Author: Prathik Desai

Compiled by: Block Unicorn

Preface

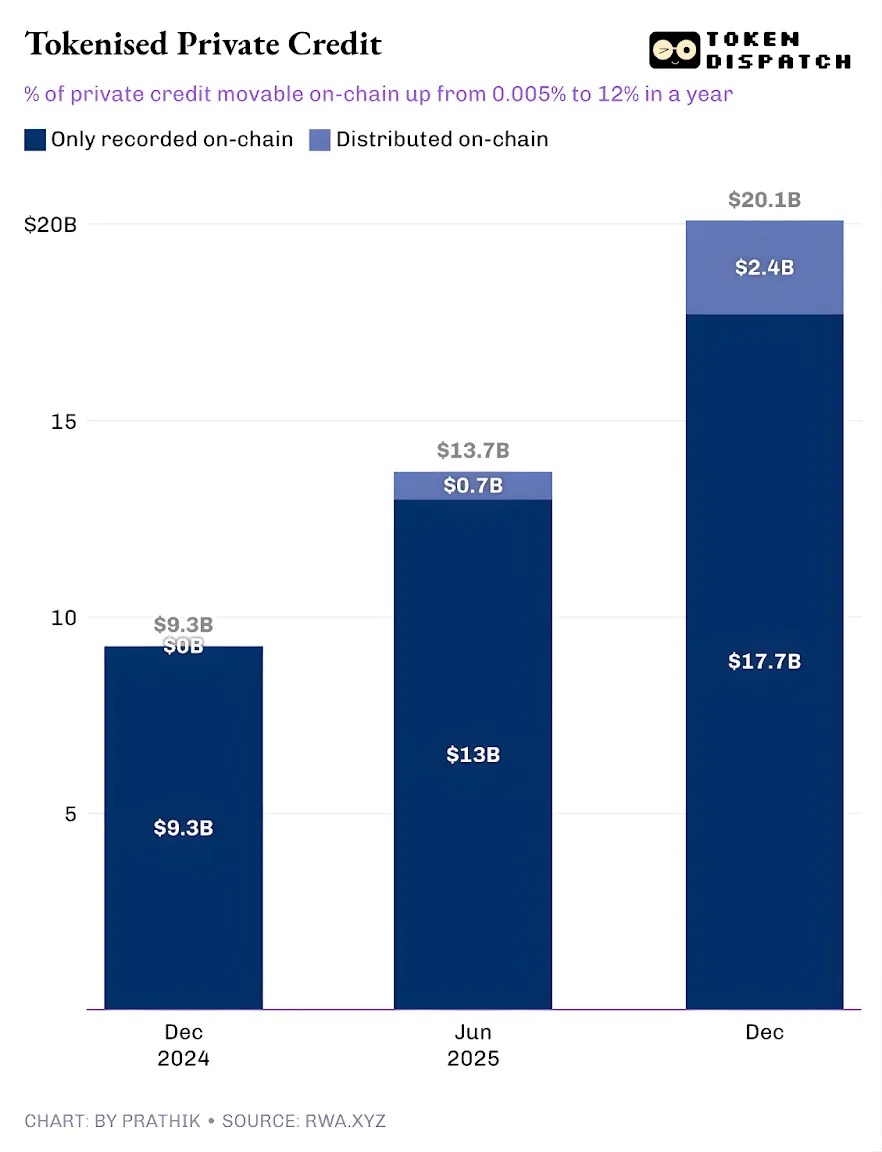

On tokenized real-world asset (RWA) platforms, private credit is at a pivotal moment. Over the past year, tokenized private credit has been the fastest-growing category, surging from less than $50,000 to approximately $2.4 billion.

If stablecoins (whose payment channels cover all on-chain activities) are excluded, tokenized private credit ranks second only to on-chain commodities. Top tokenized commodities include Tether and Paxos's gold-backed currencies, as well as Justoken's tokens backed by cotton, soybean oil, and corn. This appears to be a serious category, with real borrowers, cash flows, underwriting mechanisms, and yields—and it is less dependent on market cycles compared to commodities.

But the story only becomes complex when you dig deeper.

This $2.4 billion in outstanding tokenized private credit represents only a small fraction of the total outstanding loans. This suggests that only a portion of these assets can truly be held and transferred on-chain in tokenized form.

In today's article, I will examine the reality behind the numbers of tokenized private credit and what these numbers mean for the future of this category.

Let's dive right in.

The Dual Nature of Tokenized Private Credit

The total active loans on the RWA.xyz platform are slightly over $19.3 billion. However, only about 12% of these assets can be held and transferred in tokenized form. This highlights the dual nature of tokenized private credit.

