Written by: Prathik Desai

Compiled by: Block unicorn

Preface

Happy Year of the Horse, everyone. Last week, two highly anticipated emerging financial companies released their earnings reports within 48 hours. Both companies' revenues fell short of expectations. They were immediately framed within the same narrative: the cryptocurrency market is sluggish, trading volumes are weak, and the good days are over.

But this perspective completely misses the point.

While Coinbase and Robinhood's stock prices may be closely correlated with the price of Bitcoin (BTC), their future trajectories are not determined by BTC's performance in the fourth quarter. They are gradually moving away from the narrow definition of "company fate being tightly linked to the cryptocurrency cycle."

Both companies are undergoing significant transformations—you can see it in their financial data if you know where to look—but these changes could be completely overlooked if you only focus on the complex data from the last quarter.

But it's actually not that ambiguous. Just look at the data from the past few quarters and compare it with the series of product announcements both companies have made over the past 12 months, and it becomes clear.

The long-term trends of both companies tell us their respective directions, their bets on the future of finance, and, crucially, when their paths will begin to converge.

In today's analysis, I will dissect their stories separately before explaining their commonalities and what this reveals about the broader competitive landscape they operate in.

Part 1: Coinbase - The Infrastructure Bet

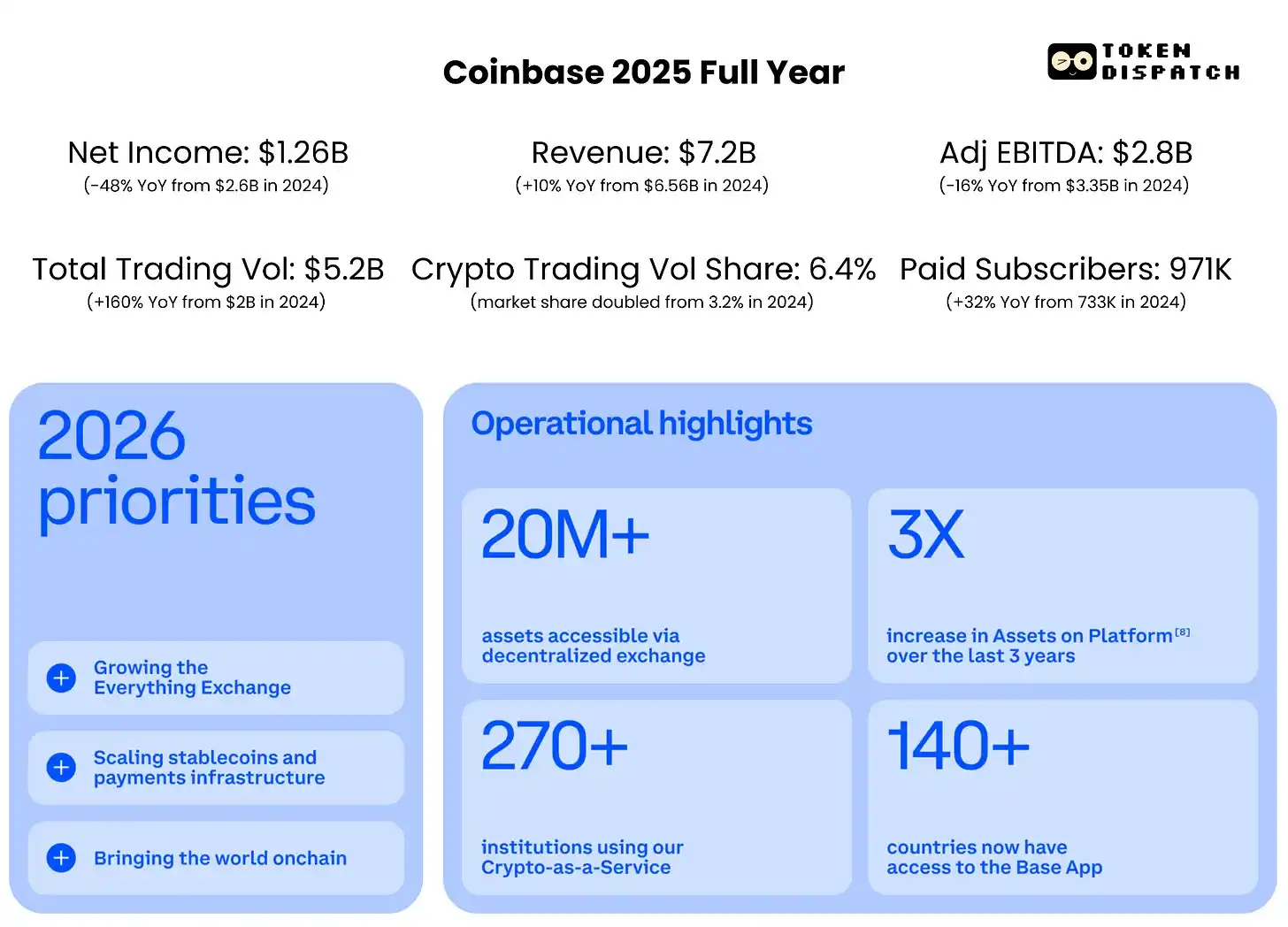

Coinbase's net loss of $667 million in Q4 2025 might make it seem like a terrible quarter. But numbers need context. The quarter also saw $718 million in unrealized losses on Coinbase's cryptocurrency holdings and a $395 million impairment loss on its investment in Circle. Excluding these non-cash paper losses, Coinbase maintained adjusted profitability for the 12th consecutive quarter.

The report showed adjusted earnings of $178 million and adjusted EBITDA of $566 million.

While this might be reassuring, there's one thing I find even more noteworthy.

