Resumo

Based on the article "Truth, Bubbles, and Illusions: A Look Back at the 2025 Crypto Report Card," here is a summary of its main points:

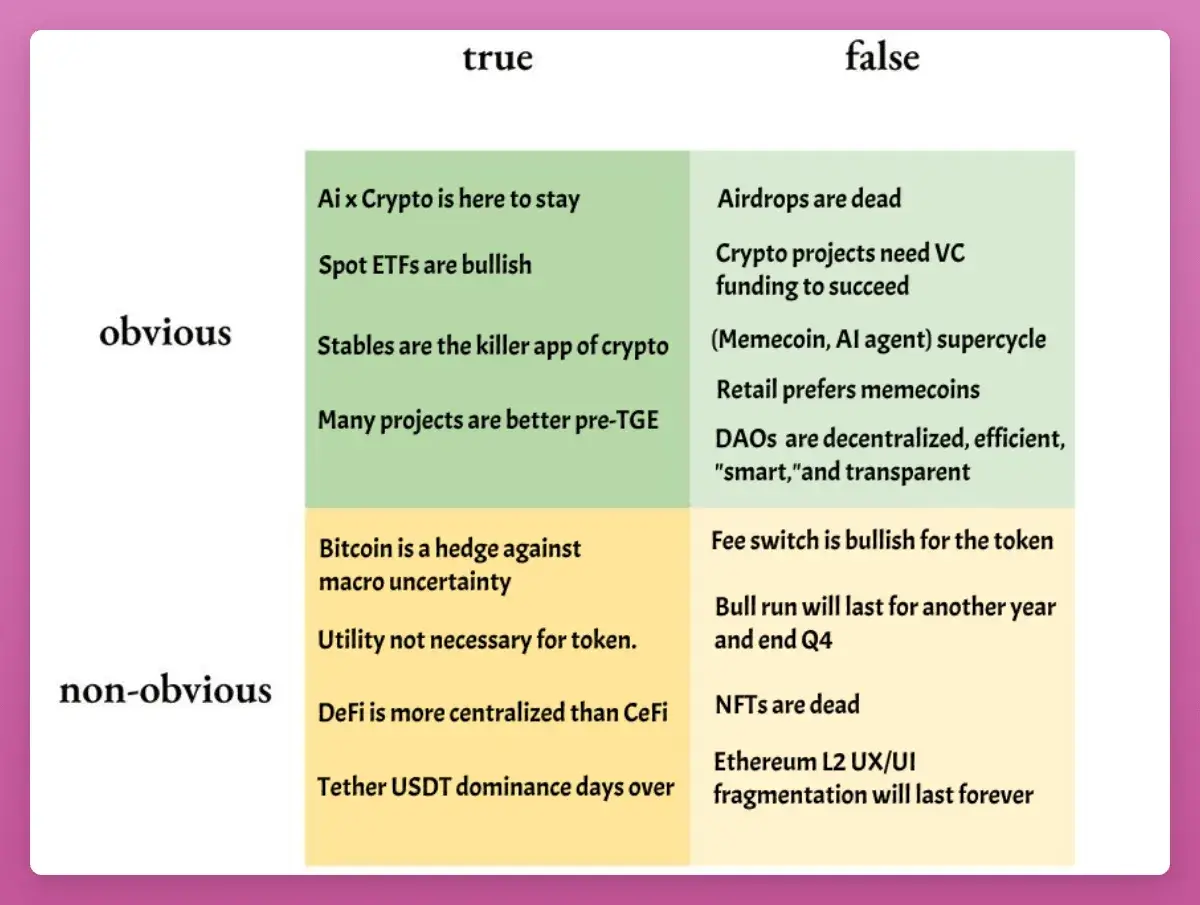

The author reflects on their 2025 predictions for the crypto market. They admit to being wrong about Bitcoin's peak in Q4, as the cycle held, and wrong about a memecoin or AI agent supercycle, as retail investors favored traditional assets like gold and AI stocks instead. The AI x Crypto narrative saw mixed results with project development but poor token performance, and NFTs were declared "dead."

