Written by: Andjela Radmilac

Compiled by: Saoirse, Foresight News

Key Takeaways

- The evaluation criteria for Bitcoin treasury stocks has shifted to the degree of equity dilution rather than just the sheer size of new coin purchases, as shareholder tolerance has hit bottom.

- Investors now deduct preferred stock, debt, and cash reserves to calculate the Bitcoin held per share; Metaplanet's current market cap is below the total value of its Bitcoin holdings.

- Once the valuation premium disappears, companies are left with options like stock buybacks, further dilution, or asset sales; the financing terms for new European treasury companies have not been priced by the market.

For the past two years, a simple announcement of increased Bitcoin holdings would send a company's treasury stock soaring. But now, MicroStrategy's Bitcoin-per-share yield is declining, Metaplanet's enterprise value is less than its own crypto assets, and the cost risks of financing proposals offered by new European entrants to investors still lack market pricing references.

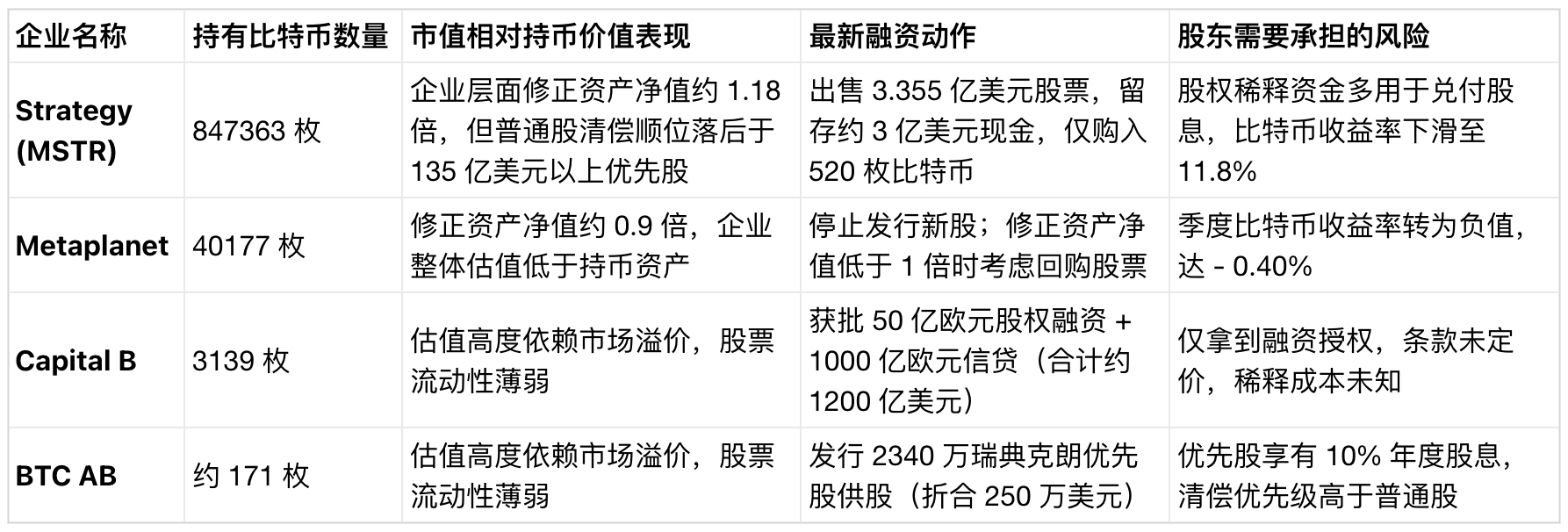

On June 22, MicroStrategy sold $335.5 million worth of common stock, retaining about $300 million as cash to boost reserves to $1.4 billion, and used the remaining funds to purchase only 520 Bitcoin.

The majority of this dilutive equity financing by the pioneer of the corporate Bitcoin treasury playbook was used to replenish the preferred stock dividend reserve; this fundraising came shortly after the company's STRC perpetual preferred shares hit an all-time low, severely damaging its core financing channel.