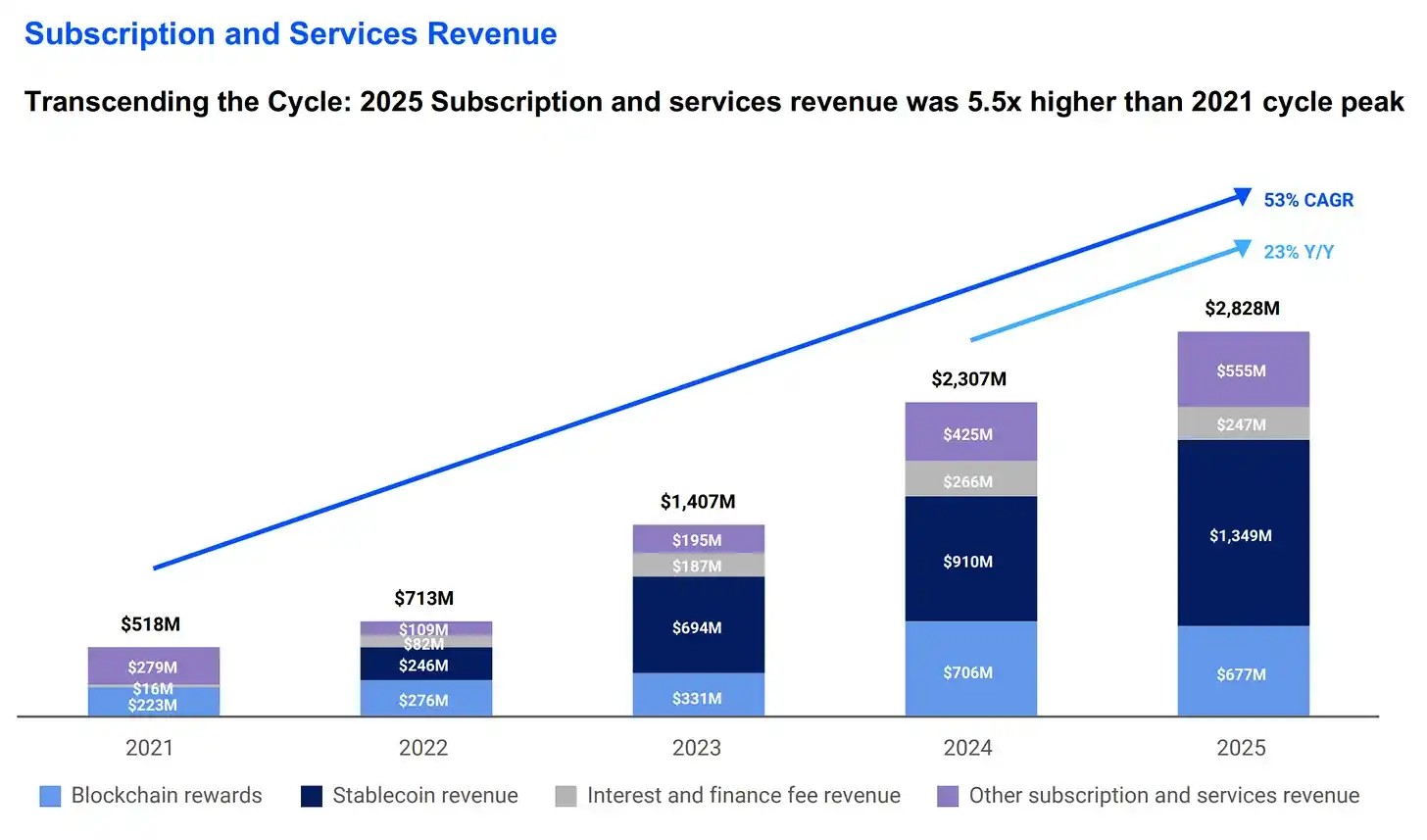

Coinbase's Subscription & Services (S&S) revenue reached $2.8 billion in 2025, a 5.5x increase from the cycle peak in 2021 and double that of 2023. This indicates Coinbase's revenue base is broadening, encompassing areas like stablecoins, custody, and blockchain rewards. In Q4, the value of USDC held in Coinbase products hit a record high of $17.8 billion, up 18% quarter-over-quarter. Currently, Coinbase holds more cryptocurrency than any other company globally, accounting for 12% of the world's crypto holdings.

However, this revenue is highly sensitive to interest rate changes. When interest rates and crypto prices fall, stablecoin yields, staking rewards, and interest income on custody balances all decrease. This is evident in the company's Q1 2026 guidance, which expects revenue from stablecoins and custody to drop to between $550 million and $630 million from $727 million in Q4.

