As the crypto market braces for the passage of the CLARITY Act, a new rule under the GENIUS Act has come to the limelight.

In a joint proposal, the U.S. Department of the Treasury’s Financial Crimes Enforcement Network (FinCEN) and the Office of Foreign Assets Control (OFAC) brought a rule that treats payment stablecoin issuers similarly to banks.

This was in the context of money laundering, terrorist financing, and sanction evasion.

For perspective, this proposed rule is part of the GENIUS Act, which was signed into law by U.S. President Donald Trump in July 2025.

What prompted the Treasury to come up with such a proposal?

Regulators believe payment stablecoin issuers can evolve the payment system in the U.S. However, given the scale and size of the financial system of the country, illicit actors find it easy to “jeopardize U.S. national security.”

Therefore, to combat such illicit financial risks, the rule ensures that permitted payment stablecoin issuers (PPSIs) are treated like financial institutions for purposes of the Bank Secrecy Act (BSA).

Needless to say, this would automatically impose the anti-money laundering (AML) obligations, which were earlier just for BSA.

Additionally, the proposal is also designed to be “fit for purpose, assist law enforcement, and minimize unnecessary burden.” That being said, all this is a part of the broader plan to “modernize BSA requirements” with consistent efforts from FinCEN.

Treasury Scott Bessent weighs in

Applauding such changes made under the U.S. President Donald Trump’s administration, Treasury Secretary Scott Bessent noted,

President Trump is strengthening American leadership in digital financial technology.

He further added,

This proposal will protect the U.S. financial system from national security threats without hindering American companies’ ability to forge ahead in the payment stablecoin ecosystem.