The company's year-to-date Bitcoin-per-share yield—a key metric CEO Michael Saylor uses to prove that each round of financing increases Bitcoin per share for common shareholders—has fallen from 13% a month ago to 11.8%, with fully diluted outstanding shares increasing to approximately 388.6 million.

This week's market performance precisely mirrors the current predicament of the entire Bitcoin treasury sector. For the past two years, any public company holding Bitcoin would see its stock price rise independently simply by announcing new purchases, raising accumulation targets, or authorizing new funding.

But now the market logic has fundamentally changed: investors scrutinize every financing deal, looking beyond the headline news of large coin purchases. They comprehensively account for equity dilution, preferred stock dividends, debt interest, and retained cash to judge whether the financing truly increases the Bitcoin share in each common shareholder's hands, or merely expands the company's total holdings while diluting existing shareholder equity.

The core of the sector's first development phase was "asset accumulation," while the new phase we are in now centers on "equity attribution accounting": after deducting all priority costs from various financing tiers, how much Bitcoin do common shareholders actually get.

The Market No Longer Provides a Blank Check

A key indicator of this sectoral shift is the contraction of the modified Net Asset Value (mNAV), which equals a treasury company's total market capitalization divided by the total value of its Bitcoin holdings. When the stock market cap is higher than the Bitcoin value, the company can issue new shares within the valuation premium range, buy Bitcoin, and simultaneously increase the Bitcoin amount corresponding to each share held by existing shareholders.

But once the premium disappears, trouble follows: the same share issuance and coin purchase operations transfer company value to new investors, harming the interests of existing shareholders.

Metaplanet, the largest corporate Bitcoin holder in Asia, holds a total of 40,177 Bitcoin, valued at approximately $2.4 billion, but its enterprise value is already below that figure, with an mNAV of only 0.9x. This means the market values the entire company at less than the Bitcoin sitting on its books. The company's stock price has plunged about 47% year-to-date, with its quarterly Bitcoin-per-share yield turning negative, falling to -0.40%.

CEO Simon Gerovich was blunt about it: once the mNAV falls below 1.0x, the company will focus on repurchasing its own stock; the current company policy also clearly states that new common shares will not be issued at this valuation level. The company previously accumulated large amounts of Bitcoin at high price ranges, currently sitting on a paper loss of about $1.6 billion. CryptoSlate has also tracked how the company is navigating this sharp asset revaluation amidst stagnant peer development.

A capital constraint loop is now playing out on balance sheets: shareholders are no longer willing to pay a valuation premium, completely halting financing models that can increase shareholder equity; as long as the valuation discount persists, companies cannot expand their Bitcoin holdings, and management can only protect the Bitcoin-per-share value by reducing the number of outstanding shares.

MicroStrategy still leads by a wide margin in terms of scale. As of June 21, the company holds 847,363 Bitcoin, accounting for over 60% of all Bitcoin on listed companies' balance sheets globally; but before common shareholders receive any asset distribution, the company has over $13.5 billion in preferred stock with priority claims.

This year, the company has purchased approximately 174,300 Bitcoin, with Bitwise estimating that 55% of the purchase funds came from STRC preferred stock issuance. As this financing channel came under pressure, the company chose to dilute common shareholder equity to ensure preferred stock dividend payments. CryptoSlate has also published views suggesting that while MicroStrategy continues to buy Bitcoin aggressively, the Bitcoin share ultimately accruing to MSTR common shareholders is continuously shrinking.

Now, all formal Bitcoin treasury companies use fully diluted Bitcoin-per-share as a core performance metric. Objectively speaking, the growth of Bitcoin on a company's books and the increase in Bitcoin per individual shareholder are no longer synchronized.

European Market Falls into the Same Trap

In Europe, the French listed company Capital B (formerly The Blockchain Group) just received shareholder approval on June 17 to raise up to €5 billion and issue credit facilities capped at €100 billion, with an overall approved financing limit equivalent to about $120 billion. This massive financing is backed by only its current holdings of 3,139 Bitcoin (worth about $200 million).

