Original Author: Hu Tao, ChainCatcher

As the encryption industry becomes increasingly mainstream, Chinese entrepreneurs seem to be moving further away from the center stage.

There was a time when projects founded by Chinese people accounted for half of the industry, including well-known cryptocurrency exchanges such as Binance, OKX, Bybit, Bitget, Gate, HTX, and Bitmart. This was even more true in the mining sector, where projects like Bitmain, Canaan, and Spark Pool held significant positions in the industry. Their commonality is that they were all established in 2017-2018 or even earlier.

Although Changpeng Zhao, Mingxing Xu, Jihan Wu, and Justin Sun are still actively working on the front lines of the industry, after the DeFi Summer boom in 2020, a general consensus has gradually formed: the visibility and influence of the new generation of Chinese entrepreneurs in the global encryption industry have declined, and so far, no leaders comparable to the previous generation of industry figures have emerged. Given this gap, what has happened to the ecosystem of Chinese entrepreneurs? Where are the future opportunities?

Regulatory and Geopolitical Reshaping: The First Impact of Ecological Disruption

The most significant factor over the past five years has been the drastic changes in regulatory and geopolitical environments.

Starting in 2021, China significantly increased its governance efforts on cryptocurrency-related activities, swiftly shutting down previously gray-area scenarios such as trading and mining. In recent market hotspots, almost any popular concept has been flagged by regulators, from earlier ICOs, NFTs, and digital collectibles to recent payment and real-world asset topics. This undoubtedly limits the inflow and support of high-quality resources into the Chinese encryption ecosystem to some extent.

These crackdowns not only accelerated the relocation of mining and exchange businesses but, more importantly, deprived Chinese entrepreneurs of a native market with natural network effects, high talent density, and capital concentration, forcing them to develop in unfamiliar overseas environments.

In the early encryption ecosystem, many explosively growing Chinese projects rapidly accumulated users through the mobilization mechanisms of Chinese internet communities: WeChat group fission, KOL networks, media matrices, offline gatherings... These channels were once one of the most efficient systems for spreading encryption narratives. However, changes in regulatory policies have largely invalidated this system.

What followed was the rapid shift of the industry's power center to Europe and America—the dominance of U.S. compliance, the influx of institutional capital, and the increasing maturity of regulatory frameworks began to shape an industry order vastly different from that of 2017–2018. New narratives, new regulatory landscapes, and new capital structures naturally favor English-speaking markets and compliance-oriented entrepreneurial teams. For example, prediction markets, which have a certain gambling nature, are unlikely to emerge in the Chinese-speaking market environment where gambling is strictly regulated.

In such an industry environment, the new generation of Chinese entrepreneurs also finds it harder to gain "default trust" from global media, regulators, capital, and users, requiring more trial and error costs in areas like marketing and compliance compared to similar European and American projects.

Shift in Capital Preferences: The Second Impact of Ecological Disruption

If the institutional barriers created by regulatory and geopolitical environments are the first impact, then the "structural shift in preferences" from the capital market side further exacerbates the marginalization trend of Chinese entrepreneurs in the new cycle.

In today's industry environment, without strong VC funding and resource support, projects are at a disadvantage in user acquisition, token listings, and narrative building. Chinese entrepreneurs are already at a disadvantage on the funding front.