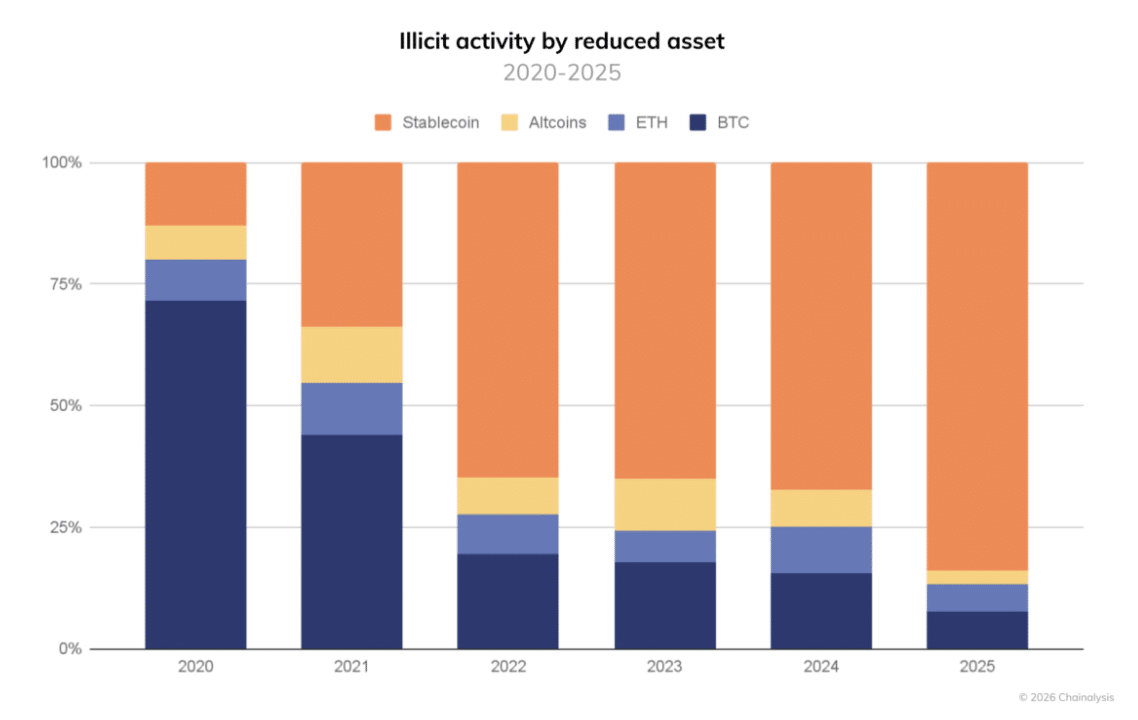

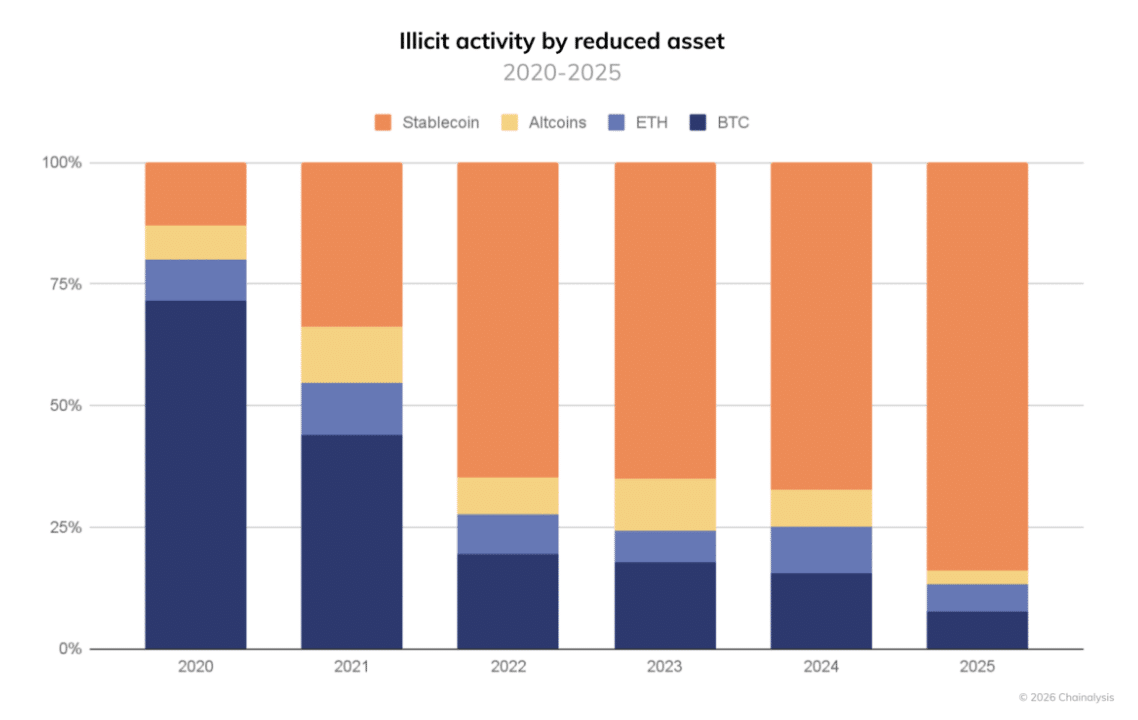

Illicit activities that targeted stablecoin in 2025 and before

This comes as the stablecoins had already been a center of target for many years. For instance, in June 2025, U.S. federal authorities seized $225.3 million worth of Tether’s USDT linked to the aforementioned scams.

Additionally, in July 2025, approximately $2 million worth of digital assets was unsealed by the DOJ, linked to a Palestine-based money exchange business. In November 2024, too, $5.5 million in stablecoins were seized from a drug trafficking operation.

Chainalysis’s recent report further confirmed these metrics, highlighting how in 2025 stablecoins accounted for “84% of all illicit transaction volume.”

Final Summary

- The joint efforts to bring in a proposed rule to address illicit activities in the stablecoin market underline the importance of the GENIUS Act passed in July 2025.

- With millions being seized and confiscated by the DOJ, this was an alarming rule that should be passed for better crypto innovation in the U.S.