Author: Claude, Deep Tide TechFlow

Deep Tide Guide: The S&P 500's CAPE ratio hit 39, the highest level since the 2000 dot-com bubble; the "Buffett Indicator" broke through 230% to set a new historical record; the top ten constituents account for over 35% of the index weight, with concentration reaching a modern market peak. Multiple valuation indicators are simultaneously signaling overheating, but Wall Street's judgment on this shows a serious divergence: one side believes AI profit growth supports the premium, while the other believes this is precisely the classic feature of a bubble top.

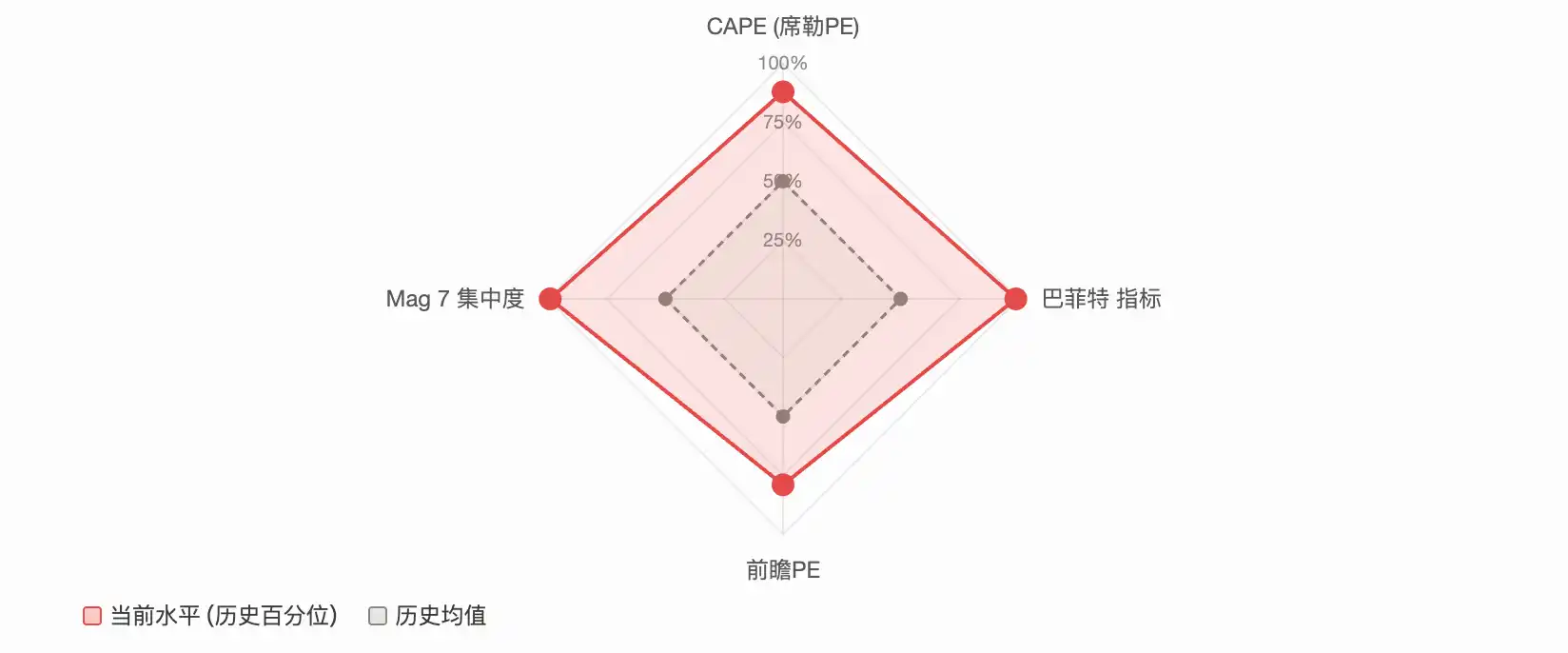

The S&P 500 is in a rare state: almost all mainstream valuation indicators are simultaneously signaling a warning.