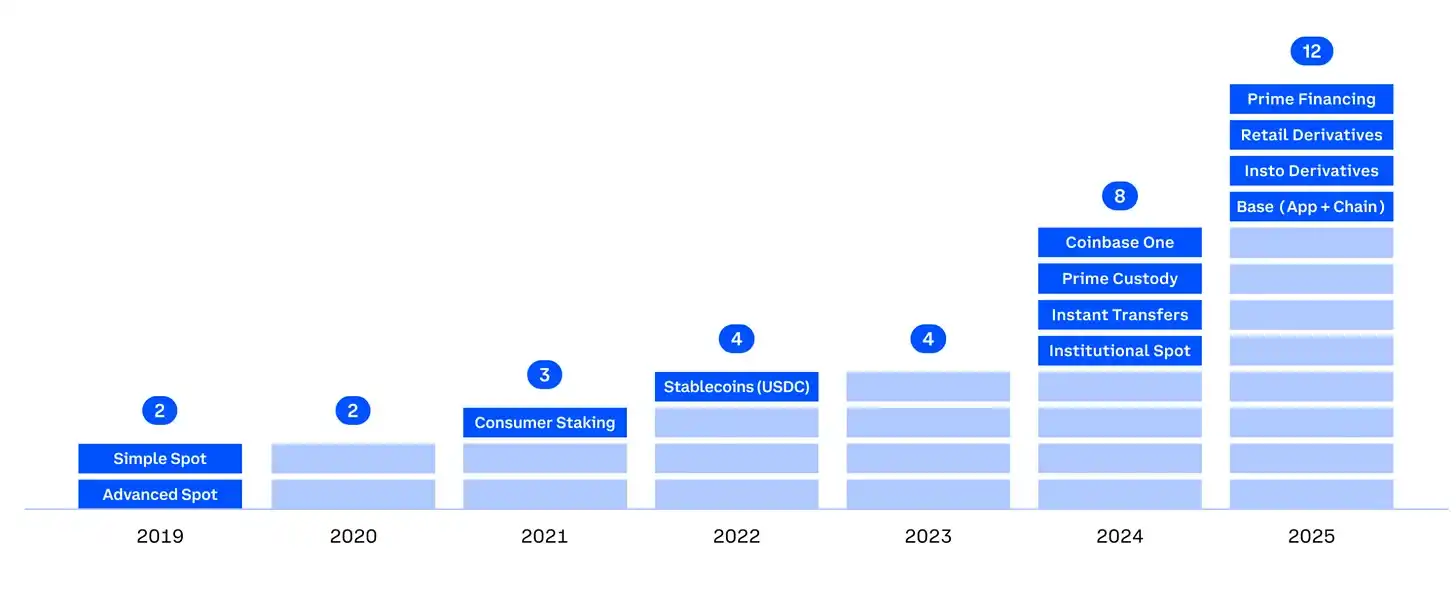

Coinbase's systematic diversification across multiple business areas, reducing its dependence on the crypto cycle, should boost investor confidence. Currently, Coinbase has 12 business units with annual revenue exceeding $100 million, 6 units over $250 million, and 2 units over $1 billion.

Coinbase's acquisition of Deribit, the largest crypto transaction ever, allows the company to capture the high-volume derivatives trading, especially during times of high spot market volatility.

