This article is from:Culper Research

Compiled by | Odaily Planet Daily (@OdailyChina); Translator | Azuma (@azuma_eth)

Editor's Note: On March 6, Wall Street short-selling firm Culper Research suddenly published an article announcing it is shorting ETH and related securities like BMNR. Culper Research's logic is that Vitalik and other developers miscalculated Ethereum's demand elasticity before the Fusaka upgrade, leading to the upgrade damaging ETH's token economic model. Culper Research also mentioned that Vitalik is well aware of this and is actively front-running with practical actions, while the deluded Tom Lee is heading towards a dead end.

In response to the firm's massive shorting, Vitalik himself and Tom Lee have not yet responded, but Vitalik's father, Dmitry Buterin (dima.eth), responded by saying: "When you see the phrase 'Vitalik knows this and is selling,' you don't need to read further. They are clowns craving attention, not researchers."

Below is the original content from Culper Research, compiled by Odaily Planet Daily. Compiling this article does not mean we agree with Culper Research's views, but is only to present the perspective and market煽动 of some Wall Street institutions regarding ETH.

Latest disclosure: We are shorting ETH and ETH-related stocks, including Bitmine (BMNR).

We believe that after the Fusaka upgrade in December 2025, ETH's token economic model has been broken. Vitalik knows this and is selling; while ETH's staunchest bull, Tom Lee, continues to add ineffective investments. ETH will continue to fall.

Tom Lee's Bitmine has consistently defended ETH, claiming that "ETH is not in a death spiral due to increasing utility." He cited the surge in active addresses and transaction numbers on Ethereum after the Fusaka upgrade as evidence of so-called "improved fundamentals" and institutional adoption, but he is completely wrong.

By Tom Lee's own logic, if on-chain activity on Ethereum does not reflect real usage growth and fundamental improvement, then ETH is indeed in a death spiral.

And our research shows that this is exactly what is happening.

