Over the past two years, the AI market has only cared about one question: Who can make the most money?

NVIDIA orders, cloud providers' capital expenditures, data center construction, model company valuations, and the pace of enterprise adoption have formed the main threads of this wave of AI transactions. Capital is buying growth, betting on profit pools, and discussing how much economic value AI can convert into corporate revenue.

But now, another question is beginning to emerge:

If AI truly creates unprecedented wealth, should that money only go to companies, employees, and shareholders?

This is the truly noteworthy aspect of OpenAI's discussion about a public wealth fund.

It is not an implemented regulatory policy, nor is it the U.S. government immediately "seizing equity in AI companies." More accurately, it is the first time the AI industry has pushed the question of "how to distribute future excess returns" onto the public policy table.

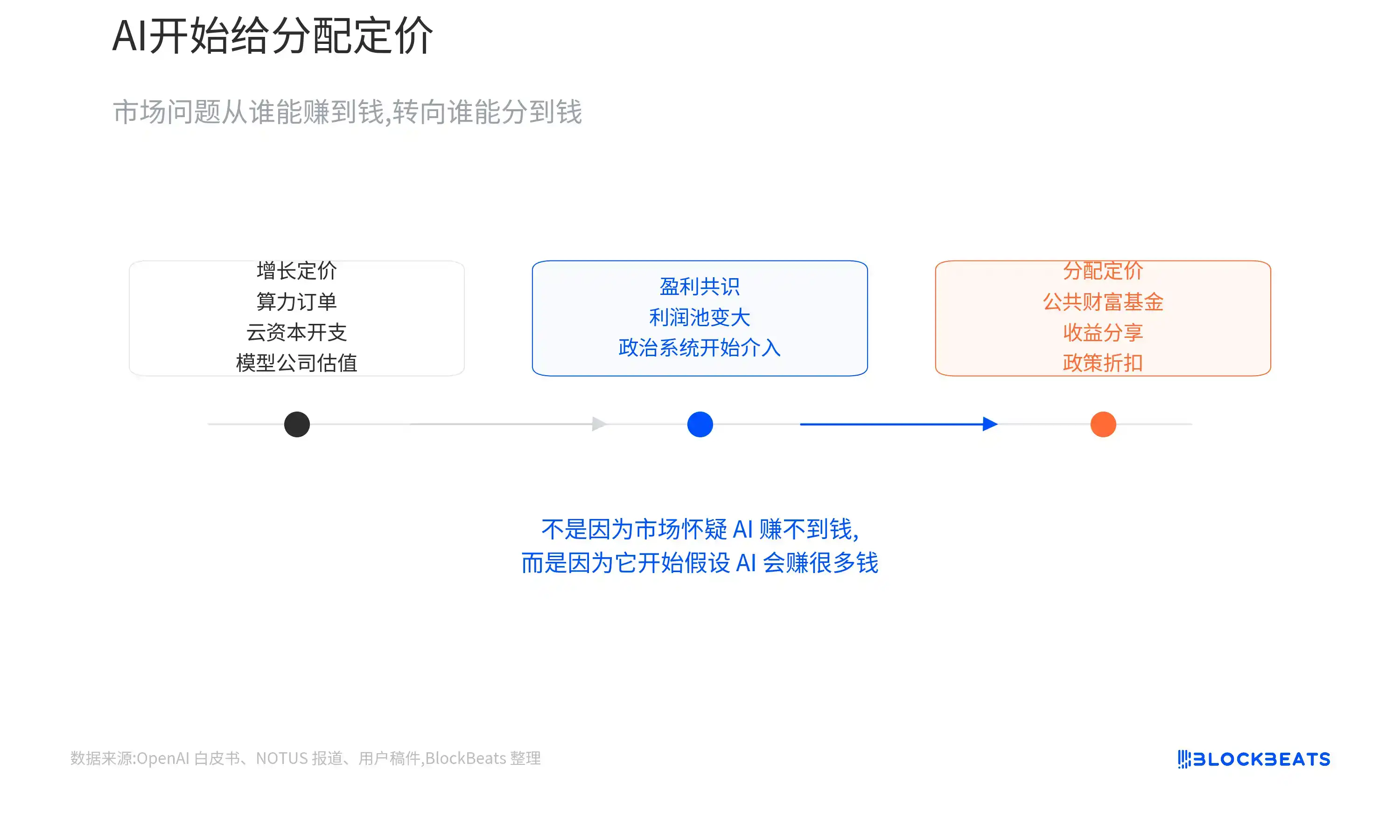

The counterintuitive aspect of this is that the market is not discussing distribution because it doubts AI's ability to make money. On the contrary, precisely because more and more people believe AI will generate substantial excess profits, the political system is beginning to ask: Can these gains be exclusively enjoyed by a few companies and investors?

AI Transactions Begin to Include a Policy Bill

First, let's clarify the factual boundaries.