Key insights from 2025 include:

1. **Bitcoin ETFs acted as a floor, not a ceiling:** Massive selling by long-term holders created a $95B supply overhang, causing BTC to underperform. However, its correlation with traditional risk assets fell, which is bullish long-term.

2. **Airdrops are not dead:** Nearly $4.5B was airdropped in 2025 (e.g., Story Protocol, Berachain). The game has shifted towards requiring more focused, high-conviction farming due to points fatigue and better Sybil detection.

3. **Fee switches set a price floor, not an engine for growth:** Token buybacks from fees establish a bottom price but don't guarantee appreciation, as seen with UNI's price action. The market treats everything as a trade.

4. **Stablecoins gained traction for payments, but "proxy trading" was difficult:** Stablecoins like USDT saw real-world adoption for payments. However, investing in related equities (e.g., Circle's IPO) proved challenging, as gains we...

Author: Ignas

Compilation: Plain Talk Blockchain

Original Title: Crypto Truth and Lies: A Review of the 2025 Report Card

A year ago, I wrote "Truth and Lies of the 2025 Crypto Market".

At that time, everyone was sharing higher Bitcoin price targets. I wanted to find a different framework to discover where the public might be wrong and to position myself differently. The goal was simple: to seek out ideas that already existed but were overlooked, disliked, or misunderstood.

Before sharing the 2026 edition, here is a clear review of what truly mattered in 2025. What we got right, what we got wrong, and what we should learn from it. If you don't examine your own thinking, you're not investing, you're guessing.

Quick Summary

-

"BTC Peaked in Q4": Most people expected this, but it seemed too good to be true. Turns out they were right, and I was wrong (and paid the price). Unless BTC skyrockets from here and breaks the 4-year cycle pattern, I'll concede this one.

-

"Retail Prefers Memecoins": The truth is, retail doesn't prefer crypto at all. They bought gold, silver, AI stocks, and anything that wasn't cryptocurrency. The supercycle for memecoins or AI Agents also did not materialize.

-

"AI x Crypto Remains Strong": Mixed results. Projects continued to deliver, the x402 standard evolved, and funding continued. But tokens failed to sustain any rallies.

-

"NFTs Are Dead": Yes.

These are easy to review in hindsight. The real insights lie in the following five larger themes.

