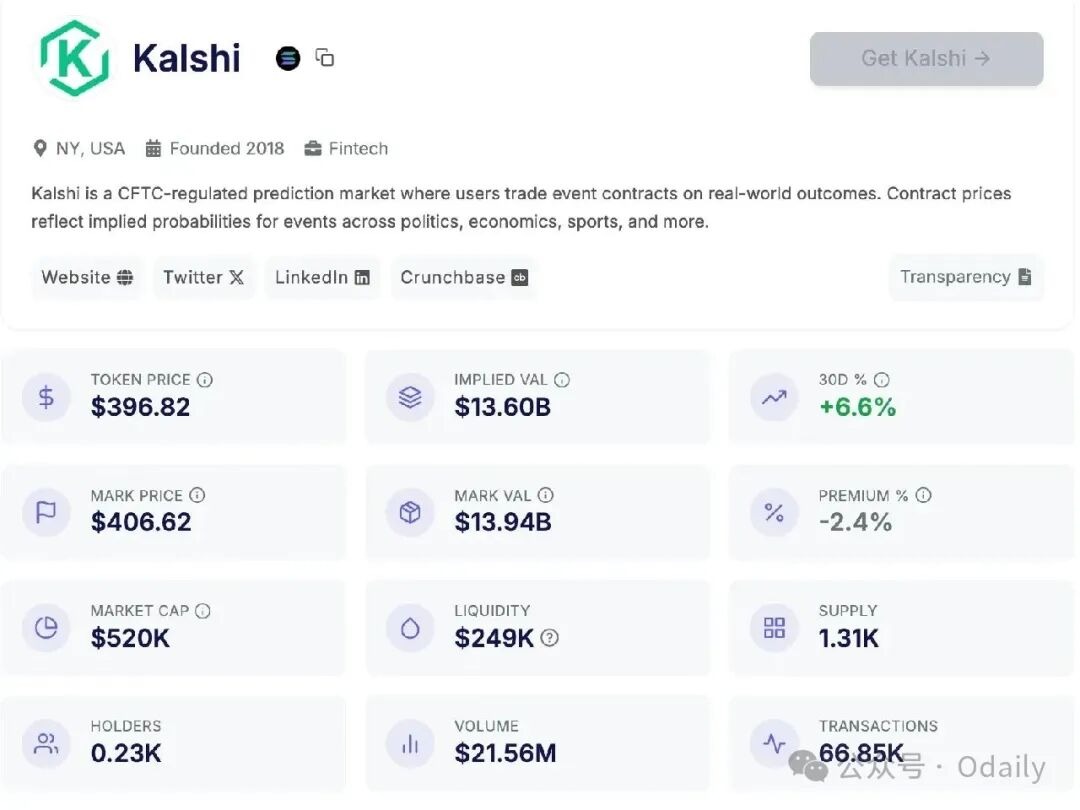

Kalshi Pre-Market Spread: Up to $148, Spread Rate About 37%

Taking the Kalshi pre-market trading market as an example, its prices on different platforms are as follows—

PreStocks platform, the pre-market price of the stock token is about $397; (Compared to the $369 we mentioned one month ago in the article "Kalshi Trading Volume Continues to Break New Highs, What is a Reasonable Pre-Market Stock Price?" (https://www.odaily.news/zh-CN/post/5209330), it has increased by nearly $30, a increase of 7.6%)

Jarsy platform, the pre-market stock price is quoted at about $545. (Compared to the $504 we mentioned one month ago in the article "Kalshi Trading Volume Continues to Break New Highs, What is a Reasonable Pre-Market Stock Price?" (https://www.odaily.news/zh-CN/post/5209330), it has increased by over $40, a increase of 8.1%)

In other words, the pre-market stock price of Kalshi has a spread of up to $148 between the two major trading platforms (Odaily Planet Daily Note: Considering that the two platforms adopt an order book trading mechanism and an on-chain liquidity token trading mechanism respectively, we are only making an abstract comparison here, temporarily not involving specific asset delivery forms, the same below). If calculated based on the $360 price of the traditional financial market pre-market trading platform Hiive, the pre-market spread is even as high as $185.