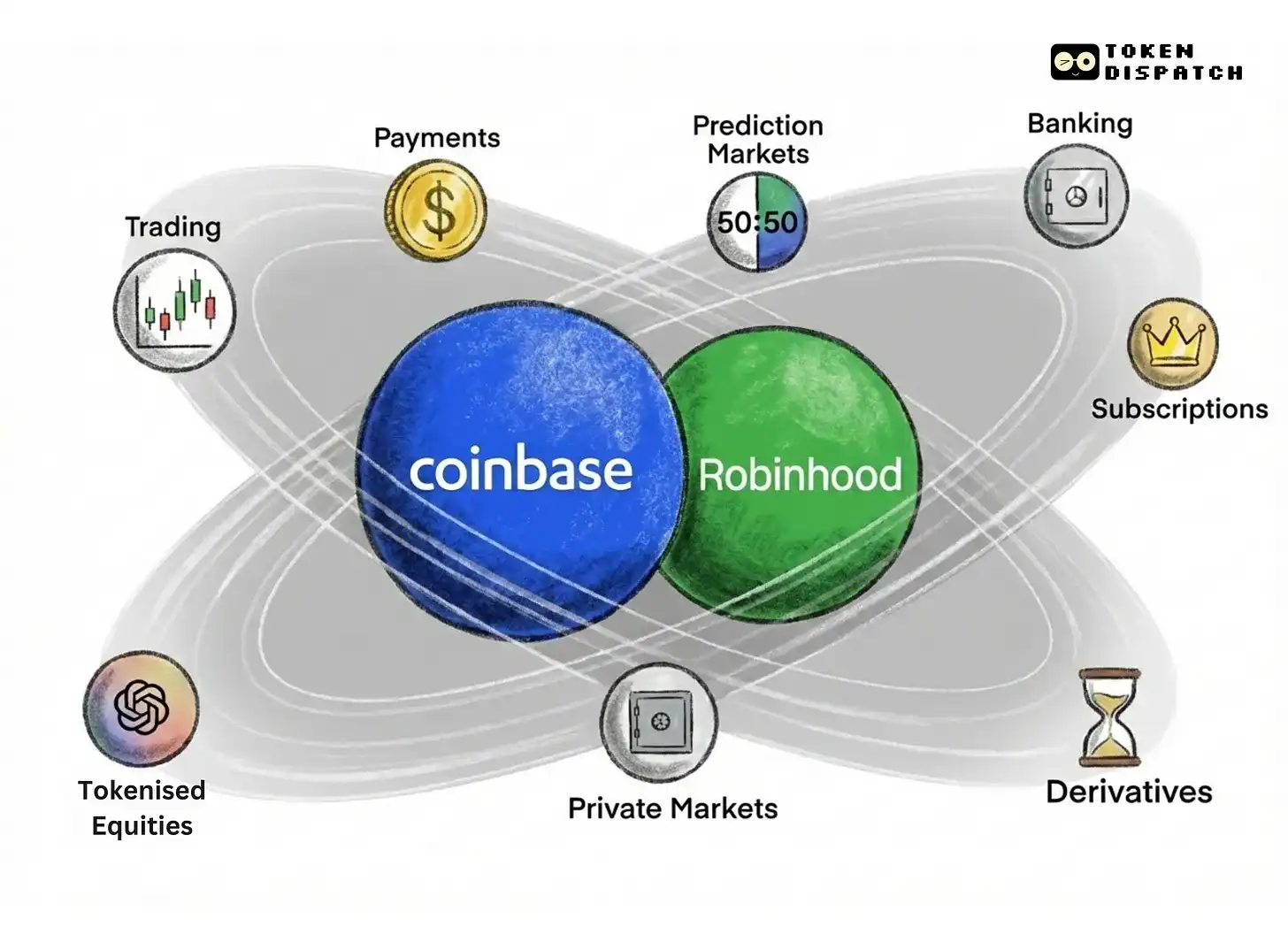

Coinbase's "Everything Exchange" vision is beginning to manifest beyond just traditional finance. Earlier this week, Armstrong revealed on Twitter that five of the world's largest Global Systemically Important Banks (G-SIBs) are collaborating with Coinbase.

J.P. Morgan has signed an agreement allowing clients to link bank accounts directly to Coinbase. BlackRock's Bitcoin ETF custody also runs on Coinbase's infrastructure. These trials indicate Coinbase's long-term goal is to become the settlement layer large institutions can plug into as finance moves on-chain.

Coinbase's recent launch of prediction markets follows the same pattern for retail customers. Launched two weeks ago, prediction markets further expand Coinbase's "everything is tradable" vision by introducing event-based trading. This creates a whole new asset class, providing Coinbase with a new revenue stream and giving customers more reason to keep assets on Coinbase rather than transfer them elsewhere.

While the short-term performance of this new business line may be modest, the strategic intent is clear. How do I know? Prediction markets have become Robinhood's fastest-growing business line, which is proof enough.

So let's look at the other side...