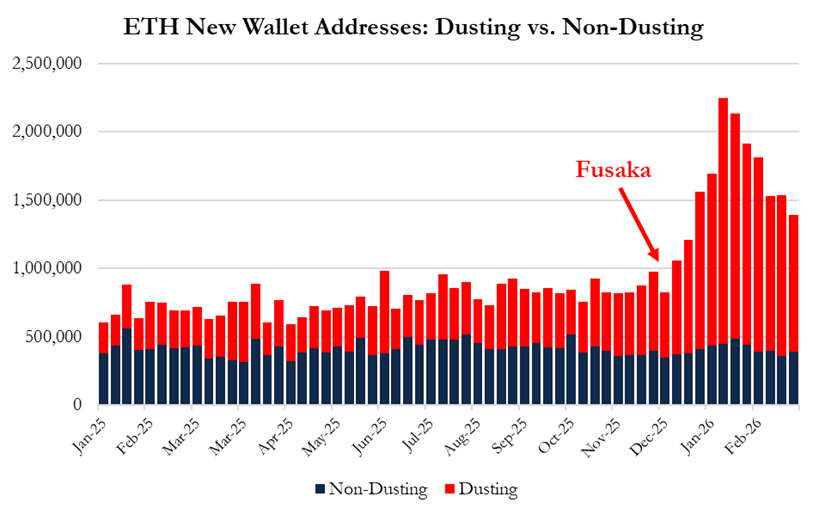

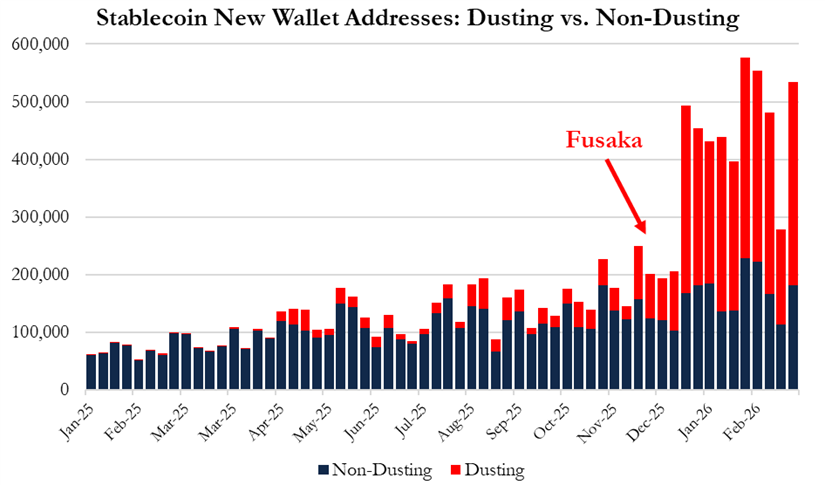

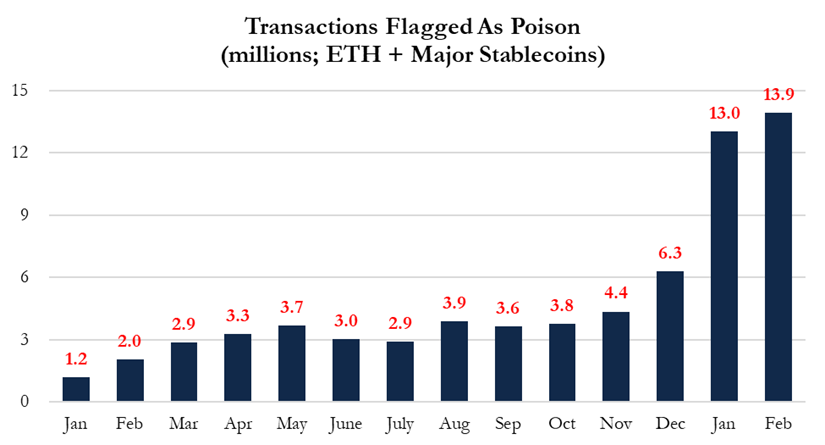

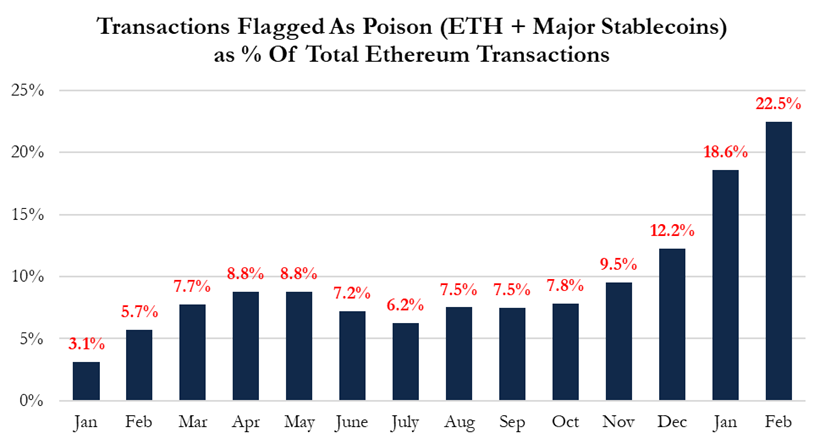

We conducted a comprehensive analysis of on-chain data from January 2025 to February 2026, and the results show that what Lee calls "institutional adoption driving Ethereum's activity growth" can actually be explained by a large number of low-value address poisoning and wallet dusting behaviors. These behaviors were triggered by the excess block space after the Fusaka upgrade.

After the Fusaka upgrade:

- 95% of new wallet growth comes from newly created dust addresses;

- Address poisoning attacks have increased by more than 3 times;

- Poisoning behavior explains over 50% of Ethereum's transaction growth;

- Poisoning transactions now account for 22.5% of all Ethereum transactions;

