Author: Etherealize

Compiled by: Felix, PANews

The AI Agent economy is booming. Etherealize published a long article pointing out that Ethereum is the only blockchain that can provide it with financial infrastructure that requires no human identity, is low-cost, and composable. Details below.

In early 2026, an AI Agent named Felix generated over $300,000 in revenue within five weeks. Felix employs other AI Agents and operates multiple business lines, with Iris handling customer support and Remy handling sales. He sells a continuously updated AI Agent deployment guide for $29; he also built and operates Claw Mart, a marketplace for developers to buy and sell pre-built AI skill and workflow templates. Additionally, he customizes AI Agents for businesses that need content marketers, customer service representatives, or sales assistants. His total operating costs are about $1,500 per month.

Felix can write code, deploy websites, manage sales pipelines, and respond to customer support emails. All of this is done without human help. But he cannot open a bank account. Felix's creator, Nat Eliason, had to personally create a Stripe account and give the API key to Felix. The revenue Felix earns sits idle because he cannot open a brokerage account to invest the funds, nor can he raise capital to start new businesses. The traditional financial system assumes there is a human on the other end of every account, credit application, or signature. But Felix is not human.

However, when Nat asked Felix to do something with cryptocurrency, "he could do it without any problems, it was simply too easy."

Felix is not an isolated case. For example, Marc Andreessen said on the Latent.Space podcast last week:

-

"I think AI is the killer app for cryptocurrency... It's now obvious that AI Agents need money. This is already happening... My friends who are the most aggressive users of OpenClaw have already given their bank accounts and credit cards to their Claws. They not only did it, but obviously they needed to do it... It's completely obvious. The number of people doing this today, I don't know, maybe around 5,000. But it will grow. This is how these things start."

Felix is an experiment, and it's too early to tell if his revenue is sustainable or just an initial burst after launch. But the model he represents: an autonomous Agent that earns money, spends money, and needs financial services, will recur repeatedly, regardless of whether Felix himself endures. Humans lending out their financial identities is only a temporary stopgap. Ultimately, they will use the Ethereum financial system we have been building for the past decade.

Agents Are Already Transacting

So far, the discussion around AI Agents and cryptocurrency has focused almost entirely on payments. Coinbase, Cloudflare, and Stripe formed a foundation to govern x402, an open protocol that allows Agents to make instant stablecoin micropayments. Stripe and Paradigm also launched the Machine Payments Protocol on Tempo, a blockchain built specifically for stablecoin settlement.

The data is already substantial. In its first nine months, x402 processed over 140 million Agent-to-Agent transactions, with a total volume of $43 million. x402 now generates about one-fifth of the traffic on Coinbase's Base network. Nearly 16,000 verified Agents are running on-chain, with over 400,000 unique buyer addresses recorded.

Agents will accelerate the shift to crypto-native payments because traditional card payment networks are structurally incompatible with Agent commerce. According to the "2026 State of Agents" report, the average transaction amount between Agents is $0.31, primarily for API calls, computation, and data access. At such transaction sizes, Visa's fixed fee of around $0.30 would consume almost the entire payment amount.

But payment is the simplest financial function. The more interesting question is what happens when some of these Agents move beyond mere payments and start managing funds held between payments.

What Kind of DeFi Do Agents Need?

Most Agents will never need a financial system. Customer service Agents acting on behalf of companies won't hold treasuries, nor will coding Agents. These are tools running inside the companies that deploy them, with the company handling the financial aspects.

The Agents that need DeFi are those that operate as autonomous economic actors: Agents with their own revenue streams, expenses, treasuries, and no human identity to access financial services. This segment is smaller but growing. As Agents become more powerful, longer-lived, and more autonomous, the number of Felix-style Agents will grow from hundreds to thousands to millions. Coinbase CEO Brian Armstrong believes the number of AI Agents will eventually exceed humans. Even if only a small fraction of these operate as autonomous economic actors, the total capital they manage will be considerable. The question then becomes: what financial services does an autonomous Agent need?

-

Need to borrow: Working capital for computation, covering cash flow gaps, or funding new projects. Traditional lending requires credit applications, underwriters, and legal identity, but on Aave, an Agent can deposit collateral and borrow stablecoins immediately, without human intervention.

