Author: Gu Yu, ChainCatcher

In the crypto industry, the pace of innovation is often a key measure of a protocol's vitality. However, Uniswap, which once single-handedly kicked off the DeFi Summer, seems to be slowing down.

Looking back at Uniswap's evolution, its iteration rhythm has always been known for its fast pace: V1, featuring the AMM mechanism, was born in 2018; V2 introduced ERC-20/ERC-20 pairs in 2020; V3 launched concentrated liquidity in 2021; and V4 proposed programmable Hooks in 2023. On average, every 1.5 years, Uniswap would introduce a highly innovative mechanism, reshaping the flow paths of tens of billions of dollars.

However, as of April 2026, nearly three years have passed since the announcement of the V4 proposal, and the market has yet to see any updates on Uniswap's next version.

Currently, Uniswap's product developments still revolve around Uniswap V4, which aims to transform Uniswap from a fixed-function AMM into a highly programmable liquidity platform. The core innovation of this version is Hooks, which are modular, programmable plugins that allow developers to insert custom logic throughout a pool's lifecycle, enabling almost limitless functions such as dynamic fees, limit orders, TWAMM (Time-Weighted Automated Market Maker), MEV protection, loss hedging, custom oracles, continuous clearing auctions (CCA), and more.

In other words, whereas developers previously had to fork Uniswap to implement certain specific functions, leading to the fragmentation of Uniswap's liquidity across many forked DEXs, now developers only need to write a Hook contract to significantly enhance the customizability of Uniswap's liquidity pools.

Although Uniswap announced the specific concept of the V4 version in June 2023, due to security concerns, the version underwent 9 independent audits and a large-scale security competition, delaying its mainnet launch from the initial Q3 2024 to the end of January 2025.

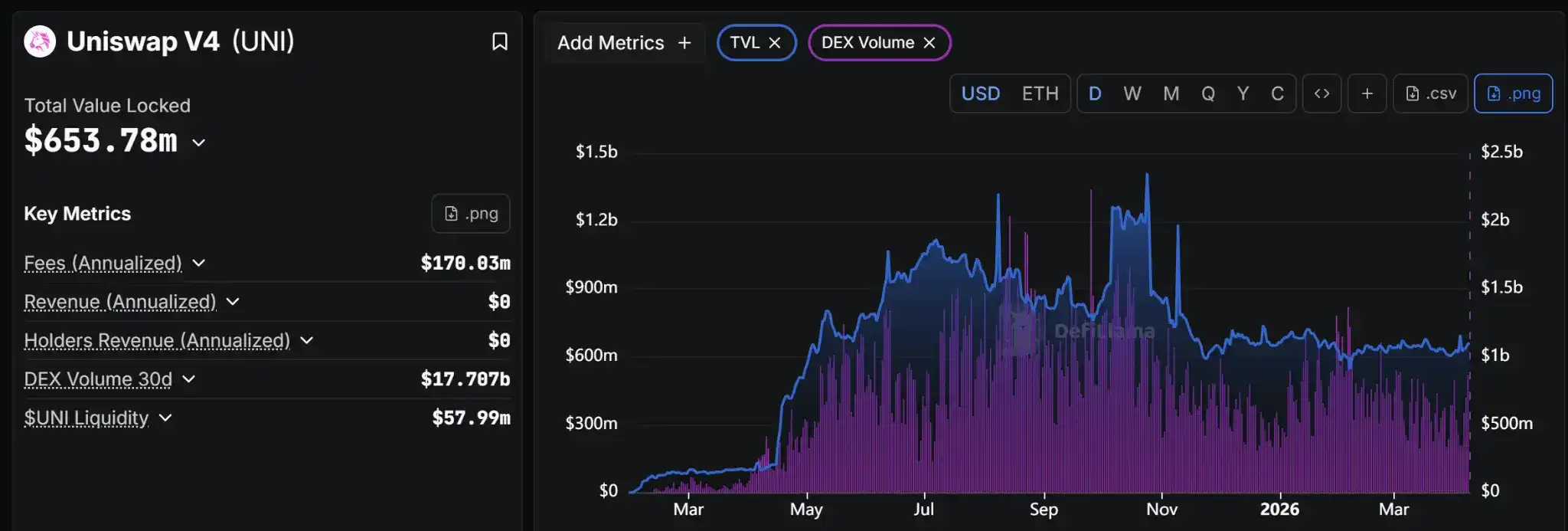

After its launch, the total value locked (TVL) in Uniswap V4 peaked at over $1.2 billion but has since fallen to $650 million, which is still only 40% of the V3 version and also lags behind the V2 version.

Meanwhile, Uniswap has also been "following the rules" in accelerating its expansion in use cases and markets. Over the past six months, Uniswap has launched on blockchains such as Linea, Tempo, X Layer, and Monad to seize market opportunities on emerging chains. On the other hand, Uniswap has been全力 expanding its API partnerships, with recent announcements including adopters like Anchorage Digital, Ledger, Privy, and MetaMask.

Of course, Uniswap has not been without new moves at the product level in recent years. For example, the appchain Unichain and the CCA token auction product have both generated significant market反响.

In February 2025, Uniswap's appchain, Unichain, officially launched on the mainnet, attracting over 90 DeFi protocol integrations. Its TVL peaked at $900 million but has since fallen to $36 million.

At the end of 2025, Uniswap announced the launch of its Continuous Clearing Auction (CCA) function, specifically designed for price discovery and liquidity bootstrapping of new assets, and subsequently partnered with Aztec and Rainbow to complete token sales.

However, it must be pointed out that by 2025, both appchains and token auctions were very "stale" business models in the crypto space. Many projects with stagnant core businesses were exploring "chain issuance" and Launchpad services. Uniswap also "followed suit" and joined this trend, but the practical impact has been very limited.

In earlier years, Uniswap also explored areas like NFT marketplaces and on-chain games through heavy acquisitions of products like Genie and Crypto: The Game. Subsequent data reflected that these were two failed acquisitions.

In the past year, the departures of key personnel such as Growth Lead Sarina Siddhanti, COO Mary Catherine Lader, Head of Strategy & Operations Zach Wong, Chief Legal Officer Katherine Minarik, and Venture Lead Julia Rosenberg also reflect Uniswap's efforts to control operational costs and its struggles with growth.

Uniswap's overall decline is also reflected in the price of its governance token, UNI. Over the past year, the price of UNI fell by over 74% at its worst, dropping below $2 at its lowest point, significantly exceeding the overall decline of mainstream cryptocurrencies. This has sparked criticism from market analysts who call the UNI token "completely worthless."

In September 2025, Arca Chief Investment Officer Jeff Dorman responded to a tweet by Uniswap founder Hayden Adams about the protocol's performance data on X, saying: "We are not bearish on Uniswap, but we are bearish on UNI. In today's market and evolving regulatory environment, it is just a completely meaningless token. Your stance and that of your venture capitalists don't matter. Either switch to a model that distributes revenue or conducts buybacks, or just don't have a token."

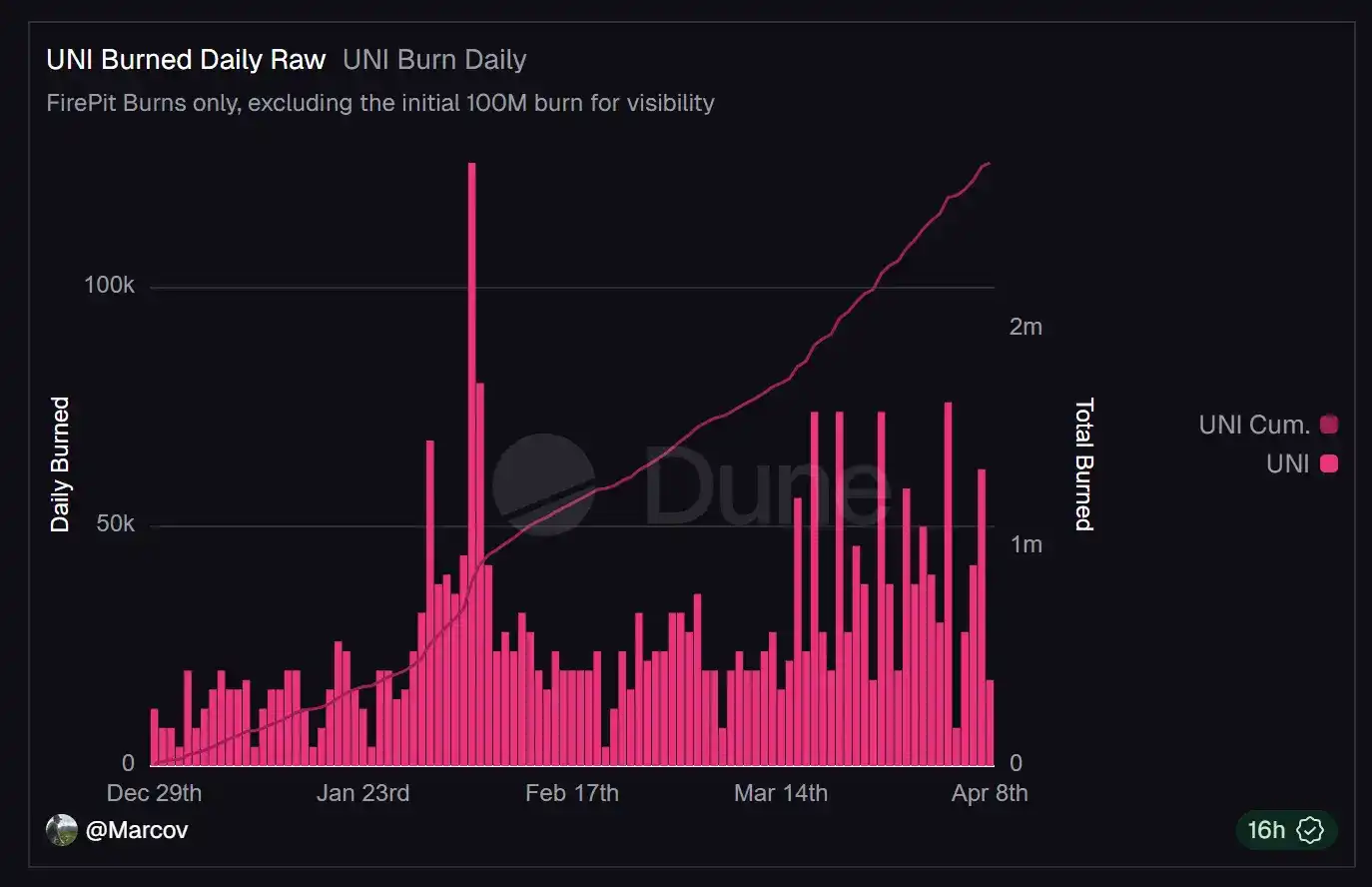

In response to market doubts and to赋予 UNI more value, the Uniswap Foundation proposed in November last year to activate the protocol fee switch for Uniswap V2 and V3 and use the fees to buy back and burn UNI, while also burning 100 million UNI from the treasury. Subsequently, UNI's price surged nearly 38% in a short time, reaching over $9 at its peak.

According to DeFillama data, Uniswap's recent daily fee income ranges between $100,000 and $200,000, with nearly $3.93 million in revenue over the past 30 days. The annualized revenue is approximately $46 million, still lagging behind other DeFi protocols like PancakeSwap, Jupiter, Lido, and Aave.

Uniswap's awkward situation is actually a projection and reflection of the bleak现状 of the DeFi industry: a lack of underlying innovation, exhausted industry narratives, and liquidity being consumed in fragmentation and存量博弈.

However, Uniswap remains one of the very few top DeFi protocols that has not suffered a hack, with no protocol-level fund theft incidents ever occurring. It is also the decentralized exchange protocol with the highest total value locked, and its industry status and user trust remain intact.

But, will there be a Uniswap V5? If so, when will it arrive? Can Uniswap continue to be the engine of the next DeFi Summer?