Written by: Vaidik Mandloi

Compiled by: Luffy, Foresight News

In the 1970s, Bruce Bent and Henry Brown founded the world's first money market fund. The business model was extremely simple: regulations enacted during the Great Depression capped US bank savings deposit rates at just 4.5%, while US Treasury yields exceeded 9% at the same time. However, the minimum entry threshold for individuals to invest in Treasuries was as high as $10,000. The two men came up with the idea of pooling small funds from retail investors, buying Treasuries in bulk, and then distributing the profits back to investors proportionally. Today, the scale of money market funds has reached approximately $8 trillion.

Stablecoins are replicating the same business logic, but this time targeting the underlying asset of private credit—a market with a scale of $2 trillion and a minimum entry threshold of at least one million dollars. Interest-bearing stablecoins channel vast amounts of small funds into the private credit market by pooling them together.

In this article, I will delve into how this is happening, and how Goldfinch collapsed, leaving $56 million of depositor funds trapped in motorcycle loans in Kenya.

How Stablecoins Become Money Market Funds for Private Credit

In the 1990s, the US banking system provided nearly half of debt financing for businesses and residents; today, this proportion is only 20%. After the 2008 financial crisis, new capital regulations were implemented, significantly increasing the cost for banks to hold leveraged loans on their balance sheets. Institutions withdrew from the middle-market credit business en masse, and private credit funds stepped in to fill the market gap.

Asset management institutions like Apollo, Blackstone, and KKR raise funds from pension funds and insurance institutions to lend to companies abandoned by banks. These companies have scarce financing channels, allowing institutions to charge high-risk premiums.

The industry's scale expanded from less than $200 billion in 2008 to over $2 trillion today, with funds almost entirely from institutional investors contributing a minimum of $5 million per investment.

The core reason for the million-dollar minimum investment threshold in private credit is the extremely high cost of post-lending management: each credit requires due diligence, debt restructuring, and continuous tracking over many years. Managing ten institutional LPs, each contributing $50 million, is far easier than managing thousands of retail investors each putting in $500; large-scale operations for retail investors are not even profitable. Over the past decade, only pension funds and insurance institutions have been able to enjoy stable credit returns in the 8%-12% range.

Interest-bearing stablecoins are fundamentally rewriting the industry landscape, just as money market funds opened up Treasury investment channels to ordinary people in the 70s. Underlying risk control and due diligence are still completed by professional institutions like Apollo to institutional standards, but tokenized bridge funds can accept deposits of any amount without threshold, uniformly funneling them into institutional credit strategies, without the need to separately handle a massive number of retail investors.