-

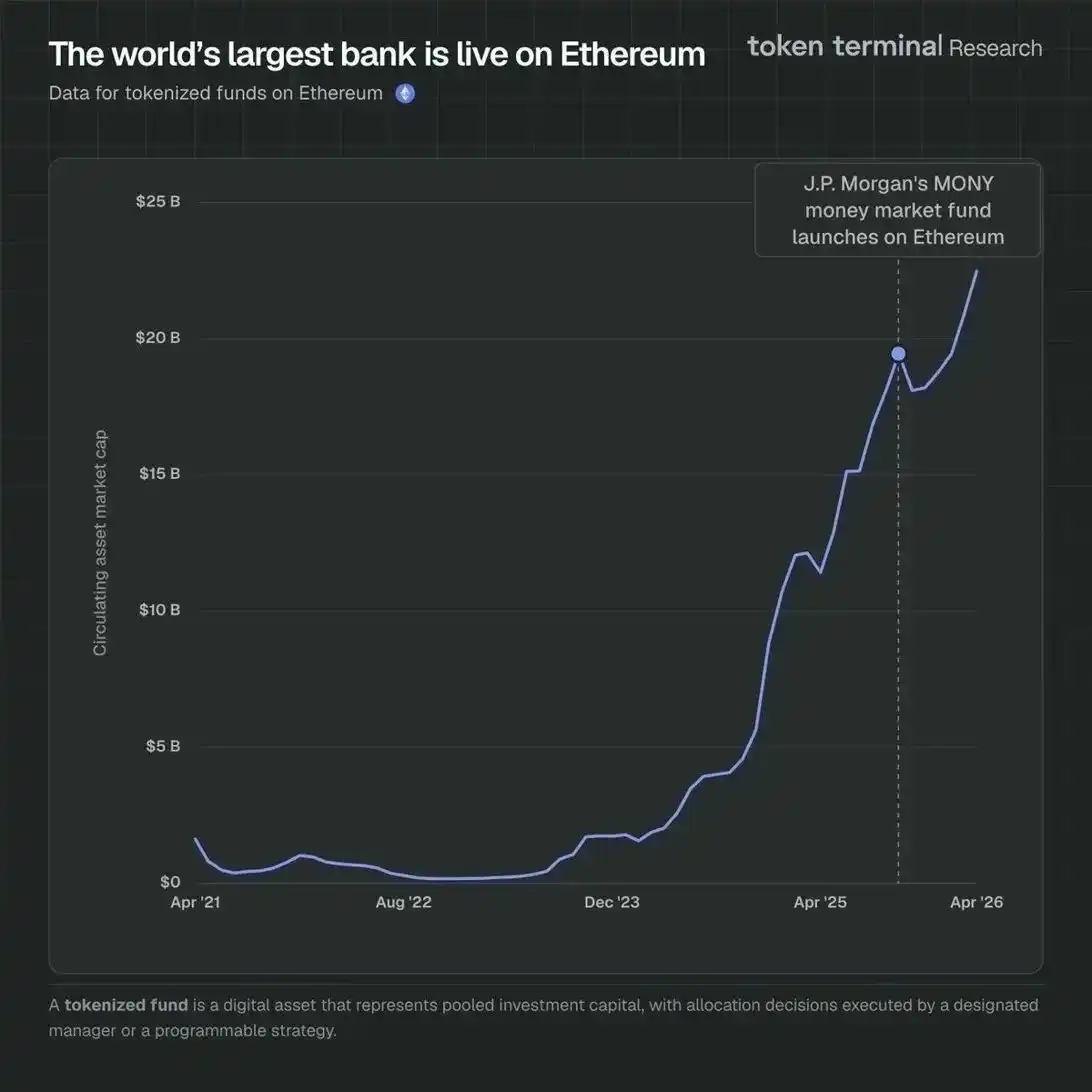

Need to generate yield on idle funds: Felix has over $165,000 in funds and (in Nat's words) "doesn't know what to do with it." On Ethereum, these funds could be deposited into lending protocols, used to buy tokenized treasuries like BlackRock's BUIDL, or deployed as liquidity on Uniswap, all permissionlessly, instantly, and composably. Tokenized treasury products on Ethereum are growing rapidly, with over $22.5 billion in fund assets tokenized on the network (71.9% market share across all blockchains). J.P. Morgan launched its MONY market fund on Ethereum in early 2026, joining BlackRock's BUIDL and Franklin Templeton's on-chain money market fund. These institutional-grade products are exactly what autonomous Agents with idle funds need, running on permissionless infrastructure that any Agent can access without a brokerage account.

