Grass

Project Twitter: https://x.com/grass

Project Website: http://grass.io/

This Unlock Amount: 57.29 million tokens

This Unlock Value: Approximately $11 million

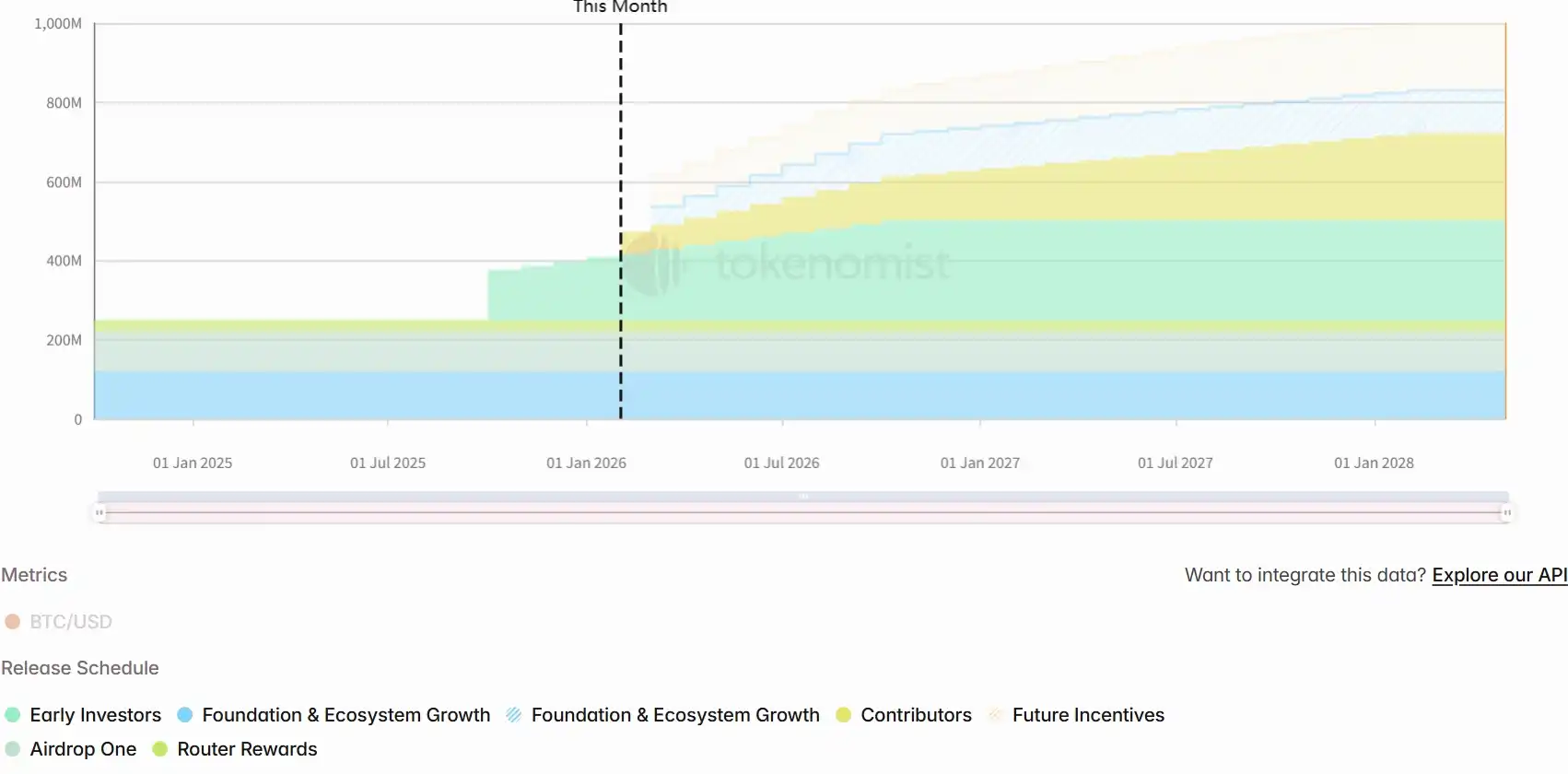

Grass is a project deployed on Solana that combines AI, DePIN, and Solana technologies, positioning itself as the data layer for AI. As a decentralized network, Grass aims to provide the data required for AI model training by accessing public networks.