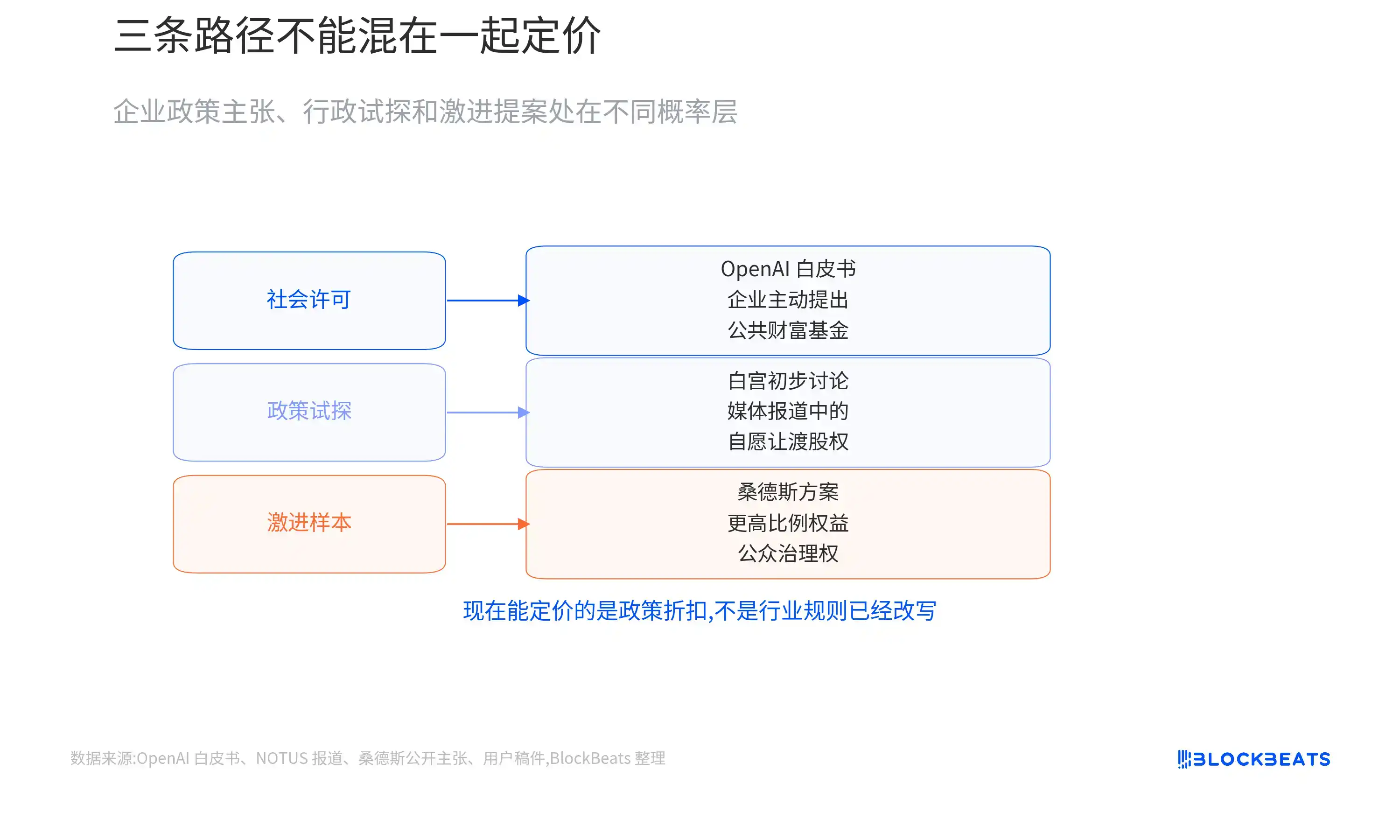

According to a NOTUS report on June 4, senior White House officials have held preliminary discussions with leading AI companies about "voluntarily ceding some equity." This direction is similar to the Alaska Permanent Fund: assets are held in part by the government or a public trust, with some of the proceeds distributed to residents.

In a white paper released in April, OpenAI also proposed the idea of establishing a public wealth fund. Large model enterprises could contribute funds, equity, or other means to allow ordinary families, who do not directly hold tech stocks, venture capital assets, or private equity, to share in the benefits of AI growth.

Sanders's version is more radical. He advocates that large AI companies cede a higher proportion of equity to the public and grant the public some governance rights. The "50% stock tax" and board seats mentioned in the materials represent the most radical political sample in this round of discussion.

But these three things cannot be viewed interchangeably.

The White House discussion remains a preliminary exploration reported by the media, with no formal proportions, legal structure, or timeline. The OpenAI white paper is a corporate policy proposal, not a government document. The Sanders proposal has strong impact, but is still a long way from becoming actual policy.

Therefore, the most reasonable assessment currently is not that "AI companies are about to be nationalized," but that a new variable, not present before, has begun to appear on the AI valuation sheet:

Will the most profitable AI companies of the future need to allocate a portion of their economic rights to gain acceptance from society and regulators?

The short-term impact on the secondary market is limited. Public market AI proxy assets like NVDA, MSFT, AMZN, GOOGL, and META are still primarily driven by demand for computing power, cloud capital expenditures, order expectations, and profit realization.

But the impact is more direct for unlisted model companies.

If companies like OpenAI, Anthropic, and xAI go public in the future, investors will not only ask how much money they can make, but also: How much of that money will need to be ceded to public funds, governments, or other public mechanisms?