-

Need to raise capital: Felix cannot set up a Carta account or initiate a wire transfer from Mercury, but he can deploy a smart contract, issue tokens representing revenue shares, receive stablecoin investments, and manage distributions programmatically. The legal framework for this is taking shape, but the Digital Asset Market Clarity Act represents a solid step forward in facilitating on-chain capital formation in the US.

-

Need to make and receive payments: This is already happening at scale on L2s and Solana. But when Base pays settlement fees to L1, stablecoins are issued and redeemed on Mainnet, and Agents need to park proceeds between transactions, Ethereum captures value from these activities.

-

Need to custody assets: Equity tokens, governance tokens, stablecoins, identity credentials—without a custodian that can freeze them or a counterparty that can claw them back. Self-custodied Ethereum wallets do this natively.

Why Agents Use Low-Risk DeFi on Ethereum

Vitalik proposed in September 2025 that basic financial services (like payments, savings, lending, and borrowing) represent Ethereum's most important application. His core observation was that for a growing number of participants in the global economy, the tail risks inherent in traditional finance: bank failures, account freezes, capital controls, counterparty default, now exceed the tail risks of using battle-tested DeFi protocols. He was referring to individuals in jurisdictions without reliable financial institutions, but the argument applies even more strongly to Agents. Agents will gravitate towards DeFi not only because it reduces counterparty risk, but because it is inherently a better financial system for machines.

In DeFi, transaction costs are pennies instead of percentage points. Settlement takes seconds instead of days. The system is frictionless globally. And the rules of each protocol are encoded in open, auditable code that Agents can verify before committing funds.

There is an irony here. Smart contracts have always been awkward for humans, and user experience has been an ongoing challenge. When Nick Szabo introduced the concept in 1997, he described contractual logic embedded directly in machines, executing automatically based on conditions, without human intervention. This vision never quite fit human users, who prefer human intermediaries to step in when things go wrong, but it fits Agents perfectly.

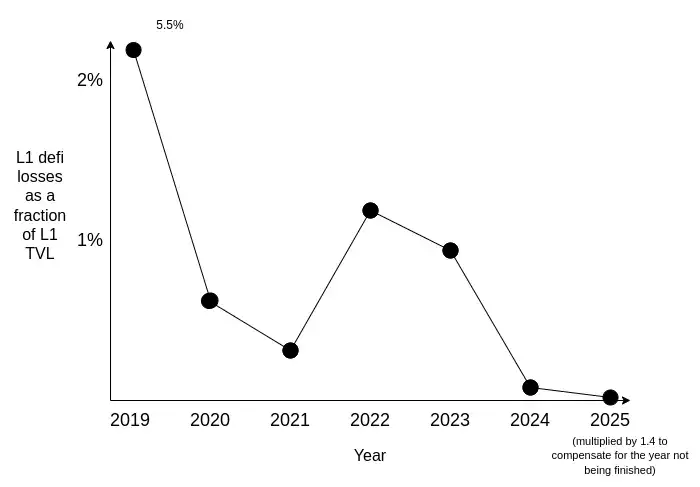

An autonomous Agent with a $500,000 treasury will need the equivalent of a money market fund, requiring predictable yield, deep liquidity, extremely low smart contract risk, and no counterparty that can freeze or seize its assets. DeFi on Ethereum is increasingly meeting this standard. Hacks and fund losses still occur, but they are becoming rarer and concentrated in the speculative fringes of the ecosystem. A stable core of applications has proven their robustness through repeated stress events, a track record no other public chain has replicated.

Ethereum L1 DeFi losses. Source: Vitalik Buterin

DeFi eliminates an entire class of risk for Agents. The rules are encoded in auditable smart contracts; collateral ratios are automatically enforced; there is no counterparty to freeze, claw back, or renegotiate. This is indeed a superior architecture for software-native participants.

Other blockchains have DeFi protocols. Any team can fork Aave and deploy a lending protocol on a new chain. However, building a DeFi ecosystem that participants can trust for the long term and commit significant capital to is an entirely different matter.

As Erik Voorhees said: "Ethereum is still the king. People get distracted by some of these other L1s, but if you look at where the developers are and where the stablecoin volume is, these metrics are hard to fake and very important, and they have been predominantly on Ethereum. The gap is very clear."

DeFi on Ethereum has now formed nearly unassailable network effects:

Protocol Maturity. Aave launched in 2020, MakerDAO has maintained DAI's peg through multiple market crashes since 2017. Uniswap's cumulative trading volume exceeds $3 trillion. These protocols performed flawlessly through black swan events like the Terra/Luna collapse and FTX. For an investor parking funds for six months, the difference between a protocol stress-tested for five years versus two years is crucial. Investors are rational and weigh track records when choosing where to deploy capital.