1. Spot ETFs Are the Floor, Not the Ceiling

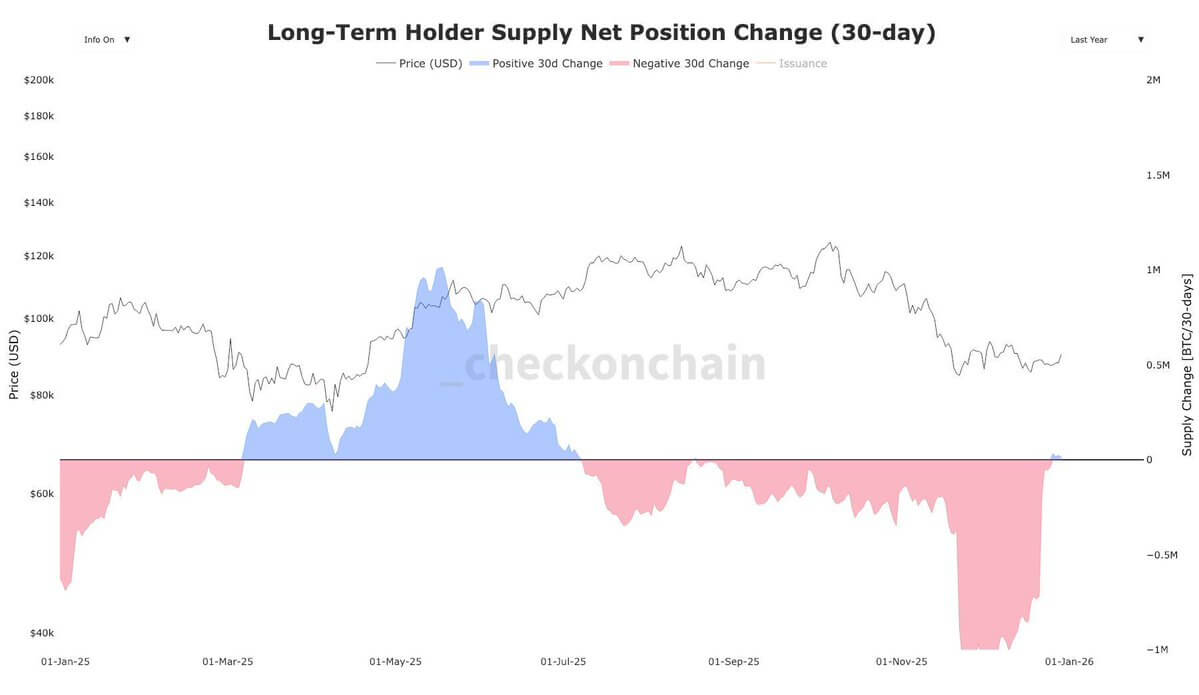

Since March 2024, long-term Bitcoin holders (OGs) have sold approximately 1.4 million BTC, worth about $121.17 billion.

Imagine the bloodbath in the crypto market without ETFs: Despite the decline in price, BTC ETF inflows remained positive ($26.9 billion).

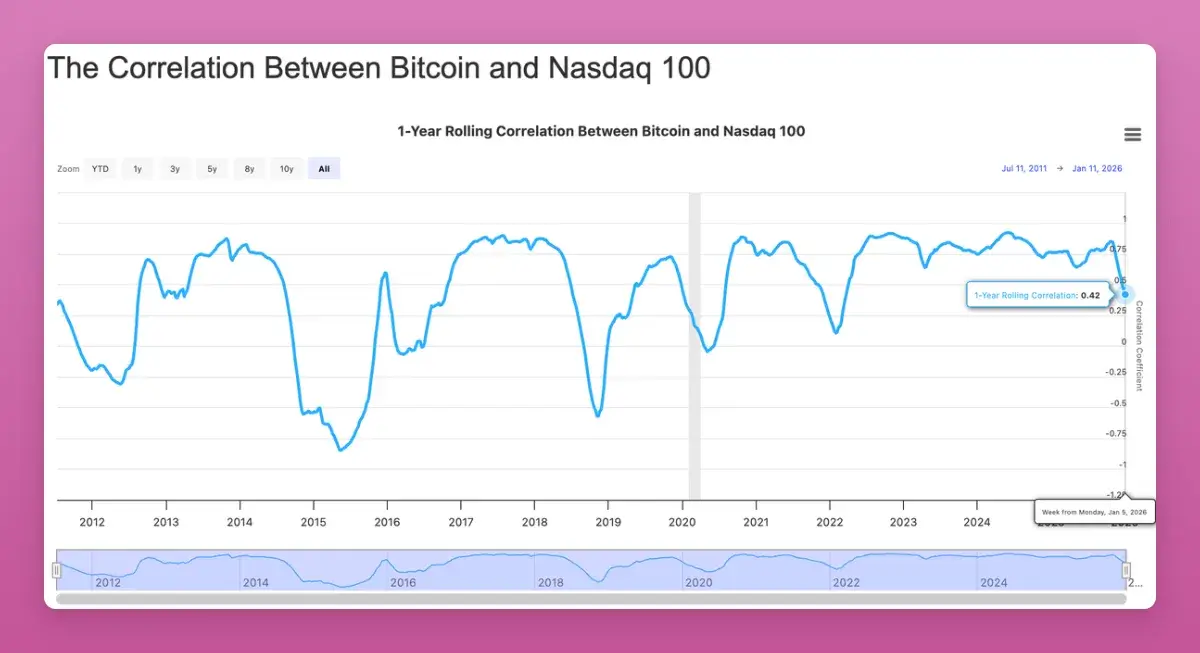

The gap of about $95 billion is precisely why BTC underperformed almost all macro assets. There's nothing wrong with BTC itself; you don't even need to dig deep into unemployment or manufacturing data to explain it—it's just the "great rotation" by whales and "4-year cycle believers".

