Written by: Jack Simison

Compiled by: Chopper, Foresight News

Payments and investments collectively generate $3 trillion in annual revenue, surpassing the total market capitalization of cryptocurrencies. They rely on entirely different user behaviors, completely different underlying infrastructures, and until today, they correspond to entirely different product systems. Here, I want to directly compare these two worlds.

One sector earns money that everyone must pay—payment is a necessity for survival, a rigid demand. The other sector earns money that the majority of people will never choose to invest—investment is a luxury behavior.

Payment and investment management are the two largest revenue-generating areas in financial services. They have long operated within independent systems: different products, different accounts, different regulatory frameworks, and different interfaces. This is both a legacy of historical system architecture and because there was no practical need to integrate payments and investments in the past.

Programmable money is breaking down this barrier. The same balance, stored in the same wallet, blockchain, or application, can now participate in both revenue streams. The two worlds are converging in the form of unified accounts.

To understand why this is important, one must see the huge differences in their underlying behavioral logic.

Payment: A Universal Behavior

Payment is the only necessary financial behavior for participating in daily economic life. Buying food, paying rent, settling utility bills... without payment, one cannot survive.

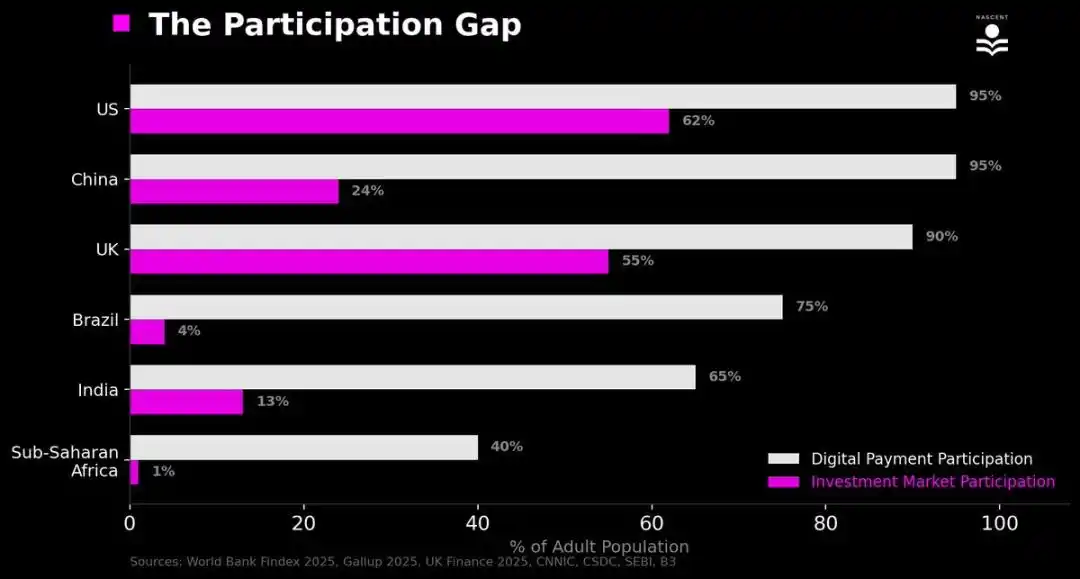

In 2025, about two-thirds of adults globally made or received digital payments. In the United States, consumers complete about 48 payments per month; in India, UPI has over 500 million unique users; in Brazil, Pix has increased the average annual transactions per person to about 193; in parts of sub-Saharan Africa, mobile payments are no longer just a convenient payment method but a core component of the financial system.

Payment is not an optional financial activity for a minority of active people but a daily behavior for the masses. It is instant, high-frequency, with low psychological burden, and the cost is usually negligible. Consumers do not consciously calculate fees at the checkout counter. Compared to cash, digital payments reduce the pain of payment, further increasing usage frequency. The lower the friction, the higher the transaction volume.

This behavioral foundation brings enormous business coverage. According to McKinsey data, the global payment system processes about 3.4–3.6 trillion transactions annually, with an annual fund flow scale of about $1.8–2.0 quadrillion. Salary payments, merchant payments, cross-border remittances, bill payments, subscription services, personal transfers... at every step, intermediaries can take a cut.