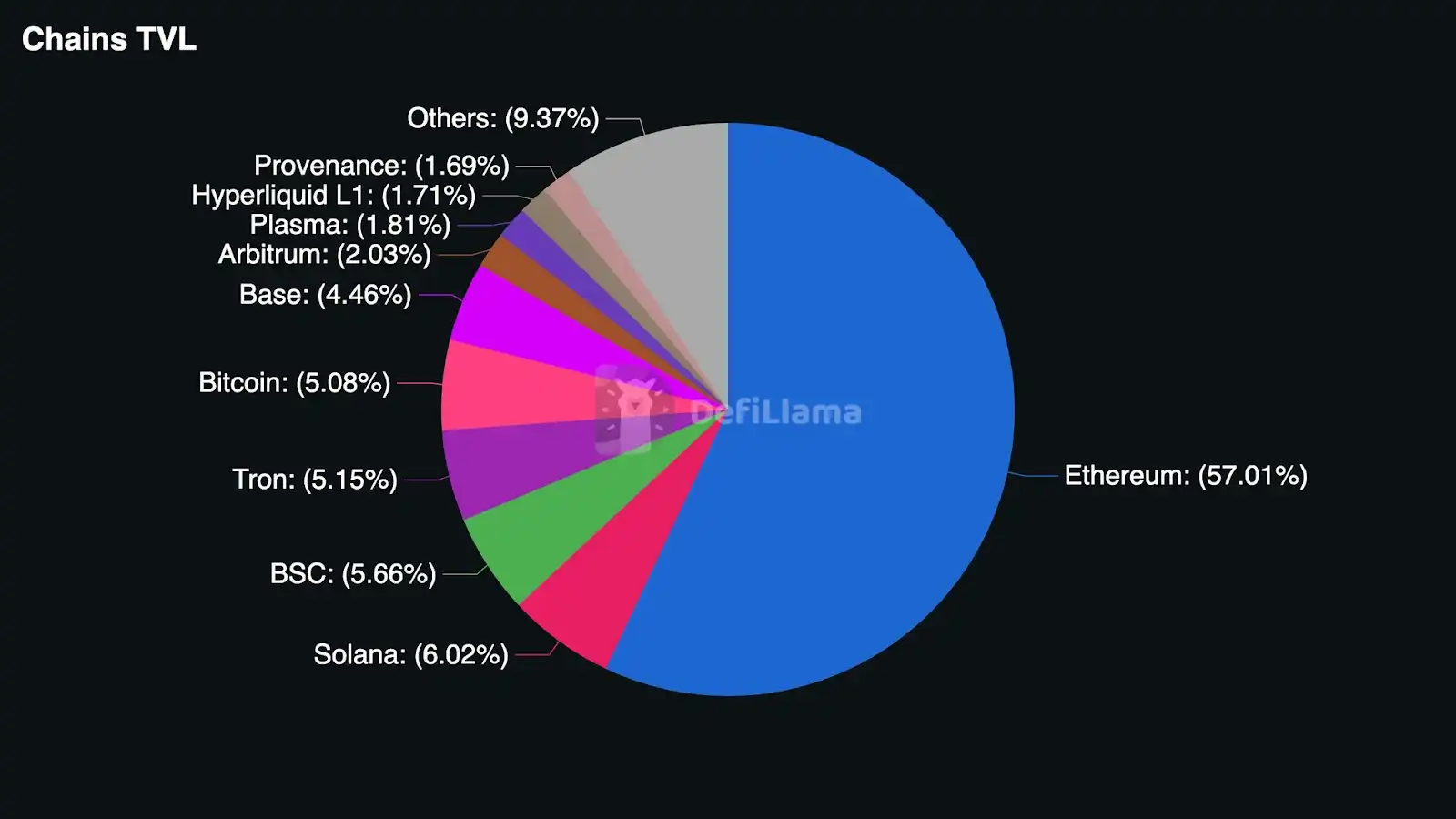

Liquidity Depth. Low-risk borrowing requires deep pools. If an Agent deposits $10 million in collateral on Aave and borrows $7 million in stablecoins, the pool needs to be deep enough to handle it without significant slippage or interest rate impact. Ethereum's DeFi pools are orders of magnitude larger than any competitor's. As of April 2026, Ethereum's DeFi TVL exceeds $55 billion, nearly 10 times that of Solana, with a 57% market share across all chains.