More importantly, Bitcoin's correlation with traditional risk assets like the Nasdaq fell to its lowest since 2022 (-0.42). While everyone hoped for an upward breakout in correlation, in the long run, this is bullish as an uncorrelated portfolio asset sought by institutions.

There are signs the supply shock is over. Therefore, I dare to predict a BTC price of $174,000 for 2026 (equivalent to 10% of gold's market cap).

2. Airdrops Clearly "Did Not" Disappear

The crypto community (CT) once again claimed airdrops were dead. But in 2025, we saw nearly $4.5 billion in large airdrop distributions:

-

Story Protocol (IP): ~$1.4B

-

Berachain (BERA): ~$1.17B

-

Jupiter (JUP): ~$7.91M

-

Animecoin (ANIME): ~$7.11M

The changes are: points fatigue, stronger Sybil detection, and lower valuations. You also need to "claim and sell" to maximize returns.

2026 will be a big year for airdrops, with heavyweights like Polymarket, Metamask, Base(?) preparing to launch tokens. This is not the year to stop clicking buttons, but to stop betting blindly. Airdrop "farming" requires concentrated effort on high-conviction bets.

3. Fee Switches Are Not Price Appreciation Engines, They Are the Floor

My prediction was: Fee switches won't automatically drive token prices up. Most protocols don't generate enough revenue to support their massive market caps.

"The fee switch doesn't affect how high the token can go; it sets a 'floor price'."

Look at the projects ranked by "Holder Revenue" on DeFillama: Except for $HYPE, all high revenue-share tokens outperformed ETH (though ETH is now the benchmark everyone challenges).

The surprise was $UNI. Uniswap finally flipped the switch and even burned $100 million worth of tokens. UNI initially surged 75% but then gave back all its gains.

Three revelations:

Token buybacks set a price floor, not a ceiling.

Everything this cycle is a trade (refer to UNI's pump and dump).

Buybacks are only one side of the story; sell pressure (unlocks) must be considered, as most tokens are still low float.

4. Stablecoins Capture Mindshare, But "Proxy Trading" Is Hard to Monetize

Stablecoins are going mainstream. When I rented a motorbike in Bali, the owner even asked for payment in USDT on TRON.

Although USDT's dominance fell from 67% to 60%, its market cap is still growing. Citibank predicts the stablecoin market cap could reach $1.9 to $4 trillion by 2030.

In 2025, the narrative shifted from "trading" to "payment infrastructure". However, trading the stablecoin narrative wasn't easy: Circle's IPO gave back all its gains after an initial surge, and other proxy assets also underperformed.

One truth of 2025: Everything is just a trade.