CAPE (Shiller P/E) is approaching 40, the highest level since the internet bubble; the "Buffett Indicator" (Market Cap/GDP ratio) broke through 230%, refreshing the historical record; the top ten constituents account for over 35% of the index weight, with market concentration in an unprecedented range in modern financial history. A post on the Reddit community r/stocks characterized the current market as the "most overextended state in history," sparking over 2,100 upvotes and 640 comments. The discussion focused on a core question:

Is this a signal of a bull market top, or the beginning of an AI-driven "new paradigm"?

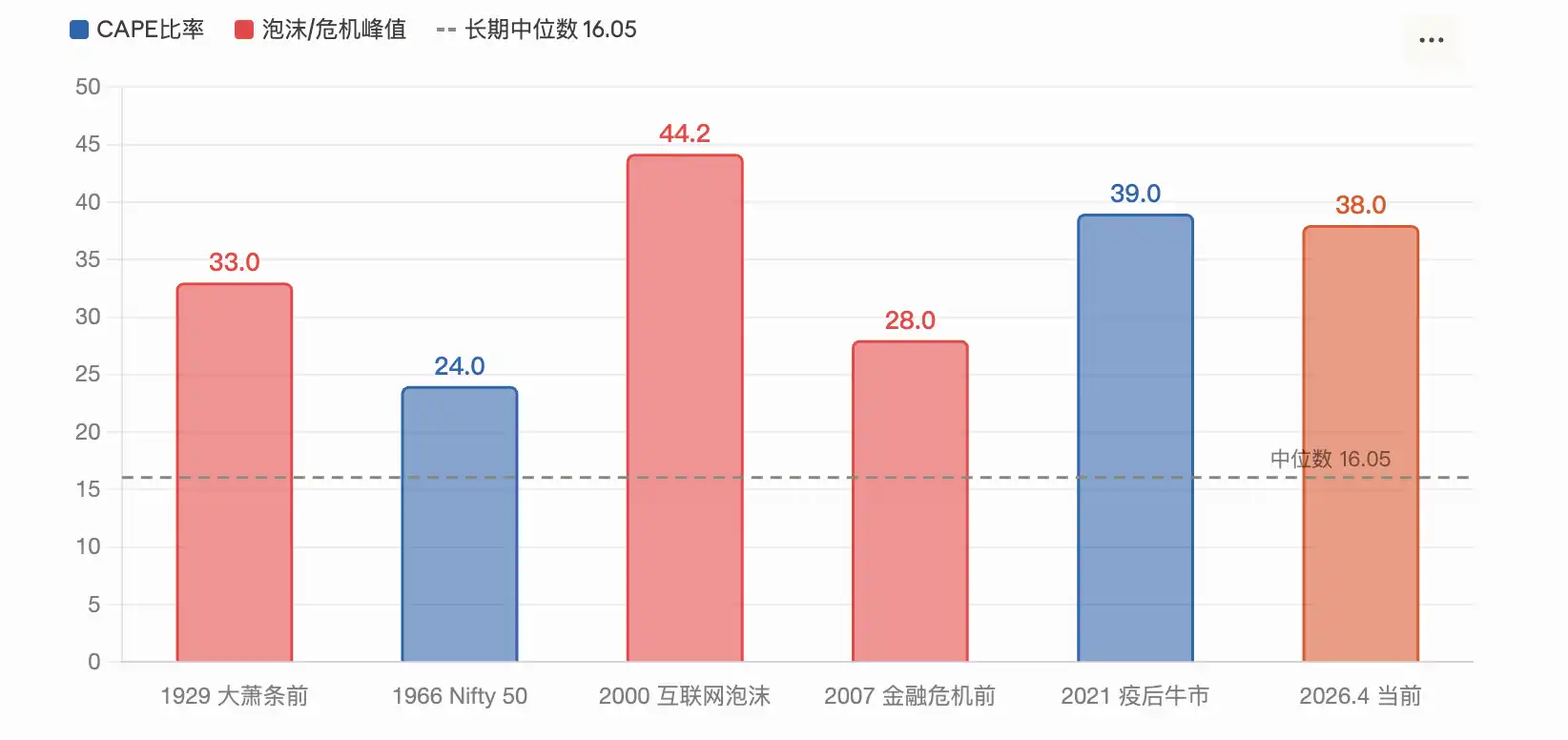

CAPE Ratio Touches 39, Second Only to the 2000 Internet Bubble Peak

The Shiller P/E ratio (CAPE) is a valuation metric developed by Nobel laureate economist Robert Shiller. It calculates the price-to-earnings ratio using the average inflation-adjusted earnings over the past 10 years, aiming to eliminate the interference of short-term economic cycles.

According to a Motley Fool report in March, the S&P 500's CAPE ratio touched 39.2 in February. According to GuruFocus data on April 1st, this indicator was 38.66. Both readings are at the second highest level in history, second only to the 44.2 during the peak of the 2000 internet bubble. The long-term median is only 16.05.

Historically, CAPE has reached similar highs twice: the late 1920s (followed by the Great Depression) and 2000 (after the internet bubble burst, the S&P 500 plummeted 49% in two and a half years). According to Shiller's research model, the current CAPE level corresponds to a future annualized return rate of only about 2%.

Motley Fool's analysis pointed out that Shiller himself expressed concern when CAPE exceeded 25, noting that since 1881, there have only been three periods that exceeded this level: around 1929, 1999, and 2007.

However, an IndexBox report also acknowledged that a high CAPE does not automatically mean a crash is imminent, as the market has risen over 40% since this indicator broke through 30 at the end of 2023.

"Buffett Indicator" Breaks 230%, Setting a Half-Century Record High