This is not an immediate valuation hit that has materialized, but a new policy discount.

OpenAI is Purchasing a Social License

OpenAI's proactive proposal for a public wealth fund is essentially purchasing a "social license" for its future expansion.

A social license is not a formal permit, but the tolerance of the public, regulators, and the political system for a company's continued expansion. The more successful an AI company becomes, the more acute this question becomes.

The stronger the model capabilities, the more discussions there are about human job displacement. The higher the valuation, the easier it is for ordinary people to perceive AI as a wealth machine exclusively for a few companies, employees, and shareholders.

OpenAI is not facing a problem typical for ordinary tech companies, but a narrative pressure approaching the scale of the Industrial Revolution:

If AI truly changes productivity, who gets to share in those benefits?

OpenAI's white paper emphasizes the need for the U.S. to maintain AI leadership while acknowledging that automation may reshape a large number of jobs. The public wealth fund is one of the buffer solutions it proposes.

Translating this into market language, OpenAI may hope to use a portion of controllable future economic rights to reduce more uncontrollable political risks.

If it completely fails to address the narrative of "AI taking jobs, profits going to the few," it may face higher taxes, stricter regulation, antitrust pressure in the future, and even be forced to disclose more complex policy risks during a potential IPO.

Proactively designing a moderate sharing mechanism might instead transform the risk from an "unknown political shock" into a "long-term cost that can be estimated."

This is somewhat like a resource company designing local employment, infrastructure, and benefit-sharing schemes before entering a region. The difference is that AI companies are not dealing with residents around a single mine, but the entire labor market and electorate.

It also isn't dealing with a one-time compensation, but with how future excess profits are accepted by society.