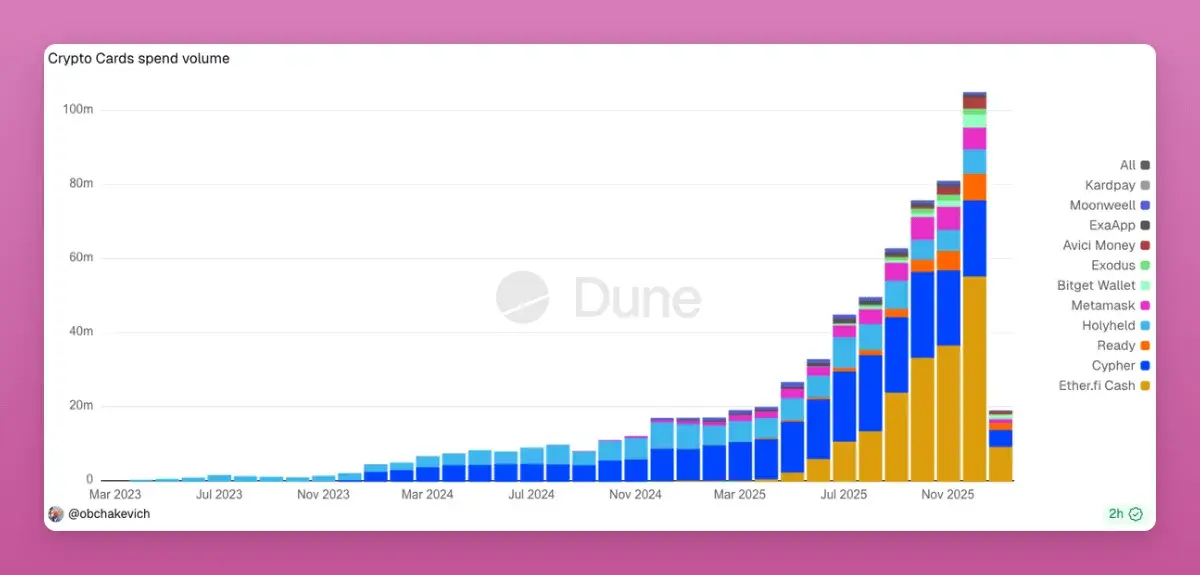

Currently, crypto payment cards are exploding due to their convenience in bypassing strict bank AML requirements. Every card swipe is a transaction on-chain. If direct peer-to-peer payments bypassing Visa/Mastercard emerge in 2026, that would be a 1000x opportunity.

5. DeFi Is More Centralized Than CeFi

This is a bold claim: DeFi's business and TVL concentration is higher than that of traditional finance (CeFi).

Aave commands over 60% of the lending market share (compared to JPMorgan's 12% in the US).

L2 protocols are mostly multi-billion dollar unregulated Multisigs.

Chainlink controls almost all value oracles in DeFi.

In 2025, the conflict between "centralized equity holders" and "token holders/DAO" became apparent. Who truly owns the protocol, IP rights, and revenue streams? The internal dispute at Aave showed that token holders have fewer rights than we thought.

If the "Labs" ultimately win, many DAO tokens will become uninvestable. 2026 will be a crucial year for aligning the interests of equity and token holders.

Summary

2025 proved one thing: Everything is a trade. Exit windows are extremely short. No token has long-term conviction.

As a result, 2025 marked the death of HODL culture, DeFi turned into Onchain Finance, and with improving regulation, DAOs are shedding their "pseudo-decentralized" disguise.

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush

Original link:https://www.bitpush.news/articles/7601755

Perguntas relacionadas

QWhat was the author's main prediction about Bitcoin's price cycle in 2025, and were they correct?

AThe author predicted that Bitcoin would peak in Q4 of 2025, but they were wrong. The market followed the expected four-year cycle, and the author admitted to paying the price for this incorrect prediction.

QAccording to the article, what was the state of the NFT market in 2025?

AThe article states that NFTs were dead in 2025, confirming the author's previous prediction.

QHow did the performance of tokens with fee switches (like UNI) compare to the author's expectations?

AThe author predicted that fee switches would not automatically drive token prices up but would instead set a price floor. This was confirmed when UNI initially surged 75% after its fee switch was activated but then gave back all its gains, showing that buybacks set a price bottom, not a ceiling.

QWhat significant shift occurred in the stablecoin narrative in 2025?

AThe narrative for stablecoins shifted from 'trading' to 'payment infrastructure' in 2025, as their use for real-world payments grew, exemplified by instances like a Balinese motorbike rental requesting payment in USDT on the TRON network.

QWhy does the author argue that DeFi is more centralized than CeFi?

AThe author argues that DeFi is more centralized due to extreme market concentration: Aave holds over 60% of the lending market share (compared to JPMorgan's 12% in the U.S.), L2 protocols are run by multi-sigs, and Chainlink dominates the oracle market for DeFi.

Leituras Relacionadas

After Three Consecutive Quarters of Decline, Can the Crypto Market Find a Window for Stabilization in Q3?