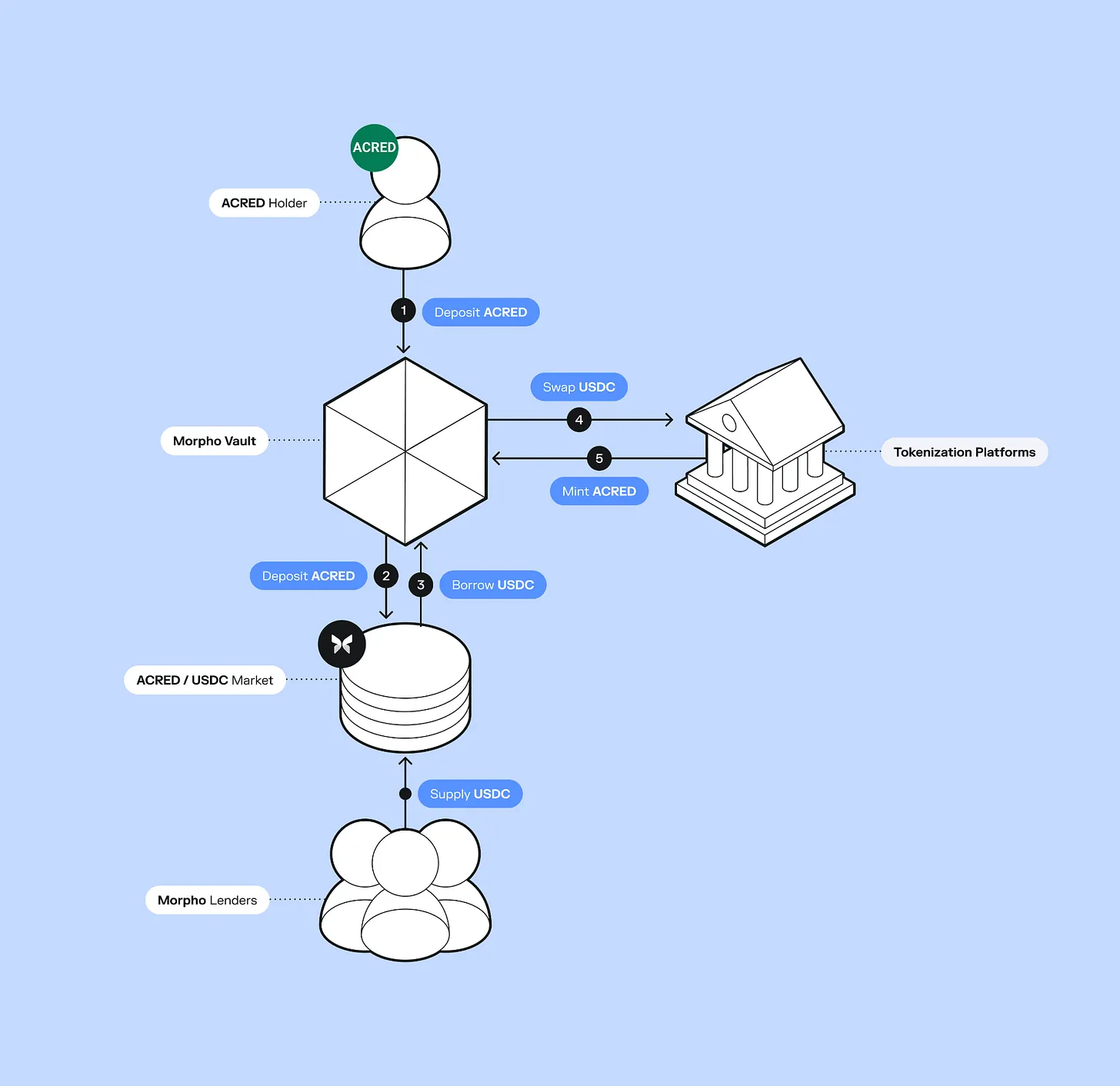

Apollo recently launched the tokenized credit fund ACRED, with $109 million already flowing into its diversified credit products. Investors can even deposit ACRED tokens into Morpho as collateral for borrowing, creating a leveraged loop to amplify returns.

Figure has built a complete on-chain lending infrastructure, with cumulative loan origination volume of $21 billion, listed on NASDAQ, while also issuing the interest-bearing stablecoin YLDS, with a circulating supply of $376 million. Protocols like Pyse and Glow delve into more niche sectors, tokenizing solar projects, allowing investors with just a few hundred dollars to invest in photovoltaic power stations in developing countries, earning annualized returns monthly from electricity fee repayments.

This does not mean the institutional funds themselves have eliminated thresholds; directly subscribing to the ACRED master fund still requires $5 million. But after tokenization, tokens can be traded on secondary markets without thresholds and can be combined with DeFi in a Lego-like manner—a feature traditional fund shares cannot achieve.

Traditional private credit has lock-up periods of several years, with quarterly redemption caps of only 5%; on-chain assets can be traded 24/7 and freely combined. For institutions like Apollo and Figure, this allows them to access the $315 billion stablecoin capital pool, which is actively seeking yield. By tokenizing their funds, they can directly enter this capital pool, opening new distribution channels without building retail infrastructure from scratch.

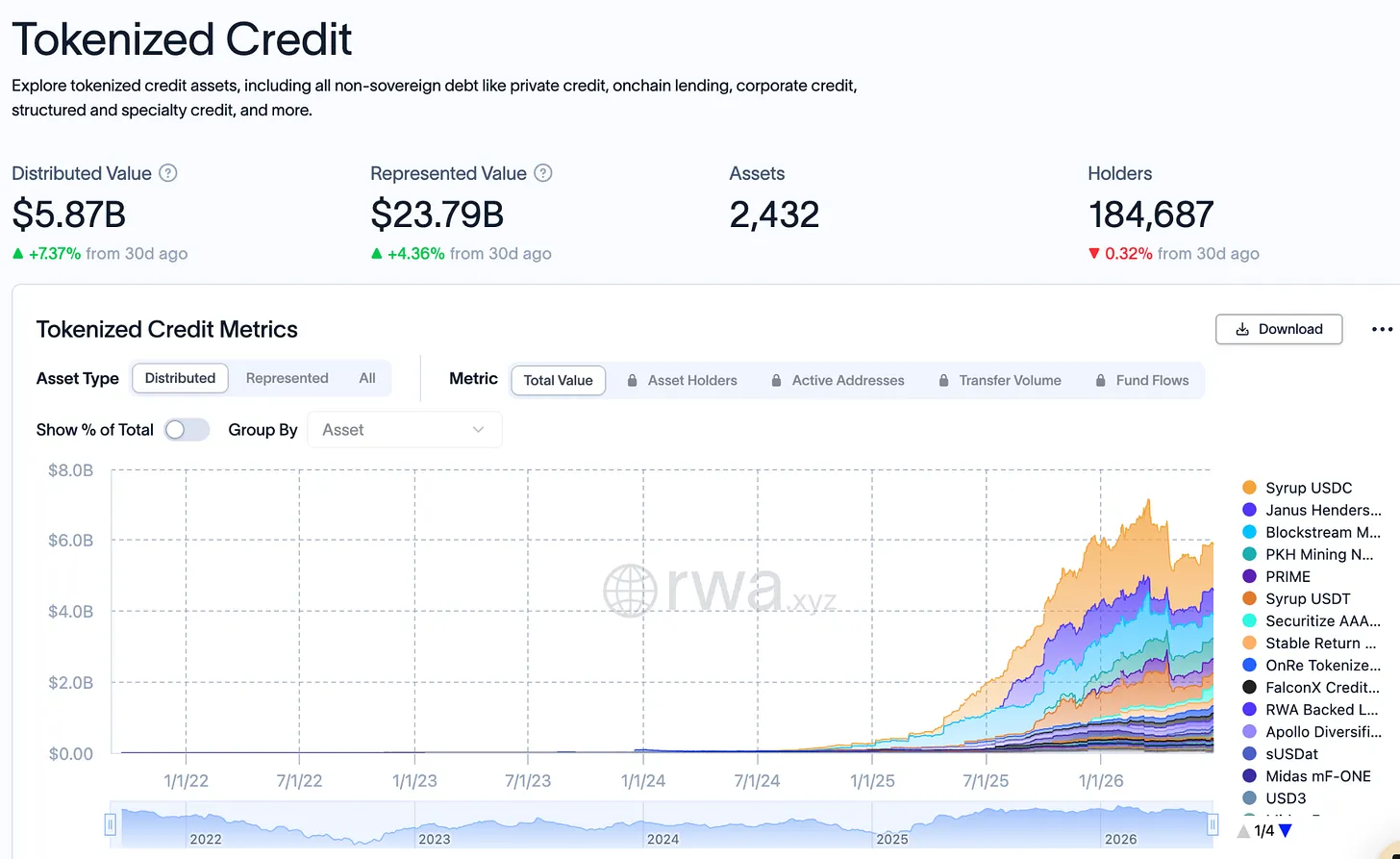

A year ago, the fully on-chain private credit scale was only $400 million; now it has reached $5.87 billion, a 15-fold increase in 12 months. Even so, this scale only accounts for 0.3% of the global $2 trillion private credit market. In Q1 2026, half of the newly issued stablecoins were yield-bearing stablecoins, meaning most new stablecoin capital is actively chasing real credit yields, no longer merely pursuing price pegging to the US dollar.

More critically, each on-chain credit asset can be used as collateral and repeatedly cycled through various DeFi protocols, ultimately generating trading volumes far exceeding the principal amount.

Take ACRED as an example: an investor deposits $10,000 worth of ACRED, borrows 7,000 USDC using it as collateral on Morpho, and then buys more ACRED to pledge again. A $10,000 principal can ultimately leverage over $17,000 in credit exposure. In contrast, with traditional private credit, a $10,000 investment can only be held statically for up to five years, with no amplification potential. The multi-layer cyclical amplification on-chain accelerates market expansion, but risks also propagate simultaneously: a default in any underlying loan will spread losses layer by layer along the leverage chain.

Asset tokenization does not eliminate the inherent risks of the underlying credit. During periods of sustained capital inflows, new deposits can cover redemption demands, masking risks; once capital inflows slow, the contradiction between the promised token yield and the true repayment ability of underlying loans becomes fully exposed. If investors apply for redemptions en masse, market liquidity dries up, causing token prices to severely deviate from the net asset value of the underlying assets.

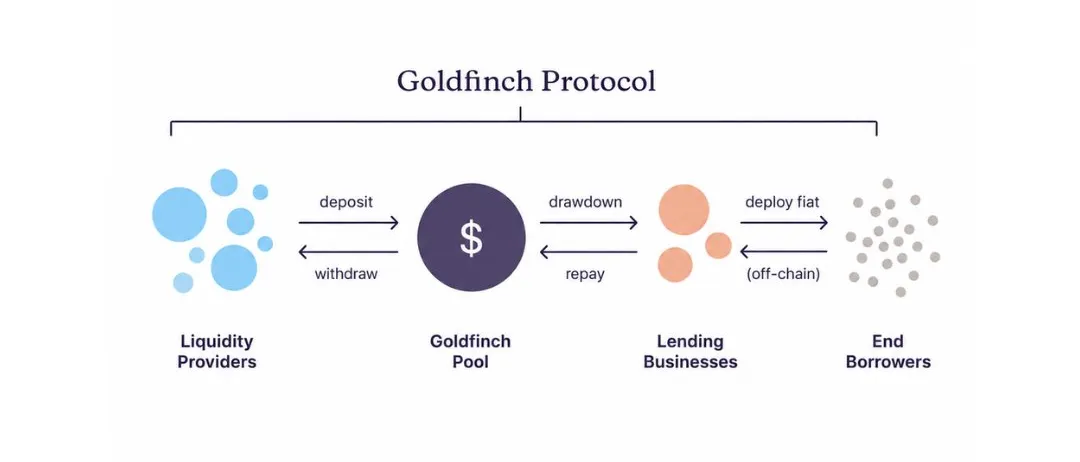

The collapse of Goldfinch is a typical case. The protocol launched in 2021 and was one of the earliest projects to bring private credit on-chain. It was recently forced to shut down, with $56 million of user funds trapped in offline loan businesses in Kenya and Nigeria.

The Fatal Mistakes Made by Goldfinch

In 2021, Goldfinch completed a $25 million funding round led by a16z. At that time, DeFi lending pools offered only 2%-3% APY. The project planned to channel crypto capital to small and micro enterprises in Africa and Southeast Asia. Traditional local banks refused to serve these customer groups, and borrowers were willing to bear high loan interest rates of 15%-25%.

The project's design logic seemed simple: users deposit USDC into a pool, and the smart contract automatically allocates funds to borrowers within seconds. But lending to a motorcycle finance company in Nairobi requires the team to thoroughly understand the local Kenyan transportation industry, conduct on-site verification of corporate finances, and even engage in doorstep collection in case of defaults.

These risk control steps cannot be completed via blockchain at all. After USDC is converted into Kenyan shillings and deployed as credit, depositors cannot track where the funds go, the operational status of the businesses, or confirm whether loan terms are being properly fulfilled. All the core information determining credit quality is stored off-chain, controlled by borrowers in countries most investors have never set foot in.

This also led to a major case of misappropriation being discovered only months after it occurred: in 2022, the local partner Tugende Kenya擅自 (unauthorized) transferred $1.9 million out of a $5 million credit line to a related entity in Uganda. Nearly 40% of the loan funds were moved to an overseas entity not specified in the contract. Meanwhile, depositors continued to receive 10%-12% nominal returns, completely unaware that the underlying funds corresponding to their returns had been improperly transferred.

Traditional private credit institutions would initiate collection and debt restructuring within days of discovering such a serious contract breach. But Goldfinch users could only learn the truth through governance forum posts, and could only initiate governance votes with no legal enforceability, with no power to seize assets or audit remaining credits.

In 2023, Tugende彻底违约、失联 (completely defaulted and lost contact). During its operational period, Goldfinch launched a total of 24 pools with a total size of $113.3 million, with only 13 pools fully repaid. Eight pools hold $53.82 million in outstanding loans, all of which have deviated from the original repayment agreements, mostly entering debt restructuring stages, with single pools receiving less than $51,000 in repayments per month. At this repayment rate, fully recovering the $53.82 million would take 8 to 15 years.

Goldfinch assumed all credit risks inherent to emerging markets, such as currency volatility and lack of credit history, without building the risk control and collection infrastructure that traditional institutions have honed over decades. For example, local Kenyan banks have physical branches and local regulatory connections, possessing sufficient leverage when bad debts arise.

Meanwhile, Goldfinch merely channeled funds from anonymous global wallets to similar high-risk borrowers but lacked a comprehensive offline risk control system, significantly widening the information asymmetry between lenders and borrowers. Once a default occurs, depositors have almost no channels to intervene or manage the situation.

Putting assets on-chain accounts for only about 10% of the workload in a credit business; the remaining 90%—due diligence, collection—heavily relies on localized resources and is extremely costly to build. Credit underwriters need to establish a trustworthy foundation for the entire asset sector. Every bad loan arising from risk control lapses raises the threshold for institutional on-chain cooperation, weakening the credibility of the entire sector.

The true difficulty of the credit business has nothing to do with on-chain technology. If practitioners in this sector fail to see this clearly, they will ultimately only replicate a second Goldfinch-style collapse.