Every layer of the payment chain is profiting from it.

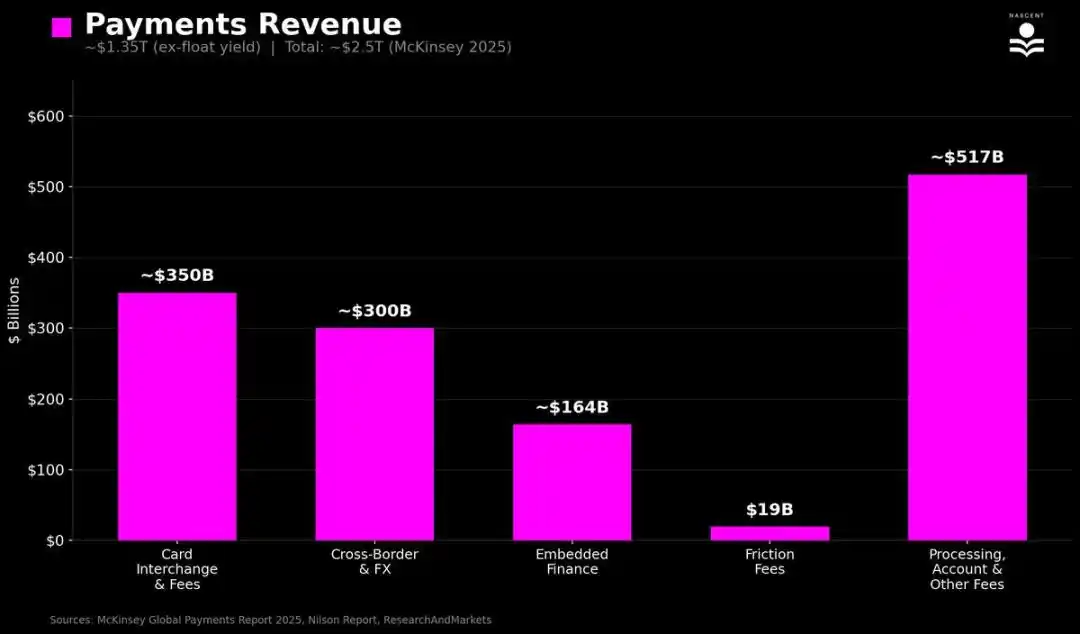

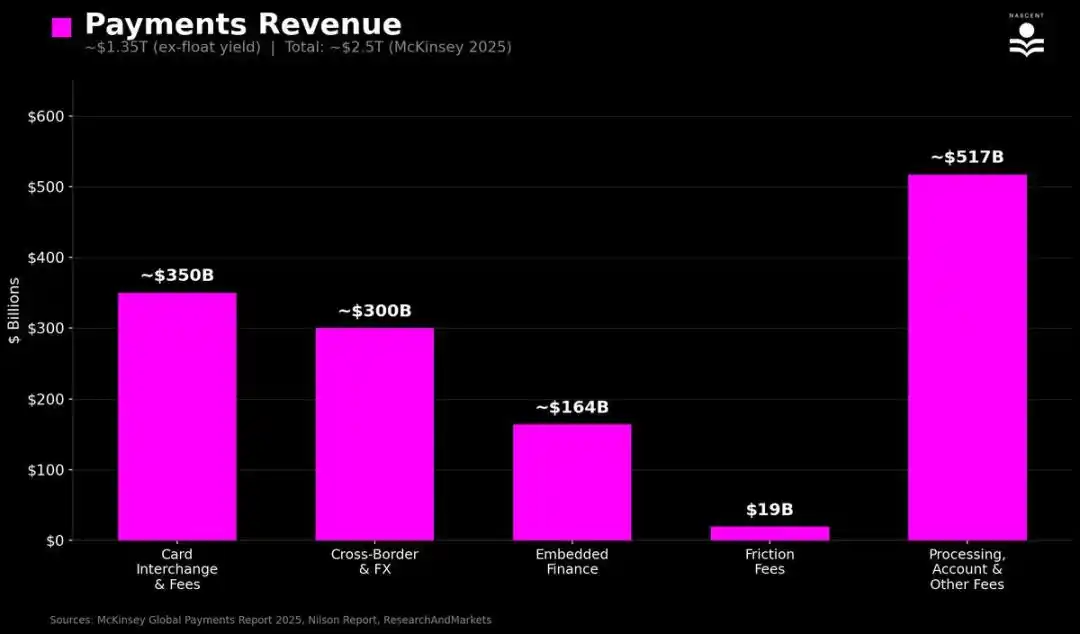

McKinsey's "2025 Global Payments Report" shows that global payment revenue is about $2.5 trillion. But nearly half of that (about $1.15 trillion) is net interest income: the earnings from idle funds in bank and payment accounts during transaction intervals. This is more like idle fund earnings rather than pure payment fees. Excluding this part, the core payment revenue from fund transfers, interchange fees, processing fees, embedded finance (Shopify, installment payments, Stripe), and friction charges (ATMs, overdrafts, on-chain fees) still amounts to about $1.35 trillion.

Investment: A Luxury Behavior

In contrast, investment is a financial behavior that no one is forced to undertake. A person can go through their entire economic life without buying stocks, opening a brokerage account, or consulting a financial advisor. Most people do just that. Active individual traders are statistically a minority.

Unlike payments, investment directly confronts loss aversion and carries a heavy cognitive burden. People instinctively avoid trading, so the funds of ordinary investors mostly lie in pension accounts, investment portfolios, ETFs, and index funds, bought and then held long-term without further action. Among those who participate in investment through pension accounts, 94% do not adjust their plans once joined and almost never trade.

The result is: the behavioral foundation of investment is narrow, passive, but extremely sticky.

The participation rate comparison is telling: even in countries with the highest investment penetration, only about half the population participates in the investment market in some form, while digital payment penetration is as high as 95%.

- United States: About 62% of adults hold some investment, mostly in rarely touched pension accounts

- United Kingdom: Follows closely, about 55%

- China: About 24% of adults have securities accounts

- India: About 13%

- Brazil: 4%

- Sub-Saharan Africa: Only about 1%

Even having an account does not mean active operation.

This leads to a global asset management scale of about $147 trillion managed by professional intermediaries, including ETFs, mutual funds, pensions, and private market funds, accounting for 43% of global household financial wealth (about $305 trillion). The vast majority of this is passive index funds with extremely low fees: stock ETFs average only 14 basis points, bond ETFs 10 basis points. Even so, the global fund industry, managing about $135 trillion in assets, still has annual revenue of about $435 billion.