The cryptocurrency market has just concluded its worst-performing quarter since 2022, with total capitalization dropping 12.6% to $2.1 trillion. All core metrics indicate capital is leaving the sector, not just rotating within it. Bitcoin fell 14.2% and Ethereum dropped 25.4% in Q2, breaking their previous correlation with US tech stocks. A key driver is the reversal in US spot Bitcoin ETF flows, which saw a net outflow of approximately $4.67 billion in Q2, including a record monthly outflow near $4.5 billion in June. While recent data suggests long-term holders are accumulating again, sustained ETF outflows mean continued selling pressure.

Market focus is now singularly on the Federal Reserve. The upcoming July FOMC meeting is seen as the most critical event for Q3. A dovish signal could support Bitcoin reclaiming a $68,000-$84,000 range, while a hawkish stance might establish a new trading band around $50,000-$56,000. Additionally, regulatory uncertainty persists, with the progress of the crucial *CLARITY Act* stalling in the Senate, reducing its perceived 2026 passage probability to 40-45%.

Despite the broad downturn, a few sectors showed growth. Prediction markets saw nominal volume surge 48.7% year-over-year to $113.8 billion, and tokenized collectibles transaction volume rose 143% quarterly to $1.4 billion. The Real-World Asset (RWA) tokenization sector also continued steady growth, now representing ~$28.1 billion in on-chain value.

The market's foundation for an extreme crash appears limited, with Bitcoin price hovering near its 200-week moving average. However, the trading paradigm has shifted from narrative-driven speculation to decisions based on price action, policy developments, and interest rate expectations, making a broad sentiment-driven rally unlikely in the near term.

marsbitHá 18h

marsbitHá 18h

The SpaceX Trade, Unlocked: SPCXON Goes Live on WEEX

WEEX has launched SPCXON/USDT, a tokenized spot instrument that provides exposure to SpaceX stock (SPCXON) for traders using USDT, bypassing traditional brokerage barriers. This product, built on Ondo's framework, mirrors SpaceX's economics for eligible non-US traders, with dividends reinvested. SpaceX's high valuation post-IPO is driven by Starlink and Starship, but skeptics note its premium price and upcoming insider unlock. SPCXON offers exposure, not direct ownership or voting rights, and may trade at a premium/discount. WEEX provides a unified platform for such tokenized equities alongside crypto. The exchange, with over 6.2 million users, emphasizes security and innovative tools.

TheNewsCryptoHá 18h

TheNewsCryptoHá 18h

BIT Trading Moment: BTC Still Suppressed by Weekly 200 EMA, Rejection May Restart Decline; Storage and Semiconductors that Surged Last Night Begin Falling in Evening Trading

**Crypto & Stock Market Wrap: Bitcoin Tests Resistance, Stocks Retreat After AI Surge**

Bitcoin consolidates around $66,000, facing key resistance near $68,000—an area seen as a major psychological and technical hurdle where previous rallies have failed. Analysts note the cryptocurrency is caught between its 200-week moving average (~$63,333) and 200-week EMA (~$68,328). A clear break above $68k is needed to signal a stronger bullish trend, while a rejection could lead to a retest of $63k support. Market sentiment remains cautious, with low futures open interest pointing to a low-liquidity rebound rather than a full bull market. Bitcoin spot ETFs saw another $203 million inflow.

US stock futures pointed lower after a strong Tuesday session led by a massive rebound in semiconductors and memory stocks. The rally was fueled by renewed optimism about AI-driven hardware demand, with Micron, SanDisk, and SK Hynix surging. However, those gains reversed in pre-market trading. Super Micro Computer (SMCI) soared over 20% after hours on strong guidance and a record backlog. Other standouts included Rocket Lab and nuclear energy plays Oklo and X-Energy. Rising oil prices (Brent above $91) and climbing Treasury yields (10-year near 4.64%), however, are reigniting inflation concerns and acting as a headwind for equities.

In Asia, markets were mixed. South Korea's KOSPI pared early gains to close slightly higher as semiconductor stocks like SK Hynix gave back initial surges. Japan's Nikkei edged lower as the yen hit a fresh 38-year low against the dollar, raising fears of potential market intervention.