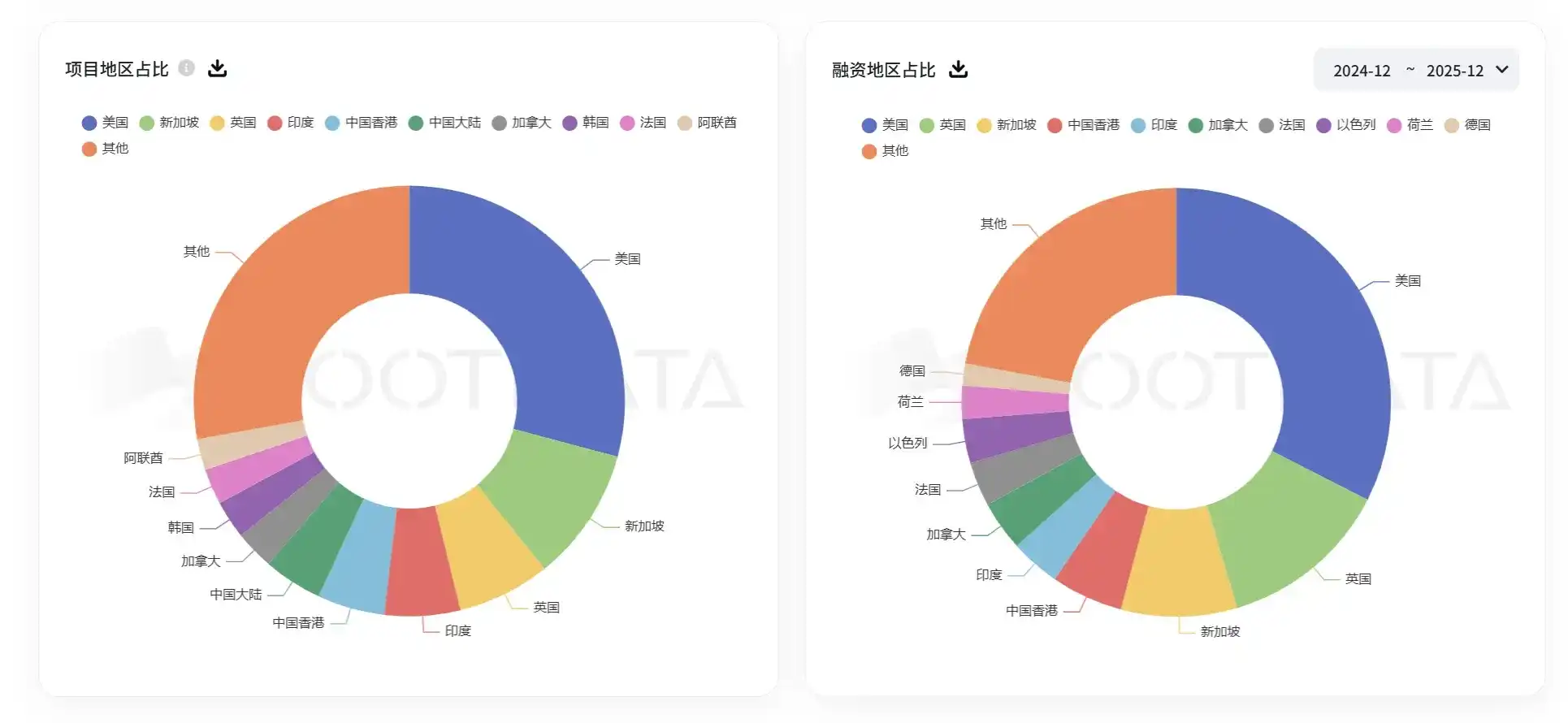

Due to the poor performance of altcoins and a significant decline in investment returns, Chinese-background VCs have largely reduced their investment frequency or even stopped entirely over the past 2-3 years. Chinese entrepreneurs face significant constraints in both financing and exit paths. When dealing with VCs dominated by Europe and America, Chinese projects struggle to gain an advantage due to language and cultural differences. As a result, the amount and number of financings secured by Chinese projects have been declining in recent years.

Industry share of the number and financing amount of projects from mainland China Source: RootData

This year, the encryption industry has seen a wave of IPOs and mergers and acquisitions, with companies like Circle and Gemini successfully listing on U.S. stock exchanges, and Coinbase and Ripple frequently making acquisitions. This has significantly boosted confidence among entrepreneurs and VCs, but these developments have largely bypassed Chinese projects. It can be said that European and American projects are enjoying the institutional dividends of the mainstreaming of the encryption industry.

In the eyes of mainstream capital, European and American projects have inherent advantages in compliance, cultural recognition, and exits. Unless Chinese projects have exceptional team composition and technical background, they are unlikely to win the favor of European and American capital.

Mismatch Between Capability Structure and Industry Maturity: The Third Impact of Ecological Disruption

Over the past decade, the main theme of the encryption industry has been in the infrastructure and tool sectors. Although new concepts like DeFi, NFTs, gaming, and inscriptions have emerged, most have failed to become mainstream projects.

In a previous interview with ChainCatcher, Jason Kam, founder of Folius Ventures, stated that over the past 5 to 10 years, Web3 development has been about laying the foundation, focusing more on product categories and states. This has been a decade biased towards ecology, infrastructure, tools, and consensus-building. In other words, it has been a decade of B2B products.