Part 2: Robinhood - The Consumer Deep Play

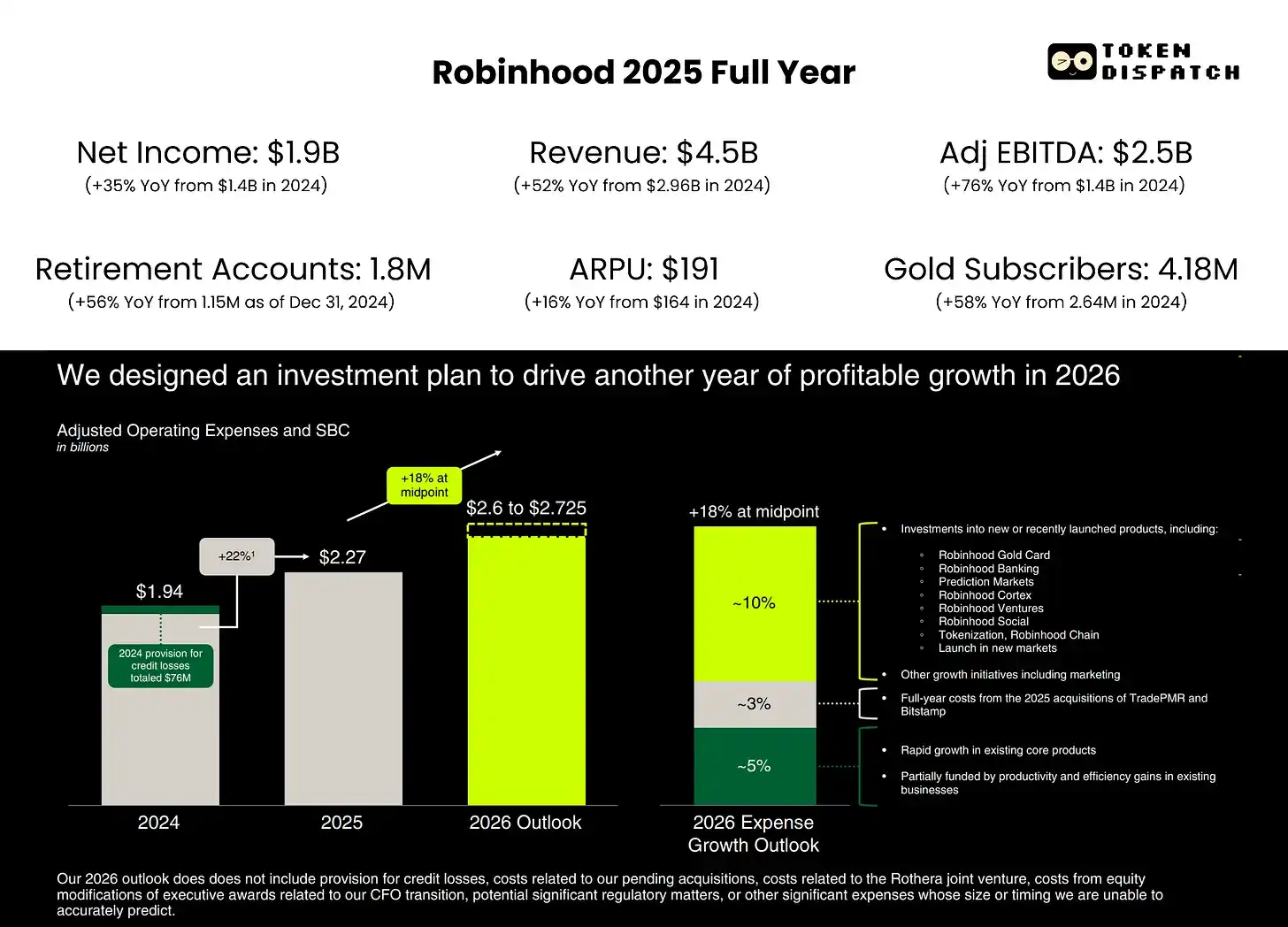

Robinhood's Q4 performance was actually quite good but was punished for the wrong reasons. Revenue missed expectations due to lower crypto trading volumes and the end of the football season, but to me, these are not the main points.

