Original | Odaily Planet Daily (@OdailyChina)

Author | Azuma (@azuma_eth)

Who knows the current state of the cryptocurrency primary market best? Naturally, it's the VCs still active in the market.

In recent days, several investors from Pantera Capital, Crucible Capital, Blockworks, and Varys Capital engaged in a small-scale discussion on X about the industry's primary market situation. Although there were some differences in their views on the market's current state, their debate might help us understand the primary market's condition a step further.

Counterintuitive Reality: VCs Aren't Short on Money, But There Aren't Many Worthwhile Investment Opportunities

On the evening of April 20, Crucible Capital Partner and GP Meltem Demirors published a short post on X explaining why the number of financing deals in the cryptocurrency industry is significantly decreasing.

Demirors believes that, overall, the "supply side" of early-stage founders and projects in the cryptocurrency industry is not as large as in other high-growth industries. Over the past 4 years, this gap has become increasingly apparent, which is why this VC has started to shift its attention outside the cryptocurrency market.

The venture capital business in the cryptocurrency market has been developing for 10 years, but the truly proven directions that can generate "VC-level returns" are actually just a few — stablecoins/payments, exchanges, and financial products. For VC investors and frontline founders, the industry now has fewer blockbusters, longer cycles, so the requirements for industry insight, resilience, and long-termism are higher, which is why the barrier from seed round to Series A is also increasing.

Although there are still some "era-defining" founders building category-defining companies (the VC's job is to find them and win the opportunity to invest in them), the reality is that there is a clear gap between "the stories founders are telling" and "what VCs can reasonably invest in."

After Demirors' short post was published, it sparked discussion among many VC peers on the topic.

Several investors replied below agreeing with Demirors' view. Among them, Blockworks Co-founder Mippo followed up summarizing, agreeing with Demirors, the current problem in the primary market is the insufficient number of excellent founders and projects; actually, the VC side has plenty of funds to invest — but at the same time, early-stage VC funding is oversupplied, while funding focused on later-stage growth is still noticeably lacking.

Partial Disagreement: Where Exactly Is the Money Concentrated?

Regarding whether VC funds are concentrated in the early discovery stage or the later growth stage, Pantera Capital investor Mason Nystrom and Varys Capital Venture Lead Tom Dunleavy held completely opposite views, and the two engaged in a heated debate.

Dunleavy first stated that he disagreed with Mippo's view that "early-stage funds are oversupplied, later-stage funds are lacking": "I would take the completely opposite view. There is actually a lot of mid-to-late stage cryptocurrency VC money right now — mostly from recently raised and currently fundraising funds, like Paradigm, Multicoin, Pantera, Dragonfly, etc., and that's not even counting traditional VCs that partially dabble in the crypto market. Conversely, funding for seed and earlier stages focused on the industry is lacking...... As long as you haven't completely switched to looking at AI, there are actually many interesting projects to invest in."

But as an insider at one of the later-stage VCs listed by Dunleavy (Pantera), Nystrom strongly refuted Dunleavy's claim. He believes that VC funds in the industry are now more concentrated in the early stages, rather than Series A, Series B, or beyond.

Nystrom did the math: if a fund wants to focus on Series A or Series B financing, they need to invest in at least 20-25 projects, each requiring a large sum — about $15 million for Series A, about $40 million for Series B — by this calculation, a fund focused on Series A needs at least $300 million in assets under management (AUM), and a fund focused on Series B needs at least $800 million. This hasn't even accounted for reserve capital, which typically requires keeping 10% - 50% cash on hand. How many funds in the industry meet this requirement?

So the reality is, there might be at least 50 funds in the industry with AUM less than $100 million, but at the same time, there might only be about 15 funds with AUM over $400 million. There are extremely few big players in the industry that can participate in Series B and beyond; there might indeed be more Series B and later-stage funding in fintech (like stablecoins), but these projects have long "graduated" into the traditional VC system and can no longer be simply considered cryptocurrency market projects.