Europe and America have three generations of extremely talented engineers who are very good at building this B2B ecosystem. In contrast, the Asia-Pacific region mainly has young engineers from the 80s and 90s generations, whose career paths developed alongside the boom of China's B2C industry starting in 2005. In other words, their engineering experience lies in B2C and applications, which is at odds with the development trajectory of blockchain. Therefore, they may not excel in public chains and infrastructure.

"If Asia-Pacific entrepreneurs compete with European and American entrepreneurs on the To C level, I believe Asia-Pacific entrepreneurs have no disadvantages; in fact, they may have advantages. Their advantages lie in their rich product experience and their highly aggressive tactics for capturing market share."

Although Chinese entrepreneurs have proven this in the more Web2-like exchange sector, and in on-chain C-end products, the fleeting success of Stepn demonstrated the talent of Chinese entrepreneurs in C-end products. However, the overall market explosion for consumer-grade products has been slow to arrive, which is closely related to the maturity of industry infrastructure. The market has not yet reached the "comfort zone" of Chinese entrepreneurs.

Entrepreneurs with Multicultural Backgrounds Are Becoming Industry Leaders

Strictly speaking, there have been no new cases of representative Chinese entrepreneurs in recent years. Jeff Yan, the founder of Hyperliquid, is of Chinese descent. His parents are Chinese immigrants, and he was born and raised in Palo Alto, California. He later attended Harvard University, majoring in mathematics and computer science. After graduation, Jeff joined the high-frequency trading giant Hudson River Trading as a quantitative trader. In 2022, Jeff founded Hyperliquid and, with the philosophy of "small but refined," no VC, and user-driven growth, built it into one of the fastest-growing giants in the encryption industry in recent years.

However, although Hyperliquid is one of the most successful projects in this cycle with "Chinese bloodline" participation, it is difficult to see it as a continuation of the influence of Chinese entrepreneurs. Jeff is almost never active in the Chinese ecosystem, projects almost entirely European and American values in the outside world, and has never expressed himself in Chinese. The rise of Jeff and Hyperliquid highlights a fact: in the new cycle, Chinese ancestry can still produce global influence, but it must integrate into the mainstream cultural system rather than rely on the old path of Chinese entrepreneurship. If you rely solely on one cultural system, you can only become a regional leader and cannot achieve excellent results in the globalization process.

In fact, the founders of many well-known Chinese projects that have become sector leaders in this cycle mostly have multicultural backgrounds, having studied in Europe or America at least during their university years. Examples include Sean Ren, founder of Sahara; Yu Hu, founder of Kaito; and Erick Zhang, founder of BuidlPad. Their long-term experiences in Europe and America play an important role in their development paths.

In fact, entrepreneurs with multicultural backgrounds are indeed more popular in the encryption industry. For example, the founders of Ethereum, Solana, and Binance's Changpeng Zhao all immigrated from China and Russia to North American countries during their childhood. The collision of different political systems and cultures allowed these entrepreneurs to recognize the value of blockchain in empowering individual sovereignty earlier and quickly take action. They prioritize cultural inclusivity in team building, resource对接, and daily operations, ultimately making it easier to gain the favor of users from different regional cultural backgrounds.

The inherently borderless nature of encryption and the regulatory and interest demands of various countries will dominate the development trends of the encryption industry for a long time through conflict and磨合. Against the backdrop of multiple conflicts between China and the U.S. and the mainstreaming of the encryption industry, Chinese entrepreneurs indeed face increasing challenges. However, as the encryption industry recently faces skepticism about gambling tendencies, nihilism, and the disproval of more and more project concepts, the development trend of Chinese entrepreneurs may no longer be an important industry question. What truly deserves attention is: as speculative growth and narrative泡沫 gradually recede, who can continue to invest in the long-term value of decentralized technology and redefine the industry's direction through real products and verifiable innovation.

The core competitiveness of the future industry landscape will depend more on whether founding teams possess cross-cultural collaboration capabilities, long-term technological investment capabilities, and institutional understanding and organizational resilience in the face of regulatory uncertainty. Regardless of cultural or national background, those who can persistently excel in these dimensions may become the true beneficiaries of the next cycle. In other words, the path to success in the encryption industry has never depended on "where they come from" but on "what they can achieve."