Specific release curve is as follows:

EigenLayer

Project Twitter: https://x.com/eigenlayer

Project Website: https://www.eigenlayer.xyz/

This Unlock Amount: 36.82 million tokens

This Unlock Value: Approximately $7.26 million

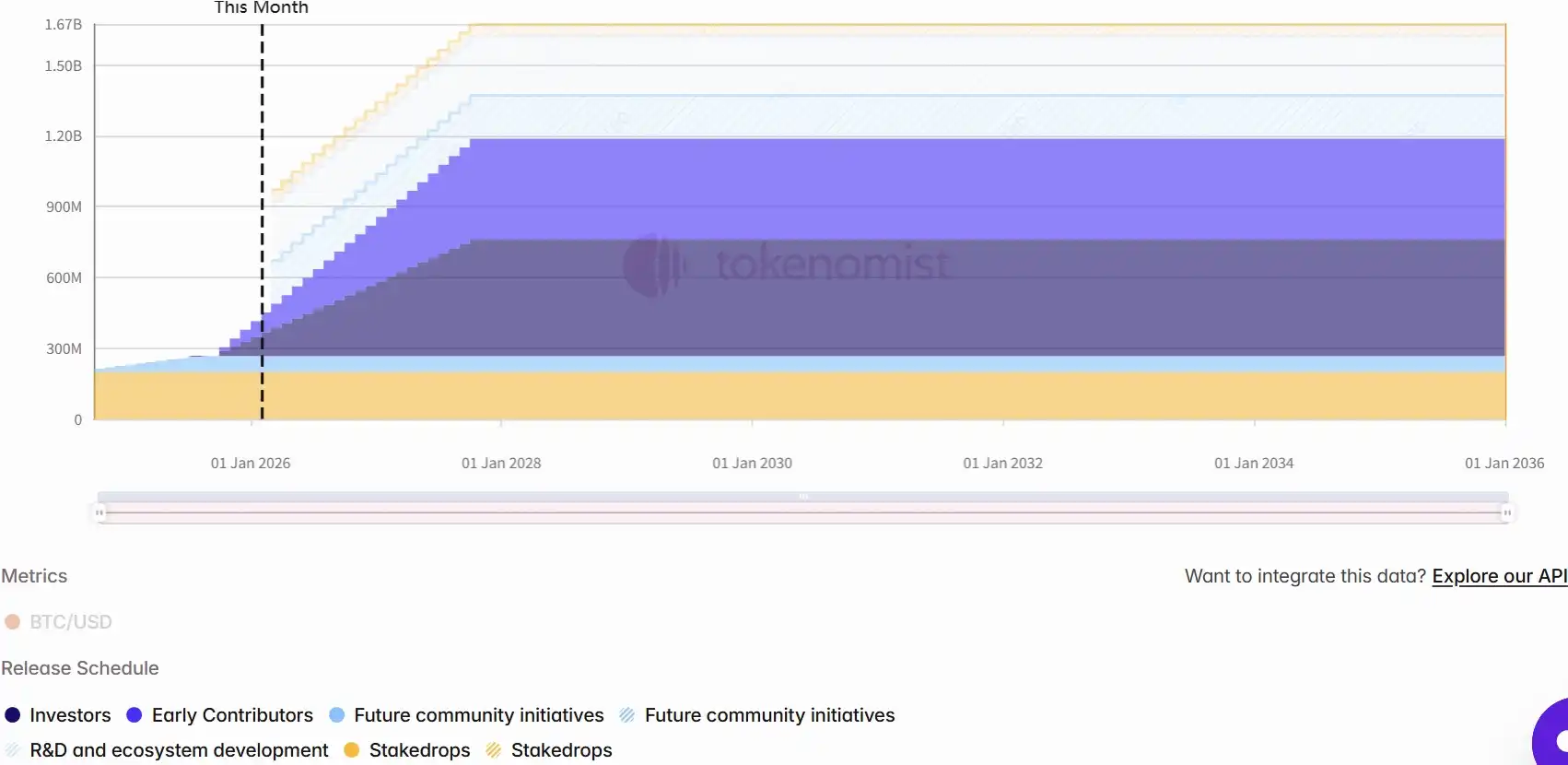

EigenLayer is a protocol built on top of Ethereum that introduces the concept of restaking, a new primitive in cryptoeconomic security. This primitive allows for the restaking of ETH at the consensus layer. Users who stake ETH can opt into EigenLayer smart contracts to restake their ETH and extend cryptoeconomic security to other applications on the network.

Specific release curve is as follows:

SoSoValue

Project Twitter: https://x.com/SoSoValueCrypto

Project Website: https://sosovalue.com/

This Unlock Amount: 13.32 million tokens

This Unlock Value: Approximately $4.99 million

SoSoValue is an AI-driven investment research platform that combines the efficiency of CeFi with the transparency of DeFi, dedicated to addressing challenges such as information overload and cross-chain asset management in the cryptocurrency market.

Specific release curve is as follows: