Glassnode has continued to expand its Traditional Finance coverage in Studio, helping users connect crypto-native market activity with the growing universe of listed instruments tied to digital assets.

This expansion reflects the growing role of ETFs, treasury companies, and other listed vehicles in digital asset market analysis, as institutional exposure increasingly moves beyond spot markets.

Two new metric families are now live:

- US Spot ETF Price & Volume

- US Digital Asset Treasury Company Price & Volume.

For each selected crypto asset, users can now retrieve daily price and traded volume across the relevant US spot ETFs and publicly listed treasury companies, with one time series per ticker. This gives investors a more complete view of how crypto exposure is being expressed through traditional equity markets.

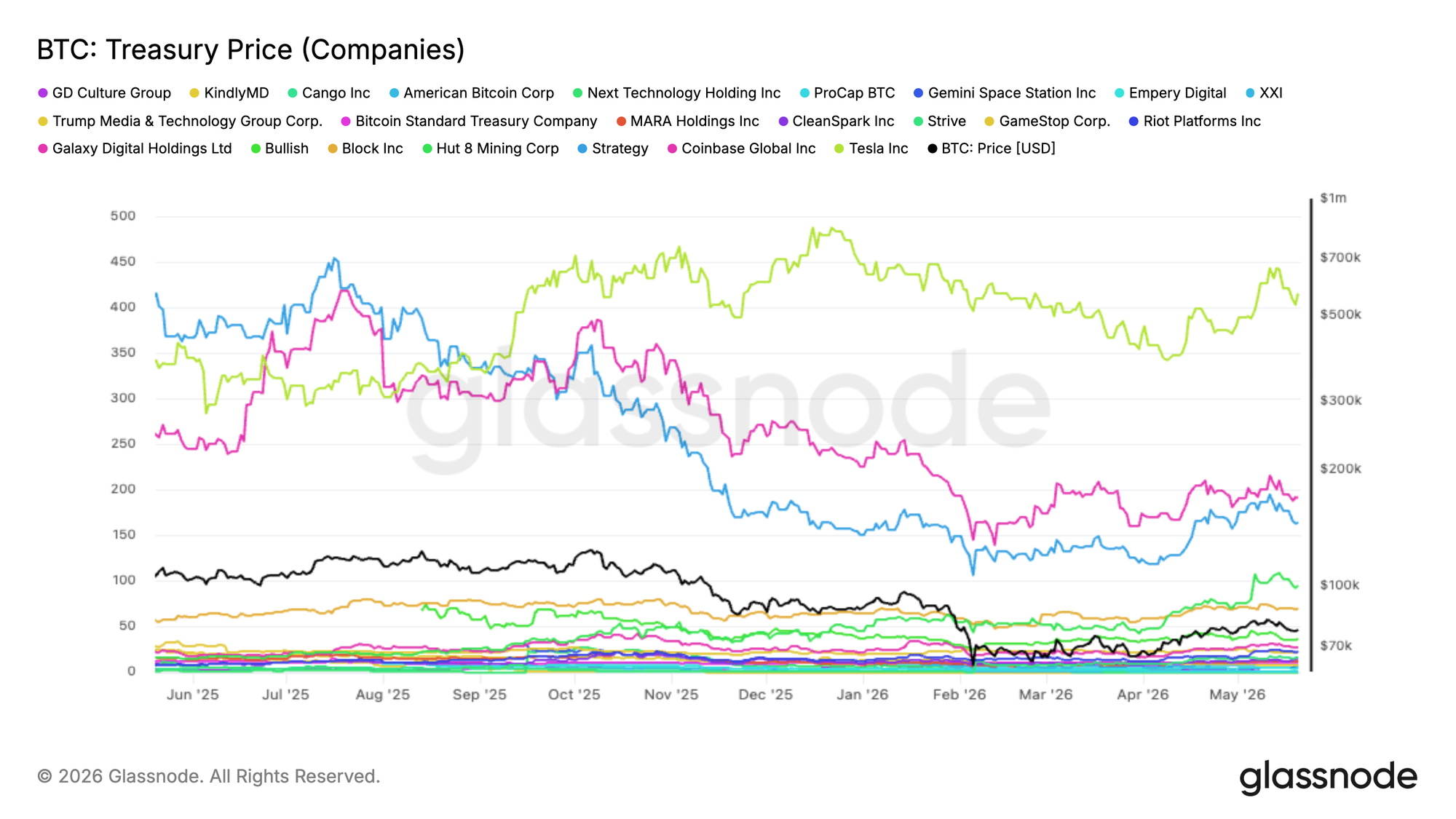

DATs: Analyzing Equity Behavior Relative to Crypto

For US Digital Asset Treasury (DAT) companies, the data makes it easier to compare how listed equities behave relative to the underlying crypto asset and assess which names exhibit stronger or weaker equity beta to crypto market movements.

For example, users can compare BTC performance against companies holding BTC on their balance sheet to identify which stocks behave more like direct crypto proxies, and which names trade with a more idiosyncratic equity profile.

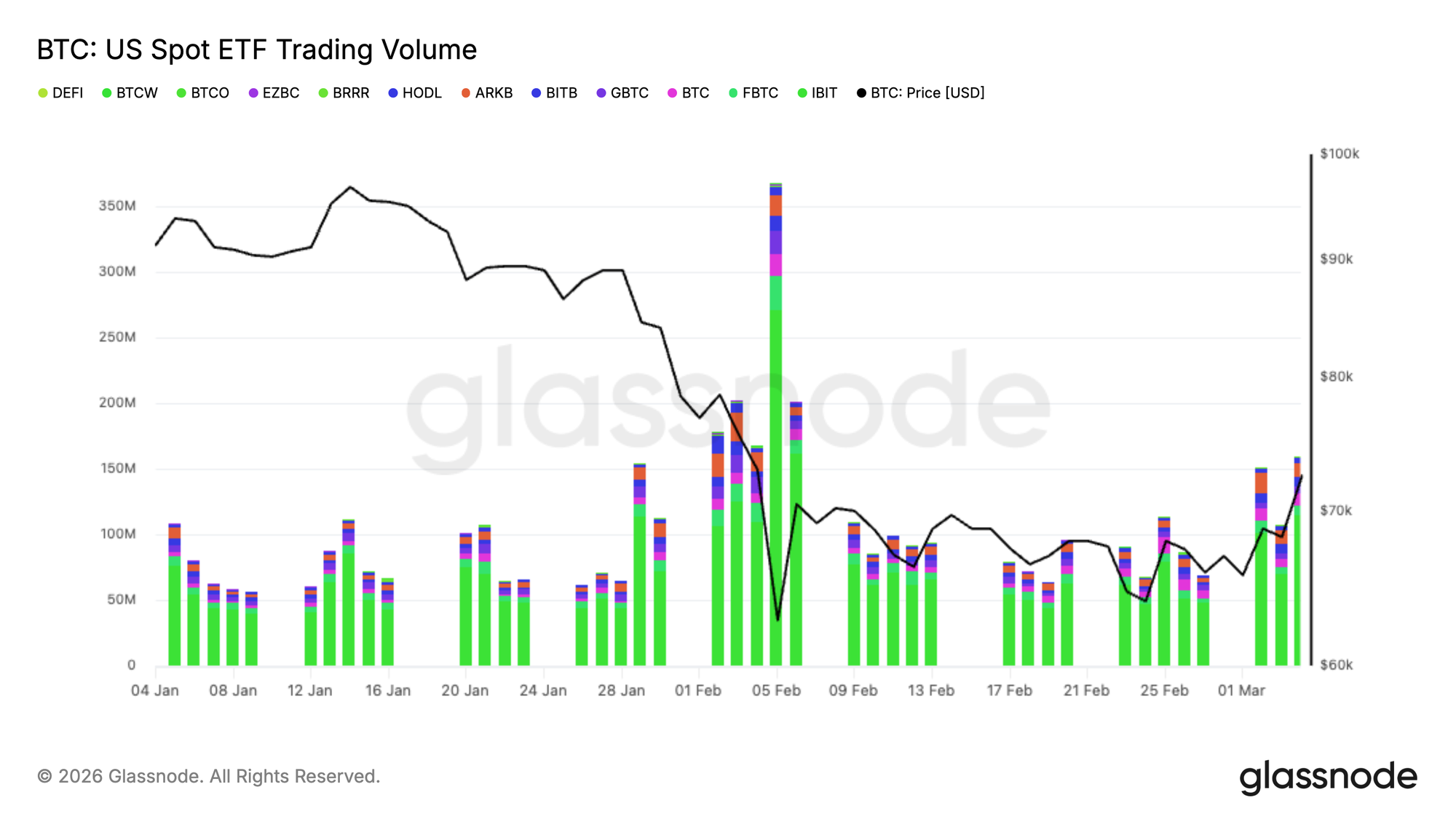

US Spot ETF Volume: Assessing Participation and Liquidity Conditions

The addition of trading volume is particularly useful for US spot ETFs. Trading volume provides insight into liquidity, participation, and conviction.

For example, a sharp spike in ETF trading volume around a major price move or macro event can signal heavy institutional repositioning — and comparing ETF volume against the underlying spot market shows how much real flow is moving through TradFi venues versus crypto-native ones. Sustained volume can confirm genuine demand behind a price trend, while thin volume on a move may warrant more caution.

Together, these new metrics strengthen Glassnode’s ability to bridge crypto-native data with traditional market instruments, giving users a unified view of spot assets, ETFs, and listed treasury vehicles directly in Studio.

Explore the new metrics in Studio

- DAT Price Companies

- DAT Trading Volume Companies

- US Spot ETF Price

- US Spot ETF Trading Volume

- Follow us on X for timely market updates and analysis

- Join our Telegram channel for regular market insights

- For on-chain metrics, dashboards, and alerts, visit Glassnode Studio

Disclaimer: This report is for informational and educational purposes only. The analysis represents a limited case study with significant constraints and should not be interpreted as investment advice or definitive trading signals. Past performance patterns do not guarantee future results. Always conduct thorough due diligence and consider multiple factors before making investment decisions.