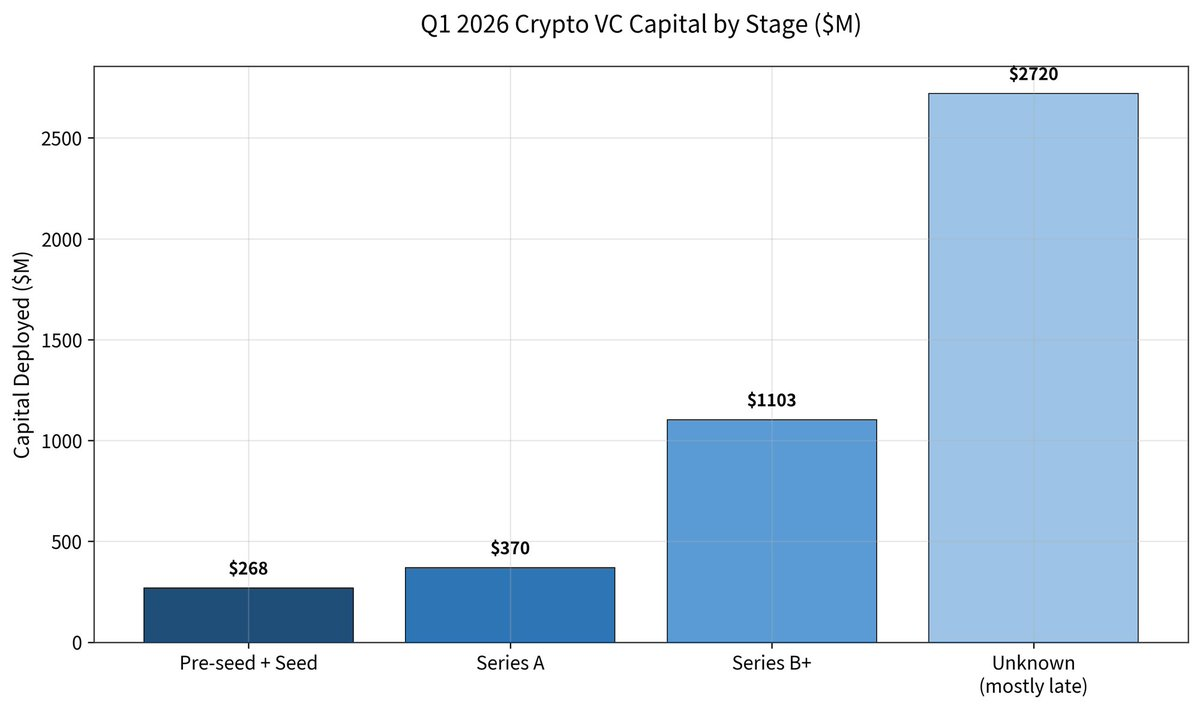

But Dunleavy was not convinced. In his response, he posted Galaxy's Q1 primary market financing report, mentioning that the number of industry-wide financing deals in Q1 fell by 49% year-on-year, but the average deal size increased by 76% (about $36 million) — the total financing amount for seed and earlier stages was only $268 million; Series A had $370 million; Series B was even higher at $1.1 billion; later stages were as high as $2.72 billion (mainly from Kalshi and Polymarket).

Dunleavy thus rebutted, saying the data proves that in 2025, over 50%+ of the industry's investment went to later stages (already a historical high), and in 2026 it has already reached 80%+.

Dunleavy finally estimated the current funding situation in the primary market — available funds for Series A and later stages are about $6 to $7 billion, concentrated in 5 to 6 large institutions; available funds for seed and earlier stages are about $1 to $2 billion, scattered across dozens of smaller, more dispersed funds.

Nystrom responded again, stating that in the data posted by Dunleavy, the vast majority of later-stage investments actually come from fintech-related "graduated" projects, but such projects have long entered the sight of traditional VCs and received investment, and should no longer be counted within the industry.

Nystrom then continued to argue based on Dunleavy's conclusion that "only 5-6 funds can invest in Series A and beyond, but dozens of funds can invest in seed stage": "This means if you can't convince 1 of those 6, you're basically out of luck; but in the early stage, as long as 1 of the dozens of funds is willing to invest, you can survive. The 'accessibility' of these two is completely unequal."

Furthermore, funds like Pantera Capital that have the ability to invest in mid-to-late stages actually also invest in seed rounds, but the reverse is not true. Additionally, more and more VCs are turning into liquidity funds, so the scale of funds in the industry that can truly invest in mid-to-late stages is much smaller than the numbers suggest.

Compared to "Is There Money", the Real Question Is "Where Is the Money, Can It Be Accessed"

In short, neither side could convince the other, but based on the direct confrontation between these two frontline investors, we got a further glimpse into the reality of the cryptocurrency primary market — "is there money" does not seem to be the core problem of the primary market; "where is the money, can it be accessed" is.

Superficially, the data shows the industry's funds are still ample, even highly concentrated in later rounds; but from actual experience, both VCs and entrepreneurs are facing a more "structurally tightened" market — early-stage funds appear dispersed but competition is fierce, mid-to-late stage funds appear ample but the threshold is extremely high. This also means the rules of the game in the primary market are changing. The era of relying on narratives, traffic, and short-cycle realization to complete the financing loop is quickly fading away; replaced by a financing environment that relies more on real business progress, long-term capabilities, and deterministic growth paths.

For VCs, this is a cycle of "making fewer moves, focusing more on judgment"; for entrepreneurs, it is a survival test that must cross a longer cycle and a higher barrier.