5% Sharing and 50% Mandatory Equity are Not the Same Thing

The phrase "cede equity" is easily alarming, but different paths have completely different impacts on valuation.

The first path involves companies voluntarily contributing a small percentage of economic rights, likely without voting rights, to a public wealth fund.

If the proportion is limited and the rights are clear, it more closely resembles a long-term policy cost. Assuming a future AI company valuation of $1 trillion, allocating 5% of economic rights to a public fund is certainly dilutive for existing shareholders, but the market can discount it as a specific figure.

The second path involves the government obtaining economic rights through industrial policy.

For example, certain subsidies, loans, or industrial support might come attached with warrants—the right to obtain a portion of future equity returns under agreed conditions. It's important to distinguish here: Warrants are not equivalent to directly taking over common shares, and non-voting economic rights are not equivalent to board seats.

The former is more like fiscal sharing; the latter enters the realm of corporate governance.

The third path is the Sanders-style mandatory high-percentage public ownership.

If large AI companies are required to surrender a high percentage of equity and allow public or government representatives onto the board, the impact is no longer just profit sharing, but issues of control, governance conflict, and innovation incentives.

The government acting simultaneously as regulator and shareholder also creates new conflicts of interest: Is it protecting consumers and competition, or is it protecting the value of the company it partly owns?

This is also why, although radical proposals are highly transmissible, they cannot currently be treated as high-probability pricing benchmarks.

The more realistic scenario remains the repeated discussion of small-scale, voluntary, economically-focused proposals. These may not materialize immediately but will become unavoidable issues in AI company financing, IPO processes, and policy communications.

For OpenAI, what is truly sensitive is not "whether to share," but whether the sharing mechanism will ultimately affect the governance structure.

Microsoft, venture capitalists, employee stock ownership entities, and strategic investors will all be concerned: Does the public fund receive economic rights or voting rights? What is the proportion? Does it affect exit valuations? Will it change the pricing logic of a future IPO?

Enterprise clients will also ask: If the government becomes an economic beneficiary in some sense, will procurement, data governance, and regulatory neutrality become more complex?

Therefore, the market implication of this is not that AI company profits are being immediately sliced away, but that the AI profit pool is being placed within a public distribution framework for the first time.

The Real Risk is the Shift from 'Voluntary Sharing' to 'Mandatory Governance'

This line of development is still in its early stages.

The evidence chain is sufficient to show that the publicization of AI returns is entering the stage of public policy exploration; but it is not yet sufficient to conclude that the rules of the AI industry have already changed.