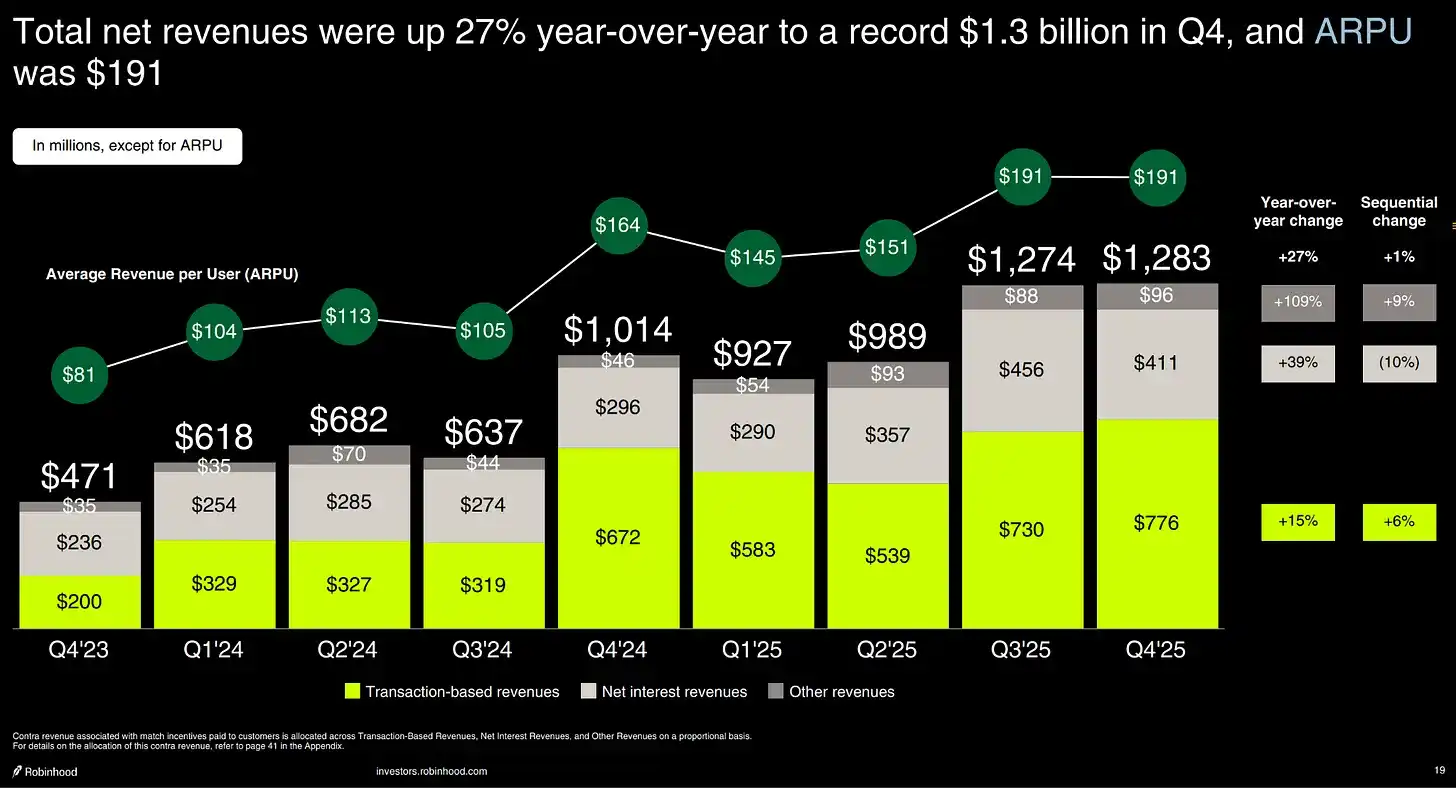

Most striking is its Average Revenue Per User (ARPU), which grew 27% year-over-year to $191, while the number of funded users grew only 7%. This indicates Robinhood is making more money from each customer without rapidly expanding its user base. This is a more diversified business model compared to its model at the time of its IPO in 2021.

Where is the ARPU growth coming from? Partly from the fastest-growing "Other Transaction Revenue," which grew 300% year-over-year to $147 million, primarily driven by prediction markets. Part of the growth also comes from options, which grew 41% to $314 million. Growth in net interest income and Gold subscriptions also contributed.

Although transaction-based crypto revenue grew over 40% year-over-year in 2025, $8 out of every $10 in Robinhood's revenue still comes from non-crypto businesses. This ensures the company is less dependent on the crypto cycle.

The $300 Million Business

The biggest indicator of Robinhood's future trajectory lies in the performance of its prediction markets. CEO Vladimir Tenev called this product line, launched less than a year ago, the fastest-growing business in Robinhood's history, which speaks volumes about its importance. The product line achieved $300 million in annualized revenue and $12 billion in contract volume in its first year. Such rapid growth clearly signals future prospects.

Robinhood is also doubled down on prediction markets by forming a joint venture with Susquehanna, Rothera LLC. Rothera LLC acquired MIAXdx in January 2026. This deal gives Robinhood its own CFTC-licensed exchange and clearinghouse. This layer helps Robinhood build the infrastructure for prediction markets, allowing it to control the pricing, contract selection, and economic models of these markets.