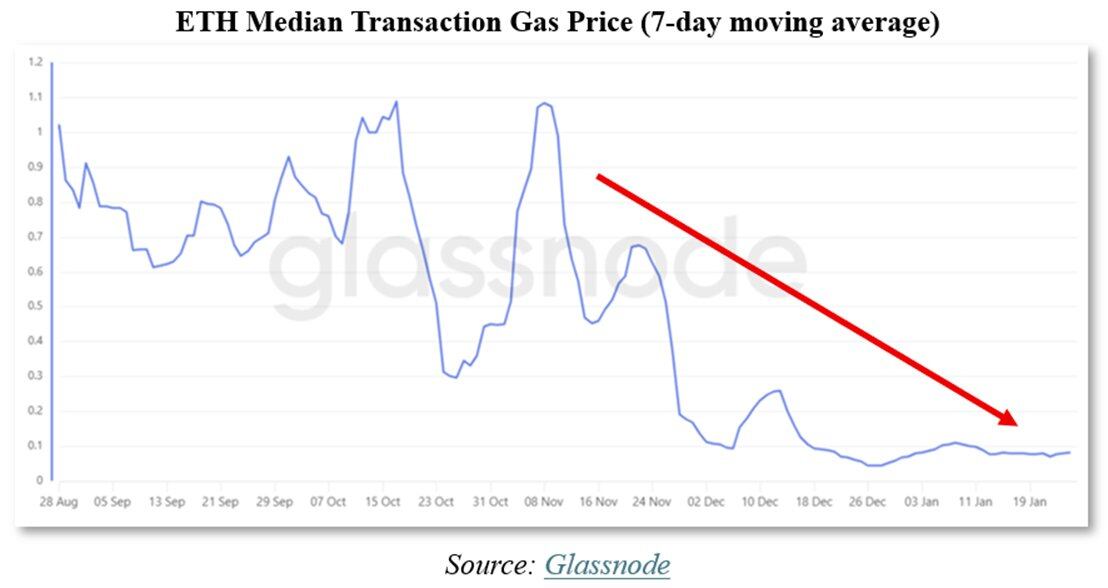

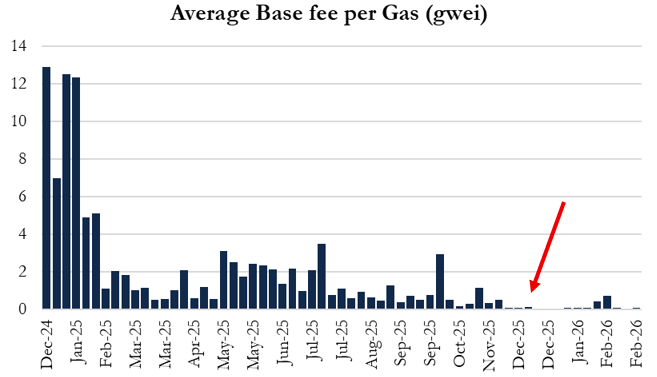

The Fusaka upgrade increased the gas limit from 45M to 60M, aiming to expand Ethereum Layer1 capacity. Vitalik and the protocol team previously predicted gas fees would drop by 10%–30%, but the reality is that gas fees dropped by about 90%.

Vitalik and the validators made a serious miscalculation in Layer1 demand elasticity. They used outdated mathematical models (based on assumptions from before EIP-1559 and before Layer2 emerged), thereby overestimating Layer1 demand by 3 to 9 times. This is also why we believe Vitalik is selling large amounts of ETH. On January 30, Vitalik announced in advance that he would sell 16,384 ETH to fund the Ethereum Foundation's "austerity period," but since then, he has sold over 19,300 ETH and is still selling.

Vitalik understands something Tom Lee does not — ETH's token economic model has been broken.

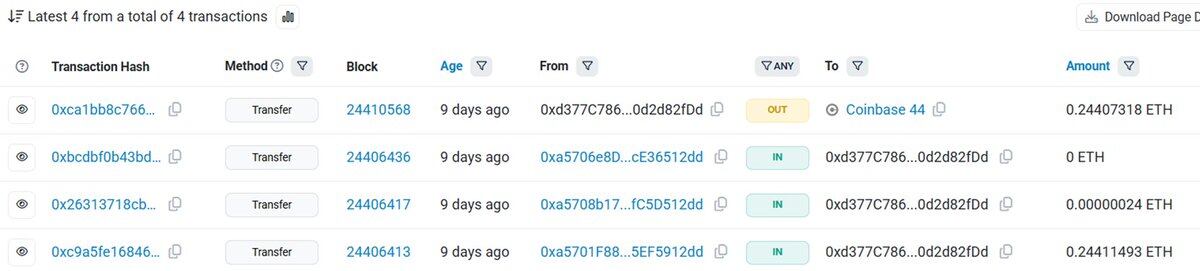

We personally documented Ethereum network address poisoning. We created two new addresses and transferred between them. Within 5 minutes, we were subjected to an address poisoning attack. We encourage readers to verify this phenomenon themselves. Currently, the rate of losses due to poisoning attacks is 8 times higher than before the Fusaka upgrade.

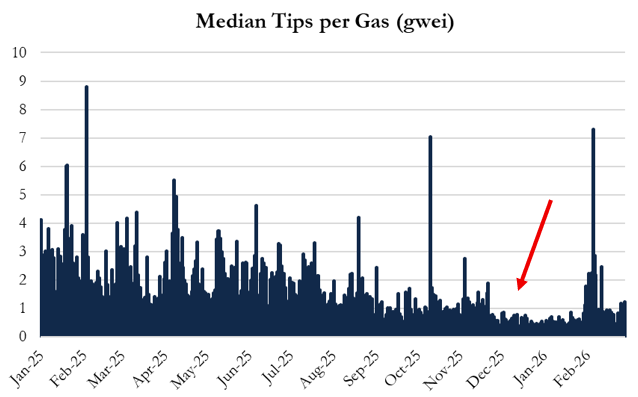

Furthermore, the increase in the gas limit has hit Ethereum's validators群体, as validators now see a 40%–50% decline in tip income per unit of gas. Falling yields will weaken staking demand and high-value transaction activity, further undermining institutional adoption. This flywheel has now started to reverse.

Meanwhile, Ethereum continues to lose market share to Solana and its own Layer2 networks.

- Solana developer count grew 29% in 2025;

- Ethereum developer growth was only 6%;

- Talent is leaving the Ethereum ecosystem;

- Institutions like Visa and Citigroup have chosen Solana for DeFi applications;

- Solana DEX trading volume is already more than double that of Ethereum.

In the dot-com bubble era, Netscape and Nokia dominated the market for over 10 years, but the real winners were Google and Apple. We believe Ethereum's situation is similar — we think Ethereum's token economic model has collapsed, Tom Lee is trapped in his own position, and ETH's price will continue to fall.