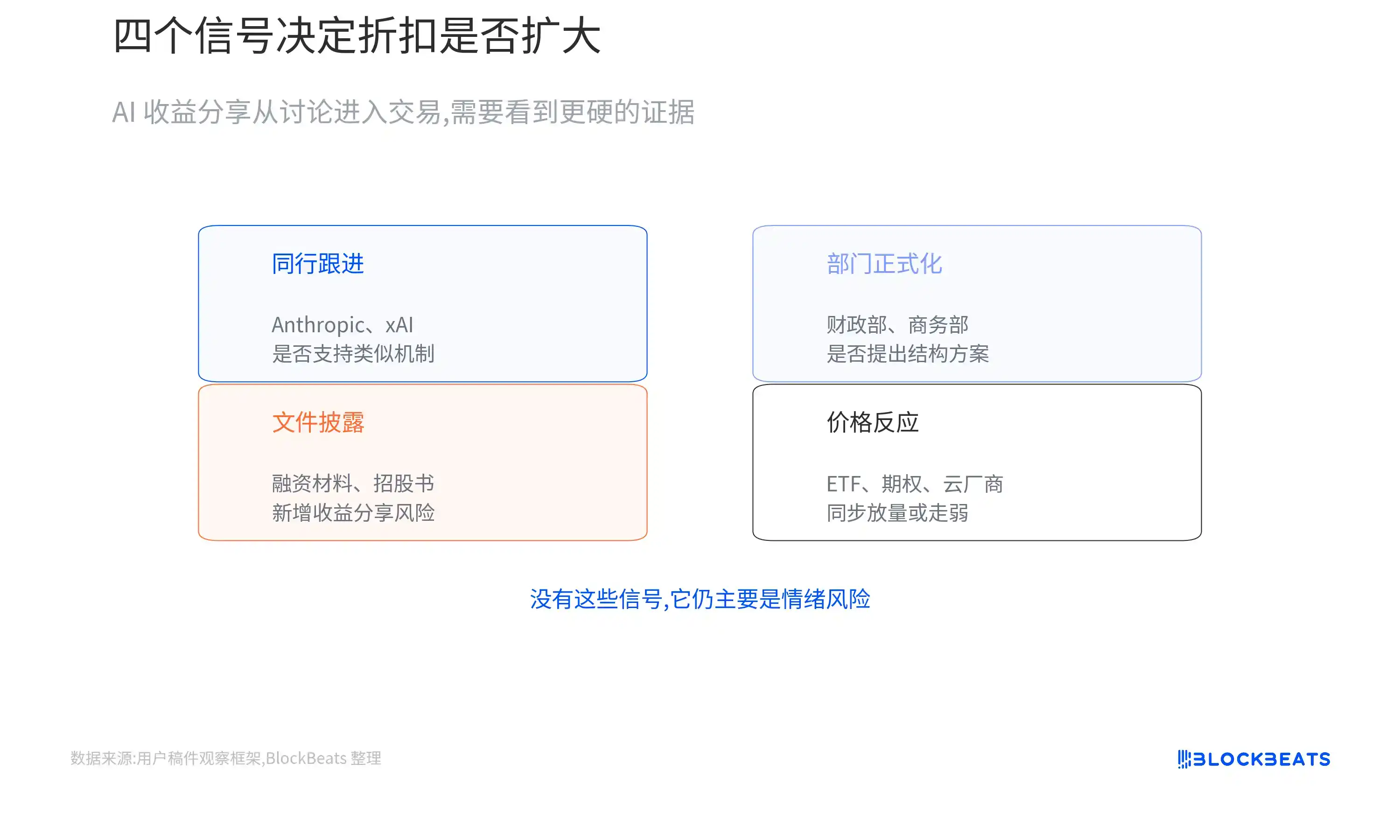

The next four observation points are most important:

First, observe whether companies other than OpenAI follow suit:

If Anthropic, xAI, or other leading model companies also begin to support similar mechanisms, this could evolve from OpenAI's single-company strategy into an industry negotiation framework. Conversely, if more companies publicly avoid or oppose it, the market will tend to view it as OpenAI's particular approach.

Second, observe whether the White House and executive departments formalize it:

If departments like the Treasury, Commerce, or the National Economic Council begin proposing fund structures, tax arrangements, or warrant schemes, policy exploration will enter a priceable stage. If it remains at the level of meetings and media leaks, the impact is mainly sentiment risk.

Third, observe financing documents and future prospectuses:

If OpenAI, Anthropic, or others add risk disclosures about "public wealth fund, revenue sharing, government economic rights, special governance arrangements" in future financing materials or IPO documents, the valuation discount will move from discussion into trading.

Fourth, observe whether market prices begin to react:

If AI-themed ETFs, semiconductor ETFs, leading cloud companies, or related options start showing amplified trading volume, rising volatility synchronized with policy news, or relative underperformance against the broader market, it would indicate capital is starting to treat this variable as a main trading theme. There is no such evidence yet.

Therefore, there is currently no need to interpret this as a valuation collapse for the AI industry.

A more accurate description is:

The AI market used to price only growth; now it's beginning to price distribution.

If the final solution is merely a small proportion, non-voting, clearly disclosed allocation of economic rights, it more closely resembles an insurance premium paid by AI companies for long-term expansion. The cost exists but is estimable, tradable, and acceptable.

But if voluntary sharing is pushed by political pressure toward mandatory equity holding, or even board and governance rights arrangements, the valuation logic will change significantly.

Because then the market would be discounting not just a portion of profits, but corporate control and long-term growth freedom.