Buffett once called the Market Cap/GDP ratio the "best single measure of where valuations stand" in a 2001 Fortune magazine interview. He suggested at the time that 75%-90% was a reasonable range, and exceeding 120% meant the market was overvalued.

According to Advisor Perspectives data, by early 2026, this indicator once touched 230.3%, the highest level on record, about 2.09 standard deviations above the trend line, defined as "significantly overvalued." The latest reading in March fell back to 227.5%, still the second highest in history. GuruFocus推算, based on this ratio, the future annualized return of US stocks over the next 8 years is approximately -0.3%. (Note: 推算 translates to推算/calculate/project. The original Chinese used this term before the percentage.)

According to GuruFocus data on April 14th, the ratio was 219.5%. Critics point out that this indicator does not fully consider two structural changes: first, the profit margins of US companies have significantly increased compared to the historical median, and second, large US companies are generating more and more revenue from overseas (which boosts market cap but is not reflected in domestic GDP). But supporters believe that even after detrending, the current reading is still in an extreme historical range.

Market Concentration at a Modern History Peak, Mag 7 Accounts for Over 30%

Valuation is only one dimension of the problem. The structural risks of the market are equally disturbing.

According to AhaSignals data on April 13th, the top ten constituents of the S&P 500 account for 35.59% of the index weight, the top five account for 25.97%, and the "Magnificent 7" (Mag 7) account for 30.44%. The comprehensive concentration risk index (ACRI) compiled by the agency reads 81/100, at a "critical" level. According to Motley Fool data from April, the weight of the Mag 7 in the S&P 500 has risen from 12.5% in 2016 to the current 33.7%.

A CNBC report in December 2025 quoted a warning from Nick Ryder, CIO of Kathmere Capital: investors are still overly concentrated in the Mag 7, and he recommended充分分散配置 beyond US large-cap growth stocks. (Note: 充分分散配置 translates to fully diversify allocations/portfolio.) Ed Yardeni, president of Yardeni Research, suggested around the same time that investors underweight the Mag 7 and overweight the "other 493" (Impressive 493).