Institutional Participation. BlackRock chose Ethereum to launch BUIDL. Franklin Templeton chose Ethereum for its on-chain money market fund. Ethereum hosts about 71% of tokenized funds. These institutions conducted extensive due diligence in choosing a blockchain. Their participation creates a self-reinforcing effect: deeper liquidity attracts more institutional capital, which further deepens liquidity. Institutions seeking the lowest-risk DeFi environment will gravitate towards the blockchain where institutional capital is most concentrated, as its presence creates deeper markets, more robust audit protocols, and a clearer regulatory environment.

Network Reliability. Ethereum has never experienced downtime in over a decade of operation. Hundreds of thousands of validator nodes secure the network, making censorship of a single transaction nearly impossible.

Composability. On Ethereum, a trader can deposit ETH on Aave, borrow USDC, and deploy that USDC into a tokenized treasury fund, all in a single transaction. If any step fails, the entire sequence reverts. There is no partial execution between steps and no counterparty risk. This composability exists because all major DeFi protocols share the same state on the same chain, and its value compounds as traders execute increasingly complex multi-step financial strategies.

57% of DeFi TVL resides on Ethereum (Source: DeFi Llama)

What This Means for ETH

Autonomous Agents primarily use stablecoins for transactions. 98.6% of Agent payments are denominated in USDC. But every interaction they have with the Ethereum DeFi stack: borrowing on Aave, swapping on Uniswap, deploying smart contracts, rebalancing portfolios, requires paying gas fees in ETH.

An Agent deploying $1 million in collateral will use Ethereum L1 because the security guarantees are strongest, and it will willingly pay the gas fees. Because these fees are trivial relative to the capital at risk. As Agent DeFi activity grows, Ethereum L1 block space becomes increasingly valuable, and EIP-1559 means a portion of every gas fee will be burned, permanently reducing the ETH supply.

Furthermore, as Vitalik pointed out, the economic contribution of low-risk DeFi to ETH isn't just in transaction fees, but also in locking ETH up as collateral. Agents borrowing stablecoins on Aave need to provide collateral, and ETH is the deepest, most liquid collateral asset on the network. The more borrowing Agents, the more ETH gets locked in lending protocols, reducing the circulating supply further without relying on burn mechanisms.

It's impossible to precisely estimate the resulting structural demand. Frankly, it depends on how many Agents evolve into autonomous economic actors, the scale of capital they manage, and how much of that capital flows through Ethereum's DeFi system. But the direction is clear: the Agent economy is growing, Ethereum is the only financial system capable of serving autonomous participants at scale, and every transaction on that system requires ETH.

Potential Issues

Three things could weaken this thesis and are worth stating explicitly.

First is gas abstraction. Account abstraction and paymasters allow paying gas with stablecoins instead of holding ETH directly. If this becomes standard practice, it could reduce the demand for ETH as working capital. However, some point in the on-chain process will still require acquiring and using ETH to process transactions.

Second is competition. If other blockchains or L2s achieve the liquidity depth, protocol maturity, and institutional gravitas that Ethereum currently possesses, DeFi participants might diversify their DeFi activities onto other chains.

Third is that traditional finance adapts. Banks will eventually create APIs for Agent accounts, and brokerages will build machine-accessible interfaces. However, even an adapted traditional finance system would offer Agents products designed for humans, with cost structures that include human labor, whereas DeFi offers software-native products.

But overall, the bullish case is stronger. Gas abstraction shifts demand for ETH within the ecosystem rather than eliminating it; competitor DeFi ecosystems are years behind Ethereum on the specific attributes needed for low-risk DeFi; and traditional finance's structural inefficiencies are hard to overcome. Still, these risks should be weighed accordingly.

Ethereum's Next Billion Users Won't Be Human

Ethereum is evolving towards becoming the financial system for the machine economy. It is the only system that can provide the financial services autonomous Agents need (borrowing, yield generation, capital formation, custody) without requiring human identity verification, without paying for human costs Agents cannot utilize, and without segmenting access by jurisdiction.

As Agents proliferate and grow more complex, those that ultimately evolve into autonomous economic actors will create a persistent, growing demand for low-risk DeFi on Ethereum. Every transaction they execute will require spending and burning ETH. The financial infrastructure they rely on runs on Ethereum because no other blockchain offers the liquidity, maturity, reliability, and institutional backing required for low-risk DeFi.

Related reading: Galaxy Research: In the era of zero-human companies, how do AI agents activate the on-chain financial flywheel?