All of the company's operational moves revolve around "increasing fully diluted Bitcoin per share," and it has disclosed plans to the market: reaching 15,000 coins by the end of 2027, with a long-term vision to hold 1% of the global Bitcoin supply.

The Swedish company BTC AB operates on a smaller, faster-paced version of the same model. The company initiated a rights issue, planning to issue up to 195,078 Class A preferred shares at 120 Swedish Krona per share, aiming to raise 23.4 million SEK (approximately $2.5 million).

These preferred shares pay a fixed annual dividend of 10%, settled monthly, with the company holding only about 171 Bitcoin as the underlying asset. The subscription window will close on June 30, and subscription intentions have already covered 27% of the total issuance. Despite its small size, there is still significant market demand for subscription.

Comparing these two European companies reveals they are making identical demands of investors: asking the market to absorb increasingly complex capital instruments, hoping that the subsequent Bitcoin purchases' value will cover all costs arising from equity dilution, preferred stock dividends, and redemption clauses. The market's focus has shifted from "which company is hoarding more coins" to "who bears the financing costs and whether the financing terms are reasonable."

The current situations of the four major companies in the sector are vastly different. A year ago, the market would give positive valuation feedback to any company increasing Bitcoin holdings; now investors price each company's stock based on its specific financing terms.

Even after accounting for preferred stock and debt, MicroStrategy still maintains a valuation premium, but the actual Bitcoin-per-share for common shareholders has shrunk; Metaplanet's market cap is completely below its own Bitcoin value; the two European companies are demanding huge capital support from the market before even finalizing their financing costs.

A core catalyst for this shift in market logic is the proliferation of spot Bitcoin ETFs. ETFs provide investors with a clean, low-cost, direct channel to hold Bitcoin; tens of billions of dollars can flow out of US spot ETFs in a single six-week period. Investors can trade Bitcoin directly with one click. Treasury companies, as leveraged, equity-diluting holding vehicles, must now provide a compelling reason to hold them.

Previously, these treasury stocks had scarcity value, serving as a mainstream way for the secondary market to gain indirect exposure to Bitcoin. But now, that scarcity has completely vanished. Companies must justify their value with additional advantages like leveraged returns, stable dividends, or efficient capital market operations. If a company can only offer Bitcoin exposure with dilution costs attached, its stock price will remain at a discount for the long term.

However, this series of changes does not directly equate to a bearish signal for Bitcoin. Investors actively penalizing reckless financing will force the entire sector to optimize capital allocation, improve information disclosure, and adopt more truthful per-share asset accounting methods. CryptoSlate's previous reports have also suggested these treasury companies have a dual impact on the industry: healthy financing models benefit Bitcoin, while aggressive financing amplifies market volatility.

Companies that can continuously issue equity within the Net Asset Value premium range while simultaneously increasing Bitcoin-per-share will retain market credibility and smoothly continue accumulating Bitcoin; weaker companies will face valuation reassessments, or even completely lose access to new financing channels.

The real risk in the sector lies in a broken financing loop: once treasury companies cannot issue stock above their Net Asset Value, they lose their path to continuously purchasing Bitcoin; meanwhile, companies must continue paying preferred stock dividends and debt interest, leaving only highly detrimental options: further diluting shareholders despite the discount, lending out Bitcoin to earn interest, or directly selling their held crypto assets.

CryptoSlate has also reported that MicroStrategy is exploring Bitcoin lending operations, a pivot that would transform the original Bitcoin-holding company into a credit business, introducing an entirely new category of risk. Once the valuation premium disappears, the original Bitcoin accumulation machine turns into a balance sheet conundrum burdened with ongoing dividend liabilities.

The winners of the sector's first phase stood out by accumulating Bitcoin faster and in larger quantities than their peers. In the next phase, companies that can stand firm will have their core competitiveness in proving that after each round of financing, the Bitcoin share in the hands of common shareholders increases rather than decreases. The market has finally started doing the math precisely.