One aspect is "representative" tokenized private credit, where the blockchain merely provides operational upgrades by establishing an on-chain ledger of outstanding loans recorded from the traditional private credit market. The other aspect is the distribution upgrade, where blockchain-driven markets coexist with traditional (or off-chain) private credit markets.

The former is used solely for recording and reconciliation, documented on a public ledger. The latter, however, can be transferred to wallets for transactions.

Once you understand this classification system, you won't ask whether private credit is on-chain. Instead, you'll pose a sharper question: How much private credit originates from the blockchain? The answer to this question might offer some insights.

The trajectory of tokenized private credit is encouraging.

Until last year, almost all tokenized private credit was merely an operational upgrade. The loans already existed, borrowers made timely payments, platforms operated normally, and the blockchain simply recorded these activities. All tokenized private credit was only recorded on-chain and could not be transferred as tokens. Within a year, this share of on-chain transferable assets has climbed to 12% of the total trackable private credit.

It showcases the growth of tokenized private credit as a distributable on-chain product. This enables investors to hold fund shares, pool tokens, notes, or structured investment exposures in tokenized form.

If this distributed model continues to expand, private credit will no longer resemble a loan ledger but rather an investable on-chain asset class. This shift will change the benefits lenders derive from transactions. Beyond yields, lenders will gain a tool with greater operational transparency, faster settlement, and more flexible custody. Borrowers will access funding that isn't dependent on a single distribution channel, which could be highly beneficial in risk-averse environments.

But who will drive the growth of the distributable private credit market?