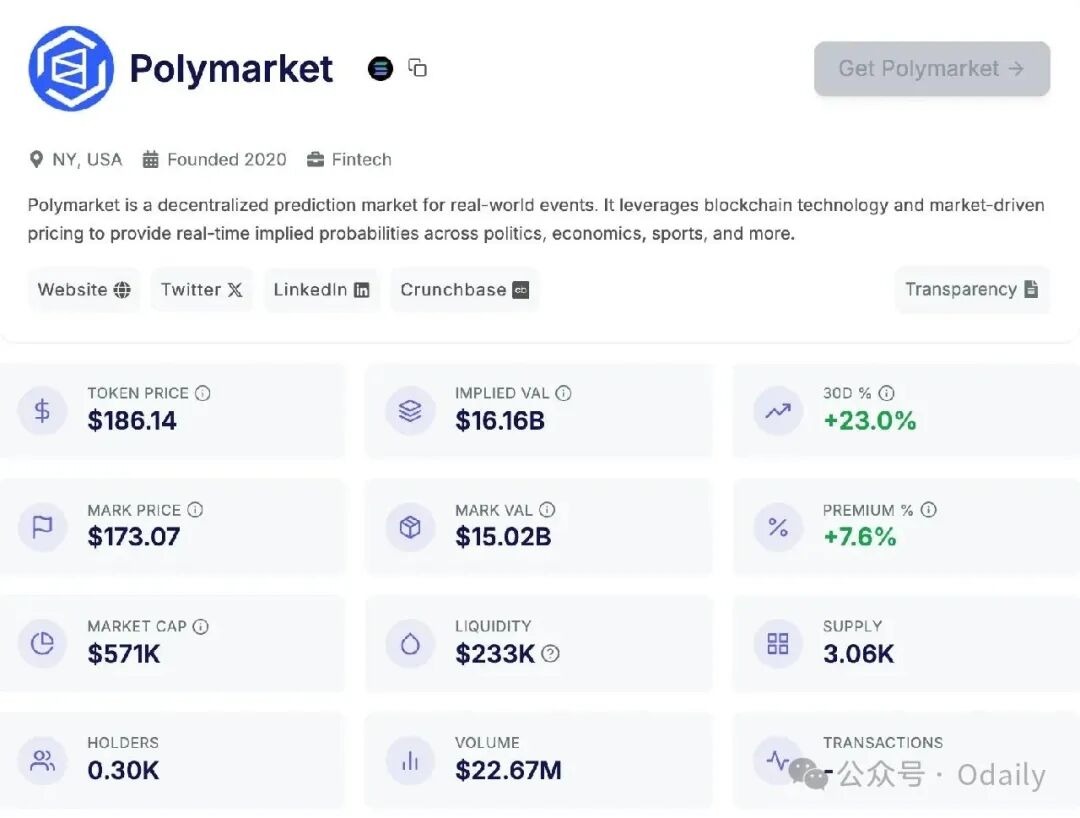

Polymarket Pre-Market Spread: Up to $94, Spread Rate Over 50%

Taking the Polymarket pre-market trading market as an example, its prices on different platforms are as follows—

PreStocks platform, the pre-market price of the stock token is about $186 (Odaily Planet Daily Note: up 23% in the past 30 days);

Jarsy platform, the pre-market stock price is quoted at about $280.

In other words, the pre-market stock price of Polymarket has a spread of about $94 between the 2 major platforms, with a spread rate of about 50.5%.

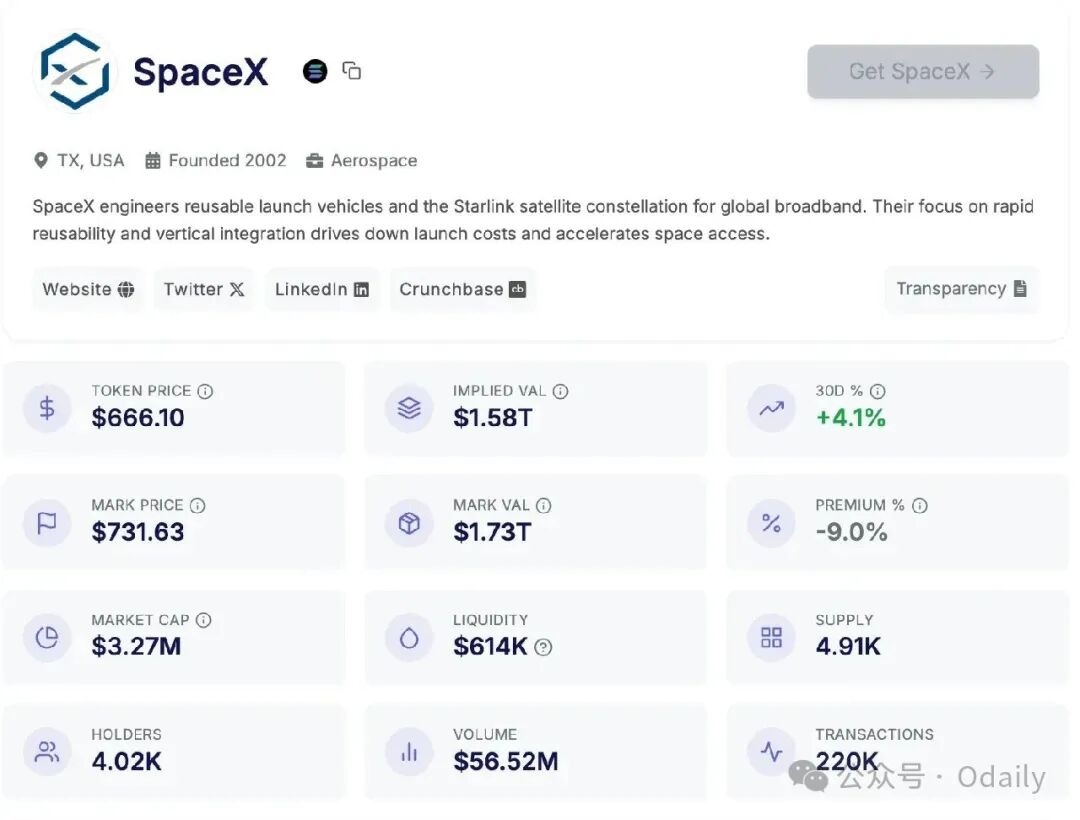

SpaceX(xAI) Pre-Market Spread: About $75, Spread Rate 12.7%

Taking SpaceX(xAI) as an example, its prices on different platforms are as follows—

PreStocks platform, the pre-market price of the stock token is about $666 (Odaily Planet Daily Note: up 4.1% in the past 30 days);

Tessera platform, the pre-market price of the stock token is temporarily reported at about $591 (Odaily Planet Daily Note: up about 14.5% in the past 30 days).

In other words, the pre-market stock price of SpaceX has a spread of about $75 between the 2 major platforms, with a spread rate of about 12.7%.

In summary, based on existing pre-market trading platforms, it might be possible to build a crypto-stock pre-market spread market to meet the trading demand and speculation demand of the market after having sufficient pre-market tokens or pre-market equity capital.

Of course, considering that the current market liquidity remains within the million-dollar level, the main business model of this platform may lie in transaction fees or LP fees, as well as the realization of price differences from the platform's own investment quotas.

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Communication Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush