A couple of days ago, The Wall Street Journal published a report featuring a hedge fund almost nobody has heard of, called Darsana Capital.

This fund was only founded in 2014 and is not particularly large. In 2019, it made a decision: to bet on a rocket company that hadn't gone public yet. Back then, SpaceX was valued at around $30 billion.

Seven years later, SpaceX is about to go public, valued at $1.75 trillion. The approximately $600 million Darsana invested over those years is now worth about $15 billion. This single bet is one of the most profitable hedge fund trades in Wall Street history. This one position in SpaceX accounts for nearly 60% of Darsana's entire assets.

SpaceX, this biggest IPO ever, is also the opening shot of this year's wave of tech company listings. Stories like Darsana's have been frequent in the news lately. Google invested $900 million in 2015, now worth over $100 billion. Founders Fund's life-saving $20 million investment in 2008 has now ballooned to $19.5 billion.

But flip to other reports, and the tone completely changes.

In late March, Bloomberg and Reuters both reported a strange phenomenon: a group of investors bought SpaceX shares but couldn't confirm whether they actually acquired them. One such investor, an entrepreneur named Tejpaul Bhatia, believes he holds SpaceX stock, but has no way to verify if the shares supposedly belonging to him are real or not.

On one side, wealth creation myths precise down to the billion; on the other, people who can't even tell if they bought anything. Same company, same IPO – why such a stark divide?

The Private Secondary Market in the Age of "AI Anxiety"

Over the past two or three years, AI has pushed private market valuations to absurd heights.

Companies like OpenAI, Anthropic, xAI, SpaceX have valuations in the hundreds of billions or even trillions of dollars, and they're still skyrocketing. Ordinary investors stare at these numbers, left with just one thought: I want a piece of that too.

Never before have so many people wanted to get in. The trouble is, these companies are not public. For ordinary people, finding a way to buy in before an IPO is nearly impossible.

Look at SpaceX's shareholder list, and it becomes clear. Major institutions and strategic shareholders hold positions worth tens or hundreds of billions; Google's parent company Alphabet alone holds over a trillion dollars worth. Meanwhile, all the accessible public channels combined—a few ETFs and funds holding SpaceX—offer exposure of only about $1 billion.

Furthermore, most avenues block ordinary people anyway. The majority of channels in the private market are only open to accredited investors. In the US, that means an annual income over $200,000, or assets over $1 million excluding your primary residence. Those who don't meet this threshold can't even squeeze through that small $1 billion opening.

With other things, such disparity might make people back off. But the logic of FOMO works the opposite way. The more scarce something is, the more you see others making money, the more you want to squeeze in.

The money hasn't retreated. It has flooded into a place called the private secondary market.

This market specializes in buying and selling shares of unlisted companies. Early investors and employees want to cash out; those who missed the early boat want to get in. The platforms, funds, and various vehicles that facilitate these trades constitute this market.

In recent years, it has exploded. From 2019 to now, its size has tripled. Volume was around $162 billion in 2024, rose to roughly $230 billion in 2025, and is projected to touch $250 billion in 2026. The number of companies willing to allow secondary transfers of their shares went from 12 to 31 within a year.

As money pours in, sellers of SpaceX emerge.

How many have emerged? According to The New York Times, there are at least 170 Special Purpose Vehicles (SPVs) that have bought into SpaceX. An SPV is a shell; whoever manages to acquire some SpaceX shares puts them into the shell, then sells pieces of the shell to investors further down the line. 170 shells, all circling the same company.

These shells come from all sorts of places.

In October 2025, an outfit called Witz Ventures launched an SPV named The Cashmere Fund on the fundraising platform Republic. This one shell bundled three of the hottest names—xAI, SpaceX, Perplexity—and sold them to retail investors. About 150 listeners of the financial podcast Rich Habits also managed to jump the queue into SpaceX through a group buy. Rapper 2 Chainz, SkyBridge founder Anthony Scaramucci have both publicly stated they hold SpaceX.

The problem is, this swarm of middlemen that popped up overnight varies widely in quality.

One firm called Vika Ventures collected $5.9 million from investors, promising to buy SpaceX shares. It was later discovered that the founder used the money to buy luxury watches and a private jet. In 2023, another financial broker was sentenced to eight years for defrauding over 50 investors of nearly $6 million by selling pre-IPO shares, including SpaceX.

Then there's Linqto, a once-red-hot platform specializing in star names like SpaceX. It went bankrupt in 2025, with the SEC investigating whether it properly verified users' accredited investor status, affecting over 13,000 investors.

Even if you don't run into a scammer, things can still be murky.

DataPower Capital is an institution dealing in SpaceX allocations. Its founder, David Yakobovitch, told The New York Times that when he acquires shares himself, he only accepts transactions that are one layer removed from SpaceX. "Once you go a few layers further down," he said, "things start to get cloudy."

Nested Five Layers Deep

Back to those 150 Rich Habits podcast listeners. What they bought wasn't actually SpaceX.

They bought into Witz Ventures, and Witz Ventures bought a stake in DataPower Capital. DataPower is the one that gets shares directly from a shareholder on SpaceX's official cap table. In other words, an ordinary person ordering through a podcast is separated from the actual SpaceX stock by at least two or three layers of shells.

With each additional layer, two things happen simultaneously.

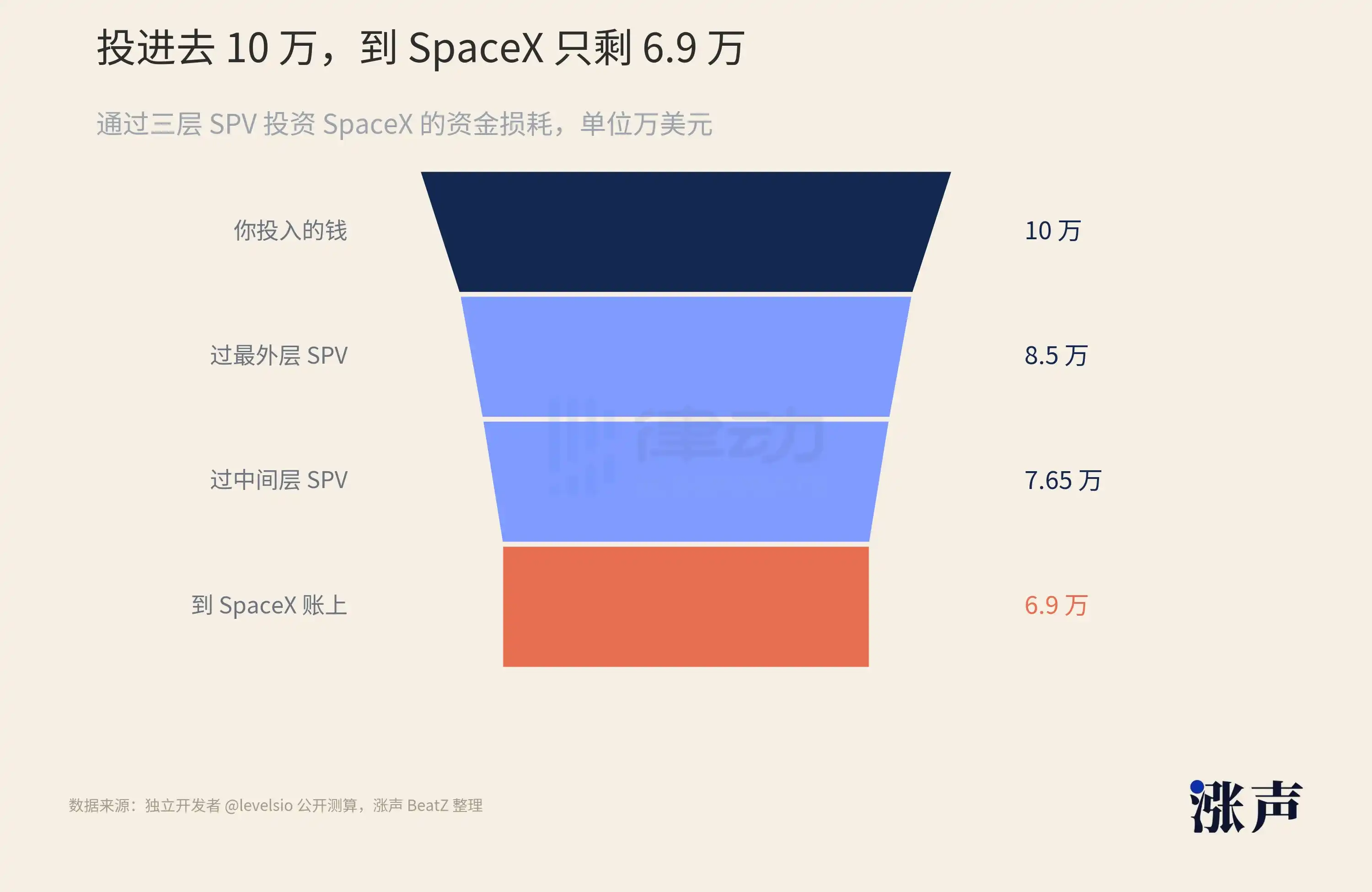

First, the money shrinks. Independent developer levelsio calculated on social media: assume you invest $100,000 into SpaceX through three layers of SPVs. The outermost layer charges a 6% setup fee; the inner two layers each take management fees and profit shares. The money that actually reaches the SpaceX underlying shares ends up being only about $69,000. You haven't even started making money, and 30% is already gone.

Second, the truth recedes. A critical feature of this SPV structure is that investors at each layer can only see the layer directly above them. You buy the outermost shell, and its manager tells you it holds the next shell. Is the next shell real or not? Does the chain ultimately lead to actual SpaceX shares at the bottom? You can't see, and you have no right to check.

170 shells, nested up to five layers deep at the most extreme. This is why Bhatia and others can't confirm their holdings. It's not that they weren't careful enough; this structure was designed from the outset not to let people outside the shell see inside.

Why did SpaceX's nesting dolls get so deeply nested?

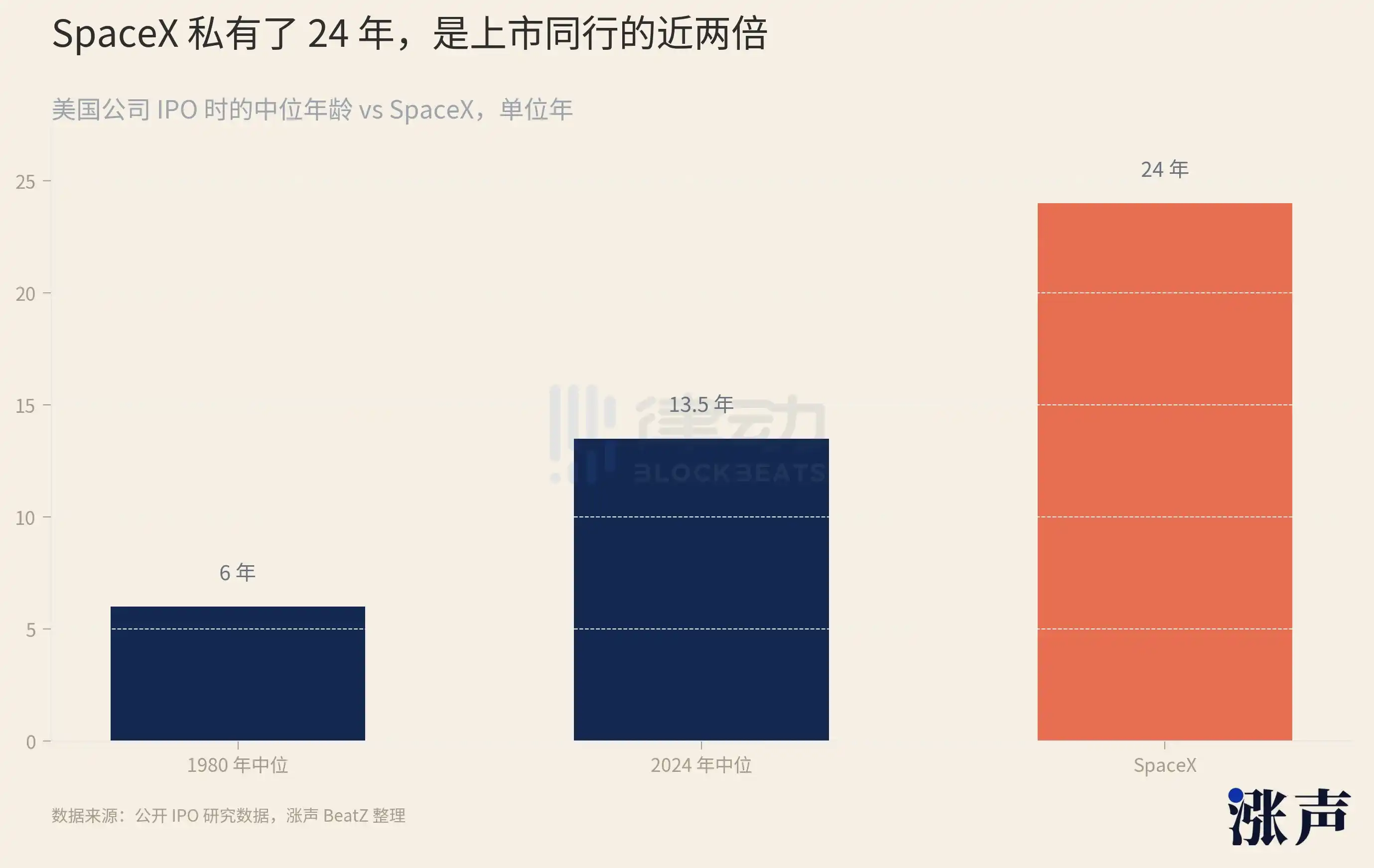

Look at how long it has been in the private market. Founded in 2002, going public in 2026 – private for a full 24 years.

What does 24 years mean? Those tech companies that went public in 1999 were, on average, only 4 years old. The 2014 batch averaged 11 years. Recently, the median age for US companies at IPO has stretched to 14 years. SpaceX's 24 years is an extreme point even on this already lengthening curve.

The longer a company stays private, the longer its shares have been repeatedly traded, transferred, and nested in shells over the years. SpaceX's shares have been circulating over-the-counter for over two decades; layers upon layers have built up outside.

Prolonged private periods aren't unique to SpaceX.

Over the years, the median age of US companies at IPO has risen from 6 years in 1980 to 13.5 years in 2024. The reason is simple: there's simply too much money in the private markets.

As of 2023, global venture capital funds still had over $650 billion in dry powder. Companies aren't short of funding, so they're in no rush to go public and face the earnings pressure and regulation of public markets. Thus, unicorns valued over $1 billion have piled up; there are now over 1,500 globally, worth a combined $6 trillion, most of which haven't raised a funding round at a public valuation in over three years.

The longer a company stays private, the longer the shares held by employees and early investors remain locked up. These people want to cash out, and the secondary market is the only exit. With demand piling up, SPVs designed to meet that demand have sprung up in batches.

At the peak of the VC frenzy in 2021, the number of newly established SPVs in the US surged 235% year-over-year. By Q3 2024, there were over 2,400 identifiable, still-active SPVs. With a tool being used on such a massive scale, repeatedly, for over twenty years, nesting five layers deep is almost an inevitable outcome.

And SpaceX happens to be one of the strictest companies in the entire private market when it comes to managing its stock. Externally, SpaceX exercises its right of first refusal on almost every share transfer, intercepting trades. It conducts share buybacks every six months, taking employees' shares they want to sell back into its controlled pool.

The tighter the door is welded shut, the more expensive the tickets at the door become.

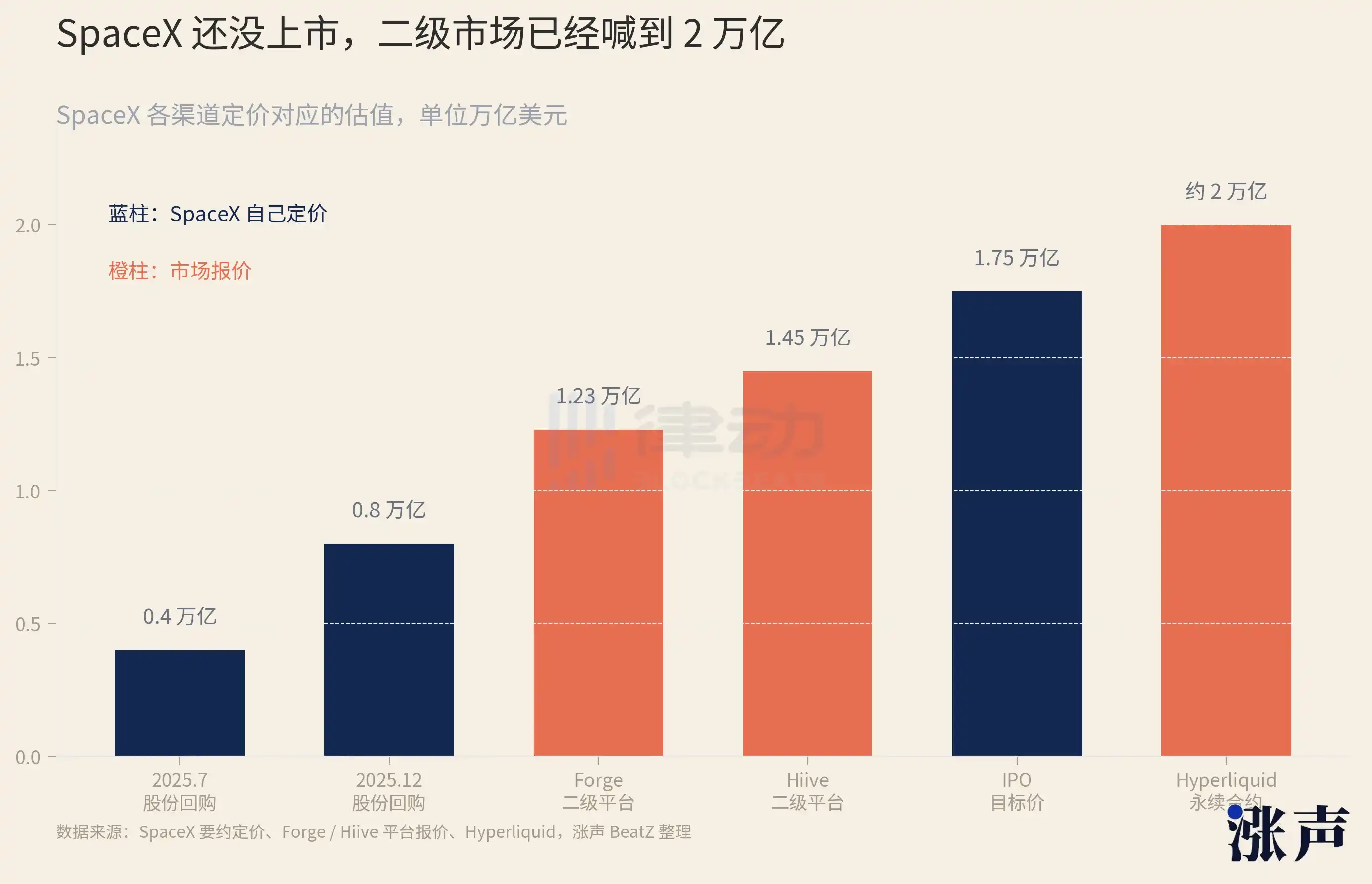

SpaceX's own pricing is known: its share buyback in July 2025 was priced at a $400 billion valuation; six months later in December, it doubled to $800 billion. But secondary market quotes were already way ahead. Forge's platform quoted around $1.23 trillion, Hiive quoted $1.45 trillion, and contracts listed on the crypto trading platform Hyperliquid even implied over $2 trillion, higher than SpaceX's own targeted IPO valuation.