Although the NFL season has ended, some short-term tailwinds make Robinhood's prediction markets more resilient. In January, NBA contract volume on the platform surpassed NFL contracts. A government shutdown also caused a significant spike in volume the same week the NFL season ended. Furthermore, the FIFA World Cup is this summer, following the ongoing Winter Olympics. Beyond this, Robinhood is building out a whole new non-sports category.

The Diversification Puzzle

Beyond prediction markets and Robinhood's current profit engines (options, margin, and Gold subscriptions), other factors will boost investor confidence. $HOOD is also building the next layer of distribution through private markets, family investing, and banking.

Robinhood Banking officially launched a few months ago, rolling out to its first customers. As of the end of January, it had 25,000 paying customers with total deposits of $400 million. Over half of these customers have enabled direct deposit, which Tenev sees as the most encouraging signal. This means these customers are moving their financial lives into the Robinhood ecosystem, not just experimenting. But $400 million in deposits is still a drop in the bucket for a platform with a market cap of $32.4 billion. Banking is a long game, and Robinhood must be prepared for the challenge.

While the world is busy building prediction markets, I believe private markets could be Robinhood's ace in the sleeve, an area few competitors are tackling. Tenev also believes private markets could "grow larger than prediction markets." Robinhood Ventures, a registered fund under Robinhood aimed at giving retail investors access to invest in private companies, has not officially launched yet. But last year, European users got a taste through the controversial gift of stock tokens for OpenAI and SpaceX. Robinhood Ventures will launch in the US in 2026, and the total addressable market is huge. Tenev has repeatedly mentioned the ongoing $100 trillion intergenerational wealth transfer. If Robinhood can capture even a fraction of this as private assets shift from institutional to retail investors, it would dramatically alter its revenue mix.

The bigger challenge will be managing customer expectations by clearly delineating the lines between tokenized equity and traditional equity.

Private markets as a revenue source may start in 2026 but will likely play out over a much longer horizon.

Same Destination, Different Timelines

At first glance, Coinbase and Robinhood's paths seem截然不同 (jiéránbùtóng - completely different). Indeed, they started from two opposite ends of the finance spectrum. However, they are now converging towards the same vision: becoming a financial super app. Their recent histories confirm this.

Robinhood entered finance the traditional way: offering commission-free stock trading designed for a user base that found traditional brokers too expensive and complex. For five years, it has been building crypto-native infrastructure on top of traditional finance (TradFi). Today, it offers margin accounts, Gold subscriptions, credit cards, banking products, a derivatives exchange, prediction markets, and tokenized strategies.

Coinbase was born in crypto, providing the most trusted way to buy, store, and trade digital assets at a time when most of Wall Street shunned cryptocurrency. Over the past five years, Coinbase has expanded from its crypto-native core into consumer products already existing in traditional finance, such as stocks, subscriptions, credit cards, and now prediction markets.

Both are rapidly converging towards the middle from opposite directions, where the battle for retail finance will be fought over the next decade.

Prediction markets are currently the clearest stage for their head-to-head competition. Robinhood is ahead here, having a head start over Coinbase, which launched just two weeks ago. $HOOD also has its own exchange and clearinghouse, while $COIN is partnering with Kalshi but not exclusively.

Tokenization will be another, more complex area of competition. Coinbase sees it as an infrastructure problem, issuing tokenized stock internally and building regulatory relationships for on-chain trading of bonds and securities. Meanwhile, Robinhood sees it as a consumer access problem, enabling trading by opening up stock tokens for non-public companies. They are taking different paths to solve different aspects of the same problem.

Private markets could be a third area where these two companies meet. Coinbase enables on-chain capital formation through its acquisition of Echo, while Robinhood is taking its first steps with its Ventures arm to bring private company investing to retail users.

Both companies know the broader market will trust the one that builds the deepest financial relationship and meets the growing demand from investors. Financial services are often one of the hardest areas to gain market acceptance. People don't easily switch banks, brokers, and custodians. If one platform allows a user to manage their retirement account, card details, prediction market positions, and eventually their private equity portfolio, it becomes very difficult for another platform to take that customer away from a competitor.