A minority of assets managed by private equity, venture capital, real estate, and hedge funds (about $13 trillion) charge 1%–2% management fees + 12.5%–20% performance fees, with annual revenue of about $363 billion.

Combining private market advisory fees, hedge fund performance fees, PE/VC carry, securities lending, trading commissions, etc., the total annual revenue of the investment industry is about $850–900 billion.

The overall revenue of the payment industry is still higher than that of investment, but the per capita revenue in the investment industry is much higher than in payments.

The Collapse of the Boundary

This asymmetric pattern has been stable for decades because the two fields have long operated in separate systems with independent infrastructures.

Payment business is scattered among banks, card networks, and payment processors. Asset management business is scattered among fund companies, wealth advisors, and pension platforms, while trading business is handled by brokerage firms.

Even if the same bank offers both checking accounts and investment services, they are packaged and operated as independent products, including separate customer registration, compliance processes, and user experience. The behavioral barrier between "spending money" and "investing" is further reinforced by the system.

The real change is that blockchain infrastructure allows modern payment applications to offer real investment services, and investment applications can offer real payment services, all using the same underlying system.

Investment balances can be directly used for payments without transferring through independent systems. The traditional brokerage process is: deposit funds → buy → sell → transfer to bank → spend. Crypto infrastructure compresses this into one step.

Wallets, neobanks, trading applications, or any programmable balance can allow the same dollar to complete cross-border transfer settlement while earning yield in a lending protocol, or be exchanged for other assets in the same interface, within the same operating session. Account holders can profit from both investment and payment ends simultaneously.

For the first time in history, the same balance, the same interface, can earn returns from both tracks at the same time.