The Figure Effect

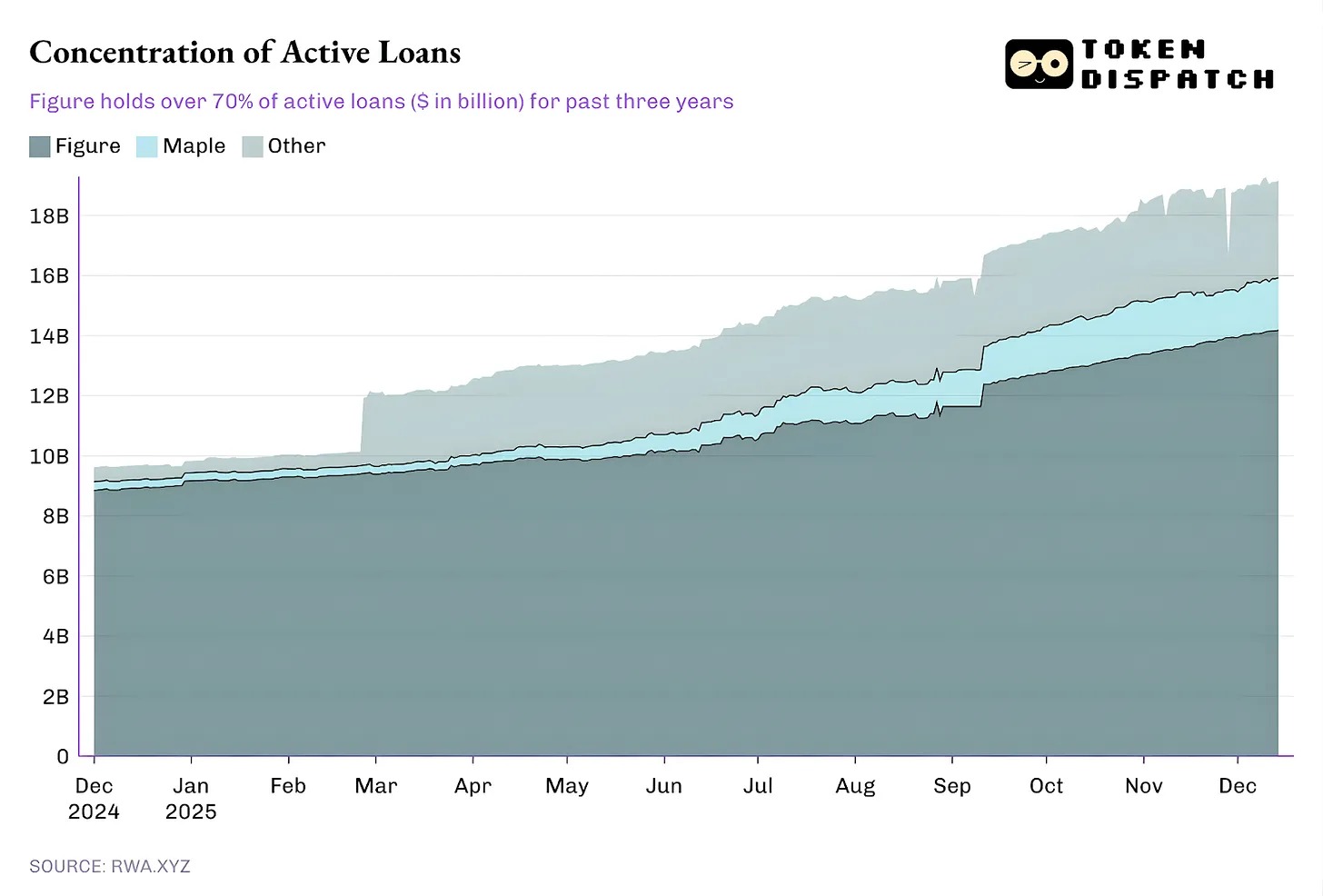

Currently, the majority of outstanding credit comes from a single platform, while the rest of the ecosystem forms a long tail.

Since October 2022, Figure has dominated the tokenized private credit market, but its market share has dropped from over 90% in February to 73% today.

But what's more interesting is Figure's private credit model.

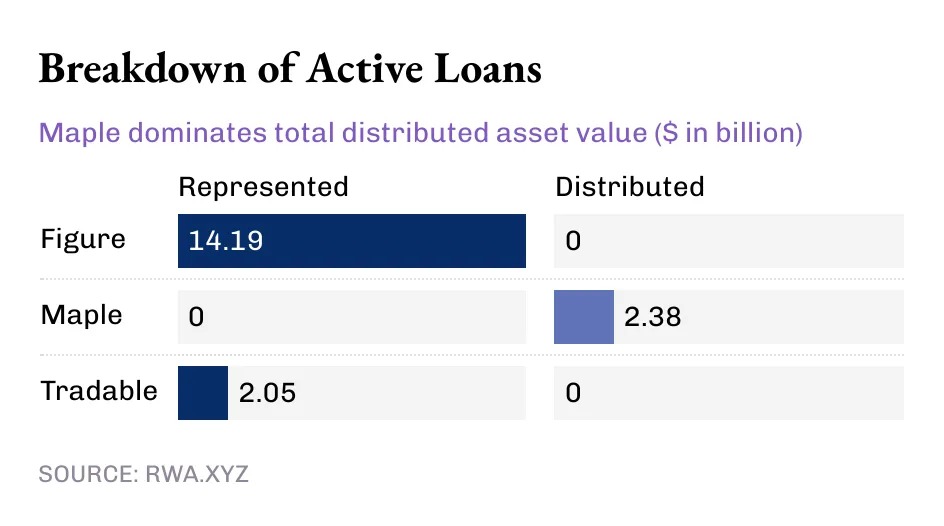

Although tokenized private credit now exceeds $14 billion, all the value of this industry leader is reflected in "representative" asset value, while the distributed value remains zero. This indicates that Figure's model is an operational pipeline that records loan issuance and ownership on the Provenance blockchain.

Meanwhile, some smaller players are driving the distribution of tokenized private credit.

Figure and Tradable hold all their tokenized private credit as representative value, while Maple's value is entirely distributed via the blockchain.

From a macro perspective, the vast majority of the $19 billion in active on-chain loans are recorded on the blockchain. But the trend over the past few months is undeniable: more and more private credit is being distributed via blockchain. Given the immense growth potential of tokenized private credit, this trend will only intensify.

Even at $19 billion, RWAs currently account for less than 2% of the total $1.6 trillion private credit market.

But why is "movable, not just recorded" private credit important?

Movable private credit offers more than just liquidity. Gaining exposure to private credit off-platform through tokens provides portability, standardization, and faster distribution speed.

Assets acquired through traditional private credit channels trap holders within a specific platform's ecosystem. Such ecosystems have limited transfer windows and cumbersome secondary market trading processes. Additionally, secondary market negotiations are slow and primarily led by professionals. This gives existing market infrastructure far more power than asset holders.

Distributable tokens can reduce these frictions by enabling faster settlement, clearer ownership changes, and simpler custody.

More importantly, "movability" is a prerequisite for the large-scale standardized distribution of private credit, which has historically been lacking. In the traditional model, private credit appears in the form of funds, business development companies (BDCs), and collateralized loan obligations (CLOs), each adding multiple layers of intermediaries and opaque fees.

On-chain distribution offers a different path: programmable wrappers enforce compliance (whitelisting), cash flow rules, and information disclosure at the tool level, rather than through manual processes.