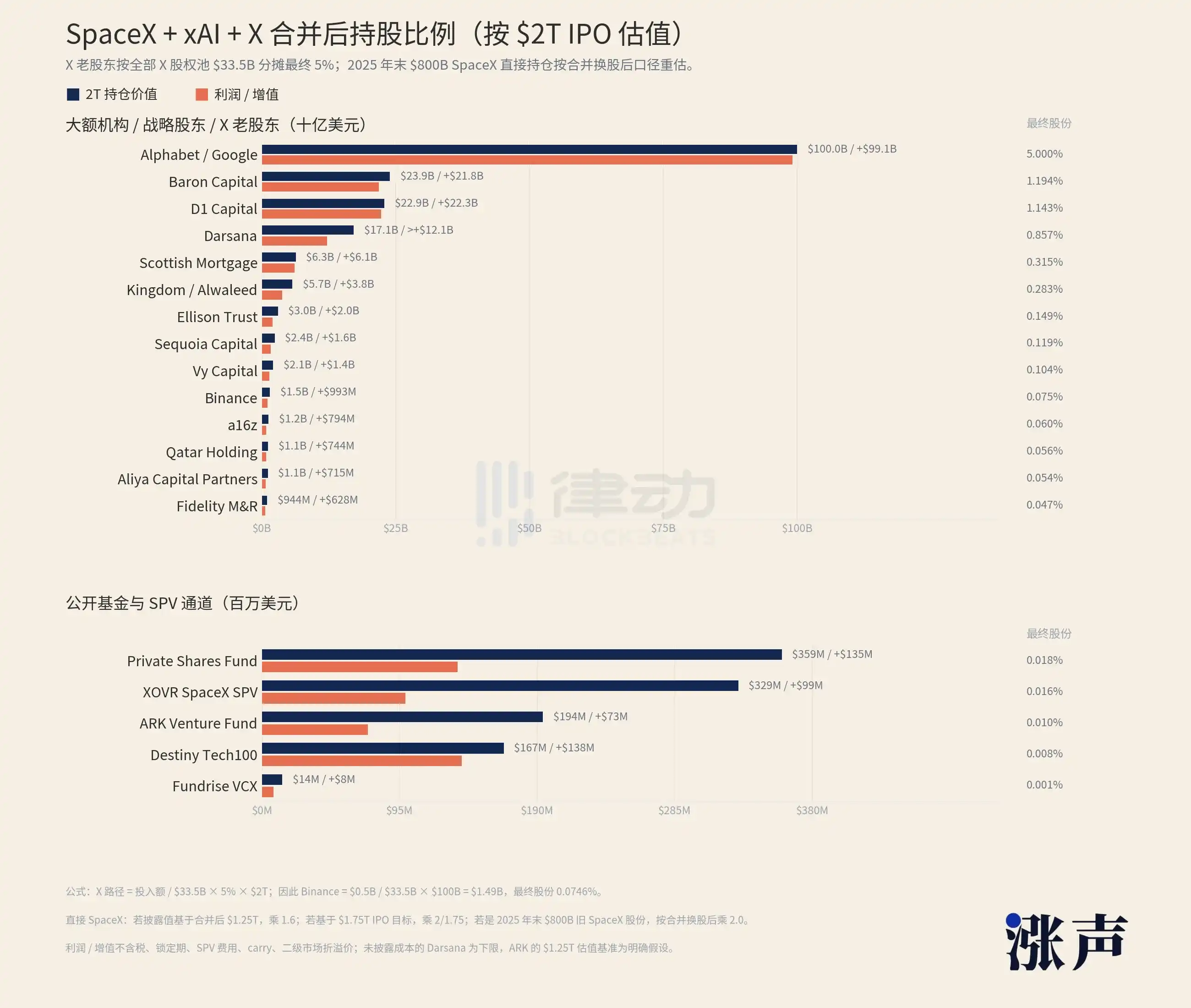

There's an even more tangled mess of threads, spun from mergers. In March 2025, Musk merged X, the former Twitter, into his AI company xAI. In February 2026, SpaceX then swallowed up the entire xAI. Everyone who bought Twitter, who bought xAI, along with their entire ecosystem of shells behind them, all ended up on SpaceX's cap table after two rounds of share swaps.

Opening a Blind Box

Nested to this extent, even the companies themselves can't sit still.