Key events to watch include the Samsung Galaxy launch, AMD's AI event, and a slew of major tech earnings from Alphabet, Tesla, and IBM after the close on Wednesday, followed by the ECB meeting and Intel's earnings on Thursday.

marsbitHá 18h

marsbitHá 18h

Former CFTC Chairman, Circle President Tarbert: Preaching Long-Termism While Cashing Out $30 Million Himself

Former CFTC Chairman and Circle President Heath Tarbert has consistently advocated for a long-term vision in public, urging patience from investors as Circle’s stock price has fallen significantly from its peak. However, it has been revealed that since Circle’s IPO, Tarbert has continuously sold his CRCL shares through pre-arranged trading plans, cashing out approximately $30 million, without making any public market purchases. This contrast between his public messaging and personal actions has drawn criticism.

Tarbert joined Circle in July 2023 as Chief Legal Officer, leveraging his regulatory experience to help guide the company through its IPO and expansion. Despite promoting stablecoins as long-term infrastructure, he established a 10b5-1 trading plan just before Circle went public, leading to substantial stock sales over the following year. In March 2026, he initiated another plan to sell more shares.

His career trajectory highlights a pattern of moving between high-level regulatory roles and influential positions in the financial sector. After resigning as CFTC Chairman in early 2021, he joined Citadel Securities as Chief Legal Officer just 27 days later, during a period of intense regulatory scrutiny for the firm. He later joined Circle, aiding its efforts to navigate regulatory challenges for its public listing.

While Tarbert's expertise in policy and compliance is valuable to companies like Circle, his actions—advocating long-term confidence while personally divesting—raise questions about the alignment between his public statements and his private financial decisions, leaving investors who followed his advice to bear the market risks.

marsbitHá 19h

marsbitHá 19h

Gate Research Institute: The 'Wall Street-ization' Wave of Crypto Financial Products – Competition or Integration?

The article titled "Gate Research Institute: Are Crypto Financial Products Sparking a 'Wall Street' Wave—Competition or Convergence?" explores the evolving relationship between the crypto ecosystem and traditional finance (TradFi).

The piece begins by reflecting on Bitcoin's original 2009 vision of decentralization, disintermediation, and moving away from banks. It then contrasts this with the 2024 landscape, where key crypto assets like Bitcoin are increasingly held through Wall Street products like ETFs issued by giants like BlackRock. The article questions whether this signifies that TradFi is systematically taking over the rights to issue, price, custody, and distribute crypto financial assets.

The core argument is that this is not a zero-sum takeover but rather a bidirectional convergence where each side addresses the other's weaknesses. Crypto offers 24/7 global markets, programmable settlement, and open access but lacks compliant channels, institutional-grade custody, deep fiat liquidity, and mainstream distribution. TradFi possesses these but is constrained by legacy systems, limited operating hours, and slow settlement.

Two primary convergence paths are highlighted:

* **Path A (CEX to TradFi):** Exemplified by Gate, which has progressed from offering tokenized stocks and CFDs to providing direct, real stock trading (US, Hong Kong, South Korea) within its platform, using USDT.

* **Path B (TradFi to Crypto):** Exemplified by Robinhood, which has integrated crypto trading, acquired exchanges like Bitstamp, and is moving traditional assets like stocks onto the blockchain via tokenization and its own Layer 2.

Both paths are ultimately competing to become the next-generation, unified financial account—a "super account" where users can seamlessly trade cryptocurrencies, stocks, ETFs, RWA (Real World Assets), and tokenized treasury products in one interface.

The growth of RWA and tokenized treasuries (e.g., BlackRock's BUIDL) is presented as the asset-layer fusion, providing stable, yield-bearing assets on-chain and acting as a bridge between the two worlds.

In conclusion, the "Wall Street-ization" of crypto is framed as a mutual transformation. Decentralized ideals persist in the protocol layer, while at the application layer, a more efficient, global, and accessible unified capital market is emerging from this convergence. The future competition lies not between crypto exchanges and stockbrokers, but between platforms vying to offer the most comprehensive asset coverage, liquidity, and user experience within a single account.

marsbitHá 19h

marsbitHá 19h