The actual risk brought by concentration is: when a few stocks dominate the index's movement, their decline can drag down the overall market with disproportionate force. The first quarter of 2026初步验证了这一点 (preliminarily verified this). According to a 24/7 Wall St report, Microsoft, Amazon, and Nvidia fell about 20%, 9%, and 6% year-to-date respectively, dragging the market-cap-weighted S&P 500 down nearly 4%, while the equal-weight S&P 500 (RSP) closed slightly positive during the same period.

Two Camps in Confrontation: "History Repeats" or "This Time is Different"

Faced with this data, Wall Street's judgment shows sharp divergence.

The core argument of the bearish camp is mean reversion of valuations. GMO co-founder Jeremy Grantham explicitly characterized the current market as a large AI-driven bubble in his latest research. He pointed out that the actual revenue from current AI investment is far less than the scale of capital expenditure, with OpenAI predicting its own 2026 operating loss will reach $17 billion and expand to $35 billion in 2027. GMO believes that the classic signals of a bubble top (speculative stock崩溃/collapse, significant outperformance by quality stocks) have not yet fully appeared, but this only means the bubble has not yet peaked, not that it doesn't exist.

IO Fund's cycle analysis also tends to be cautious. The institution's report pointed out that 2026 is simultaneously at the intersection window of the Gann 60-year major cycle and the 4-year presidential cycle, and each stock in the Mag 7 peaked between July 2025 and February 2026, with core components silently falling back while the index made its final new highs, which is a "classic warning sign of the late bull market."

The bullish camp emphasizes profit fundamentals. According to FactSet data from April, the S&P 500's forward 12-month P/E ratio is 20.4 times, although higher than the 10-year average of 18.9 times, it has fallen back from 22 times at the end of 2025. Analysts predict the S&P 500's full-year 2026 profit growth to be 17.6%. If this expectation is realized, the high valuation can be digested to some extent.

The judgment of Jurrien Timmer, Director of Global Macro at Fidelity, is relatively moderate: since the Iran conflict, the maximum drawdown of the S&P 500 has been less than 10%, a decline that historically occurs on average once every year. Profit expectations are still growing at an annualized rate of 17%, and have not yet been substantially affected by geopolitical headlines.

Morgan Stanley's investment management team also pointed out in its 2026 outlook that most bull markets last 5 to 7 years, and bull markets entering their fourth year have historically recorded positive returns. The bank's non-US equity allocation ratio has risen to a historical high.

BlackRock stated that the gains in tech stocks in 2025 were mainly driven by profit growth rather than valuation expansion, and the current valuation is reasonable based on growth expectations.

Overlaid with Geopolitical Shock: Iran War and Stagflation Risks

Beyond the valuation debate, the macro environment adds additional uncertainty.

The Iran conflict pushed oil prices above $100 per barrel, and the S&P 500 once fell below its 200-day moving average in March. According to a FinancialContent report, the Fed's March meeting maintained a "hawkish hold," and the updated dot plot only anticipated one more rate cut for the remainder of 2026. UBS, in a report on March 17, characterized the recent volatility as a "necessary reset of high valuations" rather than the beginning of a bear market, maintaining a year-end target of 7700 points.

Goldman Sachs has raised the probability of a recession in the next 12 months to about 30%. This resonates with the warning from valuation indicators: if an economic recession coincides with high valuations, the S&P 500's historical average peak-to-trough decline is 32%. But if profits continue to grow (FactSet consensus expectation is 17%), significant corrections have historically often been limited in幅度/magnitude and recovered from quickly.

For investors, the contradiction at the signal level is already very clear. Long-term valuation indicators are almost all flashing red, but short-to-medium-term profit data remains strong. The market has reached the crossroads of "valuations say no" and "profits say yes." The outcome depends on whether AI capital expenditure can translate into sustained profits, and whether geopolitical shocks ultimately translate into recession.