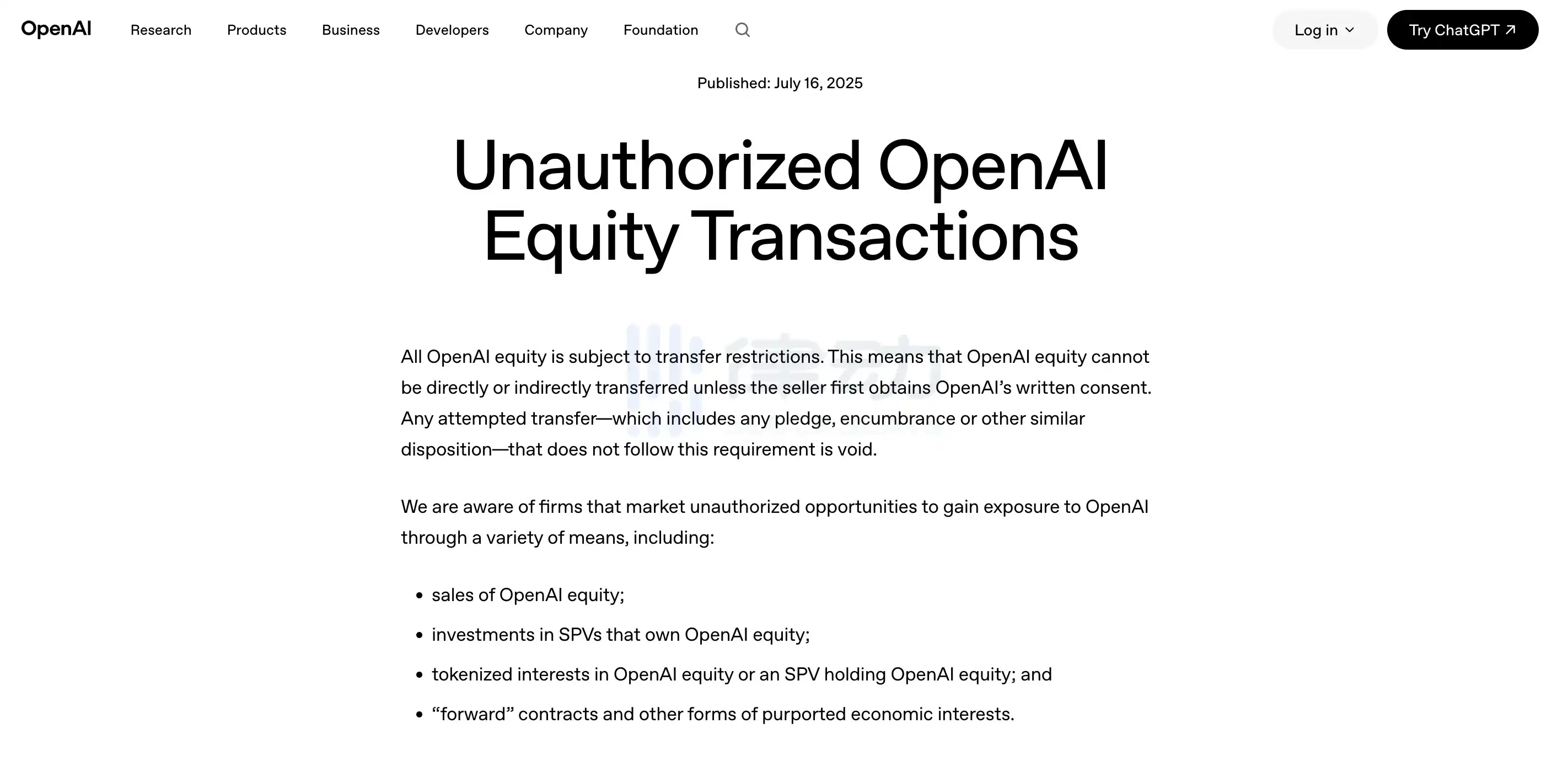

In May 2026, Anthropic and OpenAI issued public statements one after another, explicitly telling the market that any share transfers not approved by their boards are invalid and won't be recorded on the company's books. Both named platforms including Forge and Hiive as unauthorized. The news triggered an immediate flash crash in the related tokens linked to these companies on the on-chain secondary markets specializing in pre-IPO shares, plunging 30-40% in a single day.

These public announcements regarding secondary market transactions are not spur-of-the-moment decisions by one or two companies.

Recently, when robot company Figure AI was rumored to be valued at $39.5 billion, it also intervened to block secondary trading of its shares. Almost all the hottest names in the private market—Anthropic, SpaceX, Anduril, Stripe, Databricks—are doing the same thing: dialing down their tolerance for secondary trading all the way to zero.

Why are they collectively turning hostile?

This relates to a little-noticed IPO "red line." Under US rules, if a company has over 2,000 shareholders, even if it's not public, it must disclose its financials regularly like a public company. Nested SPVs make it impossible for a company to count its actual shareholders. One SPV counts as a single entity on the cap table, but may hold hundreds of individuals behind it. If a company inadvertently crosses that 2,000 line, it is forced to open its books.

Another reason is pricing employee stock options. If a company's stock is freely traded on the secondary market and driven to high prices, the company can't avoid that number when setting the exercise price for employee options. The crazier the secondary market gets, the less valuable employees' options become.

More crucially, it's about information. Shareholders have a legal right to access company information. For AI companies, model architecture, training data, computing power arrangements are their most guarded secrets. When a company can't even count its own shareholders, it also can't tell to whom this information is flowing.

Clearing up uncountable shareholders, protecting option pricing, closing information leaks—none of these issues are new by themselves. But when the secondary market swells to $230 billion and nesting reaches five layers, companies find that handling it quietly is no longer enough. So they step into the open, putting the phrase "your shares are invalid" into a public announcement for the first time. SpaceX hasn't issued a similar statement. But its right of first refusal accomplishes the same thing.

That one word, "invalid," from the company leaves those nested shells dangling in mid-air. You buy an SPV, you pay. Whether the underlying SpaceX shares in that allocation were ever approved, whether they count—until the company publicly reconciles its books, no one can give you an answer.

Thus, buying an SPV linked to SpaceX is increasingly like opening a blind box.

The box's opening date is fixed. On June 12th, when SpaceX rings the bell on Nasdaq, its IPO filing will for the first time contain a public, verifiable shareholder register. Every single layer of shell wrapped around its shares over the past twenty-plus years will have to be reconciled at this moment. If it matches, the box contains real stock; if not, it's worthless paper. Bhatia will find out on that day which lot he drew.

But after SpaceX, there's OpenAI, there's Anthropic, and a long list of names queuing up. Just scroll through your social feed a few times, and you'll see posts about "proxy investments" in these hottest AI companies.

The hot money generated by AI in recent years is overflowing with nowhere to go. The truly worthwhile targets are just a handful, and they're all tightly locked up. Too much money, too narrow a gate, and countless shells sprout in the middle.

As long as this imbalance persists, the private secondary market will remain as it is now: a blind box everyone wants to play, but no one can truly say what they've drawn.